Food Contact Paper Market Size, Share and Trends 2026 to 2035

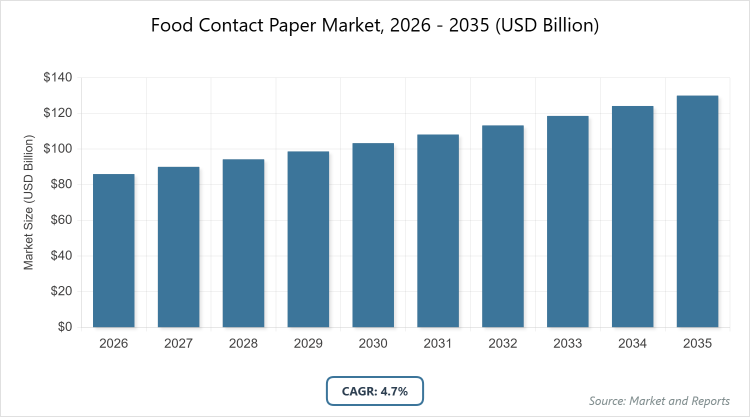

According to MarketnReports, the global Food Contact Paper market size was estimated at USD 86 billion in 2025 and is expected to reach USD 137 billion by 2035, growing at a CAGR of 4.7% from 2026 to 2035. Food Contact Paper Market is driven by growing demand for eco-friendly and sustainable packaging solutions.

What are the Key Insights into Food Contact Paper Market?

- The global food contact paper market was valued at USD 86 billion in 2025 and is projected to reach USD 137 billion by 2035.

- The market is expected to grow at a CAGR of 4.7% during the forecast period from 2026 to 2035.

- The market is driven by increasing consumer preference for sustainable packaging alternatives to plastic, coupled with stringent regulations on single-use plastics.

- In the type segment, kraft paper dominates with a 40% share due to its superior strength, recyclability, and versatility in applications like grocery bags and food wrapping.

- In the application segment, fresh produce dominates with a 30% share owing to the rising demand for eco-friendly packaging for fruits and vegetables that extends shelf life and reduces waste.

- In the end-user segment, fast food outlets dominate with a 35% share because of the high volume of takeaway and delivery services requiring lightweight, disposable, and compliant packaging.

- Asia Pacific dominates the regional market with a 35% share, attributed to rapid urbanization, expansion of the food service industry in countries like China and India, and government initiatives banning plastic packaging.

What is the Industry Overview of Food Contact Paper Market?

The food contact paper market encompasses materials specifically designed for direct interaction with food products, ensuring safety, hygiene, and preservation while complying with stringent regulatory standards. This market includes various types of paper used in packaging, wrapping, and containment applications within the food industry, focusing on properties like grease resistance, moisture barrier, and non-toxicity to prevent contamination. Market definition refers to paper-based products certified for food contact, excluding plastics or metals, and emphasizes sustainability as a core attribute amid rising environmental concerns.

What are the Market Dynamics of Food Contact Paper Market?

Growth Drivers

The primary growth drivers in the food contact paper market include the surging demand for sustainable and biodegradable packaging solutions, driven by heightened environmental awareness among consumers and businesses alike. Governments worldwide are imposing bans and restrictions on single-use plastics, prompting a shift towards paper-based alternatives that are recyclable and compostable, thereby reducing carbon footprints and aligning with circular economy principles. Additionally, the expansion of the food delivery and e-commerce sectors, accelerated by changing lifestyles and the post-pandemic surge in online food ordering, has increased the need for efficient, hygienic, and customizable packaging that maintains food quality during transit. Innovations in coating technologies, such as plant-based barriers, further enhance the functionality of food contact paper, making it suitable for a wider range of applications and contributing to market expansion.

Restraints

Key restraints impacting the food contact paper market revolve around concerns over chemical migration and health risks associated with certain additives used to improve paper properties like grease resistance. Regulatory bodies enforce rigorous testing, but uncertainties about long-term effects of these chemicals, including potential endocrine disruption, deter widespread adoption in sensitive applications. Moreover, the higher production costs of specialized food contact paper compared to traditional plastics can limit market penetration in price-sensitive regions, especially where raw material fluctuations in pulp and fiber affect pricing stability. Supply chain disruptions, such as those from global events or raw material shortages, also pose challenges, hindering scalability and consistent availability for manufacturers.

Opportunities

Opportunities in the food contact paper market are abundant, particularly with the globalization of food trade requiring versatile packaging that meets diverse international standards for safety and sustainability. The rise of innovative products, like PFAS-free and compostable papers, opens doors for market players to capture shares in emerging segments such as ready-to-eat meals and organic foods, where consumers prioritize eco-friendly options. Expansion in developing economies, fueled by urbanization and increasing disposable incomes, presents untapped potential for customized solutions in food service and retail. Partnerships with e-commerce platforms and investments in R&D for advanced barrier technologies can further drive growth, enabling companies to differentiate and address evolving consumer demands for transparent, traceable, and low-impact packaging.

