Faba Beans Market Size, Share and Trends 2026 to 2035

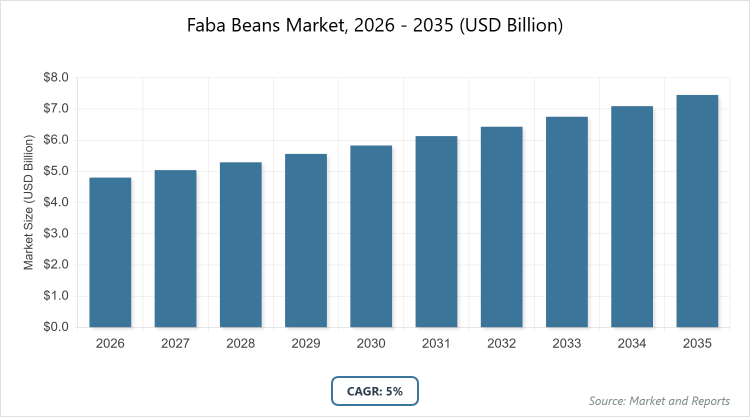

According to MarketnReports, the global Faba Beans market size was estimated at USD 4.8 billion in 2025 and is expected to reach USD 7.8 billion by 2035, growing at a CAGR of 5.0% from 2026 to 2035. Faba Beans Market is driven by increasing demand for plant-based proteins.

What are the Key Insights into the Faba Beans Market?

- The global Faba Beans market was valued at USD 4.8 billion in 2025 and is projected to reach USD 7.8 billion by 2035.

- The market is anticipated to grow at a CAGR of 5.0% during the forecast period from 2026 to 2035.

- The Faba Beans market is driven by rising demand for plant-based proteins, health-conscious consumer preferences, and sustainable agricultural practices.

- In the type segment, whole Faba beans dominate with a 40% share due to their versatility in culinary applications, long shelf life facilitating global trade, and traditional use in diets worldwide; Faba bean flour is the second dominant with 20% share as it gains traction in gluten-free baking and processed foods, helping drive the market through innovation in functional ingredients.

- In the application segment, food and beverages dominate with a 60% share owing to increasing incorporation in snacks, bakery items, and plant-based meats amid vegan trends; animal feed is the second dominant with 25% share, contributing to market growth by providing a cost-effective, nutrient-dense alternative to imported soy.

- In the end-user segment, food processing companies dominate with a 50% share because of large-scale demand for processed Faba bean products in ready-to-eat foods and alternatives; households are the second dominant with 20% share, boosting the market through retail consumption driven by health awareness.

- Asia Pacific dominates the global Faba Beans market with a 40% share due to high production volumes in countries like China and strong traditional consumption in regional cuisines, supported by government initiatives for pulse cultivation.

What is the Faba Beans Market Industry Overview?

The Faba Beans market encompasses the global production, distribution, and consumption of Faba beans, also known as broad beans or Vicia faba, which are nutrient-rich legumes valued for their high protein, fiber, and mineral content. This market includes various forms such as whole beans, processed products like flour and protein isolates, and applications spanning food, feed, and industrial uses. It involves agricultural cultivation in diverse climates, processing into value-added items, and trade across regions, driven by their role in sustainable farming as nitrogen-fixing crops that enhance soil health without heavy reliance on synthetic fertilizers. The market definition covers the entire value chain from farming and harvesting to end-use in human nutrition, animal feed, and emerging sectors like plant-based alternatives, excluding unrelated legumes like soybeans or chickpeas.

What are the Dynamics in the Faba Beans Market?

