Chocolate Confectionery Market Size, Share and Trends 2026 to 2035

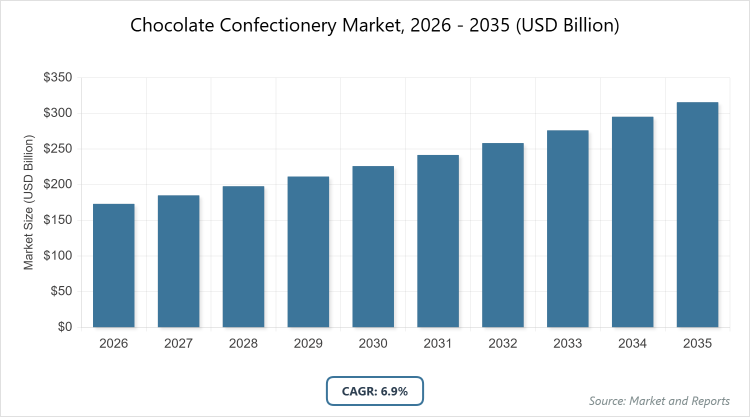

According to MarketnReports, the global Chocolate Confectionery market size was estimated at USD 173.2 billion in 2025 and is expected to reach USD 336 billion by 2035, growing at a CAGR of 6.9% from 2026 to 2035. Chocolate Confectionery Market is driven by rising demand for premium, health-focused, and innovative flavor variants.

What is the Industry Overview of Chocolate Confectionery?

The chocolate confectionery market comprises products made from cocoa, sugar, and milk or alternatives, shaped into bars, truffles, pralines, and other forms for consumption as snacks, gifts, or ingredients in desserts and beverages. This market focuses on indulgence, flavor innovation, and health-oriented options like dark and sugar-free varieties. Market definition refers to the production and sale of chocolate-based sweets, driven by consumer preferences for premium quality, ethical sourcing, and diverse tastes, influenced by cultural traditions and seasonal demands.

What are the Key Insights into Chocolate Confectionery?

- The global Chocolate Confectionery market size was estimated at USD 173.2 billion in 2025 and is expected to reach USD 336 billion by 2035.

- The market is expected to grow at a CAGR of 6.9% during the forecast period from 2026 to 2035.

- The market is driven by premiumization trends, health awareness boosting dark chocolate demand, and e-commerce expansion.

- In the product type segment, milk chocolate dominates with a 51% share due to its creamy texture and broad appeal across age groups.

- In the application segment, snacking holds the largest share at 47% because of convenient on-the-go consumption and impulse buying.

- In the end-user segment, households dominate with 55% share owing to everyday indulgence and family-oriented purchases.

- Europe dominates the market with a 52% share, attributed to strong cultural affinity for chocolate and presence of premium brands in countries like Switzerland and Belgium.

What are the Market Dynamics in Chocolate Confectionery?

Growth Drivers

Growth drivers include increasing consumer preference for premium and artisanal chocolates, fueled by rising disposable incomes and a desire for indulgent experiences. Innovations in flavors, such as exotic fruits and nuts, along with health-focused variants like high-cocoa dark chocolate, attract health-conscious consumers. E-commerce platforms enhance accessibility, while seasonal gifting during holidays boosts sales volumes. Sustainable sourcing practices, like fair-trade cocoa, appeal to ethical buyers, further driving market expansion through brand loyalty and new product launches.

Restraints

Restraints involve fluctuating cocoa prices due to supply chain disruptions from climate change and geopolitical issues, increasing production costs. Health concerns over sugar and calorie content lead to regulatory pressures on labeling and advertising. Competition from healthier snacks like nuts and fruits erodes market share, while counterfeit products in emerging markets undermine trust. Environmental regulations on packaging add compliance costs for manufacturers.

Opportunities

Opportunities stem from the growing demand for plant-based and vegan chocolates, opening niches for dairy-free innovations using alternatives like oat milk. Expansion in emerging markets in Asia-Pacific, with rising middle-class populations, offers untapped potential for affordable premium products. Collaborations with food tech for functional chocolates enriched with vitamins or probiotics can target wellness trends. Digital marketing and personalized packaging enhance consumer engagement, while sustainable initiatives like carbon-neutral production attract eco-friendly segments.

