Shared Mobility Market Size, Share and Trends 2026 to 2035

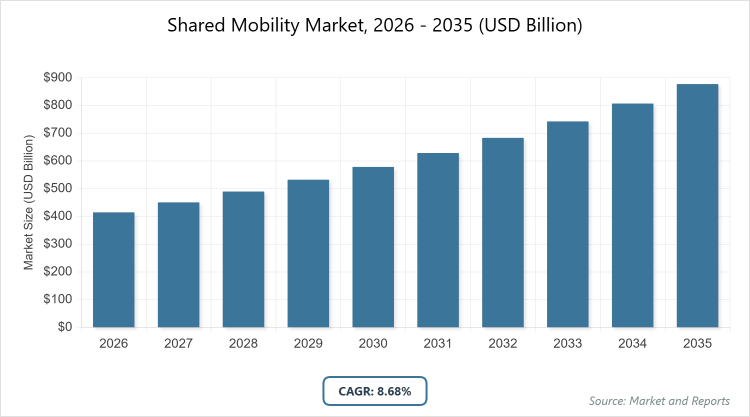

According to MarketnReports, the global Shared Mobility market size was estimated at USD 414.71 billion in 2025 and is expected to reach USD 953.73 billion by 2035, growing at a CAGR of 8.68% from 2026 to 2035. Increasing urbanization and demand for sustainable transportation options.

Key Insights

- The global shared mobility market size was valued at USD 414.71 billion in 2025 and is projected to reach USD 953.73 billion by 2035.

- The market is anticipated to grow at a CAGR of 8.68% during the forecast period from 2026 to 2035.

- The market is driven by rapid urbanization, environmental concerns, and technological advancements in app-based services.

- Ride-hailing dominates the type segment with a 55% share due to its convenience, widespread app adoption, and ability to address immediate urban transport needs.

- Urban mobility dominates the application segment with a 60% share because of high demand in congested cities for efficient, short-distance travel options.

- Personal end-use dominates with a 65% share owing to individual consumers seeking affordable, flexible alternatives to car ownership.

- Asia Pacific dominates the regional segment with a 54% share attributable to dense populations, rapid urbanization, and strong digital infrastructure in countries like China and India.

What is the Shared Mobility Market?

The shared mobility market refers to the ecosystem of transportation services where vehicles, rides, or resources are accessed on-demand and shared among multiple users, reducing the need for individual ownership. This includes ride-hailing, car-sharing, bike-sharing, and scooter-sharing platforms that leverage digital apps for seamless booking and payments. The market definition encompasses both peer-to-peer and business-operated models focused on efficient, cost-effective, and eco-friendly urban transport solutions, distinct from traditional public transit or private vehicle ownership, emphasizing flexibility and sustainability in modern mobility needs.

Market Dynamics

Growth Drivers

The shared mobility market’s growth is primarily driven by accelerating urbanization in emerging economies, where traffic congestion and limited parking push consumers toward efficient alternatives like ride-hailing and micromobility. Environmental regulations promoting low-emission transport, coupled with the integration of electric vehicles in fleets, further boost adoption by aligning with sustainability goals. Technological advancements, such as AI-driven route optimization and seamless app integrations, enhance user experience and operational efficiency, attracting tech-savvy millennials and Gen Z users who prioritize convenience over ownership.

Restraints

Restraints in the shared mobility market include stringent regulatory frameworks varying by region, such as licensing requirements and safety standards, which increase operational costs and delay expansions. Infrastructure limitations, particularly in developing areas lacking charging stations for EVs or dedicated lanes for bikes and scooters, hinder scalability. Additionally, concerns over data privacy and cybersecurity in app-based platforms erode user trust, while high initial investments in fleet electrification pose financial barriers for smaller operators.

Opportunities

Opportunities in the shared mobility market arise from the expansion of Mobility-as-a-Service (MaaS) platforms that integrate multiple transport modes into unified apps, offering seamless urban travel experiences. Partnerships with public transit systems and corporate sectors for employee commuting solutions can tap into untapped B2B segments. The rise of autonomous vehicles and AI analytics presents avenues for cost reductions and personalized services, while government incentives for green mobility in smart city projects encourage innovation and market entry in underserved rural areas.

Challenges

Challenges in the shared mobility market involve navigating inconsistent global regulations, where differing policies on vehicle standards and labor rights complicate cross-border operations. Ensuring vehicle maintenance and hygiene, especially post-pandemic, demands significant resources amid fluctuating demand. Intense competition from established players like Uber and local rivals leads to price wars, squeezing margins, while addressing equity issues, such as accessibility in low-income areas, requires strategic investments to avoid market fragmentation.

Shared Mobility Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Shared Mobility Market |

| Market Size 2025 | USD 414.71 Billion |

| Market Forecast 2035 | USD 953.73 Billion |

| Growth Rate | CAGR of 8.68% |

| Report Pages | 220 |

| Key Companies Covered |

Uber Technologies Inc., Didi Chuxing, Lyft Inc., Grab Holdings Inc., Ola (ANI Technologies Pvt. Ltd.), and Others |

| Segments Covered | By Type, By Application, By End-Use, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

Market Segmentation

The Shared Mobility market is segmented by type, application, end-use, and region.

