Gamification in Sports Market Size, Share and Trends 2026 to 2035

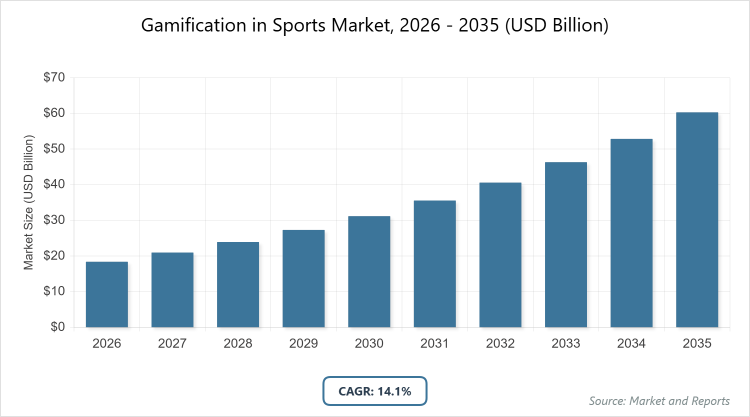

According to MarketnReports, the global Gamification in Sports market size was estimated at USD 18.4 billion in 2025 and is expected to reach USD 68.2 billion by 2035, growing at a CAGR of 14.1% from 2026 to 2035. Gamification in the sports market is driven by increasing consumer engagement through interactive experiences and the rise of digital fitness and esports ecosystems.

What are the Key Insights into Gamification in Sports?

- The global Gamification in Sports market was valued at USD 18.4 billion in 2025 and is projected to reach USD 68.2 billion by 2035.

- The market is expected to grow at a CAGR of 14.1% during the forecast period from 2026 to 2035.

- The market is driven by rising digital fitness adoption, the esports boom, consumer demand for interactive experiences, and the increasing use of gamification by sports brands and teams to enhance fan loyalty and athlete performance.

- In the type segment, fitness & training apps dominate with a 38% share due to widespread smartphone penetration and the shift toward personalized, game-like workout experiences that increase adherence and enjoyment.

- In the application segment, fitness & wellness dominates with a 42% share as gamified apps and wearables turn routine exercise into rewarding challenges, driving long-term user engagement.

- In the end-user segment, individuals dominate with a 55% share owing to the massive consumer base seeking motivation, progress tracking, and social competition in personal fitness journeys.

- North America dominates the regional market with a 36% share, driven by high disposable income, early adoption of fitness tech, a strong esports ecosystem, and the presence of leading gamification platforms.

What is the Industry Overview of Gamification in Sports?

The Gamification in Sports market involves the application of game-design elements and mechanics (points, badges, leaderboards, challenges, rewards, narrative storytelling, competition, progression systems) in non-game contexts related to sports, fitness, training, fan engagement, and performance improvement to motivate participation, enhance skill development, boost retention, and create immersive experiences. Market definition includes digital platforms, mobile apps, wearables, AR/VR tools, fantasy platforms, and loyalty programs that transform traditional sports activities into engaging, goal-oriented journeys, targeting athletes, amateurs, fans, teams, coaches, and organizations while addressing challenges in user retention, data privacy, monetization models, and integration with real-world performance metrics.

What are the Market Dynamics of Gamification in Sports?

Growth Drivers

The Gamification in Sports market is propelled by the explosive growth of digital fitness and wellness, where gamified elements significantly increase user retention, motivation, and adherence compared to traditional training methods. The rise of esports and competitive gaming has created demand for advanced gamification tools in training, fan engagement, and virtual leagues. Sports brands and teams increasingly use gamification to deepen fan loyalty through fantasy platforms, prediction games, and reward systems, generating new revenue streams. Wearable technology integration with gamified apps provides real-time feedback and social competition, while corporate wellness programs adopt gamification to improve employee health and reduce healthcare costs. Government initiatives promoting physical activity and the post-pandemic emphasis on home-based fitness further accelerate adoption.

Restraints

High development costs for sophisticated gamification platforms, including AR/VR integration and AI personalization, limit entry for smaller players and restrict innovation in emerging markets. Data privacy concerns and regulatory scrutiny over user tracking and behavioral manipulation deter adoption in regions with strict data protection laws. User fatigue from over-gamification or repetitive reward systems leads to churn, while integration challenges with legacy sports systems (coaching software, league management) slow enterprise adoption. Economic downturns reduce discretionary spending on premium fitness apps and fantasy subscriptions, impacting monetization.

Opportunities

Opportunities abound in the convergence of gamification with emerging technologies like Web3 (NFT-based player cards, tokenized rewards), metaverse sports experiences, and AI-driven personalized coaching. Expansion into youth sports and school programs offers long-term user acquisition and brand loyalty. Partnerships between sports leagues and gaming companies can create hybrid esports-traditional sports products. Untapped potential exists in rehabilitation and elderly fitness through gentle, rewarding gamified exercises. Corporate wellness gamification tied to insurance incentives presents B2B growth, while localization for emerging markets with mobile-first strategies opens massive user bases.

