Edge AI Hardware Market Size, Share and Trends 2026 to 2035

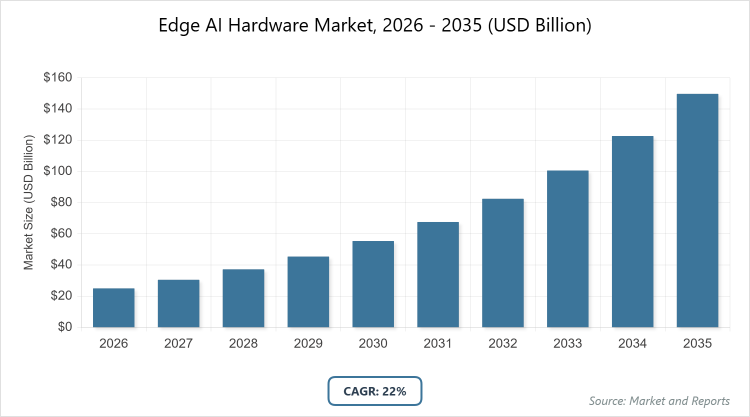

According to MarketnReports, the global Edge AI Hardware Market size was estimated at USD 25 billion in 2025 and is expected to reach USD 180 billion by 2035, growing at a CAGR of 22% from 2026 to 2035. Edge AI Hardware Market is driven by the increasing need for real-time data processing and low-latency applications in IoT and autonomous systems.What are the Key Insights of the Edge AI Hardware Market?

- The edge AI hardware market was valued at USD 25 billion in 2025 and is projected to reach USD 180 billion by 2035.

- The market is expected to grow at a CAGR of 22% during the forecast period from 2026 to 2035.

- The market is driven by growing deployment of IoT devices and demand for low-latency AI processing across industries.

- GPU dominates the processor segment with a 50% share because it offers superior parallel processing for complex AI workloads, enabling efficient handling of large datasets; Smartphones dominate the device type segment with a 35% share due to widespread integration of AI features like voice assistants and camera enhancements; Consumer Electronics dominates the end-use industry segment with a 30% share owing to the proliferation of smart devices requiring on-device intelligence for user personalization.

- North America dominates the market with a 38% share due to the presence of major technology innovators and substantial investments in AI research and development.

What is the Industry Overview of the Edge AI Hardware Market?

The edge AI hardware market involves the development and deployment of specialized computing components, such as processors, chips, and sensors, designed to perform artificial intelligence tasks directly on devices at the network's edge rather than relying on centralized cloud servers. Market definition encompasses hardware solutions that enable on-device AI inference and training, including GPUs, ASICs, NPUs, and other accelerators, which facilitate faster decision-making, enhanced data privacy, and reduced bandwidth usage in applications like autonomous vehicles, smart cities, and industrial automation. This market supports the shift toward decentralized computing by integrating AI capabilities into edge devices, addressing latency issues in real-time scenarios, and promoting efficiency in sectors where immediate data analysis is critical, ultimately fostering innovation in connected ecosystems and sustainable technology practices.

What are the Market Dynamics of the Edge AI Hardware Market?

Growth Drivers

The edge AI hardware market is propelled by the exponential rise in IoT devices and the need for instantaneous data analysis in applications such as smart manufacturing and healthcare monitoring. Technological advancements in semiconductor design, including more efficient processors and accelerators, allow for compact, power-efficient hardware that supports complex AI models at the edge, reducing dependency on cloud infrastructure and minimizing latency. Furthermore, the push for data privacy regulations and the desire to process sensitive information locally without transmission risks are accelerating adoption. Increasing investments from governments and enterprises in smart city initiatives and autonomous technologies also contribute significantly, as they require robust edge hardware to handle real-time computations in dynamic environments.

Restraints

Significant restraints include the high costs associated with developing and integrating advanced edge AI hardware, which can be prohibitive for small-scale enterprises and developing regions lacking sufficient infrastructure. Power consumption and thermal management challenges in compact devices limit the deployment of high-performance chips, potentially hindering scalability in battery-operated applications. Additionally, the complexity of optimizing AI models for diverse hardware architectures leads to compatibility issues and extended development timelines. Supply chain disruptions for critical components, such as semiconductors, further exacerbate delays and increase prices, while a shortage of skilled professionals in AI hardware design impedes innovation and widespread implementation.

Opportunities

Opportunities abound with the advent of 5G and emerging 6G networks, which enhance connectivity and enable more sophisticated edge AI applications in remote and mobile settings. The growing emphasis on sustainable computing opens doors for energy-efficient hardware innovations, such as neuromorphic chips that mimic human brain functions for lower power usage. Expansion into untapped sectors like agriculture and environmental monitoring presents potential for specialized solutions that leverage edge AI for precision tasks. Collaborations between hardware manufacturers and software developers can foster integrated ecosystems, while government incentives for domestic semiconductor production create avenues for localized manufacturing and reduced import dependencies.

