B2B2C Insurance Market Size, Share and Trends 2026 to 2035

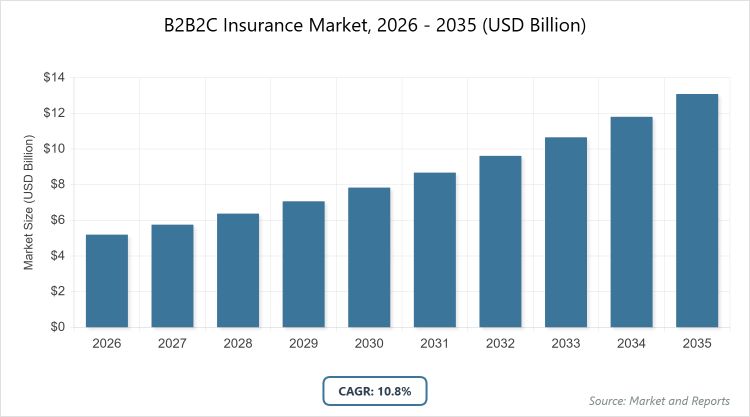

According to MarketnReports, the global B2B2C Insurance market size was estimated at USD 5.2 billion in 2025 and is expected to reach USD 14.5 billion by 2035, growing at a CAGR of 10.8% from 2026 to 2035. B2B2C Insurance Market is driven by increasing digital partnerships and embedded insurance solutions.

What are the Key Insights into the B2B2C Insurance Market?

- The global B2B2C Insurance market was valued at USD 5.2 billion in 2025 and is projected to reach USD 14.5 billion by 2035.

- The market is expected to grow at a CAGR of 10.8% during the forecast period.

- The market is driven by rising digital transformation and partnerships between insurers and non-insurance intermediaries.

- In the type segment, non-life insurance dominates with 62% share due to its alignment with on-demand, embedded offerings in high-volume sectors like auto and travel.

- In the distribution channel segment, online platforms dominate with 55% share as they enable seamless integration and real-time personalization in e-commerce and mobile apps.

- In the end-use industry segment, banks & financial institutions dominate with 38% share owing to established trust and bancassurance models that facilitate cross-selling.

- North America dominates the regional market with 35% share because of advanced technological infrastructure, high digital adoption, and supportive regulations.

What is the B2B2C Insurance Market?

Industry Overview

The B2B2C insurance market involves the distribution of insurance products through business intermediaries to end consumers, creating a seamless integration where insurers partner with non-insurance companies like retailers, banks, or e-commerce platforms to offer tailored coverage at the point of sale. This model enhances accessibility by embedding insurance into everyday transactions, such as purchasing a gadget or booking travel, thereby reducing friction in the buying process and leveraging the trust of intermediary brands. Market definition encompasses all life, health, property, and casualty policies sold via these channels, focusing on digital enablement, personalization, and ecosystem collaborations that drive efficiency, customer loyalty, and broader market penetration while addressing evolving consumer needs for convenience and protection.

What are the Market Dynamics Shaping the B2B2C Insurance Market?

Growth Drivers

The growth drivers in the B2B2C insurance market are primarily fueled by the rapid digitalization of distribution channels, enabling insurers to embed products seamlessly into partner ecosystems like e-commerce and fintech platforms, which enhances customer convenience and expands reach. Increasing consumer demand for personalized, on-demand coverage, coupled with rising awareness of financial protection needs amid economic uncertainties, accelerates adoption. Strategic partnerships between insurers and intermediaries, such as banks and retailers, leverage existing customer relationships to drive trust and loyalty, while advancements in AI and data analytics allow for real-time underwriting and tailored offerings. Favorable regulatory environments promoting innovation and consumer-centric models further propel market expansion by facilitating easier integration and compliance.

Restraints

Significant restraints in the B2B2C insurance market include complex regulatory compliance across diverse regions and industries, which increases operational costs and delays product launches due to varying data privacy laws like GDPR and CCPA. Data security concerns, heightened by frequent cyber threats, erode consumer trust and hinder partnerships, as intermediaries hesitate to share sensitive information. Limited technological infrastructure in emerging markets restricts scalability, while high integration costs for legacy systems pose barriers for smaller players. Additionally, consumer skepticism toward embedded insurance, stemming from perceived lack of transparency or over-reliance on intermediaries, can slow adoption rates and limit market penetration.

Opportunities

Opportunities in the B2B2C insurance market emerge from the integration of emerging technologies like blockchain and IoT, which enhance transparency, reduce fraud, and enable usage-based policies for sectors such as automotive and health. Expanding into underserved emerging markets, where rising middle-class populations and smartphone penetration create demand for affordable, accessible coverage through local partnerships. The growth of the gig economy offers potential for flexible, micro-insurance products tailored to freelancers via platforms like ride-sharing apps. Furthermore, sustainability-focused initiatives, such as green insurance tied to eco-friendly purchases, can attract environmentally conscious consumers and open new revenue streams through collaborations with sustainable brands.

