Bioplastic Textile Market Size, Share and Trends 2026 to 2035

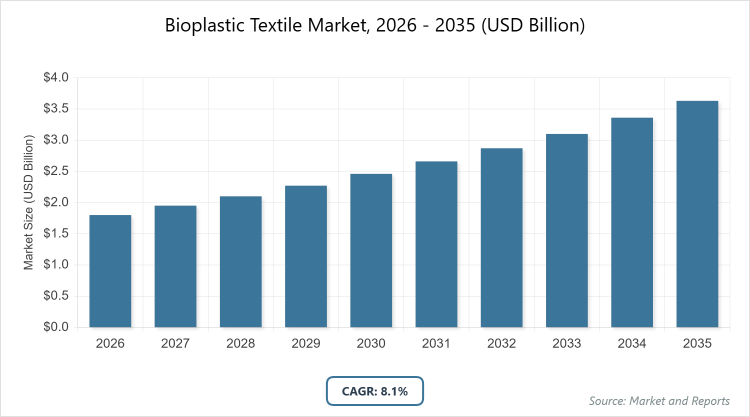

According to MarketnReports, the global Bioplastic Textile market size was estimated at USD 1.8 billion in 2025 and is expected to reach USD 4.0 billion by 2035, growing at a CAGR of 8.1% from 2026 to 2035. Increasing demand for sustainable and eco-friendly materials in the textile industry.

What are the Key Insights into the bioplastic textile market?

- The global Bioplastic Textile market was valued at USD 1.8 billion in 2025 and is projected to reach USD 4.0 billion by 2035.

- The market is expected to grow at a CAGR of 8.1% during the forecast period.

- The market is driven by rising environmental awareness and regulatory pressures to reduce plastic pollution in the textile sector.

- In the material segment, PLA dominates with 47% share due to its excellent biodegradability, versatility in processing, and cost-effectiveness compared to other biopolymers.

- In the application segment, apparel dominates with 42% share as fashion brands increasingly adopt sustainable materials to meet consumer demands for eco-friendly clothing.

- In the end-user segment, fashion & apparel brands dominate with 40% share owing to their direct consumer interaction and emphasis on branding through sustainability initiatives.

- Europe dominates the regional market with 40% share because of stringent environmental regulations, high consumer awareness, and strong government support for bio-based innovations.

What is the Bioplastic Textile Market?

Industry Overview

The bioplastic textile market encompasses the production, distribution, and application of textiles derived from bioplastics, which are polymers made from renewable biological sources such as plants, algae, or bacteria, offering a sustainable alternative to traditional petroleum-based synthetic fibers. This market involves the creation of fibers, yarns, and fabrics that are biodegradable or bio-based, reducing environmental impact through lower carbon emissions and decreased reliance on fossil fuels. Market definition includes all bio-based and biodegradable materials used in textile manufacturing, spanning from raw polymer production to finished products, with a focus on promoting circular economy principles by enabling compostability and recyclability while maintaining performance qualities like durability, flexibility, and comfort essential for various textile uses.

What are the Market Dynamics Shaping the Bioplastic Textile Market?

Growth Drivers

The primary growth drivers in the bioplastic textile market stem from escalating global environmental concerns and the push for sustainable alternatives to conventional synthetic textiles, which contribute significantly to microplastic pollution and landfill waste. Increasing consumer preference for eco-friendly products, coupled with corporate sustainability commitments from major fashion and textile brands, is accelerating adoption. Technological advancements in biopolymer production, such as improved PLA and PHA formulations, enhance material performance, making them viable for high-demand applications like apparel and automotive interiors.

Government regulations banning single-use plastics and promoting circular economy practices further bolster market expansion by incentivizing investments in renewable feedstock sourcing and biodegradable fiber development.

Restraints

High production costs remain a significant restraint in the bioplastic textile market, as bio-based materials often require expensive raw feedstocks like corn or sugarcane, leading to premiums of 20-50% over petroleum-based alternatives. Limited scalability of production infrastructure and inconsistent supply chains for renewable resources pose challenges, particularly in regions with competing agricultural demands. Performance limitations, such as lower durability or heat resistance in certain bioplastics, hinder widespread adoption in technical textiles. Additionally, the lack of standardized certification and composting facilities globally complicates end-of-life management, potentially undermining consumer trust and regulatory compliance.

Opportunities

Emerging opportunities in the bioplastic textile market arise from innovations in bio-based polymers, such as mycelium-derived fibers and advanced PHA blends, which offer enhanced properties like water resistance and tensile strength for expanding applications in sportswear and medical textiles. Growing investments in research and development, supported by collaborations between textile manufacturers and biotech firms, can lower costs and improve scalability. The rise of e-commerce and direct-to-consumer brands focused on sustainability opens new distribution channels. Furthermore, untapped markets in developing regions, where urbanization drives textile demand, present potential for growth through localized production using abundant agricultural waste as feedstocks.

