Artificial Blood Vessels Market Size, Share and Trends 2026 to 2035

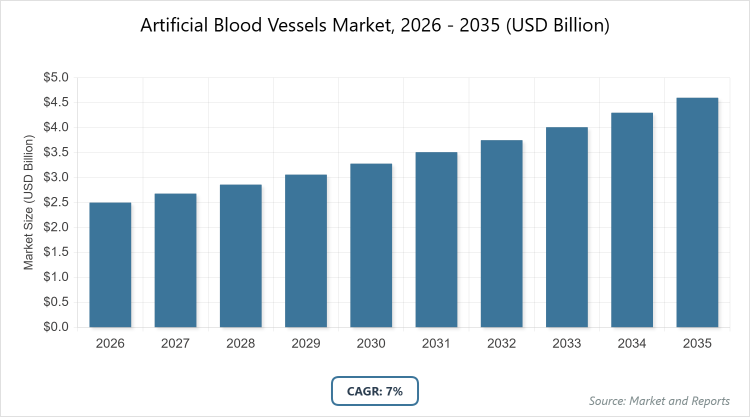

According to MarketnReports, the global Artificial Blood Vessels market size was estimated at USD 2.5 billion in 2025 and is expected to reach USD 5 billion by 2035, growing at a CAGR of 7% from 2026 to 2035. Rising prevalence of cardiovascular diseases, aging populations, and advancements in biomaterials and tissue engineering technologies.

What are the Key Insights in the Artificial Blood Vessels Market?

- The global Artificial Blood Vessels market was valued at USD 2.5 billion in 2025 and is projected to reach USD 5 billion by 2035.

- The market is expected to grow at a CAGR of 7% during the forecast period 2026-2035.

- The market is driven by increasing cardiovascular disease burden, growing demand for minimally invasive vascular procedures, and progress in biocompatible and tissue-engineered grafts.

- Polyethylene Terephthalate holds the dominant share among polymer types (approximately 40%) due to its proven biostability, durability, and widespread clinical adoption in large-diameter grafts.

- Aortic Disease dominates applications (around 42%) because of the high incidence of aneurysms and dissections requiring urgent intervention with reliable large-vessel replacements.

- Hospitals lead end-user segments (over 55%) owing to high-volume surgical procedures and access to advanced infrastructure for complex vascular repairs.

- North America dominates regionally (approximately 42%) due to advanced healthcare systems, high cardiovascular disease rates, and strong regulatory support for innovative grafts.

What defines the Artificial Blood Vessels Market?

Industry Overview

The Artificial Blood Vessels Market refers to synthetic or bioengineered conduits designed to replace or bypass damaged or diseased natural blood vessels, primarily in cardiovascular and vascular procedures. These include polymer-based grafts (such as polyethylene terephthalate and expanded polytetrafluoroethylene), tissue-engineered vessels, and hybrid composites that mimic native vessel properties for improved patency, biocompatibility, and reduced thrombosis. The market supports critical applications like aortic aneurysm repair, peripheral revascularization, hemodialysis access, and coronary bypass, addressing the limitations of autologous vein grafts such as availability and harvest morbidity. It integrates innovations in 3D bioprinting, regenerative medicine, and smart materials to enhance long-term outcomes and patient safety in vascular surgery.

What are the Market Dynamics in the Artificial Blood Vessels Market?

Growth Drivers

The market growth is fueled by the escalating global burden of cardiovascular diseases, including aortic aneurysms, peripheral artery disease, and end-stage renal failure requiring hemodialysis access. An aging population increases the need for vascular interventions, while technological advancements in biomaterials—such as improved endothelialization and antithrombotic coatings—enhance graft performance and longevity. Rising adoption of minimally invasive endovascular techniques, coupled with investments in tissue-engineered and 3D-printed vessels, reduces complications and supports broader clinical use. Government initiatives and funding for regenerative medicine further accelerate innovation and market penetration.

Restraints

High development and manufacturing costs for advanced tissue-engineered grafts limit accessibility, particularly in low-resource settings. Long-term patency issues, such as thrombosis, infection, and intimal hyperplasia, remain challenges for synthetic grafts, leading to revisions or failures. Stringent regulatory approvals for novel bioengineered products delay commercialization, while the limited availability of large-scale clinical data on newer materials restrains physician adoption. Competition from autologous grafts and emerging alternatives like xenografts adds pressure.

