Specialty Optical Fibers Market Size, Share and Trends 2026 to 2035

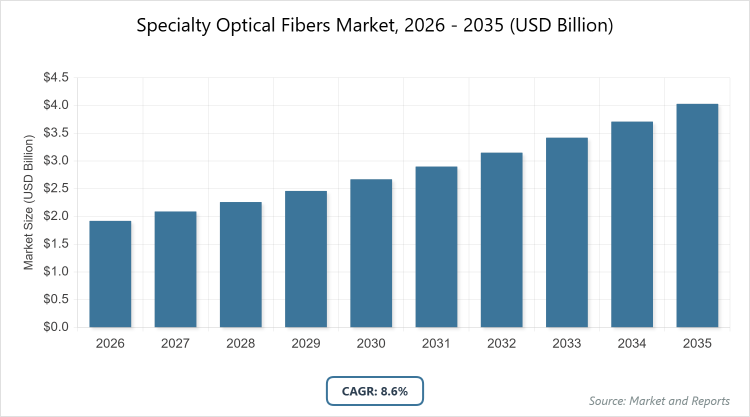

According to MarketnReports, the global Specialty Optical Fibers market size was estimated at USD 1.92 billion in 2025 and is expected to reach USD 4.50 billion by 2035, growing at a CAGR of 8.6% from 2026 to 2035. Specialty Optical Fibers Market is driven by increasing demand for high-speed data transmission and advancements in telecommunications infrastructure.

What are the Key Insights into Specialty Optical Fibers?

- The global specialty optical fibers market size was valued at USD 1.92 billion in 2025 and is projected to reach USD 4.50 billion by 2035.

- The market is expected to grow at a CAGR of 8.6% during the forecast period from 2026 to 2035.

- The market is driven by rising demand for high-speed data transmission, 5G network expansion, and advancements in medical and industrial applications.

- In the product type segment, single-mode fiber dominates with a 60% share due to its ability to transmit data over long distances with minimal loss, making it ideal for telecommunications and high-bandwidth needs.

- In the application segment, telecommunications holds the largest share at 35% owing to the surge in internet penetration and data center growth, which require robust fiber solutions for efficient connectivity.

- In the end-user segment, telecom operators lead with a 40% share because of their extensive investments in infrastructure upgrades to support IoT and cloud computing.

- North America dominates the regional market with a 33% share, driven by advanced technological infrastructure, high adoption of 5G, and presence of major data centers in the U.S.

What is the Industry Overview of Specialty Optical Fibers?

The specialty optical fibers market encompasses advanced fiber optic technologies designed for specific applications beyond standard telecommunications, including high-performance data transmission, sensing, and medical uses. These fibers are engineered with unique properties such as enhanced durability, low signal loss, or resistance to extreme environments, distinguishing them from conventional optical fibers. Market definition includes fibers like single-mode, multi-mode, and specialty variants used in sectors such as healthcare, defense, oil & gas, and industrial sensing, where they enable reliable, high-bandwidth connectivity and precise signal delivery in challenging conditions.

What are the Market Dynamics of Specialty Optical Fibers?

Growth Drivers

The primary growth driver for the specialty optical fibers market is the escalating demand for high-speed and reliable data transmission fueled by the global rollout of 5G networks and the proliferation of data centers. As industries increasingly rely on real-time data processing for applications like IoT and cloud computing, specialty fibers provide the necessary bandwidth and low latency, enabling seamless connectivity in telecommunications and beyond. Additionally, advancements in fiber technology, such as improved resistance to environmental factors, are expanding their use in harsh conditions, further accelerating market expansion across sectors like oil & gas and defense.

Restraints

High installation and manufacturing costs pose a significant restraint to the specialty optical fibers market, as the production of these advanced fibers requires specialized materials and precision engineering, leading to elevated prices compared to standard optical fibers. This cost barrier limits adoption in price-sensitive regions and applications, particularly in emerging markets where infrastructure budgets are constrained. Moreover, the complexity of handling and deploying these delicate fibers can result in technical challenges, deterring smaller enterprises from investing in upgrades despite the long-term benefits.

Opportunities

Emerging opportunities in the specialty optical fibers market arise from the growing adoption of fiber optics in healthcare for minimally invasive procedures and diagnostic imaging, where fibers enable precise light delivery and sensing. The rise of telemedicine and remote monitoring, accelerated by global health trends, creates demand for biocompatible and flexible fibers. Furthermore, innovations in sustainable fiber materials, such as biodegradable options, align with environmental regulations and open new avenues in eco-conscious industries like renewable energy, positioning the market for substantial growth through diversified applications.

