ABS Alloys Market Size, Share and Trends 2026 to 2035

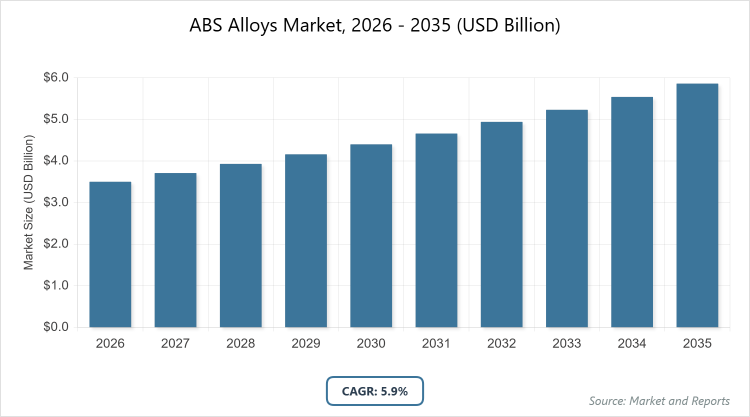

According to MarketnReports, the global ABS Alloys market size was estimated at USD 3.5 billion in 2025 and is expected to reach USD 6.2 billion by 2035, growing at a CAGR of 5.9% from 2026 to 2035. ABS Alloys Market is driven by increasing demand in the automotive and electronics sectors for lightweight and durable materials.

What are the Key Insights into ABS Alloys?

- The global ABS Alloys market was valued at USD 3.5 billion in 2025 and is projected to reach USD 6.2 billion by 2035.

- The market is expected to grow at a CAGR of 5.9% during the forecast period from 2026 to 2035.

- The market is driven by rising adoption in automotive for lightweight components, growth in electronics, and advancements in polymer blending technologies.

- In the type segment, Polycarbonate ABS Alloys (PC ABS Alloys) dominate with a 45% share due to their superior impact strength and heat resistance, ideal for automotive and electronics.

- In the application segment, Automotive Parts dominate with a 40% share as they provide durability and weight reduction, essential for fuel efficiency.

- In the end-user segment, the Automotive Industry dominates with a 35% share owing to high demand for interior and exterior components.

- Asia Pacific dominates the regional market with a 50% share, driven by manufacturing hubs in China, rapid industrialization, and cost-effective production.

What is the Industry Overview of ABS Alloys?

The ABS Alloys market encompasses blends of Acrylonitrile Butadiene Styrene (ABS) with other polymers to enhance properties such as impact resistance, heat tolerance, and chemical stability, used in applications requiring robust, lightweight materials. Market definition includes engineered thermoplastics like ABS/PC or ABS/PET that combine ABS’s toughness with additives for improved performance, catering to industries needing customized solutions for durability, aesthetics, and cost-efficiency while addressing challenges in processing, recyclability, and environmental compliance.

What are the Market Dynamics of ABS Alloys?

Growth Drivers

The ABS Alloys market is propelled by the automotive industry’s push for lightweight materials to improve fuel efficiency and reduce emissions, where ABS alloys offer excellent strength-to-weight ratios and moldability for complex parts like dashboards and bumpers. Advancements in blending technologies enhance properties like flame retardancy and UV resistance, expanding applications in electronics for durable casings and consumer goods. Rising demand in emerging economies for affordable, high-performance plastics in construction and appliances further drives growth. Sustainability trends favor recyclable ABS alloys, while R&D investments yield innovative formulations for harsh environments, boosting market adoption.

Restraints

High raw material costs for specialty polymers and volatility in styrene and acrylonitrile prices constrain market growth, particularly in price-sensitive regions. Environmental concerns over non-biodegradable plastics lead to regulatory restrictions on VOC emissions during production, increasing compliance expenses. Limited recycling infrastructure for blended alloys reduces appeal in eco-conscious markets. Competition from alternative materials like polypropylene and polycarbonate hinders penetration in certain applications. Supply chain disruptions from geopolitical tensions affect monomer availability, impacting production stability.

Opportunities

Opportunities lie in developing bio-based ABS alloys to meet sustainability demands, attracting investments from green manufacturing initiatives. Expansion into electric vehicles requires heat-resistant alloys for battery casings and interiors, opening new segments. Partnerships with 3D printing firms for custom prototypes can innovate product development. Emerging markets in Asia and Africa offer growth through urbanization and infrastructure projects needing durable coatings. Advancements in nanotechnology for enhanced properties like self-healing can differentiate offerings in high-end electronics.

Challenges

Challenges include intense competition from pure polymers and composites offering similar properties at lower costs, pressuring pricing strategies. Rapid technological changes demand continuous innovation, straining R&D budgets for smaller players. Regulatory variations across regions complicate global standardization and exports. Ensuring consistent quality in alloy blends requires advanced testing, increasing operational complexity. Environmental scrutiny on plastic waste necessitates eco-friendly alternatives, while talent shortages in polymer engineering hinder progress.

