Carbon Black Market Size, Share and Trends 2026 to 2035

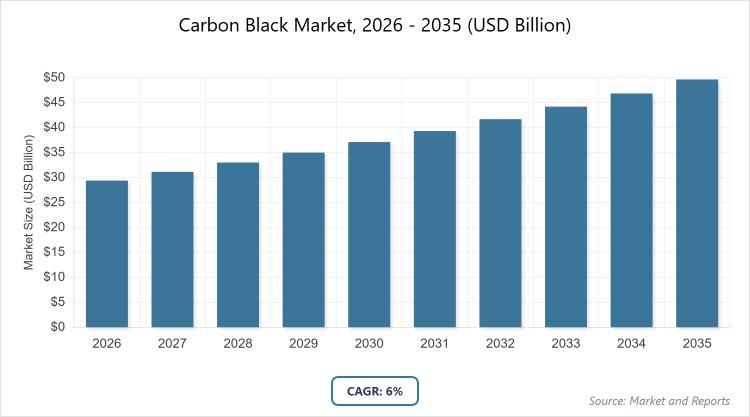

According to MarketnReports, the global Carbon Black market size was estimated at USD 29.4 billion in 2025 and is expected to reach USD 52.7 billion by 2035, growing at a CAGR of 6.0% from 2026 to 2035. The Carbon Black Market is driven by surging demand from the tire manufacturing and automotive industries amid global vehicle production growth.

What are the Key Insights into the Carbon Black Market?

- The global Carbon Black market was valued at USD 29.4 billion in 2025 and is projected to reach USD 52.7 billion by 2035.

- The market is expected to grow at a CAGR of 6.0% during the forecast period from 2026 to 2035.

- The market is driven by expanding tire production, rising automotive demand, and growth in specialty applications like EV batteries and conductive polymers.

- In the process segment, furnace black dominates with approximately 62% market share due to its cost-effective production and versatility in tire reinforcement.

- In the grade segment, standard grade dominates with around 72% share because of its widespread use in high-volume tire and rubber applications.

- In the application segment, tires hold the largest share at about 70% owing to carbon black’s essential role in enhancing durability and performance.

- Asia Pacific dominates the regional market with roughly 60% share, driven by massive tire manufacturing, rapid industrialization, and strong presence in China and India.

What is the Carbon Black Industry Overview?

The Carbon Black market involves the production, distribution, and application of a fine black powder made primarily from hydrocarbons, used as a reinforcing filler, pigment, and conductive agent in various industrial products. Carbon black is defined as an amorphous form of carbon with a high surface area-to-volume ratio, produced through incomplete combustion or thermal decomposition of hydrocarbons, offering properties like UV protection, electrical conductivity, and mechanical strength enhancement, making it essential in tires, plastics, coatings, inks, and batteries across automotive, construction, electronics, and consumer goods sectors.

What are the Carbon Black Market Dynamics?

Growth Drivers

The Carbon Black market is propelled by the booming automotive industry, where increasing vehicle production and tire demand in emerging economies necessitate high volumes of reinforcing fillers like carbon black to improve tread wear, traction, and fuel efficiency. Advancements in specialty carbon black for conductive applications in EV batteries, electronics, and energy storage drive innovation and premium pricing. Rising construction and plastics sectors utilize carbon black for UV stabilization and pigmentation, supported by urbanization. Sustainable production methods, such as bio-based feedstocks, align with environmental goals, attracting investments.

Restraints

Restraints include stringent environmental regulations on emissions from furnace processes, increasing compliance costs and pushing for cleaner alternatives. Volatility in raw material prices, particularly hydrocarbons like oil and natural gas, impacts profitability. Shift to green tires and silica substitutes reduces demand in some applications. Supply chain disruptions from geopolitical tensions affect global availability.

Opportunities

Opportunities emerge from the rise of recovered carbon black (rCB) from tire recycling, offering sustainable, cost-effective alternatives amid circular economy pushes. Growth in EV and lithium-ion batteries boosts specialty grade demand for conductivity. Expansion in Asia’s plastics and coatings sectors provides market entry. Investments in low-emission production technologies open premium segments.

Challenges

Challenges involve high energy consumption in production, contributing to the carbon footprint, and facing regulatory scrutiny. Competition from alternatives like silica in tires erodes the share. Skilled labor shortages in advanced manufacturing hinder innovation. Balancing quality with sustainability requires ongoing R&D.

