Video Conferencing Market Size, Share and Trends 2026 to 2035

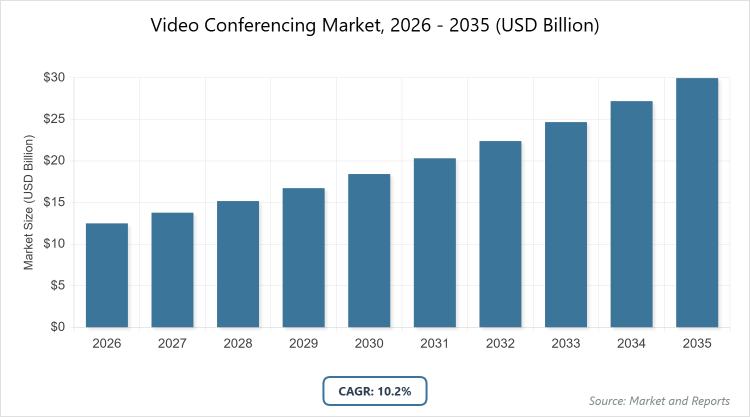

According to MarketnReports, the global Video Conferencing market size was estimated at USD 12.5 billion in 2025 and is expected to reach USD 32.8 billion by 2035, growing at a CAGR of 10.2% from 2026 to 2035. The video conferencing market is driven by increasing remote work trends, digital transformation in enterprises, and advancements in AI-integrated communication tools.

What are the Key Insights into Video Conferencing?

- The global Video Conferencing market was valued at USD 12.5 billion in 2025 and is projected to reach USD 32.8 billion by 2035.

- The market is expected to grow at a CAGR of 10.2% during the forecast period from 2026 to 2035.

- The market is driven by hybrid work models, AI enhancements for better user experience, cloud adoption, and demand for secure communication in enterprises.

- In the type segment, cloud-based dominates with a 55% share due to its scalability, ease of deployment, and cost-effectiveness for remote teams.

- In the application segment, corporate meetings dominate with a 40% share as it enables efficient business collaboration across geographies.

- In the end-user segment, enterprises dominate with a 50% share owing to large-scale adoption for internal and client communications.

- North America dominates the regional market with a 35% share, driven by tech innovation, high corporate adoption, and presence of key players like Zoom and Microsoft.

What is the Industry Overview of Video Conferencing?

The Video Conferencing market encompasses hardware, software, and services that enable real-time audio-visual communication over the internet or networks, facilitating remote collaboration, meetings, and interactions with features like screen sharing, recording, and integration with productivity tools. Market definition includes cloud-based, on-premise, and hybrid platforms that provide secure, scalable solutions for high-quality video calls, supporting industries requiring efficient remote engagement while addressing challenges in bandwidth, security, interoperability, and user adoption for seamless global connectivity.

What are the Market Dynamics of Video Conferencing?

Growth Drivers

The Video Conferencing market is propelled by the widespread shift to hybrid and remote work environments, where platforms offer seamless integration with tools like calendars and file sharing, enhancing productivity and reducing travel costs for global teams. Advancements in AI for features like real-time translation, noise cancellation, and virtual backgrounds improve user experience, driving adoption in diverse sectors. Increasing cloud infrastructure enables scalable, secure solutions with low latency, while rising cybersecurity measures address data privacy concerns. Government initiatives for digital education and telehealth further boost demand in public sectors, supported by 5G rollout for high-quality mobile conferencing.

Restraints

High dependency on internet bandwidth and connectivity issues in rural or developing areas limit accessibility, leading to poor user experience and adoption barriers. Data security and privacy risks from cyber threats like zoombombing require constant investments in encryption, deterring sensitive industries. Competition from free or low-cost alternatives reduces revenue for premium providers. Integration challenges with legacy systems increase implementation costs for enterprises. Economic downturns can cut IT budgets, delaying upgrades to advanced platforms.

Opportunities

Opportunities arise from AI-driven enhancements like sentiment analysis and automated summaries, appealing to enterprise analytics needs. Expansion into emerging markets with improving internet infrastructure offers growth for affordable, mobile-first solutions. Partnerships with AR/VR firms for immersive meetings can revolutionize collaboration. The rise of telehealth and online education creates specialized niches. Development of sustainable, energy-efficient data centers supports eco-friendly cloud services, attracting green-conscious users.