ABS Alloys Market: Report Scope

| Report Attributes | Report Details |

| Report Name | ABS Alloys Market |

| Market Size 2025 | USD 3.5 Billion |

| Market Forecast 2035 | USD 6.2 Billion |

| Growth Rate | CAGR of 5.9% |

| Report Pages | 210 |

| Key Companies Covered | LG Chem, CHIMEI, INEOS Styrolution, Formosa Plastics, BASF, Kumho Petrochemical, Lotte Chemical, Cheil Industries, and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of ABS Alloys?

The ABS Alloys market is segmented by type, application, end-user, and region.

By Type. Polycarbonate ABS Alloys (PC ABS Alloys) are the most dominant subsegment, holding approximately 45% market share, due to their balanced mechanical properties and versatility in high-impact applications. This dominance drives the market by enabling lightweight designs that meet stringent performance standards in automotive and electronics, reducing material costs and enhancing product lifespan. Polyethylene Terephthalate ABS Alloys (PET ABS alloys) rank as the second most dominant, with around 20% share, offering superior chemical resistance, propelling growth through applications in packaging and medical devices where durability is critical.

By Application. Automotive Parts emerges as the most dominant subsegment, capturing about 40% share, primarily because of the need for robust, lightweight components in vehicles. This leads to market growth by supporting fuel efficiency and design flexibility, crucial for modern automotive manufacturing. Electrical & Electronics follows as the second most dominant, with roughly 25% share, providing insulation and impact protection, driving the market via demand for reliable consumer devices.

By End-User. The automotive industry represents the most dominant subsegment at about 35% share, driven by requirements for interior and exterior durability. This dominance accelerates market expansion through volume production and innovation in electric vehicles. The electronics industry ranks second most dominant, holding around 25% share, due to needs for housing and components, contributing to growth via technological advancements in gadgets.

What are the Recent Developments in ABS Alloys?

- In September 2025, Formosa Plastics unveiled a USD 450 million plan for a 300 kt-per-year ABS plant in Louisiana, timed for 2028 and aimed at automotive and appliance accounts.

- In July 2025, INEOS Styrolution announced its decision to permanently close its ABS production site in Addyston, Ohio.

- In June 2025, LG Chem completed the expansion of ABS production capacity by 40%, targeting the automotive and electronics industries.

- In January 2024, Covestro partnered with Youyi Group to supply butyl acrylate and 2-ethylhexyl acrylate for adhesive materials, supporting ABS alloy production.

- In December 2023, CHIMEI invested $200 million in sustainable ABS production, reducing environmental impact.

What is the Regional Analysis of ABS Alloys?

- Asia Pacific to dominate the global market.

Asia Pacific holds the largest share at approximately 35%, with China as the dominating country, due to rapid industrialization, massive manufacturing bases, and government initiatives promoting infrastructure development. This region’s growth is fueled by low-cost labor, abundant raw materials, and increasing investments in oil & gas and mining, positioning it as a key hub for coating production and consumption. High urbanization rates drive demand in the construction and transportation sectors. India’s Make in India campaign boosts local manufacturing of coatings.

Southeast Asian nations like Vietnam expand through foreign direct investments. Environmental policies push for low-VOC innovations. Strong export networks enhance global supply chains. The region’s diverse climate conditions require versatile coatings for humidity and corrosion resistance. Vocational training programs improve application skills across industries. Rising middle-class consumption increases demand in consumer goods protection.

North America follows closely, driven by advanced technological adoption and stringent safety standards, where the United States dominates through its robust energy sector and R&D investments. Growth stems from shale gas exploration and renewable energy projects requiring durable coatings, though higher costs moderate expansion. Canadian oil sands operations demand specialized solutions for harsh climates. Government subsidies for green energy promote sustainable coatings.

The region’s focus on aerospace and automotive industries requires high-performance materials. Collaborations between universities and companies foster innovation in nanotechnology. Strict OSHA regulations ensure worker safety in application processes. The growth of e-commerce facilitates faster distribution of coating products. Investments in infrastructure renewal projects, like bridges and pipelines, amplify demand. Emphasis on domestic manufacturing reduces import dependencies.

Europe exhibits strong performance with emphasis on sustainability and regulation, led by Germany through its engineering excellence and firms like BASF. The region’s expansion benefits from EU environmental policies favoring low-VOC coatings and a focus on marine and power industries. Horizon Europe funds research in eco-friendly formulations.

The UK’s offshore wind farms increase demand for marine protection. Multilingual compliance aids exports to diverse markets like France and Italy. Circular economy initiatives recycle coating waste, reducing environmental impact. REACH regulations drive safer chemical usage in production. Collaborative industry consortia share best practices for application efficiency. The region’s aging infrastructure requires retrofitting with advanced coatings. Focus on renewable energy transitions boosts wind and solar component protections.