Challenges

Supply chain disruptions and raw material shortages present ongoing challenges in the specialty optical fibers market, as the industry relies on high-purity silica and rare-earth elements that are vulnerable to geopolitical tensions and mining limitations. These issues can lead to production delays and increased costs, impacting market stability. Additionally, the need for skilled labor to install and maintain these advanced systems adds complexity, particularly in regions with limited technical expertise, hindering widespread deployment and market penetration.

Specialty Optical Fibers Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Specialty Optical Fibers Market |

| Market Size 2025 | USD 1.92 Billion |

| Market Forecast 2035 | USD 4.50 Billion |

| Growth Rate | CAGR of 8.6% |

| Report Pages | 220 |

| Key Companies Covered |

Corning Incorporated, Fujikura Ltd., Furukawa Electric Co., LEONI, YOFC, Nufern, Hengtong Group, Fiberguide, FiberHome, Fibercore, and Others |

| Segments Covered | By Product Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Specialty Optical Fibers?

The Specialty Optical Fibers market is segmented by product type, application, end-user, and region.

Based on Product Type Segment: Single-mode fiber emerges as the most dominant subsegment, holding approximately 60% market share, due to its superior long-distance transmission capabilities with low signal attenuation, which drives the market by supporting high-bandwidth applications in telecommunications and data centers. Multi-mode fiber is the second most dominant, with around 30% share, as it excels in short-range, high-data-rate environments like local networks, contributing to market growth by enabling cost-effective solutions for enterprise and industrial settings.

Based on Application Segment: Telecommunications stands out as the most dominant subsegment with about 35% share, propelled by the need for robust infrastructure in 5G and broadband expansion, driving overall market growth through enhanced global connectivity. Healthcare & medical devices is the second most dominant at roughly 25%, owing to the fibers’ precision in endoscopic and surgical tools, which boosts the market by facilitating advancements in minimally invasive procedures and diagnostic accuracy.

Based on End-User Segment: Telecom operators dominate with a 40% share, driven by massive investments in network upgrades for IoT and cloud services, propelling market expansion through increased demand for reliable, high-speed fibers. Military & defense follows as the second most dominant with 20% share, as these fibers provide secure, resilient communication in extreme conditions, contributing to growth by supporting advanced sensing and surveillance technologies.

What are the Recent Developments in Specialty Optical Fibers?

- In November 2025, Exail launched a new erbium/ytterbium co-doped fiber, enhancing power scalability for free-space communication systems, with demonstrated 30W output over 700 hours, advancing applications in LiDAR and quantum technologies.

- In January 2024, OFS introduced the Dual-Band LaserWave OM4+ multimode optical fiber, complementing OM5 and OM4 lines with superior attenuation and bandwidth, targeting high-performance data center and enterprise networks.

- In March 2024, Furukawa Electric collaborated with Movistar to deploy InvisiLight technology, providing easy-to-install, aesthetically preserving fiber optics for buildings, boosting adoption in telecommunications.

What is the Regional Analysis of Specialty Optical Fibers?

North America to dominate the global market.

North America leads the specialty optical fibers market, driven by robust technological infrastructure and high 5G adoption, with the U.S. as the dominating country due to its extensive data centers and innovation hubs like Silicon Valley, fostering rapid deployment in telecom and defense sectors.

Asia Pacific follows as a high-growth region, fueled by industrialization and digital initiatives, where China dominates through massive investments in fiber networks and manufacturing, supporting 5G rollout and smart city projects across urban centers.

Europe exhibits steady expansion, supported by stringent regulations and renewable energy focus, with Germany as the key country owing to its advanced industrial base and emphasis on precision engineering for applications in healthcare and automotive.

Latin America shows emerging potential amid improving connectivity, led by Brazil’s telecom upgrades and oil & gas explorations, which drive demand for durable fibers in remote and harsh environments.

The Middle East and Africa region grows through infrastructure developments, with the UAE dominating via smart city initiatives in Dubai, leveraging fibers for surveillance and energy management in arid conditions.

Who are the Key Market Players in Specialty Optical Fibers?

- Corning Incorporated focuses on innovation through R&D investments in advanced fiber technologies like ClearCurve fibers, expanding its portfolio via strategic alliances and acquisitions to enhance global market presence in telecom and data centers.