Opportunities

Opportunities abound in tissue-engineered and biohybrid vessels that promote regeneration and reduce rejection risks, particularly for pediatric and small-diameter applications. Emerging markets in Asia Pacific offer growth through rising healthcare expenditure, increasing vascular disease prevalence, and local manufacturing expansions. Integration of AI for personalized graft design, smart sensors for monitoring, and 3D bioprinting for custom solutions present avenues for differentiation. Partnerships between biotech firms and medical device companies can accelerate innovation and market entry.

Challenges

Challenges include achieving consistent long-term patency comparable to native vessels, especially in small-diameter applications where thrombosis is prevalent. Microbial resistance and infection risks in implanted grafts require ongoing material improvements. Supply chain vulnerabilities for specialized biomaterials, varying global regulatory standards, and high R&D costs for clinical validation pose barriers. Educating surgeons on new technologies and managing reimbursement issues in different healthcare systems further complicate adoption.

Artificial Blood Vessels Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Artificial Blood Vessels Market |

| Market Size 2025 | USD 2.5 Billion |

| Market Forecast 2035 | USD 5 Billion |

| Growth Rate | CAGR of 7% |

| Report Pages | 220 |

| Key Companies Covered |

B. Braun Melsungen AG, Medtronic plc, Terumo Medical Corporation, W. L. Gore & Associates, Humacyte Inc., LeMaitre Vascular Inc., and Others |

| Segments Covered | By Polymer Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Artificial Blood Vessels Market Segmented?

The Artificial Blood Vessels market is segmented by polymer type, application, end-user, and region.

Based on Polymer Type Segment, Polyethylene Terephthalate is the most dominant segment due to its excellent biostability, mechanical strength, and established track record in large-diameter grafts for aortic and peripheral applications, driving market growth through reliable performance in high-stakes surgeries. The second most dominant is Expanded Polytetrafluoroethylene, preferred for its low thrombogenicity and flexibility in medium-diameter uses like hemodialysis and peripheral bypass, contributing to growth by addressing patency needs in chronic vascular access.

Based on Application Segment, Aortic Disease is the most dominant segment as it involves life-threatening conditions like aneurysms requiring durable large-vessel replacements, supporting market expansion through urgent procedural volumes and advanced imaging integration. The second most dominant is Hemodialysis, driven by the growing end-stage renal disease population needing reliable arteriovenous access grafts, fueling demand via increasing dialysis treatments globally.

Based on the End-User Segment, Hospitals are the most dominant segment due to centralized facilities equipped for complex vascular surgeries, advanced monitoring, and multidisciplinary teams, propelling growth through high procedural throughput and innovation adoption. The second most dominant is Ambulatory Surgical Centers, benefiting from cost-efficiency and shorter recovery for elective peripheral procedures, driving market expansion as outpatient care rises.

What Recent Developments have occurred in the Artificial Blood Vessels Market?

- In December 2024, the FDA approved Humacyte’s SYMVESS, the first acellular tissue-engineered vascular conduit for extremity arterial trauma repair when autologous veins are unavailable, marking a milestone in bioengineered grafts.

- Terumo Corporation expanded its vascular access manufacturing capacity in Puerto Rico with a USD 30 million investment in February 2024, enhancing production of guidewires and related vascular products.

- PECA Labs received CE Mark approval in March 2024 for its exGraft, a growth-accommodating conduit designed for pediatric vascular applications.

- University of Sydney researchers developed 3D-printed glass-based artificial blood vessels in November 2025, replicating native fluid dynamics to advance stroke research and potential clinical translation.

- Jiangsu Bioda Life Science Co., Ltd. obtained class III medical device approval in November 2022 for its artificial blood vessel,l indicated for aortic conditions, supporting expansion in Asia Pacific markets.

Which Region Dominates the Artificial Blood Vessels Market?

- North America is expected to dominate the global market.

North America dominates the Artificial Blood Vessels market primarily due to high prevalence of cardiovascular diseases, advanced healthcare infrastructure, substantial R&D investments, and favorable reimbursement for innovative grafts; the United States leads with major players, extensive clinical trials, and strong FDA pathways for approvals.

Europe holds a significant share supported by robust regulatory frameworks, aging populations driving vascular interventions, and a focus on minimally invasive techniques across Germany, the UK, and France.