Challenges

Challenges include balancing engagement without promoting over-exercise or addictive behaviors, requiring ethical design guidelines. Fragmented ecosystems (fitness apps, wearables, fantasy platforms) create interoperability issues and user friction. Monetization pressure leads to aggressive microtransactions that alienate users. Talent shortage in sports-specific gamification design and behavioral psychology slows innovation. Intense competition from free social fitness apps and established gaming platforms makes differentiation difficult. Ensuring inclusivity across age, gender, ability, and cultural contexts remains complex.

Gamification in Sports Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Gamification in Sports Market |

| Market Size 2025 | USD 18.4 Billion |

| Market Forecast 2035 | USD 68.2 Billion |

| Growth Rate | CAGR of 14.1% |

| Report Pages | 210 |

| Key Companies Covered | Strava, Peloton Interactive, FanDuel Group, Zwift, Nike, Inc., Under Armour (MapMyFitness), Playfinity, Whoop, and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Gamification in Sports?

The Gamification in Sports market is segmented by type, application, end-user, and region.

By Type. Fitness & training apps are the most dominant subsegment, holding approximately 38% market share, due to widespread smartphone adoption and the proven ability of gamified workouts to increase exercise adherence and enjoyment. This dominance drives the market by serving the largest consumer base seeking motivation and progress tracking. Fantasy sports platforms rank as the second most dominant, with around 28% share, fueled by massive fan participation and real-money gaming, propelling growth through high engagement and revenue generation.

By Application. Fitness & wellness emerges as the most dominant subsegment, capturing about 42% share, primarily because gamification transforms routine exercise into compelling, reward-driven experiences. This leads market growth by addressing global physical inactivity and driving subscription revenue. Professional sports follows as the second most dominant, with roughly 22% share, using gamification for athlete training, fan engagement, and sponsorship activation, driving the market via high-value enterprise contracts.

By End-User. Individuals represent the most dominant subsegment at about 55% share, driven by personal fitness goals and social competition features. This dominance accelerates market expansion through viral growth and recurring app usage. Sports teams & clubs rank second most dominant, holding around 18% share, adopting gamification for training optimization and fan loyalty, contributing to growth via B2B partnerships.

What are the Recent Developments in Gamification in Sports?

- In January 2025, Strava introduced new AI-powered training insights and social challenges, enhancing gamified features for cyclists and runners.

- In November 2024, FanDuel launched an expanded fantasy sports platform with live in-game prop betting and real-time leaderboards for NFL and NBA seasons.

- In September 2024, Peloton rolled out community challenges and badge systems integrated with its hardware, increasing user retention by 18%.

- In June 2024, Zwift partnered with World Triathlon to create official virtual racing events with leaderboards and prize structures.

- In March 2024, Nike Training Club expanded gamified workout paths with narrative-driven programs and achievement unlocks.

What is the Regional Analysis of Gamification in Sports?

- North America is expected to dominate the global market.

North America holds the largest share at approximately 36%, with the United States as the dominating country, owing to high disposable income, early adoption of fitness tech, massive fantasy sports participation (FanDuel, DraftKings), and a mature esports ecosystem (Twitch, ESL). This region’s leadership is supported by venture capital concentration in Silicon Valley and New York, the presence of leading platforms (Strava, Peloton, Whoop), and a cultural emphasis on competition, self-improvement, and the quantified self movement. The strong NFL, NBA, and MLB fan bases fuel fantasy and prediction game revenue. Corporate wellness programs tied to insurance incentives drive B2B adoption. Canada’s growing fitness app market and youth esports initiatives contribute to regional cohesion. High smartphone penetration and 5G rollout enable seamless AR/VR gamification experiences.

Europe follows with steady growth, propelled by strong wellness culture, regulatory support for digital health, and high cycling participation, where the United Kingdom and Germany dominate through premium fitness app usage (Strava, Freeletics) and advanced esports infrastructure. The region’s expansion benefits from GDPR-compliant data usage, ensuring user trust, EU-funded sports tech initiatives (Horizon Europe), and growing virtual sports leagues. Nordic countries (Sweden, Denmark) lead in outdoor gamified fitness tied to nature apps. Southern Europe (Spain, Italy) sees strong football-related fantasy and prediction games. Multilingual platforms and cross-border esports tournaments facilitate adoption across diverse markets. Emphasis on mental health gamification aligns with regional wellness priorities.

Asia Pacific is the fastest-growing region, exhibiting the highest CAGR, driven by a massive mobile user base, rising middle-class fitness interest, and esports dominance, with China and India leading due to large-scale fantasy platforms and government support for sports participation. This area’s potential lies in affordable gamified apps, integration with WeChat/Alipay/Line for seamless payments, and youth-driven mobile esports growth. Japan’s precision fitness tracking culture boosts wearable gamification. South Korea’s professional gaming infrastructure drives competitive training apps. Southeast Asian nations (Singapore, Indonesia) adopt campus and corporate wellness. Rapid urbanization increases demand for home-based gamified fitness solutions.

