Construction Chemicals Market Size, Share and Trends 2026 to 2035

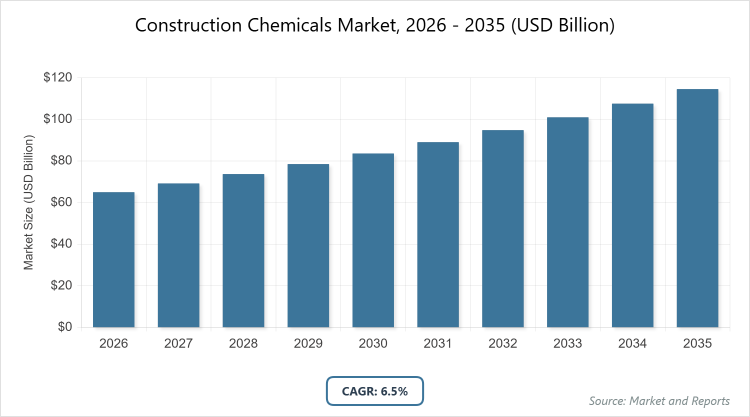

According to MarketnReports, the global Construction Chemicals market size was estimated at USD 65 billion in 2025 and is expected to reach USD 120 billion by 2035, growing at a CAGR of 6.5% from 2026 to 2035. Rapid urbanization and infrastructure development worldwide.

Key Insights

- The global construction chemicals market size was valued at USD 65 billion in 2025 and is projected to reach USD 120 billion by 2035.

- The market is anticipated to grow at a CAGR of 6.5% during the forecast period from 2026 to 2035.

- The market is driven by increasing urbanization, infrastructure investments, and demand for sustainable building solutions.

- Concrete admixtures dominate the type segment with a 46% share due to their essential role in enhancing concrete workability, strength, and reducing water usage in large-scale projects.

- Non-residential applications dominate with a 55% share because of extensive use in commercial and infrastructure projects requiring high-performance materials for durability under heavy loads.

- Asia Pacific dominates the regional segment with a 43% share owing to rapid construction growth in emerging economies like China and India.

What is the Construction Chemicals Market?

The construction chemicals market encompasses a wide range of specialty chemicals used to enhance the performance, durability, and sustainability of building materials and structures. These chemicals include additives that improve concrete strength, sealants that provide weather resistance, and coatings that protect surfaces from environmental damage. The market definition refers to products specifically formulated for use in construction activities, excluding general-purpose chemicals, and focuses on their role in modern building practices that prioritize efficiency, longevity, and eco-friendliness.

Market Dynamics

Growth Drivers

The primary growth drivers in the construction chemicals market stem from escalating global infrastructure projects and urbanization trends, particularly in developing regions. Governments worldwide are investing heavily in transportation networks, smart cities, and residential developments, which necessitate advanced chemicals for enhanced material performance and longevity. Additionally, the push for sustainable construction practices, including the use of low-carbon admixtures and eco-friendly sealants, is accelerating market expansion as regulations tighten around environmental impact.

Restraints

Market restraints are largely influenced by volatility in raw material prices, especially petroleum-based inputs like resins and solvents, which can increase production costs and squeeze profit margins for manufacturers. Supply chain disruptions, exacerbated by geopolitical tensions and global events, further challenge consistent availability, leading to project delays and higher expenses for end-users in the construction sector.

Opportunities

Opportunities abound in the shift toward green and bio-based construction chemicals, driven by regulatory incentives for low-VOC and recyclable products. Innovations in smart materials, such as self-healing concrete admixtures, present new avenues for market players to differentiate offerings and capture premium segments in retrofitting and energy-efficient building projects.

Challenges

Challenges include navigating fragmented regulatory landscapes across regions, where differing environmental standards and building codes complicate product formulation and compliance. Skilled labor shortages in application techniques also pose hurdles, as improper use of advanced chemicals can lead to suboptimal performance and increased rework costs in construction projects.

Construction Chemicals Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Construction Chemicals Market |

| Market Size 2025 | USD 65 Billion |

| Market Forecast 2035 | USD 120 Billion |

| Growth Rate | CAGR of 6.5% |

| Report Pages | 220 |

| Key Companies Covered |

Sika AG, BASF SE, MAPEI S.p.A., RPM International Inc., Saint-Gobain, and Others |

| Segments Covered | By Type, By Application, By End-Use, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

Market Segmentation

The Construction Chemicals market is segmented by type, application, end-use, and region.

Based on Type Segment, Concrete admixtures are the most dominant subsegment, holding 46% market share, followed by waterproofing chemicals at around 20%. Concrete admixtures lead due to their critical function in optimizing concrete mixes for strength, workability, and reduced curing time, which directly drives efficiency in large infrastructure projects by minimizing material waste and accelerating construction timelines.

Based on Application Segment, Non-residential is the most dominant subsegment with 55% share, followed by residential at 30%. Non-residential dominates because it encompasses commercial, industrial, and infrastructure builds that demand robust chemicals for high-load bearing and weather-resistant structures, thereby propelling overall market growth through sustained demand from government-funded megaprojects.