Growth Drivers

The primary growth drivers in the Faba Beans market include the surging global demand for plant-based proteins, as consumers increasingly adopt vegan, vegetarian, and flexitarian diets due to health, ethical, and environmental concerns. Faba beans, offering a complete protein profile with essential amino acids, fiber, vitamins, and minerals, serve as an ideal substitute in meat alternatives, snacks, and functional foods, with innovations like protein isolates enhancing their appeal in sports nutrition and dairy-free products. Additionally, sustainable farming practices propel the market, as Faba beans act as nitrogen-fixing crops that improve soil fertility, reduce fertilizer needs, and support crop rotation, aligning with eco-friendly agriculture trends amid climate change pressures. Technological advancements in breeding disease-resistant varieties and efficient processing techniques further boost yields and product quality, enabling expansion into new markets and applications such as aquafeed and biofuels, while rising disposable incomes in emerging economies like India and China shift preferences toward nutrient-dense, affordable legumes.

Restraints

Key restraints hindering the Faba Beans market growth encompass intense competition from alternative legumes and proteins, such as chickpeas, lentils, peas, and soybeans, which often have established supply chains, lower prices, and broader consumer familiarity, capturing over 60% of the plant-based protein share and limiting Faba beans’ penetration without targeted marketing of their unique benefits like superior fiber content. Agronomic challenges pose significant barriers, including vulnerability to diseases like chocolate spot and rust, sensitivity to climatic conditions requiring specific temperatures and moisture levels, and impacts from unpredictable weather patterns due to climate change, which increase production costs and reduce yields in key growing regions. Moreover, limited consumer awareness in non-traditional markets, coupled with health concerns like potential allergenicity or risks for individuals with G6PD deficiency causing favism, necessitates education efforts and could slow adoption, particularly in developing regions where supply chain inefficiencies further exacerbate availability issues.

Opportunities

Opportunities in the Faba Beans market are abundant, particularly in the expansion of value-added products like gluten-free flours, protein concentrates, and isolates for niche sectors such as infant nutrition, functional foods, and biodegradable materials, capitalizing on the rising prevalence of gluten intolerance and demand for non-GMO, allergen-friendly ingredients that can command premium pricing. The growing role in animal feed and aquafeed presents lucrative prospects, as Faba beans offer a sustainable, cost-effective alternative to soybean meal with comparable amino acid profiles, enabling cost reductions of up to 15% in livestock and fish farming while addressing import dependencies in regions like Europe. Emerging markets in the Middle East and Africa provide untapped potential through government investments in agro-modernization, food security initiatives, and population growth driving demand for nutrient-rich staples, with innovations in organic cultivation and online distribution channels facilitating broader accessibility and market diversification.

Challenges

Challenges facing the Faba Beans market include supply chain vulnerabilities stemming from seasonal production cycles and regional concentration of cultivation, leading to price volatility and availability constraints that affect consistent supply to processors and end-users, especially during off-seasons or amid global trade disruptions. Developing resilient varieties requires substantial investment in research to combat pests, diseases, and climate variability, yet funding gaps in smaller producing countries hinder progress and limit scalability. Additionally, regulatory hurdles related to food safety standards, anti-nutritional factors in raw beans, and environmental compliance for sustainable claims add complexity to market entry and expansion, while shifting consumer preferences toward ultra-processed alternatives demand continuous innovation to maintain relevance.

Faba Beans Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Faba Beans Market |

| Market Size 2025 | USD 4.8 Billion |

| Market Forecast 2035 | USD 7.8 Billion |

| Growth Rate | CAGR of 5.0% |

| Report Pages | 220 |

| Key Companies Covered |

AGT Food and Ingredients Inc., Archer Daniels Midland Company (ADM), Cargill Incorporated, Roquette Frères, The Scoular Company, Prairie Fava Ltd., and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Segmentation of the Faba Beans Market?

The Faba Beans market is segmented by type, application, end-user, and region.

Based on Type Segment. The most dominant subsegment is whole Faba beans, holding a 40% share, due to their widespread use in traditional cuisines, ease of storage and transportation enabling global exports, and nutritional versatility as a direct protein source; this dominance drives the market by supporting bulk trade and serving as a base for further processing into value-added items. The second most dominant is Faba bean flour with 20% share, prominent for its role in gluten-free and fortified products amid rising health trends, contributing to market growth through innovation in bakery and snack formulations that appeal to health-conscious consumers.