Challenges

Challenges in the food contact paper market include navigating complex and varying regulatory landscapes across regions, which demand extensive certification and compliance testing to ensure non-toxicity and safety. The need for continuous innovation to match the performance of plastic alternatives, such as superior moisture and grease resistance without compromising recyclability, strains R&D resources. Environmental factors, like deforestation concerns tied to pulp sourcing, require sustainable forestry practices to maintain credibility. Additionally, market volatility from fluctuating raw material prices and competition from alternative materials, such as bioplastics, challenge profitability and long-term planning for stakeholders.

Food Contact Paper Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Food Contact Paper Market |

| Market Size 2025 | USD 86 Billion |

| Market Forecast 2035 | USD 137 Billion |

| Growth Rate | CAGR of 4.7% |

| Report Pages | 220 |

| Key Companies Covered |

Mondi Plc, Twin Rivers Paper Company, Nordic Paper, Westrock Company, Smurfit Kappa, Stora Enso, Ahlstrom-Munksjo, Nippon Paper Industries, and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Food Contact Paper Market?

The Food Contact Paper market is segmented by type, application, end-user, and region.

Based on Type Segment, kraft paper emerges as the most dominant subsegment, commanding a significant market share due to its robustness, cost-effectiveness, and eco-friendly nature derived from renewable wood pulp, which makes it ideal for heavy-duty applications like food containers and bags. The second most dominant is greaseproof paper, valued for its oil-resistant properties achieved through mechanical processing, without heavy chemical reliance, enabling its use in wrapping fatty foods while promoting sustainability; both drive the market by addressing the need for durable, recyclable alternatives to plastics, reducing environmental impact and meeting consumer demands for green packaging that enhances food preservation and safety.

Based on Application Segment, fresh produce stands out as the most dominant, driven by the preference for breathable, moisture-absorbent paper that prolongs shelf life of fruits and vegetables, aligning with retail trends toward minimal plastic use and organic presentation. Dry groceries follow as the second most dominant, utilizing sturdy paper for packaging staples like grains and sugars, offering protection against contaminants while being lightweight and recyclable; these segments propel market growth by catering to the surge in sustainable retail practices and e-commerce deliveries, where efficient, customizable packaging reduces waste and supports global efforts to curb plastic pollution.

Based on End-User Segment, fast food outlets are the most dominant, leveraging disposable, grease-resistant paper for quick-service items like burgers and fries, which supports high-volume operations and complies with hygiene standards amid rising takeaway demand. Hotels & restaurants rank as the second most dominant, employing versatile paper for liners, wraps, and trays to enhance presentation and sustainability in dining experiences; together, they fuel market expansion by integrating eco-conscious materials into food service workflows, responding to regulatory pressures and consumer shifts toward responsible consumption that minimizes environmental footprints.

What are the Recent Developments in Food Contact Paper Market?

- In October 2024, UPM Specialty Papers collaborated with Eastman to launch a fully compostable paper-based packaging solution featuring a biobased coating, aimed at providing sustainable alternatives for food wrapping and reducing reliance on traditional plastics.

- In November 2024, Smurfit Kappa Group acquired a specialty paper mill in Southeast Asia, enhancing its production capacity for high-barrier, PFAS-free food contact papers to address increasing demand in the region for compliant and eco-friendly packaging.

- In January 2025, Ahlstrom Oyj introduced a new line of fully compostable and recyclable grease-resistant papers using a proprietary plant-based coating, offering a viable substitute for fluorochemical-treated products in bakery and fast food applications.

- In April 2025, International Paper Co. announced a major investment in its North American facilities to upgrade pulp-processing technology, boosting its ability to produce recycled-content papers that meet updated FDA food safety regulations.

- In March 2024, ProAmpac LLC acquired UP Paper LLC to expand its portfolio of food-safe paper products, strengthening its market position in sustainable packaging for the food industry.

What is the Regional Analysis of Food Contact Paper Market?

Asia Pacific to dominate the global market.

Asia Pacific holds the dominant position in the food contact paper market, with China leading as the key country due to its massive food production scale, rapid urbanization, and stringent plastic ban policies set for full implementation by 2025, driving widespread adoption of paper alternatives in packaging for exports and domestic consumption. India follows closely, propelled by expanding food service sectors and government initiatives promoting biodegradable materials, which enhance market penetration through affordable, customizable solutions for diverse applications like street food and e-commerce deliveries.

North America exhibits strong growth, with the United States as the dominating country, fueled by the booming takeout and delivery industries, consumer demand for sustainable options, and innovations in coated papers that comply with FDA standards, supporting a shift from plastics in retail and foodservice. Canada contributes through its emphasis on recyclable materials, driven by environmental regulations and increasing exports of packaged goods.

Europe maintains a significant share, led by Germany, where strict EU regulations on single-use plastics and high consumer awareness of ecological issues accelerate the use of certified food contact paper in bakery and dairy sectors. France and the UK bolster the region with investments in R&D for advanced barrier technologies, aligning with sustainability goals and reducing dependency on non-renewable resources.

Latin America is emerging rapidly, with Brazil as the dominant country, supported by foreign investments in food processing and proximity to North American markets, fostering demand for cost-effective paper packaging in agriculture and exports. Mexico aids growth through manufacturing hubs focused on compliant, eco-friendly solutions for cross-border trade.