Based on the End-Use Segment, Infrastructure is the most dominant subsegment at 37%, followed by commercial at 25%. Infrastructure leads owing to massive investments in roads, bridges, and utilities requiring durable, corrosion-resistant chemicals, which in turn fuels market expansion by addressing long-term asset maintenance needs in aging global networks.

Recent Developments

- In April 2025, Sika AG acquired HPS North America to expand its building-finishing and waterproofing portfolio, enhancing its presence in the U.S. market through integrated solutions for sustainable construction.

- In February 2025, Saint-Gobain completed its USD 1.025 billion acquisition of Fosroc, adding 3,000 employees and 20 plants to bolster its global waterproofing and admixture offerings, particularly in North America.

- In April 2024, MAPEI S.p.A. launched Mapeflex MS 55, a hybrid adhesive and sealant with high elasticity, low VOC emissions, and compatibility with damp surfaces, targeting both professional and domestic applications for improved versatility.

Asia Pacific to Dominate the Global Market

- Asia Pacific is poised to dominate the global construction chemicals market

China leads the Asia Pacific market as the dominant country, fueled by its massive annual construction of billions of square meters of floor space in high-speed rail, smart cities, and mega-projects like the Greater Bay Area, which demand high-performance admixtures and waterproofing systems to ensure structural integrity in diverse climates.

India follows as a key contributor, with its National Infrastructure Pipeline valued at USD 1.4 trillion driving demand for durable chemicals in tropical environments, particularly corrosion-resistant admixtures for coastal cities like Mumbai and Chennai.

Europe maintains a strong position through its emphasis on sustainability and infrastructure renewal, with Germany and France leading in low-carbon admixtures and protective coatings under the EU’s Green Deal, focusing on retrofitting pre-1945 building stock for extended service life.

North America benefits from federal initiatives like the Infrastructure Investment and Jobs Act, allocating USD 1.2 trillion, with the U.S. as the dominant country emphasizing rehabilitation chemicals for structurally deficient bridges and energy-efficient solutions in residential builds.

Latin America and the Middle East & Africa show emerging growth, supported by urbanization in Brazil and Saudi Arabia, where investments in commercial and public infrastructure require weather-resistant sealants and coatings for harsh environmental conditions.

Key Market Players and Strategies

- Sika AG employs a strategy of strategic acquisitions and R&D investments in sustainable products, such as bio-based admixtures, to expand its global footprint and meet green building standards.

- BASF SE focuses on innovation in low-carbon concrete solutions and vertical integration to stabilize supply chains, enhancing its competitive edge in high-performance applications.

- MAPEI S.p.A. prioritizes product diversification with low-VOC sealants and adhesives, coupled with regional manufacturing expansions to cater to local market needs efficiently.

- RPM International Inc. leverages partnerships and technology advancements in protective coatings, aiming to capture premium segments in infrastructure rehabilitation.

- Saint-Gobain pursues mergers like the Fosroc acquisition to broaden its waterproofing portfolio, emphasizing sustainability to align with regulatory trends.

Market Trends

- Increasing adoption of bio-based and low-VOC formulations to comply with environmental regulations and support green building certifications.

- Rise in self-healing and smart materials, such as advanced admixtures that enhance concrete durability through nanotechnology.

- Growing focus on energy-efficient insulation and thermal coatings for sustainable urban development.

- Expansion of digital tools for mix-design optimization, improving chemical efficiency in construction projects.

- Shift toward recycled-content binders and circular economy practices in product development.

Market Segments and their Subsegments Covered in the Report

By Type

- Concrete Admixtures

- Waterproofing & Roofing

- Repair

- Flooring

- Sealants and Adhesives

- Protective Coatings

- Grouts and Anchors

- Cement Grinding Aids

- Asphalt Additives

- Others

By Application

- Residential

- Commercial

- Industrial

- Infrastructure

By End-Use

- Commercial

- Industrial and Institutional

- Infrastructure

- Residential

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

Construction chemicals are specialty products used to improve the quality, durability, and performance of building materials, including admixtures, sealants, coatings, and waterproofing agents.

Key factors include rapid urbanization, infrastructure investments, regulatory push for sustainable materials, and innovations in eco-friendly formulations.

The market is projected to grow from approximately USD 69 billion in 2026 to USD 120 billion by 2035.

The CAGR is expected to be 6.5% during the forecast period.

Asia Pacific will contribute the most, driven by construction booms in China and India.

Major players include Sika AG, BASF SE, MAPEI S.p.A., RPM International Inc., and Saint-Gobain.

The report provides in-depth analysis of market size, trends, segments, regional insights, key players, and forecasts.

Stages include raw material sourcing, manufacturing, distribution, application in construction projects, and end-of-life recycling or disposal.

Trends are shifting toward sustainable, bio-based products, with consumers preferring low-VOC and energy-efficient solutions for green buildings.

Stricter emissions standards, green building codes like LEED, and policies promoting low-carbon materials are key influencers.