Challenges

Challenges persist in achieving standardization across edge AI hardware platforms, as fragmented ecosystems complicate interoperability and increase integration costs for end-users. Ensuring robust security against cyber threats in distributed edge environments remains a critical issue, given the vulnerability of devices to attacks without centralized oversight. Balancing performance with cost-effectiveness in resource-constrained devices requires ongoing R&D, which can strain budgets. Moreover, evolving regulatory landscapes around AI ethics and environmental impact add compliance burdens, potentially slowing market entry for new innovations and affecting global supply chains.

Edge AI Hardware Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Edge AI Hardware Market |

| Market Size 2025 | USD 25 Billion |

| Market Forecast 2035 | USD 180 Billion |

| Growth Rate | CAGR of 22% |

| Report Pages | 220 |

| Key Companies Covered |

NVIDIA, Intel, Qualcomm, AMD, Huawei, Arm Holdings, and Others. |

| Segments Covered | By Processor, By Device Type, By End-Use Industry, and By Region. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 - 2024 |

| Forecast Year | 2026 - 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of the Edge AI Hardware Market?

The Edge AI Hardware Market is segmented by processor, device type, end-use industry, and region.By Processor Segment: The GPU segment dominates with a 50% share, as its architecture excels in parallel computing essential for training and inferencing large AI models, driving the market by enabling high-speed processing in data-intensive applications like video analytics. The ASIC segment is the second most dominant at 20%, offering customized efficiency and lower power consumption for specific tasks, which helps propel market growth through optimized performance in embedded systems and cost reductions over time.

By Device Type Segment: The Smartphones segment dominates with a 35% share, integrating advanced AI for features like real-time image recognition and natural language processing, which drives the market by boosting consumer demand for intelligent mobile experiences and encouraging hardware upgrades. The Surveillance Cameras segment is the second most dominant at 25%, providing on-device analytics for security and monitoring, contributing to market expansion by reducing bandwidth needs and enabling proactive threat detection in urban and industrial settings.

By End-Use Industry Segment: The Consumer Electronics segment dominates with a 30% share, leveraging edge AI for personalized devices like wearables and smart homes, propelling the market through mass adoption and innovation in user-centric technologies. The Automotive segment is the second most dominant at 25%, focusing on autonomous driving and safety systems, driving growth by enhancing vehicle intelligence and compliance with regulatory standards for real-time decision-making.

What are the Recent Developments in the Edge AI Hardware Market?

- In May 2025, Samsung released the Galaxy S25 series, including S25, S25+, S25 Ultra, and S25 Edge smartphones, which incorporate advanced edge AI capabilities via Galaxy AI for on-device processing and personalized user experiences.

- In September 2025, Tata Consultancy Services and Qualcomm launched an innovation lab in Bengaluru to co-develop scalable edge AI solutions using Qualcomm platforms, targeting smart and efficient applications across industries.

- In October 2025, NVIDIA, in collaboration with Booz Allen, Cisco, MITRE, ODC, and T-Mobile, introduced the first AI-native wireless stack for 6G, built on the NVIDIA AI Aerial platform to integrate AI across hardware and software.

- In November 2025, EdgeCortix closed an oversubscribed Series B financing round, raising total funding to over USD 110 million to support the global deployment of its SAKURA-II AI accelerator and upcoming SAKURA-X chiplet platform.

- In February 2025, Apple collaborated with educational institutions like UCLA’s Center for Education of Microchip Designers to strengthen AI and silicon engineering talent, supporting future edge AI hardware initiatives.

- In April 2024, Huawei Technologies entered a strategic partnership with the China Building Materials Federation and Conch Group to deploy edge AI solutions in manufacturing, telecom, and smart infrastructure for enhanced efficiency.

What is the Regional Analysis of the Edge AI Hardware Market?

North America to dominate the global market.North America maintains dominance in the edge AI hardware market, fueled by robust technological infrastructure, significant venture capital investments, and a concentration of leading semiconductor firms. The United States stands as the dominating country, where companies like NVIDIA and Intel drive innovation through extensive R&D in AI chips and collaborations with tech giants, supporting applications in autonomous vehicles and data centers while benefiting from policies like the CHIPS Act that bolster domestic production.

Asia Pacific emerges as the fastest-growing region, driven by rapid industrialization, expanding 5G networks, and government initiatives promoting digital transformation. China leads as the dominating country, with heavy investments in AI hardware manufacturing by firms like Huawei, enabling widespread adoption in smart cities and consumer electronics amid national strategies to achieve technological self-reliance.