Based on Application Segment. Food and beverages dominate with a 60% share, driven by increasing integration into plant-based meats, snacks, and beverages owing to Faba beans’ neutral flavor and high protein content; this leads market expansion by aligning with vegan trends and enabling product diversification in processed foods. Animal feed is the second dominant at 25%, valued for its cost-effective nutrient profile as a soy alternative, helping propel the market through sustainable feed solutions that reduce environmental impact in livestock industries.

Based on End-User Segment. Food processing companies lead with 50% share, as they utilize large volumes for manufacturing ready-to-eat products and alternatives, fueled by demand for clean-label ingredients; this drives overall market growth via scaled production and innovation in functional foods. Households rank second with 20% share, supported by retail availability and awareness of health benefits, contributing to the market by boosting direct consumption through home cooking and dietary shifts.

What are the Recent Developments in the Faba Beans Market?

- In May 2024, Roquette Frères launched NUTRALYS Fava S900M, a new fava bean protein isolate for European and North American markets, emphasizing clean flavor and sustainability to cater to plant-based food demands, marking a step toward broader adoption in dairy alternatives and snacks.

- In January 2024, the U.S. Department of Agriculture granted $2.7 million to researchers for developing fava beans as a sustainable crop in the mid-Atlantic region, focusing on climate-resilient varieties to enhance domestic production and reduce import reliance.

- In May 2023, the French government initiated the AlinOVeg project, partnering with agricultural organizations to boost domestic fava bean protein production, aiming to strengthen local supply chains and support vegan protein alternatives.

- In July 2024, Australia’s Wide Open Agriculture Limited announced advancements in producing high-quality protein isolates from fava beans using proprietary technology, targeting export markets and plant-based meat sectors.

What is the Regional Analysis of the Faba Beans Market?

Asia Pacific to dominate the global market.

Asia Pacific holds the largest share at 40%, with China as the dominating country due to its position as the world’s top producer and consumer, yielding vast quantities in regions like Yunnan and Sichuan for traditional dishes and food processing; this dominance stems from government support for pulse farming, rising population-driven protein needs, and established supply chains that facilitate exports and domestic use, contributing significantly to global market stability.

Europe accounts for a substantial portion, with France leading as the dominating country through initiatives like a 15% increase in fava bean agriculture in 2023 via ministry programs, driven by demand for organic and vegan products, efforts to reduce soybean imports, and collaborations for protein development; the region’s focus on sustainable farming and innovation in plant-based foods bolsters its growth.

North America represents a growing market, dominated by Canada with over 200,000 metric tonnes produced in 2023 for food and feed, fueled by plant-based diet shifts, gluten-free trends, and government-backed sustainable practices; the U.S. complements this with expanding cultivation and distribution through supermarkets and online channels.

Latin America shows potential, with Brazil as the key country emerging through investments in legume crops for food security, though smaller in scale; growth is supported by favorable climates and increasing exports to meet global demand for affordable proteins.

The Middle East and Africa is the fastest-growing, led by Egypt with annual imports of 500,000-550,000 tonnes and an 18% production rise via improved varieties; this is propelled by food security concerns, population growth, and agro-modernization to provide nutrient-rich staples sustainably.

Who are the Key Players in the Faba Beans Market?

- AGT Food and Ingredients Inc. AGT Food and Ingredients Inc., a leading Canadian company, focuses on pulse processing and export, with strategies including investments in sustainable sourcing, product innovation like fava bean flours for gluten-free markets, and partnerships with growers to ensure supply chain resilience, enabling expansion into North American and European plant-based sectors.

- Archer Daniels Midland Company (ADM). ADM, a global agribusiness giant, employs strategies such as R&D in protein extraction technologies for fava bean isolates, strategic acquisitions to broaden its plant-based portfolio, and emphasis on eco-friendly farming to meet demand for functional ingredients in food and feed applications.