The Middle East and Africa show promising expansion, dominated by Saudi Arabia, where rising food industries and government programs for bio-based packaging drive adoption in hospitality and retail. The UAE enhances the region with regulatory support for sustainable wraps, addressing urbanization and tourism-driven food consumption needs.

What are the Key Market Players in Food Contact Paper Market?

- Mondi Plc focuses on innovation through launches like EcoVantage kraft paper made from recycled fibers for dry food packaging and investments in new production facilities to expand sustainable flexible packaging, aiming to reduce plastic waste and capture demand in e-commerce and food delivery sectors.

- Twin Rivers Paper Company emphasizes expanding PFAS-free and fluorochemical-free product lines under the EcoBarrier brand, targeting fast food services transitioning away from chemical-based grease-proofing, while prioritizing R&D to enhance environmental compliance and market share in North America.

- Nordic Paper pursues acquisitions such as Glassine Canada Inc. to strengthen its North American presence and develops natural greaseproof papers without fluorochemicals, focusing on sustainable alternatives that meet global regulations and appeal to eco-conscious consumers in bakery and takeaway applications.

- Westrock Company leverages mergers and process innovations to lower costs and improve product quality, adopting sustainable practices to meet end-user demands in food packaging while investing in recyclable materials to align with circular economy trends.

- Smurfit Kappa acquires specialty mills to boost production of high-barrier papers and collaborates on PFAS-free solutions, emphasizing R&D for lightweight, compliant packaging that supports food safety and reduces environmental impact in Asia and Europe.

- Stora Enso forms joint ventures for renewable product development and focuses on next-generation papers with enhanced recyclability, targeting food contact applications to drive sustainability and competitive positioning in mature markets.

- Ahlstrom-Munksjo introduces plant-based coated papers for grease resistance and invests in compostable innovations, aiming to replace traditional treatments and expand in segments like bakery through regulatory-compliant, eco-friendly offerings.

- Nippon Paper Industries enhances barrier technologies for Asian markets, focusing on cost-effective, recyclable papers for fresh produce and dry goods, while adapting to regional plastic bans to grow market share.

What are the Market Trends in Food Contact Paper Market?

- Increasing shift toward PFAS-free and fluorochemical-free papers, driven by health concerns and regulations, promoting plant-based coatings for grease resistance in bakery and fast food packaging.

- Rising adoption of compostable and recyclable solutions, such as biobased barrier papers, to align with global sustainability goals and reduce plastic dependency in food delivery.

- Growth in e-commerce and online food ordering, boosting demand for customizable, lightweight paper packaging that ensures hygiene and product integrity during transit.

- Innovations in laminated and coated papers to prevent leakages and extend shelf life, particularly for fresh produce and liquid foods, enhancing functionality without compromising eco-friendliness.

- Expansion of AI-enabled smart packaging for predicting spoilage and optimizing barrier formulations, improving food safety and appealing to tech-savvy consumers.

- Focus on circular economy practices, including recycled-content papers, to lower carbon footprints and meet corporate sustainability targets in the food industry.

What Market Segments and their Subsegments are Covered in the Food Contact Paper Report?

- By Type

- Kraft Paper

- Greaseproof Paper

- Glassine Paper

- Parchment Paper

- Others

- By Application

- Fresh Produce

- Dry Groceries

- Bakery Products

- Liquid Food and Drinks

- Takeaway and Vending Foods

- Others

- By End-User

- Hotels & Restaurants

- Bakeries & Cafes

- Fast Food Outlets

- Cinemas & Theaters

- Airline & Railway Catering

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

Food contact paper refers to specialized paper materials designed for direct interaction with food, ensuring safety, non-toxicity, and compliance with regulations while providing properties like grease resistance and moisture barriers for packaging and wrapping applications.

Key factors include rising demand for sustainable packaging, bans on single-use plastics, expansion of food delivery services, innovations in eco-friendly coatings, and increasing consumer awareness of environmental impacts.

The market is projected to grow from approximately USD 90 billion in 2026 to USD 137 billion by 2035.

The CAGR is expected to be 4.7% during the forecast period.

Asia Pacific will contribute notably, driven by rapid food industry growth and plastic bans in countries like China and India.

Major players include Mondi Plc, Twin Rivers Paper Company, Nordic Paper, Westrock Company, Smurfit Kappa, Stora Enso, Ahlstrom-Munksjo, and Nippon Paper Industries.

The report provides comprehensive analysis including market size, trends, segmentation, regional insights, key players, drivers, restraints, opportunities, and forecasts.

Stages include raw material sourcing (pulp and fibers), manufacturing (coating and processing), distribution, end-use application in food packaging, and recycling or disposal.

Trends are shifting toward PFAS-free, compostable papers, with consumers preferring sustainable, recyclable options that reduce plastic use and support eco-friendly food packaging.

Factors include stringent FDA and EU regulations on chemical safety, global plastic bans, and environmental policies promoting biodegradable materials to minimize pollution and health risks.