Europe demonstrates strong growth through a focus on sustainable and regulated AI deployments, with emphasis on privacy-compliant hardware for industrial and healthcare sectors. Germany dominates the region, leveraging its engineering prowess and automotive industry leaders like Bosch to integrate edge AI in manufacturing and connected vehicles, supported by EU funding for green technology advancements.

Latin America shows promising expansion with increasing digitalization in agriculture and mining, where edge AI hardware aids in remote monitoring and efficiency gains. Brazil is the dominating country, adopting solutions for smart agriculture and urban security, driven by government programs to enhance connectivity and attract foreign tech investments.

The Middle East and Africa exhibit potential through oil & gas and smart city projects, utilizing edge AI for operational optimization and surveillance. The United Arab Emirates dominates, with initiatives in Dubai's smart ecosystem integrating hardware for AI-driven services in tourism and logistics, backed by substantial investments in innovation hubs.

What are the Key Market Players and Strategies in the Edge AI Hardware Market?

NVIDIA: NVIDIA emphasizes innovation in high-performance GPUs and accelerators like the Rubin platform, focusing on partnerships with cloud providers and AI software integration to reduce inference costs and expand into data centers and edge computing.

Intel: Intel pursues diversification through NPUs and open-source ecosystems, investing in foundry expansions and collaborations for energy-efficient chips to capture market share in enterprise and automotive applications.

Qualcomm: Qualcomm prioritizes mobile and IoT-focused processors like Snapdragon, leveraging 5G integration and strategic labs for co-development to enhance on-device AI for consumer devices and industrial solutions.

AMD: AMD concentrates on competitive ASICs and GPUs with advanced architectures, targeting cost-effective alternatives for data centers and edge servers through acquisitions and R&D in power optimization.

Huawei: Huawei focuses on self-reliant chip design and partnerships in manufacturing sectors, emphasizing secure, high-efficiency hardware for telecom and smart infrastructure to navigate global trade challenges.

Arm Holdings: Arm Holdings adopts a licensing model for customizable cores, collaborating with device manufacturers to enable scalable edge AI in wearables and IoT, driving adoption through energy-efficient designs.

What are the Market Trends in the Edge AI Hardware Market?

- Advancements in specialized AI chips like NPUs and ASICs for improved performance per watt in edge devices.

- Integration of 5G and 6G technologies enabling faster, low-latency AI processing in remote applications.

- Emphasis on energy-efficient hardware to support sustainable computing and battery-powered deployments.

- Rise of neuromorphic computing mimicking brain functions for ultra-low power AI tasks.

- Adoption of hybrid edge-cloud architectures for balanced workload distribution and scalability.

- Growth in model optimization techniques such as quantization to run complex AI on resource-limited hardware.

- Increasing focus on security features in hardware to protect against edge-specific cyber threats.

- Expansion of AI-native wireless stacks for seamless integration in telecommunications.

- Shift toward chiplet designs for modular, customizable hardware solutions.

- Regulatory-driven innovations addressing data privacy and ethical AI in hardware development.

What are the Market Segments and their Subsegments Covered in the Edge AI Hardware Market Report?

By Processor

- GPU

- ASIC

- NPU

- CPU

- FPGA

- VPU

- TPU

- Neuromorphic Chips

- Accelerators

- Sensors

- Others

By Device Type

- Smartphones

- Surveillance Cameras

- Robots

- Wearables

- Edge Servers

- Smart Speakers

- Automotive

- Smart Mirrors

- Drones

- Head-Mounted Displays

- Others

By End-Use Industry

- Consumer Electronics

- Automotive

- Aerospace and Defense

- Healthcare

- Industrial

- Retail

- Construction

- Energy and Utilities

- Government

- Telecommunications

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

The edge AI hardware market comprises specialized components like processors and chips that enable AI computations on devices at the network edge for real-time processing and efficiency.

Key factors include IoT proliferation, 5G advancements, demand for low-latency applications, and innovations in energy-efficient chips driving adoption across sectors.

The market is projected to grow from USD 25 billion in 2025 to USD 180 billion by 2035.

The CAGR is expected to be 22% from 2026 to 2035.

North America will contribute notably, holding a 38% share due to technological leadership and investments.

Major players include NVIDIA, Intel, Qualcomm, AMD, Huawei, and Arm Holdings.

The report offers detailed analysis of market size, trends, segments, regional outlooks, key players, and forecasts from 2026 to 2035.

Stages include raw material sourcing, chip design and manufacturing, assembly and integration, distribution, and end-user deployment with after-sales support.

Trends are moving toward efficient, specialized chips and hybrid architectures, with consumers preferring low-power, privacy-focused devices for seamless AI experiences.

Regulations on data privacy like GDPR and environmental pushes for green computing are promoting secure, energy-efficient hardware designs and sustainable manufacturing.