Challenges

Challenges in the B2B2C insurance market revolve around achieving seamless technological integration between insurers and diverse intermediaries, as mismatched systems can lead to inefficiencies and poor user experiences. Balancing personalization with privacy concerns remains difficult, with increasing scrutiny on data usage potentially leading to regulatory backlash. Competition from insurtech startups disrupts traditional models, pressuring incumbents to innovate rapidly while managing partnership dependencies. Economic volatility affects consumer spending on non-essential insurance, and educating intermediaries on product complexities is essential to avoid mis-selling risks that could damage reputations and invite legal issues.

B2B2C Insurance Market: Report Scope

| Report Attributes | Report Details |

| Report Name | B2B2C Insurance Market |

| Market Size 2025 | USD 5.2 Billion |

| Market Forecast 2035 | USD 14.5 Billion |

| Growth Rate | CAGR of 10.8% |

| Report Pages | 220 |

| Key Companies Covered |

Allianz, AXA, Zurich Insurance Group, Berkshire Hathaway, UnitedHealth Group, Prudential, and Others |

| Segments Covered | By Type, By Distribution Channel, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Market Segmentation Structured in the B2B2C Insurance Market?

The B2B2C Insurance market is segmented by type, distribution channel, end-use industry, and region.

Based on Type Segment, non-life insurance is the most dominant subsegment, followed by life insurance as the second most dominant. Non-life insurance’s dominance arises from its suitability for embedded, contextual offerings in high-frequency transactions like travel or gadget purchases, where immediate protection needs drive demand; this propels the market by enabling quick, low-commitment sales through intermediaries, boosting overall accessibility and volume, whereas life insurance’s growth is supported by long-term financial planning integrated into banking or employer platforms, driving the market through enhanced customer retention and bundled services that foster loyalty and recurring revenue.

Based on the Distribution Channel Segment, online platforms are the most dominant subsegment, followed by bancassurance as the second most dominant. Online platforms lead due to their scalability and integration with digital ecosystems like e-commerce, allowing real-time policy issuance and customization that meets modern consumer expectations for speed; this advances the market by lowering distribution costs and expanding global reach, while bancassurance thrives on established trust in financial institutions, driving growth through cross-selling opportunities that combine insurance with banking products, thereby increasing penetration in underserved segments and supporting comprehensive financial solutions.

Based on End-Use Industry Segment, banks & financial institutions are the most dominant subsegment, followed by retailers as the second most dominant. Banks & financial institutions dominate because of their direct access to consumer financial data and trust-based relationships, enabling personalized insurance bundling with loans or accounts; this accelerates market growth by streamlining approvals and enhancing customer lifetime value, whereas retailers gain prominence through point-of-sale integrations for product-specific coverage, propelling the market via impulse purchases and loyalty programs that integrate insurance into shopping experiences, thus broadening consumer engagement.

What are the Recent Developments in the B2B2C Insurance Market?

- In April 2024, Wakam received approval from the Financial Conduct Authority and Prudential Regulation Authority to launch its UK subsidiary, Wakam UK Limited, aiming to expand embedded insurance offerings in the European market through digital platforms.

- In May 2023, Lexasure Financial Group launched LexasureCloud 1.0, a cloud-based B2B2C insurtech platform designed to digitize risk and enhance competitiveness for insurance companies in Asia, focusing on partner distribution channels.

- In October 2023, Allianz Partners formed a strategic alliance with Bolttech to provide embedded device and appliance protection insurance across Asia-Pacific and the US, leveraging combined strengths for point-of-need solutions.

- In Q2 2024, Bolttech raised USD 196 million in Series B funding led by Tokio Marine, to accelerate growth in embedded insurtech solutions and expand B2B2C partnerships globally.

How does Regional Analysis Impact the B2B2C Insurance Market?

- North America is expected to dominate the global market.

North America commands the B2B2C insurance market, propelled by robust technological advancements, high digital literacy, and a mature insurance landscape that fosters innovative partnerships; the United States dominates as the key country, with leading firms like UnitedHealth Group and AIG driving adoption through fintech integrations and regulatory support, enabling widespread embedded insurance in e-commerce and banking sectors.

Europe demonstrates substantial growth in the B2B2C insurance market, supported by stringent data protection regulations like GDPR and a focus on consumer-centric models; Germany emerges as the dominating country, where companies such as Allianz and Munich Re excel in bancassurance and digital platforms, bolstered by EU-wide initiatives promoting cross-border collaborations and sustainable insurance products.

Asia Pacific is surging in the B2B2C insurance market, driven by rapid urbanization, increasing smartphone penetration, and government pushes for financial inclusion; China leads as the dominant country, with giants like Ping An and China Life leveraging e-commerce giants for massive scale, supported by policies encouraging insurtech innovation and addressing underinsured populations.