Challenges

Key challenges in the bioplastic textile market include achieving performance parity with synthetic fibers while maintaining affordability, as bioplastics often exhibit limitations in dyeability, wrinkle resistance, and longevity under repeated use. Competition from recycled synthetics and other sustainable alternatives dilutes market focus. Fluctuating prices of renewable feedstocks due to climate variability and food security concerns create supply instability. Moreover, educating consumers and stakeholders on the true environmental benefits versus greenwashing claims is crucial, as misconceptions about biodegradability in non-ideal conditions can lead to backlash and slower adoption rates.

Bioplastic Textile Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Bioplastic Textile Market |

| Market Size 2025 | USD 1.8 Billion |

| Market Forecast 2035 | USD 4.0 Billion |

| Growth Rate | CAGR of 8.1% |

| Report Pages | 220 |

| Key Companies Covered |

NatureWorks, BASF, Toray, Teijin, Indorama Ventures, Lenzing, and Others |

| Segments Covered | By Material, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Market Segmentation Structured in the Bioplastic Textile Market?

The Bioplastic Textile market is segmented by material, application, end-user, and region.

Based on the Material Segment, PLA is the most dominant subsegment, followed by PHA as the second most dominant. PLA’s dominance stems from its widespread availability, derived from renewable sources like corn starch, and its superior biodegradability under industrial composting conditions, which aligns with global sustainability goals; this drives the market by enabling cost-effective production of versatile fibers suitable for mass-market apparel and reducing reliance on fossil fuels, while PHA’s growing prominence is due to its full marine biodegradability and microbial production process, helping propel market expansion through applications in high-performance textiles where environmental impact is a key concern.

Based on Application Segment, apparel is the most dominant subsegment, followed by home textiles as the second most dominant. Apparel leads because of the fashion industry’s shift toward sustainable materials amid consumer pressure for eco-friendly clothing, allowing brands to differentiate through biodegradable fabrics that minimize microplastic shedding; this fuels market growth by integrating bioplastics into high-volume consumer products, whereas home textiles gain traction for their use in durable items like curtains and upholstery, driving the market through increased adoption in interior design where long-term environmental benefits like compostability at end-of-life enhance overall sustainability efforts.

Based on End-User Segment, fashion & apparel brands is the most dominant subsegment, followed by automotive industry as the second most dominant. Fashion & apparel brands dominate due to their direct engagement with environmentally conscious consumers and ability to leverage marketing around sustainable collections, which accelerates market penetration by scaling bioplastic use in trendy garments; this propels the market by creating demand pull from retail giants, while the automotive industry’s rise is attributed to regulations on vehicle emissions and interior materials, driving growth through incorporation of bioplastic textiles in seats and panels that reduce carbon footprints and support lightweighting for fuel efficiency.

What are the Recent Developments in the Bioplastic Textile Market?

- In Q2 2024, BASF and Indorama Ventures announced a strategic partnership to co-develop bioplastic-based textile fibers for apparel and home textiles, aiming to accelerate sustainable material adoption in large-scale manufacturing through combined expertise in polymer chemistry and fiber production.

- In Q1 2025, NatureWorks LLC launched its new Ingeo bioplastic textile yarn targeted at the fashion industry, offering enhanced biodegradability and performance for apparel, which supports the growing demand for eco-friendly alternatives in fast fashion while improving processing efficiency for manufacturers.

- In Q1 2025, Novamont and H&M Group formed a partnership to develop compostable bioplastic textiles for H&M’s sustainable clothing lines, focusing on reducing the environmental footprint of fast fashion by integrating materials that decompose naturally and align with circular economy principles.

- In Q2 2025, Futerro opened a new PLA bioplastic textile production plant in Belgium, expanding output capacity to meet rising European demand for renewable textile materials, thereby strengthening supply chains and enabling broader adoption across apparel and industrial applications.

How does Regional Analysis Impact the Bioplastic Textile Market?

- Europe to dominate the global market.

Europe leads the bioplastic textile market, driven by stringent regulations like the EU’s Plastics Strategy and high consumer awareness of sustainability, fostering innovation in bio-based fibers; Germany stands out as the dominating country, with its robust chemical industry and companies like BASF pioneering advanced biopolymers, supported by government incentives that promote research and large-scale production for apparel and automotive sectors.

North America exhibits strong growth in the bioplastic textile market, fueled by corporate sustainability initiatives and increasing demand for eco-friendly consumer goods; the United States is the dominating country, where firms like NatureWorks lead in PLA production, backed by state-level plastic bans and investments in biotech, enabling expansion in fashion and medical textiles.

Asia Pacific is rapidly expanding in the bioplastic textile market, propelled by urbanization, rising textile manufacturing, and government policies on plastic reduction; China dominates as the key country, with its massive production capacity and access to affordable feedstocks like sugarcane, driving adoption in apparel and industrial fabrics through local innovations and export-oriented supply chains.

Latin America shows emerging potential in the bioplastic textile market, supported by abundant agricultural resources for bio-feedstocks and growing export demands for sustainable products; Brazil is the dominating country, leveraging its sugarcane industry for bio-PE and PLA, with initiatives like partnerships with global brands enhancing market growth in apparel and home textiles.