Latin America shows steady but moderate advancement, dominated by Brazil’s oil & gas and mining sectors, supported by foreign investments, though limited by economic fluctuations. Mexico benefits from NAFTA ties, enhancing trade with North America for supply chains. Government infrastructure plans in Argentina promote road and bridge protection. The rise of renewable projects in Chile creates niches for wind turbine coatings. However, political instability affects consistent investments.

Emerging mining in Peru demands wear-resistant solutions for equipment. Regional trade agreements like Mercosur facilitate cross-border material supply. Vocational programs in Colombia build skills for industrial applications. Biodiversity concerns push for eco-friendly coatings in sensitive areas. Growing urban centers increase construction-related demand.

The Middle East and Africa remain emerging, with the United Arab Emirates and Saudi Arabia leading through oil-funded infrastructure, constrained by lower diversification but showing potential via energy projects. Vision 2030 in Saudi Arabia invests in downstream chemical processing. South Africa’s mining industry adopts conveyor and pump protections.

Technology transfers from European partners build local expertise in Egypt. However, water scarcity influences waterborne coating preferences. Investments in solar farms create demand for dust-resistant surfaces in arid areas. OPEC policies affect the oil & gas sector stability. Vocational training initiatives in Nigeria improve workforce capabilities. Emerging ports in Kenya require marine coatings for trade growth. Focusing on sustainable development goals promotes green innovations in the region.

What are the Key Market Players in ABS Alloys?

- LG Chem. LG Chem focuses on expanding production capacity for high-performance ABS alloys, targeting automotive and electronics through sustainable innovations and strategic partnerships.

- CHIMEI. CHIMEI invests in eco-friendly ABS production, emphasizing reduced environmental impact and supplying high-quality alloys for consumer goods and appliances.

- INEOS Styrolution. INEOS Styrolution optimizes operations by closing inefficient sites and focusing on high-margin specialty ABS alloys for automotive applications.

- Formosa Plastics. Formosa Plastics pursues large-scale plant expansions in key markets like the U.S., aiming to meet growing demand in automotive and consumer sectors.

- BASF. BASF develops advanced polymer blends, leveraging R&D for flame-retardant and heat-resistant ABS alloys used in electrical and industrial applications.

- Kumho Petrochemical. Kumho Petrochemical emphasizes cost-effective production and supply chain efficiency for ABS alloys in electronics and packaging.

- Lotte Chemical. Lotte Chemical invests in R&D for bio-based ABS alloys, targeting sustainable solutions for automotive interiors.

- Cheil Industries. Cheil Industries focuses on high-impact ABS alloys for consumer electronics, pursuing global expansion through acquisitions.

What are the Market Trends in ABS Alloys?

- Increasing adoption of bio-based and recyclable ABS alloys for sustainability.

- Growth in flame-retardant ABS for electronics and automotive safety.

- Rise of high-heat-resistant alloys for under-hood applications.

- Expansion of lightweight ABS/PC blends in electric vehicles.

- Integration of nanotechnology for enhanced mechanical properties.

- Shift toward low-VOC formulations to meet environmental regulations.

What Market Segments and Subsegments are Covered in the ABS Alloys Report?

By Type

- Polycarbonate ABS Alloys (PC ABS Alloys)

- Polyethylene Terephthalate ABS Alloys (PET ABS alloys)

- Polybutylene Terephthalate ABS Alloys

- Polyamide ABS Alloys

- Polyvinyl Chloride ABS Alloys

- Polystyrene ABS Alloys

- Acrylic ABS Alloys

- Flame Retardant ABS Alloys

- High Impact ABS Alloys

- Heat-Resistant ABS Alloys

- Others

By Application

- Automotive Parts

- Electrical & Electronics

- Architectural Components

- Consumer Goods

- Industrial Machinery

- Medical Devices

- Packaging

- Furniture

- Appliances

- Toys

- Others

By End-User

- Automotive Industry

- Electronics Industry

- Construction Industry

- Consumer Goods Industry

- Healthcare Industry

- Manufacturing Industry

- Aerospace Industry

- Marine Industry

- Oil & Gas Industry

- Chemical Industry

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

ABS Alloys are blended thermoplastics combining Acrylonitrile Butadiene Styrene with other polymers for enhanced properties like impact resistance and heat tolerance.

Key factors include automotive lightweighting, electronics growth, sustainable materials demand, and technological advancements in polymer blending.

The market is projected to grow from USD 3.5 billion in 2025 to USD 6.2 billion by 2035.

The CAGR is expected to be 5.9%.

Asia Pacific will contribute notably, holding around 50% share due to manufacturing dominance.

Major players include LG Chem, CHIMEI, INEOS Styrolution, Formosa Plastics, and BASF.

The report provides detailed analysis of size, trends, segments, regional outlook, key players, and forecasts.

Stages include raw material sourcing, polymer blending, extrusion, molding, distribution, and end-use application.

Trends evolve toward sustainable and high-performance alloys, with preferences for lightweight, durable materials.

Regulations on VOC emissions and environmental pushes for recyclable alloys influence production and adoption.