Challenges

Challenges include managing supply chain volatility for cocoa beans, affected by weather and labor issues in producing regions. Balancing taste with health reforms, such as reducing sugar without compromising flavor, requires R&D investments. Intense competition from local artisans and global giants pressures pricing strategies. Regulatory variances across countries complicate international trade, while consumer shifts toward low-sugar diets demand continuous adaptation.

Chocolate Confectionery Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Chocolate Confectionery Market |

| Market Size 2025 | USD 173.2 Billion |

| Market Forecast 2035 | USD 336 Billion |

| Growth Rate | CAGR of 6.9% |

| Report Pages | 220 |

| Key Companies Covered |

Mars, Incorporated, Nestle S.A., The Hershey Company, Mondelez International, Inc., Ferrero Group, Lindt & Sprungli AG, Barry Callebaut AG, Meiji Co., Ltd., Ezaki Glico Co., Ltd., Pladis Global, and Others |

| Segments Covered | By Product Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

The Chocolate Confectionery market is segmented by product type, application, end-user, and region.

Based on Product Type Segment, milk chocolate is the most dominant subsegment, holding approximately 51% market share, followed by dark chocolate as the second most dominant. Milk chocolate dominates due to its smooth, sweet flavor appealing to a wide demographic, including children and adults, driving the market by boosting everyday consumption and gifting through versatile formats like bars and countlines; dark chocolate follows, gaining traction for health benefits like antioxidants, contributing to growth via premium positioning and functional claims.

Based on Application Segment, snacking is the most dominant subsegment with around 47% share, while gifting ranks second. Snacking leads because of convenient, portable formats like single-serve bars meeting on-the-go needs, driving market growth through impulse purchases and innovation in flavors; gifting follows, essential for holidays and occasions, expanding the market via seasonal boxed assortments and premium packaging.

Based on End-User Segment, households dominate with about 55% share, with food service as the second dominant. Households’ dominance arises from routine indulgence and family sharing, propelling the market through bulk purchases and variety packs; food service follows, incorporating chocolate in desserts and beverages, sustaining growth via menu innovations in restaurants and cafes.

What are the Recent Developments in Chocolate Confectionery?

- In 2025, Nestle launched a new line of plant-based milk chocolates using oat milk, targeting vegan consumers and expanding its sustainable product portfolio.

- In early 2026, Hershey acquired a premium dark chocolate brand to strengthen its health-focused offerings amid rising demand for antioxidant-rich products.

- In late 2025, Mondelez introduced sugar-reduced versions of its popular bars, complying with new health regulations and appealing to calorie-conscious buyers.

- In 2025, Lindt partnered with a tech firm for AR-enabled packaging, enhancing consumer engagement through interactive unboxing experiences.

- In January 2026, Ferrero expanded its production facilities in Asia to meet growing demand for nut-filled chocolates in emerging markets.

How Does Regional Analysis Impact Chocolate Confectionery?

- Europe to dominate the global market.

Europe maintains the largest market share, driven by deep-rooted chocolate culture, high per capita consumption, and innovation in premium products. Germany dominates the region with its advanced manufacturing and export prowess, supported by brands like Lindt and Ritter Sport, ensuring quality through strict cocoa standards and seasonal traditions boosting sales.

North America ranks second, fueled by diverse flavor preferences and e-commerce growth. The United States leads with massive retail networks and marketing campaigns, emphasizing indulgence via Hershey and Mars, addressing health trends with dark variants amid high obesity awareness.

Asia-Pacific is the fastest-growing region, propelled by urbanization and rising incomes. China dominates through increasing Western influences and gifting customs, with rapid adoption of premium imports and local production expansions to cater to young consumers.

Latin America shows moderate growth, supported by cocoa production advantages. Brazil leads with domestic consumption and exports, leveraging affordable milk chocolates for mass markets while innovating in fruit-infused varieties.