Latin America presents growing opportunities in the B2B2C insurance market, aided by expanding digital economies and rising middle-class demands for accessible coverage; Brazil stands out as the dominating country, where partnerships with retailers and banks, led by players like Porto Seguro, capitalize on mobile banking trends and regulatory reforms to enhance market accessibility.

The Middle East and Africa exhibit emerging traction in the B2B2C insurance market, fueled by diversification efforts and increasing fintech adoption; the United Arab Emirates dominates, with initiatives like Dubai’s smart city projects enabling embedded insurance through telecom and retail channels, while South Africa contributes via financial inclusion programs.

Who are the Key Market Players in the B2B2C Insurance Market?

- Allianz pursues growth through strategic partnerships with digital platforms and insurtech firms, emphasizing embedded insurance solutions to enhance customer engagement and expand into emerging markets with AI-driven personalization.

- AXA focuses on innovation in bancassurance and e-commerce integrations, leveraging data analytics for tailored products while prioritizing sustainability to meet regulatory demands and attract eco-conscious consumers.

- Zurich Insurance Group adopts a multi-channel approach, collaborating with retailers and telecom providers for on-demand coverage, with strategies centered on digital transformation to improve efficiency and global reach.

- Berkshire Hathaway employs a diversified portfolio strategy, investing in technology for seamless B2B2C distribution, focusing on risk management and long-term partnerships to solidify its position in non-life segments.

- UnitedHealth Group concentrates on health-focused B2B2C models through employer and fintech alliances, utilizing real-time data for personalized wellness plans to drive retention and compliance in regulated environments.

- Prudential leverages Asian market expertise for expansion, partnering with financial institutions for life insurance bundling, with emphasis on mobile-first solutions to capture growing digital consumer bases.

What are the Market Trends in the B2B2C Insurance Market?

- Rapid adoption of embedded insurance in e-commerce and fintech platforms for seamless point-of-sale coverage.

- Increasing use of AI and data analytics for personalized, real-time underwriting and policy recommendations.

- Growth in partnerships between insurers and non-traditional intermediaries like retailers and telecoms.

- Shift toward on-demand and micro-insurance products tailored to gig economy workers.

- Emphasis on sustainability-linked insurance offerings to appeal to environmentally aware consumers.

- Expansion of blockchain for enhanced transparency and fraud reduction in claims processing.

- Rising focus on cyber insurance integrations amid increasing digital risks.

What Market Segments and their Subsegments are Covered in the B2B2C Insurance Report?

By Type

- Life Insurance

- Health Insurance

- Property & Casualty Insurance

- Travel Insurance

- Auto Insurance

- Home Insurance

- Pet Insurance

- Gadget Insurance

- Cyber Insurance

- Liability Insurance

- Others

By Distribution Channel

- Online Platforms

- Offline Channels

- Bancassurance

- E-commerce

- Insurance Brokers

- Aggregator Websites

- Mobile Applications

- Retail Chains

- Telecom Providers

- OEMs/Device Manufacturers

- Others

By End-Use Industry

- Banks & Financial Institutions

- Automotive

- Retailers

- Telecom

- Utilities

- Healthcare

- Consumer Electronics

- Travel & Hospitality

- Small & Medium Enterprises

- Large Enterprises

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global B2B2C Insurance Market - Industry Analysis

Chapter 4. Global B2B2C Insurance Market- Competitive Landscape

Chapter 5. Global B2B2C Insurance Market - Type Analysis

Chapter 6. Global B2B2C Insurance Market - Distribution Channel Analysis

Chapter 7. Global B2B2C Insurance Market - End-Use Industry Analysis

Chapter 8. B2B2C Insurance Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

B2B2C insurance refers to insurance products distributed through business intermediaries to end consumers, embedding coverage into transactions via partners like banks or retailers for enhanced accessibility.

Key factors include digital transformation, rising partnerships, consumer demand for personalization, regulatory support, and technological advancements like AI and blockchain.

The B2B2C insurance market is projected to grow from USD 5.2 billion in 2025 to USD 14.5 billion by 2035.

The market is expected to grow at a CAGR of 10.8% from 2026 to 2035.

North America will contribute notably, holding around 35% market share due to advanced tech and high adoption.

Major players include Allianz, AXA, Zurich Insurance Group, Berkshire Hathaway, UnitedHealth Group, and Prudential, driving growth through innovations and partnerships.

The report offers in-depth analysis including market size, trends, segmentation, regional insights, key players, and forecasts from 2026 to 2035.

Stages include product development by insurers, partnership formation with intermediaries, distribution through channels, policy issuance to consumers, and claims management.

Trends lean toward embedded and on-demand insurance, with consumers preferring personalized, digital-first experiences integrated into daily transactions.

Factors include data privacy regulations like GDPR, supportive policies for digital insurance, and growing emphasis on sustainable products amid climate concerns.