Asia Pacific is the fastest-growing region, fueled by rising cardiovascular incidence, improving healthcare access, increasing investments in medical technology, and local manufacturing in countries like China, India, and Japan.

Latin America and the Middle East & Africa show emerging potential through growing awareness, infrastructure development, and partnerships, though limited by economic constraints and regulatory variations.

Who are the Key Market Players in the Artificial Blood Vessels Market?

- B. Braun Melsungen AG focuses on polymer-based grafts and minimally invasive solutions, with strategies emphasizing R&D in biocompatible materials and global distribution expansions.

- Medtronic plc invests in advanced synthetic and drug-eluting grafts, leveraging acquisitions and partnerships to enhance its portfolio for aortic and peripheral applications.

- Terumo Medical Corporation prioritizes hydrophilic-coated and guidewire-integrated products, employing manufacturing expansions and regulatory approvals to strengthen vascular access offerings.

- W. L. Gore & Associates develops ePTFE-based grafts with innovative coatings, focusing on long-term patency and clinical evidence to maintain leadership in hemodialysis and aortic segments.

- Humacyte Inc. specializes in bioengineered acellular vessels, with strategies centered on FDA approvals, clinical trials, and commercialization for trauma and dialysis access.

- LeMaitre Vascular Inc. targets niche vascular applications with biologic and synthetic grafts, utilizing acquisitions and direct sales networks for growth in peripheral and hemodialysis markets.

What are the Market Trends in the Artificial Blood Vessels Market?

- Increasing adoption of tissue-engineered and biohybrid grafts for better integration and reduced complications.

- Rise in 3D bioprinting and personalized vessel design using AI and digital twins.

- Growth in smart sensor-enabled grafts for real-time monitoring of patency and flow.

- Expansion of minimally invasive endovascular procedures is boosting demand for flexible grafts.

- Focus on absorbable and biodegradable polymers for pediatric and temporary applications.

- Enhanced emphasis on antimicrobial coatings to prevent graft infections.

What Market Segments and Subsegments are Covered in the Report?

By Polymer Type

- Polyethylene Terephthalate

- Expanded Polytetrafluoroethylene

- Polyurethane

- Polydioxanone

- Biosynthetic/Tissue-Engineered

- Others

By Application

- Aortic Disease

- Peripheral Artery Disease

- Hemodialysis

- Coronary Artery Bypass Grafting

- Traumatic Vascular Injury

- Pediatric Congenital Vessel Repair

- Others

By End-User

- Hospitals

- Ambulatory Surgical Centers

- Cardiac Catheterization Laboratories

- Specialty Clinics

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Artificial Blood Vessels Market - Industry Analysis

Chapter 4. Global Artificial Blood Vessels Market- Competitive Landscape

Chapter 5. Global Artificial Blood Vessels Market - Polymer Type Analysis

Chapter 6. Global Artificial Blood Vessels Market - Application Analysis

Chapter 7. Global Artificial Blood Vessels Market - End-User Analysis

Chapter 8. Artificial Blood Vessels Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Artificial blood vessels are synthetic or bioengineered tubes used to replace or bypass damaged natural blood vessels in cardiovascular and vascular surgeries, providing structural support and blood flow.

Key factors include rising cardiovascular diseases, aging demographics, advancements in biomaterials and tissue engineering, increasing minimally invasive procedures, and investments in regenerative medicine.

The market is projected to grow from USD 2.5 billion in 2025 to USD 5 billion by 2035.

The market is expected to grow at a CAGR of 7% during 2026-2035.

North America will contribute notably due to its dominant share from advanced infrastructure and high disease prevalence.

Major players include B. Braun Melsungen AG, Medtronic plc, Terumo Medical Corporation, W. L. Gore & Associates, Humacyte Inc., and LeMaitre Vascular Inc..

The report delivers in-depth analysis of market size, growth trends, segmentation, dynamics, regional insights, key players, and forecasts to support strategic decision-making.

Stages include raw material sourcing (polymers and biologics), R&D and graft fabrication, regulatory approval and clinical testing, manufacturing and sterilization, distribution to healthcare facilities, and implantation with post-market surveillance.

Trends are shifting toward bioengineered and personalized grafts with regenerative properties, reduced thrombogenicity, and smart monitoring capabilities to improve long-term outcomes.

Regulatory factors include stringent FDA and EU approvals for safety and efficacy; environmental factors involve sustainable biomaterials and reduced waste in manufacturing to meet green healthcare standards.