Challenges

Challenges include ensuring interoperability across platforms and devices, requiring standard protocols to avoid fragmentation. Rapid technological evolution demands continuous updates, straining R&D resources. Privacy regulations like GDPR complicate global operations, increasing compliance costs. User fatigue from prolonged video calls necessitates ergonomic improvements. Cybersecurity threats evolve with market growth, requiring proactive defenses.

Video Conferencing Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Video Conferencing Market |

| Market Size 2025 | USD 12.5 Billion |

| Market Forecast 2035 | USD 32.8 Billion |

| Growth Rate | CAGR of 10.2% |

| Report Pages | 210 |

| Key Companies Covered | Zoom Video Communications, Microsoft Corporation, Cisco Systems, Inc., Google LLC, RingCentral, Inc., Avaya Holdings Corp., Poly (HP Inc.), LogMeIn (GoTo), and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Video Conferencing?

The Video Conferencing market is segmented by type, application, end-user, and region.

By Type. Cloud-based is the most dominant subsegment, holding approximately 55% market share, due to its flexibility, automatic updates, and subscription models. This dominance drives the market by lowering entry barriers and enabling remote access for distributed teams. Hybrid ranks as the second most dominant, with around 25% share, combining on-premise security with cloud scalability, propelling growth through customized enterprise solutions.

By Application. Corporate meetings emerge as the most dominant subsegment, capturing about 40% share, primarily because of the need for efficient remote collaboration. This leads to market growth by supporting global business operations and decision-making. Education & training follows as the second most dominant, with a roughly 20% share, enabling interactive learning, driving the market via e-learning expansion.

By End-User. Enterprises represent the most dominant subsegment at about 50% share, driven by scalability needs for large organizations. This dominance accelerates market expansion through integration with business tools. Educational institutions rank second most dominant, holding around 15% share, due to remote learning demands, contributing to growth via digital education trends.

What are the Recent Developments in Video Conferencing?

- In January 2025, Zoom announced AI-powered meeting summaries and real-time translation for 30 languages, enhancing global collaboration.

- In October 2024, Microsoft Teams integrated with Copilot AI for automated note-taking and task assignment.

- In July 2024, Cisco Webex launched end-to-end encryption for all meetings to address security concerns.

- In April 2024, Google Meet expanded hybrid features with auto-framing and noise cancellation for better user experience.

- In February 2024, RingCentral acquired a VR startup to develop immersive video conferencing capabilities.

What is the Regional Analysis of Video Conferencing?

- North America is expected to dominate the global market.

Asia Pacific holds the largest share at approximately 40%, with China as the dominating country, due to booming pharma exports, semiconductor fabrication, and government support for biotech parks. This region’s growth is fueled by low costs, skilled labor, and increasing FDI, positioning it as a global manufacturing hub for cleanroom-dependent industries. Massive semiconductor clusters in Taiwan drive demand for ultra-clean facilities. India’s pharma export growth requires GMP-compliant cleanrooms. Japan’s electronics precision favors high-end modular systems. South Korea’s display industry demands particle-free environments. Cultural emphasis on quality accelerates validation training. Export-oriented policies enhance global competitiveness. Rising middle-class consumption increases medical device cleanrooms. Environmental regulations push for energy-efficient designs. Vocational programs build expertise in cleanroom maintenance across the region. Strong supply chains enable quick deployment of modular units.

North America follows closely, driven by advanced R&D and stringent FDA regulations, where the United States dominates through its biopharma leadership and tech innovation. Growth stems from high healthcare spending and demand for sterile manufacturing, though higher costs moderate expansion compared to Asia. Biotech clusters in Boston and San Francisco accelerate modular cleanroom adoption. NIH grants fund advanced filtration research. Defense applications in aerospace require contamination-free assembly. University-industry partnerships in MIT and Stanford advance monitoring technologies. High insurance coverage for biologics supports facility investments. Strict cGMP guidelines ensure market preference for validated systems. Reshoring of pharma production boosts domestic demand. Emphasis on sustainable energy reduces operational carbon footprints.

Europe exhibits strong performance with emphasis on GMP compliance and sustainability, led by Germany through its pharma giants and engineering firms. The region’s expansion benefits from EU funding for clean tech and focus on biologic production. Horizon Europe programs support collaborative cleanroom projects. The UK’s advanced biopharma hubs in Cambridge promote adoption in cell therapy. Multilingual compliance aids diverse markets like France and Italy. REACH regulations ensure safe material usage. Industry consortia share validation best practices. Aging infrastructure renewal projects adopt modular upgrades. Vocational training centers build expertise in cleanroom operations. Circular economy initiatives recycle consumables, reducing waste. Green deal policies promote energy-efficient HVAC systems.