The Middle East and Africa exhibit emerging potential, driven by tourism and expatriate demands. South Africa dominates in Africa with established retail, while the UAE leads in the Middle East through luxury imports for high-end consumers.

Who are the Key Market Players in Chocolate Confectionery?

Mars, Incorporated focuses on sustainable cocoa sourcing and innovation in low-sugar bars to capture health-conscious segments.

Nestle S.A. emphasizes plant-based alternatives and global expansions, targeting vegan markets with new product lines.

The Hershey Company pursues acquisitions and flavor fusions, strengthening premium offerings in North America.

Mondelez International, Inc. invests in digital marketing and reduced-sugar formulations for broader appeal.

Ferrero Group leverages nut-based specialties and seasonal gifting, expanding in Asia-Pacific.

Lindt & Sprungli AG prioritizes artisanal quality and ethical practices, dominating luxury segments.

Barry Callebaut AG adopts B2B supply strategies, focusing on functional ingredients for manufacturers.

Meiji Co., Ltd. concentrates on Asian innovations, blending traditional flavors with chocolate.

Ezaki Glico Co., Ltd. pursues health-oriented snacks, integrating probiotics in chocolates.

Pladis Global emphasizes affordable indulgence, targeting emerging markets with value packs.

What are the Market Trends Shaping Chocolate Confectionery?

- Premiumization with high-cocoa dark chocolates for health benefits.

- Rise in plant-based and vegan options using alternative milks.

- Innovation in exotic flavors and functional additives like vitamins.

- Sustainable sourcing and fair-trade certifications gaining traction.

- Growth in e-commerce and direct-to-consumer sales channels.

- Reduced-sugar and organic variants addressing health concerns.

- Seasonal and gifting packaging enhancements for holidays.

- Integration of AR and interactive elements in branding.

- Expansion of nut-free and allergen-friendly products.

- Collaborations with artisans for limited-edition releases.

By Product Type

-

- Milk Chocolate

- Dark Chocolate

- White Chocolate

- Ruby Chocolate

- Filled Chocolate

- Truffle

- Praline

- Ganache

- Caramel Chocolate

- Nut Chocolate

- Others

By Application

-

- Gifting

- Snacking

- Baking

- Beverage

- Dessert

- Confectionery Making

- Seasonal

- Promotional

- Bulk

- Specialty

- Others

By End-User

-

- Households

- Food Service

- Retailers

- Manufacturers

- Online Buyers

- Gift Shops

- Supermarkets

- Convenience Stores

- Specialty Stores

- Department Stores

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Chocolate Confectionery Market - Industry Analysis

Chapter 4. Global Chocolate Confectionery Market- Competitive Landscape

Chapter 5. Global Chocolate Confectionery Market - Product Type Analysis

Chapter 6. Global Chocolate Confectionery Market - Application Analysis

Chapter 7. Global Chocolate Confectionery Market - End-User Analysis

Chapter 8. Chocolate Confectionery Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Chocolate confectionery refers to sweets made from cocoa, sugar, and milk or alternatives, including bars, truffles, and pralines for indulgence and gifting.

Key factors include premiumization, health trends favoring dark chocolate, flavor innovations, and e-commerce expansion.

The market value is projected to grow from USD 173.2 billion in 2025 to USD 336 billion by 2035.

The market is expected to grow at a CAGR of 6.9% during the forecast period from 2026 to 2035.

Europe will contribute notably, holding the largest share due to cultural affinity and premium brands.

Major players include Mars, Incorporated, Nestle S.A., The Hershey Company, Mondelez International, Inc., and Ferrero Group.

The report offers in-depth analysis of size, trends, segmentation, regional insights, key players, and forecasts.

Stages include cocoa sourcing, processing, manufacturing, packaging, distribution, and retail sales.

Trends favor sustainable, health-focused products, with preferences shifting to dark and vegan options.

Regulations on sugar content and sustainable cocoa sourcing are influencing innovation and supply chains.