Based on Type Segment, Ride-hailing is the most dominant subsegment, holding 55% market share, followed by car sharing at around 20%. Ride-hailing leads due to its on-demand accessibility via apps, real-time tracking, and affordability for urban commuters, which drives market growth by reducing reliance on personal vehicles and alleviating traffic congestion in densely populated areas.

Based on Application Segment, Urban mobility is the most dominant subsegment with 60% share, followed by last-mile connectivity at 25%. Urban mobility dominates because it addresses daily commuting challenges in cities with high population density and limited infrastructure, thereby propelling overall market expansion through increased adoption of integrated, sustainable transport solutions.

Based on the End-Use Segment, Personal is the most dominant subsegment at 65%, followed by Business at 20%. Personal leads owing to individual preferences for flexible, cost-effective alternatives to ownership amid rising fuel and maintenance costs, which fuels market growth by broadening consumer access to eco-friendly options.

Recent Developments

- In April 2025, Bolt partnered with ETH Zurich to establish a sustainable urban transitions lab, focusing on innovative shared mobility solutions to enhance eco-friendly transport in cities.

- In April 2025, Flock Mobility raised 1 million euros to expand its AI-driven platform for shared electric vehicle transport, targeting organizational needs and boosting the shared mobility ecosystem.

- In April 2025, Voi Technology partnered with Wible in Spain to integrate e-scooters into the Wible multi-modal app, enabling unified access to carsharing and micromobility services.

Asia Pacific to Dominate the Global Market

- Asia Pacific is poised to dominate the global shared mobility market

China leads Asia Pacific as the dominant country, with massive investments in ride-hailing giants like Didi and widespread EV integration in shared fleets, supporting over 1 billion urban trips annually amid government pushes for green transport in megacities like Beijing and Shanghai.

India follows closely, propelled by platforms like Ola and Uber expanding into tier-2 cities, where affordable two-wheeler sharing addresses traffic woes in densely populated areas like Mumbai and Delhi, backed by national smart city initiatives.

Europe maintains strong growth through sustainability-focused policies, with Germany and France leading in car-sharing networks under EU emission targets, emphasizing integrated public-private models in cities like Berlin and Paris.

North America benefits from tech innovations, with the U.S. as the dominant country, where companies like Uber and Lyft dominate urban ride-hailing, supported by autonomous vehicle pilots in states like California and Arizona.

Latin America and the Middle East & Africa show emerging potential, led by Brazil and the UAE, where urbanization drives demand for app-based services in Sao Paulo and Dubai, focusing on affordable micromobility amid infrastructure developments.

Key Market Players and Strategies

- Uber Technologies Inc. focuses on global expansions, EV fleet integrations, and partnerships with public transit for seamless MaaS offerings to enhance urban accessibility.

- Didi Chuxing emphasizes AI-driven optimizations and autonomous tech investments in China, prioritizing safety and efficiency to maintain dominance in high-density markets.

- Lyft Inc. pursues sustainability through electric vehicle incentives and community programs, targeting U.S. urban users with affordable, eco-friendly ride options.

- Grab Holdings Inc. adopts multi-modal strategies in Southeast Asia, combining ride-hailing with deliveries and financial services for comprehensive user ecosystems.

- Ola (ANI Technologies Pvt. Ltd.) invests in electric two-wheelers and rural expansions in India, leveraging local regulations for cost-effective, scalable growth.

Market Trends

- Accelerated adoption of electric vehicles in shared fleets to meet sustainability goals and reduce emissions.

- Integration of AI for predictive maintenance, route optimization, and personalized user experiences.

- Expansion of Mobility-as-a-Service (MaaS) platforms combining multiple transport modes in unified apps.

- Growth in micromobility options like e-scooters and bikes for last-mile urban connectivity.

- Increased focus on rural and suburban markets to address underserved transport needs.

Market Segments and their Subsegments Covered in the Report

By Type

- Ride-Hailing

- Car Sharing

- Bike Sharing

- Scooter Sharing

- Public Transit

- Microtransit

- Car Rental

- Peer-to-Peer Car Sharing

- Ride Sourcing

- Others

- Others

By Application

- Short Distance

- Long Distance

- Last-Mile Connectivity

- Corporate Transportation

- Urban Mobility

- Airport Transfers

- Event Transportation

- Others

- Others

By End-Use

- Personal

- Business

- Government

- Corporates

- Tourists

- Educational Institutions

- Others

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

Shared mobility refers to transportation services where vehicles or rides are accessed on-demand and shared among users, including ride-hailing, car-sharing, and micromobility options.

Key factors include urbanization, sustainability initiatives, technological advancements, and government support for eco-friendly transport.

The market is projected to grow from approximately USD 451.20 billion in 2026 to USD 953.73 billion by 2035.

The CAGR is expected to be 8.68% during the forecast period.

Asia Pacific will contribute the most, driven by rapid urbanization in China and India.

Major players include Uber Technologies Inc., Didi Chuxing, Lyft Inc., Grab Holdings Inc., and Ola (ANI Technologies Pvt. Ltd.).

The report provides analysis of market size, trends, segments, regional insights, key players, and forecasts.

Stages include fleet acquisition, app development, user acquisition, operations, maintenance, and partnerships.

Trends shift toward electrification and MaaS, with consumers preferring convenient, sustainable options over ownership.

Emission regulations, urban policies, and incentives for EVs are key influencers.