The Middle East and Africa represent nascent but promising growth in the bioplastic textile market, driven by diversification from oil-based economies and increasing focus on sustainable development; Saudi Arabia emerges as a key player, investing in bio-based technologies through Vision 2030, while South Africa contributes with agricultural feedstocks, fostering regional adoption in industrial and consumer textiles.

Who are the Key Market Players in the Bioplastic Textile Market?

- NatureWorks focuses on expanding its Ingeo PLA portfolio through investments in production capacity and collaborations with fashion brands, emphasizing biodegradability and performance to capture sustainable apparel markets while advancing circular economy solutions.

- BASF employs strategies centered on innovation in bio-based polymers like ecovio, partnering with textile manufacturers to develop high-performance fibers for industrial applications, prioritizing regulatory compliance and supply chain sustainability to strengthen its global presence.

- Toray leverages advanced synthetic expertise to integrate bio-PET into its textile offerings, pursuing R&D in eco-friendly yarns for apparel and automotive sectors, with a focus on Asian markets and carbon footprint reduction initiatives.

- Teijin adopts a multi-material approach, combining bio-based polyesters with recycled fibers for sportswear and technical textiles, emphasizing technological advancements and strategic alliances to meet evolving environmental standards.

- Indorama Ventures concentrates on scaling bio-PET production using renewable feedstocks, targeting apparel and home textiles through vertical integration and sustainability certifications to enhance competitiveness in emerging markets.

- Lenzing prioritizes wood-based biopolymers like TENCEL, expanding into bioplastic blends for fashion and home furnishings, with strategies rooted in ethical sourcing and innovation to drive premium sustainable textile adoption.

What are the Market Trends in the Bioplastic Textile Market?

- Integration of bioplastic textiles into mainstream apparel collections to meet consumer demands for eco-friendly fashion.

- Advancements in biopolymer technology are improving textile performance, such as enhanced flexibility and durability.

- Increasing collaborations between biotech firms and textile manufacturers for the scalable production of bio-based fibers.

- Shift toward circular economy models emphasizing biodegradability and recyclability in textile supply chains.

- Rising adoption in the automotive and medical sectors for lightweight, sustainable interior materials.

- Government incentives and regulations promoting bio-based alternatives to reduce microplastic pollution.

- Expansion of feedstock diversity using agricultural waste to lower costs and improve supply resilience.

What Market Segments and their Subsegments are Covered in the Bioplastic Textile Report?

By Material

- PLA

- PHA

- Bio-PET

- Bio-PE

- PHB

- Starch Blends

- Bio-based Polyamides

- PBS

- Bio-based Polyesters

- Mycelium

- Others

By Application

- Apparel

- Home Textiles

- Industrial Textiles

- Automotive Textiles

- Medical Textiles

- Footwear

- Clothing

- Sportswear

- Packaging

- Consumer Goods

- Others

By End-User

- Fashion & Apparel Brands

- Sportswear Companies

- Home Furnishing Companies

- Automotive Industry

- Medical and Healthcare Sector

- Consumer Brands

- Institutional Buyers

- Technical Users

- Agriculture

- Electronics

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Bioplastic Textile Market - Industry Analysis

Chapter 4. Global Bioplastic Textile Market- Competitive Landscape

Chapter 5. Global Bioplastic Textile Market - Material Analysis

Chapter 6. Global Bioplastic Textile Market - Application Analysis

Chapter 7. Global Bioplastic Textile Market - End-User Analysis

Chapter 8. Bioplastic Textile Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Bioplastic textiles are fibers and fabrics produced from renewable biological sources like plants or bacteria, offering biodegradable or bio-based alternatives to traditional synthetic textiles with reduced environmental impact.

Key factors include rising environmental regulations, consumer demand for sustainable products, technological advancements in biopolymers, and corporate sustainability commitments across fashion and industrial sectors.

The bioplastic textile market is projected to grow from USD 1.8 billion in 2025 to USD 4.0 billion by 2035.

The market is expected to grow at a CAGR of 8.1% from 2026 to 2035.

Europe will contribute notably, holding around 40% market share due to strong regulatory support and high adoption rates.

Major players include NatureWorks, BASF, Toray, Teijin, Indorama Ventures, and Lenzing, driving growth through innovation and sustainable strategies.

The report provides comprehensive analysis including market size, trends, segmentation, regional insights, key players, and forecasts from 2026 to 2035.

Stages include raw material sourcing from renewable feedstocks, polymer production, fiber extrusion, textile manufacturing, distribution, and end-of-life management like composting or recycling.

Trends show a shift toward biodegradable fibers in apparel, with consumers preferring eco-friendly brands, and increasing focus on circular models for reduced waste.

Factors include bans on single-use plastics, EU Green Deal initiatives, and global carbon reduction targets, pushing adoption of bio-based materials for compliance and sustainability.