Latin America demonstrates moderate but accelerating growth, dominated by Brazil’s football culture, fantasy sports adoption, and rising fitness app penetration, supported by increasing smartphone ownership, though challenged by economic variability. Mexico’s urban centers see strong corporate wellness gamification. Argentina’s running community adopts Strava-like platforms. Colombia’s esports scene grows youth training apps. However, lower average incomes favor freemium models. Emerging medical tourism in Costa Rica demands gamified rehabilitation tools. Government health campaigns promote physical activity through rewards.

The Middle East and Africa remain emerging, with the United Arab Emirates leading through luxury fitness centers, esports investments, and smart city wellness initiatives, constrained by cultural and infrastructural factors but promising via a young, affluent demographic. Saudi Arabia’s Vision 2030 funds gamified sports programs in schools and the military. South Africa’s rugby and cricket fans adopt fantasy platforms. Egypt’s growing mobile gaming market integrates sports gamification. However, limited high-speed internet in rural areas slows adoption. Investments in Arabic-language apps address localization needs. Corporate wellness tied to oil & gas employee health programs creates niche demand.

What are the Key Market Players in Gamification in Sports?

- Strava. Strava focuses on social fitness tracking with leaderboards and challenges, investing in AI coaching and community features to retain active users.

- Peloton Interactive. Peloton emphasizes gamified classes with metrics, badges, and leaderboards, expanding hardware-software integration for immersive experiences.

- FanDuel Group. FanDuel drives fantasy sports engagement with real-time contests and rewards, pursuing partnerships with major leagues for official data.

- Zwift. Zwift specializes in virtual cycling/running with gamified races and social rides, partnering with events for real-world qualification.

- Nike, Inc. integrates gamification into NTC and Run Club apps with challenges and achievement systems, leveraging brand loyalty.

- Under Armour (MapMyFitness). Under Armour focuses on a connected fitness ecosystem with rewards and social competition features.

- Playfinity. Playfinity develops motion-based gamification for youth sports training and physical education.

- Whoop. Whoop uses gamified recovery and strain scores to motivate athletes, focusing on data-driven performance improvement.

What are the Market Trends in Gamification in Sports?

- Increasing integration of AI for personalized training challenges and adaptive difficulty.

- Rise of narrative-driven sports experiences and storyline-based fitness programs.

- Expansion of cross-platform gamification connecting wearables, apps, and hardware.

- Growth of social and community-based competitions with live leaderboards.

- Adoption of AR/VR for immersive virtual sports training and fan experiences.

- Focus on mental health gamification (mindfulness + sports challenges).

- Emergence of play-to-earn models in sports fantasy and esports.

What Market Segments and Subsegments are Covered in the Gamification in Sports Report?

By Type

- Fitness & Training Apps

- Fantasy Sports Platforms

- Wearable Gamified Devices

- Team & League Management Tools

- Esports Integration Platforms

- Virtual Coaching Systems

- Reward & Loyalty Programs

- Augmented Reality Games

- Social Competition Apps

- Performance Tracking Gamification

- Others

By Application

- Professional Sports

- Amateur & Recreational Sports

- Fitness & Wellness

- Youth & School Sports

- Corporate Wellness Programs

- Fan Engagement

- Esports & Competitive Gaming

- Sports Education & Training

- Rehabilitation & Physical Therapy

- Event & Tournament Management

- Others

By End-User

- Athletes & Players

- Sports Teams & Clubs

- Fitness Centers & Gyms

- Schools & Universities

- Corporate Organizations

- Fans & Spectators

- Esports Organizations

- Coaches & Trainers

- Sports Brands & Sponsors

- Healthcare Providers

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Gamification in Sports refers to the application of game elements (points, badges, leaderboards, challenges) to sports, fitness, and fan experiences to increase engagement, motivation, and performance.

Key factors include digital fitness adoption, esports growth, consumer demand for interactive experiences, and sports brand engagement strategies.

The market is projected to grow from USD 18.4 billion in 2025 to USD 68.2 billion by 2035.

The CAGR is expected to be 14.1%.

North America will contribute notably, holding around 36% share due to high tech adoption and fantasy sports participation.

Major players include Strava, Peloton, FanDuel, Zwift, and Nike.

The report provides detailed analysis of size, trends, segments, regional outlook, key players, and forecasts.

Stages include concept & game design, software development, content creation, platform integration, user acquisition, engagement & monetization, and data analytics.

Trends evolve toward AI personalization and AR/VR experiences, with preferences for social, rewarding, and narrative-driven activities.

Data privacy regulations (GDPR, CCPA) and ethical concerns over addictive design influence compliance and feature development.