Latin America shows moderate advancement, dominated by Brazil’s pharma and biotech growth, supported by foreign investments though limited by infrastructure; expansion is aided by regional trade agreements. Mexico benefits from NAFTA ties, facilitating tech transfers from North America. Government health initiatives in Argentina promote GMP facilities. The rise of generics in Chile creates demand for sterile production. However, economic variability affects consistent investments. Emerging medical device manufacturing in Colombia adopts cleanroom standards. Regional pacts like Mercosur ease equipment imports. Vocational programs in Peru build validation skills. Biodiversity concerns influence eco-friendly cleanroom materials. Urban expansion drives hospital cleanroom demand. Foreign aid supports biotech park development in smaller nations.

The Middle East and Africa remain emerging, with the United Arab Emirates leading through medical tourism and pharma diversification, constrained by lower tech access but promising via infrastructure projects. Saudi Arabia’s Vision 2030 funds advanced cleanroom facilities. South Africa’s biotech sector adopts for vaccine production. Technology partnerships with European firms build expertise in Egypt. However, water scarcity impacts HVAC cooling. Investments in solar-powered cleanrooms address energy needs. OPEC policies stabilize pharma-related applications. Vocational initiatives in Nigeria train for future jobs. Emerging labs in Kenya require imaging for medical research. Focus on sustainable development goals promotes green cleanroom innovations. Oil-funded health hubs in Gulf states drive high-end facility demand.

What are the Key Market Players in Video Conferencing?

- Zoom Video Communications. Zoom focuses on AI enhancements and security, expanding enterprise features through acquisitions.

- Microsoft Corporation. Microsoft integrates Teams with Office 365, investing in hybrid work tools for productivity.

- Cisco Systems, Inc. Cisco emphasizes Webex security and interoperability, pursuing hardware-software bundles.

- Google LLC. Google develops Meet for seamless integration with Workspace, focusing on user-friendly mobile access.

- RingCentral, Inc. RingCentral targets SMBs with cloud PBX, strategizing on VR for immersive meetings.

- Avaya Holdings Corp. Avaya offers unified communications, emphasizing on-premise to cloud transitions.

- Poly (HP Inc.) Poly specializes in hardware endpoints, partnering for room systems.

- LogMeIn (GoTo). LogMeIn focuses on remote support, expanding GoToMeeting for small teams.

What are the Market Trends in Video Conferencing?

- Increasing AI for transcription and virtual assistants.

- Rise of hybrid meeting solutions with AR/VR.

- Adoption of end-to-end encryption for security.

- Growth in mobile-first platforms for flexibility.

- Focus on sustainability with energy-efficient data centers.

- Expansion of telehealth-specific features.

What Market Segments and Subsegments are Covered in the Video Conferencing Report?

By Type

- Cloud-Based

- On-Premise

- Hybrid

- Hardware-Based

- Software-Based

- Managed Services

- Video Endpoint Systems

- Web-Based Conferencing

- Mobile Apps

- Room-Based Systems

- Others

By Application

- Corporate Meetings

- Education & Training

- Healthcare Consultations

- Government & Public Sector

- Financial Services

- Legal Proceedings

- Sales & Marketing

- Product Demonstrations

- Customer Support

- Event Management

- Others

By End-User

- Enterprises

- Education Institutions

- Healthcare Providers

- Government Organizations

- Financial Institutions

- Legal Firms

- Retail & E-Commerce

- Manufacturing

- Media & Entertainment

- Non-Profit Organizations

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Video Conferencing is a technology enabling real-time audio-visual communication over networks for remote meetings and collaboration.

Key factors include hybrid work, AI advancements, cloud adoption, and security enhancements.

The market is projected to grow from USD 12.5 billion in 2025 to USD 32.8 billion by 2035.

The CAGR is expected to be 10.2%.

North America will contribute notably, holding around 35% share due to tech innovation.

Major players include Zoom Video Communications, Microsoft Corporation, Cisco Systems, Inc., Google LLC, and RingCentral, Inc.

The report provides detailed analysis of size, trends, segments, regional outlook, key players, and forecasts.

Stages include hardware manufacturing, software development, cloud infrastructure, integration, distribution, and support services.

Trends evolve toward AI and hybrid solutions, with preferences for secure, user-friendly platforms.

Data privacy regulations like GDPR and environmental concerns over data center energy consumption influence operations.