- Fujikura Ltd. emphasizes high-performance manufacturing and sustainability, adopting eco-friendly production methods while partnering with telecom giants for 5G deployments, strengthening its position in Asia Pacific through localized supply chains.

- Furukawa Electric Co. pursues vertical integration by developing specialized fibers for industrial applications, leveraging collaborations like with Movistar to penetrate emerging markets and prioritize reliability in defense and oil & gas sectors.

- LEONI adopts a customer-centric approach with customized fiber solutions, investing in automation for efficient production and forming joint ventures to tap into Europe’s growing healthcare and automotive demands.

- YOFC (Yangtze Optical Fibre and Cable) leverages cost-effective scaling in China, focusing on export expansion and R&D in rare-earth doped fibers to compete globally in high-speed networks.

- Nufern specializes in laser and amplifier fibers, employing acquisition strategies to broaden its defense and medical offerings, while emphasizing quality certifications for international compliance.

- Hengtong Group drives growth through massive infrastructure projects, adopting green manufacturing and digital twins for optimization, targeting Africa’s connectivity initiatives.

- Fiberguide prioritizes precision engineering for sensing applications, using partnerships with research institutions to innovate in quantum technologies and expand in North America.

- FiberHome focuses on integrated solutions for smart cities, investing in AI-driven design to reduce latency, and forming alliances for submarine cable projects.

- Fibercore (Humanetics) targets niche markets like aerospace with polarization-maintaining fibers, employing mergers to enhance sensor capabilities and focus on U.S. military contracts.

What are the Market Trends in Specialty Optical Fibers?

- Integration of optical amplifiers to boost signal efficiency in long-haul networks.

- Adoption of biodegradable and eco-friendly fibers aligning with sustainability goals.

- Rise of polarization-maintaining fibers for enhanced telecom reliability.

- Expansion of fiber-to-the-home initiatives driven by broadband demand.

- Increasing use in quantum computing and LiDAR for advanced sensing.

- Development of hollow-core fibers for reduced latency in 5G applications.

- Growth in medical applications for minimally invasive tools.

- Focus on high-vibration resistant fibers for industrial environments.

- Emergence of AI-optimized fiber designs for data centers.

- Shift toward multi-core fibers for higher data capacity.

What Market Segments and their Subsegments are Covered in the Specialty Optical Fibers Report?

By Product Type

-

Multimode Fiber

-

Singlemode Fiber

-

Photonic Crystal Fiber

-

Rare Earth Doped Fiber

-

Polarization Maintaining Fiber

-

Dispersion Compensating Fiber

-

Nonlinear Fiber

-

Plastic Optical Fiber

-

Chalcogenide Fiber

-

Sapphire Fiber

-

Others

By Application

- Telecommunications

- Medical

- Industrial Sensing

- Defense

- Oil & Gas

- Energy

- Rail Transit

- Data Centers

- Automotive

- Aerospace

- Others

By End-User

- Telecom Operators

- Hospitals & Clinics

- Oil Companies

- Military

- Manufacturers

- Automotive Industry

- Rail Operators

- Data Center Providers

- Aerospace Companies

- Research Institutions

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

Specialty optical fibers are advanced optical cables engineered for specific high-performance applications, featuring unique properties like enhanced durability, low attenuation, or environmental resistance, used in sectors such as telecom, healthcare, and defense.

Key factors include 5G expansion, rising IoT adoption, demand for high-bandwidth data transmission, advancements in medical devices, and infrastructure developments in emerging markets.

The market is projected to grow from USD 2.06 billion in 2026 to USD 4.50 billion by 2035.

The CAGR is expected to be 8.6% from 2026 to 2035.

North America will contribute notably, driven by technological advancements and high infrastructure investments.

Major players include Corning Incorporated, Fujikura Ltd., Furukawa Electric Co., LEONI, and YOFC.

The report provides comprehensive analysis including market size, forecasts, segments, trends, key players, and regional insights.

Stages include raw material sourcing, fiber manufacturing, coating and assembly, testing, distribution, and end-user integration.

Trends lean toward sustainable, high-capacity fibers, with preferences shifting to eco-friendly materials and solutions supporting 5G and remote healthcare.

Regulations on data security and environmental standards promote sustainable manufacturing, while climate concerns drive demand for resilient fibers in extreme conditions.