- Cargill Incorporated. Cargill leverages its extensive supply network for fava beans, with strategies centered on collaborative research for disease-resistant varieties, diversification into aquafeed alternatives, and marketing campaigns highlighting nutritional benefits to capture shares in emerging markets like Asia Pacific.

- Roquette Frères. Roquette Frères, a French leader in plant-based ingredients, pursues strategies like launching innovative products such as NUTRALYS fava protein isolates, forging alliances with food manufacturers for vegan applications, and investing in sustainable production to align with global health and environmental trends.

- The Scoular Company. The Scoular Company, based in the U.S., adopts strategies including direct farmer partnerships for quality sourcing, expansion into specialty ingredients like fava bean concentrates, and digital platforms for efficient distribution, targeting growth in animal nutrition and human food sectors.

- Prairie Fava Ltd. Prairie Fava Ltd., a Canadian specialist, focuses on high-yield fava bean varieties, with strategies involving export-oriented processing, collaborations with research institutions for climate-resilient crops, and promotion of organic options to tap into premium markets.

What are the Trends Shaping the Faba Beans Market?

- Increasing adoption of plant-based diets and veganism, boosting demand for fava beans in meat substitutes and functional foods.

- Rise in gluten-free and non-GMO products, with fava bean flour gaining popularity in bakery and snacks.

- Expansion of sustainable agriculture practices, emphasizing fava beans’ nitrogen-fixing benefits for eco-friendly farming.

- Growth in online retail channels, enhancing accessibility and consumer education on nutritional advantages.

- Innovation in protein extraction technologies, leading to new applications in sports nutrition and dairy alternatives.

- Shift toward organic and locally sourced fava beans amid health-conscious preferences.

- Integration into animal feed as cost-effective soy alternatives, reducing environmental impact.

- Development of disease-resistant varieties through government and private R&D initiatives.

What Market Segments and Subsegments are Covered in the Faba Beans Report?

By Type

- Dry Faba Beans

- Fresh Faba Beans

- Canned Faba Beans

- Frozen Faba Beans

- Faba Bean Flour

- Protein Concentrate

- Protein Isolate

- Roasted Faba Beans

- Faba Bean Snacks

- Starch

- Others

By Application

- Food and Beverages

- Animal Feed

- Aquafeed

- Pharmaceuticals

- Cosmetics

- Industrial Uses

- Bakery and Confectionery

- Plant-Based Meat Alternatives

- Flour and Pasta

- Biofuel

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

Faba beans, also known as broad beans or Vicia faba, are nutrient-dense legumes rich in protein, fiber, vitamins, and minerals, commonly used in food, feed, and industrial applications.

Key factors include rising demand for plant-based proteins, sustainable farming practices, technological advancements in processing, health awareness, and expansion in emerging markets.

The Faba Beans market is projected to grow from approximately USD 5.04 billion in 2026 to USD 7.8 billion by 2035.

The CAGR is expected to be 5.0% during the forecast period from 2026 to 2035.

Asia Pacific will contribute notably, holding around 40% of the market value due to high production and consumption in countries like China.

Major players include AGT Food and Ingredients Inc., Archer Daniels Midland Company (ADM), Cargill Incorporated, Roquette Frères, The Scoular Company, and Prairie Fava Ltd.

The report provides in-depth analysis of market size, trends, segments, regional insights, key players, drivers, restraints, opportunities, and forecasts from 2026 to 2035.

Stages include cultivation and harvesting, processing (drying, milling, protein extraction), distribution through wholesale and retail channels, and end-use in food production, feed formulation, and industrial applications.

Trends are shifting toward plant-based and gluten-free products, with consumers preferring sustainable, organic options and innovative applications like protein isolates for vegan diets.

Factors include regulations on food safety and GMO labeling, environmental policies promoting sustainable agriculture, and incentives for nitrogen-fixing crops to reduce fertilizer use amid climate goals.