Carbon Black Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Carbon Black Market |

| Market Size 2025 | USD 29.4 Billion |

| Market Forecast 2035 | USD 52.7 Billion |

| Growth Rate | CAGR of 6.0% |

| Report Pages | 220 |

| Key Companies Covered | Cabot Corporation, Birla Carbon, Orion Engineered Carbons, Mitsubishi Chemical, PCBL Limited, and Others |

| Segments Covered | By Process, By Grade, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Carbon Black Market Segmentation?

The Carbon Black market is segmented by process, grade, application, and region.

By process, furnace black emerges as the most dominant subsegment, holding over 62% share, due to its scalable, cost-effective production and superior reinforcing properties for tires and rubber, which drives the market by enabling high-volume output in automotive applications; the second most dominant is thermal black, which supports market growth through specialty uses in inks and coatings requiring high purity.

By grade, standard grade stands as the most dominant, accounting for about 72% share, as it meets bulk requirements for tire reinforcement at lower costs, propelling overall market expansion in high-demand sectors; specialty grade follows as the second dominant, aiding market drive by offering enhanced conductivity for batteries and electronics.

By application, tires dominate with around 70% share, driven by carbon black’s critical role in improving durability and performance, which accelerates market growth amid global vehicle demand; plastics are the second dominant, contributing to market advancement through UV protection and pigmentation needs.

What are the Recent Developments in the Carbon Black Market?

- In September 2025, Birla Carbon launched BC1060, a new grade for tire applications, at RubberTech 2025 in Shanghai.

- In June 2025, Epsilon Carbon introduced N134 grade hard carbon black at its Vijayanagar facility to reduce import dependency in India’s tire sector.

- In February 2025, Phillips Carbon Black announced a new plant in Naidupeta, Andhra Pradesh, with a capacity of up to 450,000 tons per year.

- In January 2025, Epsilon Carbon launched Terrablack, a sustainable recovered carbon black line, at the India International Tire Exhibition in New Delhi.

- In March 2024, Cabot Corporation unveiled PROPEL E8, an engineered reinforcing carbon black for tire treads.

What is the Regional Analysis of Carbon Black Market?

- Asia Pacific to dominate the global market.

Asia Pacific leads the Medical X-ray Film market, holding approximately 40% of the global share, driven by the region’s rapid expansion of healthcare infrastructure in densely populated nations like China, India, and Indonesia, where governments are investing heavily in building new hospitals, diagnostic centers, and primary care facilities to meet the needs of billions of people, high prevalence of chronic diseases such as tuberculosis, cancer, and orthopedic conditions that require frequent and affordable X-ray diagnostics, delayed transition to full digital radiography in vast rural and semi-urban areas due to the high costs of digital systems, limited electricity and internet access in remote locations, and a preference for cost-effective analog solutions that can be easily maintained with basic darkroom setups. China dominates within the region with the largest consumption, fueled by its massive hospital networks serving over 1.4 billion people, surging demand for orthopedic and chest X-rays from industrialization-related injuries, pollution-induced respiratory issues, and an aging population, local manufacturing of cost-effective green and blue sensitive films to reduce import dependency and keep prices low, and national health policies like Healthy China 2030 emphasizing widespread diagnostic upgrades to improve early detection and treatment outcomes.

North America follows with steady demand despite the widespread digital shift, commanding around 30% market share, supported by continued use of analog films in rural hospitals, small independent clinics, and specialized applications like veterinary or dental where cost, simplicity, and immediate availability outweigh the benefits of digital systems, along with strict regulatory compliance ensuring high standards of image quality and patient safety. The United States is the dominant country, driven by high procedure volumes in orthopedics, emergency care, oncology, and veterinary diagnostics, rigorous FDA standards mandating reliable film performance to minimize errors, and sustained demand in underserved rural communities with limited access to advanced digital infrastructure. Canada benefits through its public healthcare system, prioritizing cost-effective diagnostics in remote northern regions, with a focus on dental and veterinary films to support widespread access. The region’s stability is reinforced by ongoing R&D in eco-friendly films with reduced silver content, niche applications like portable radiography for field medicine, and a mature supply chain that ensures consistent availability.

Europe experiences moderate but consistent growth with 20% market share, with a strong emphasis on eco-friendly and low-silver-content films under EU environmental regulations aimed at reducing hazardous waste from silver halide processing and promoting sustainable medical practices. Germany leads, leveraging its advanced medtech industry and high adoption in dental clinics, orthopedic centers, and hospitals for precise imaging, supported by national health insurance systems that cover cost-effective analog diagnostics. The UK and France contribute via public health systems like the NHS emphasizing efficient, budget-controlled imaging in hospitals and diagnostic centers, with a focus on green-sensitive films for lower radiation in pediatric and general radiography. Europe’s mature market supports specialized growth through innovations in recyclable materials, compliance with REACH chemical regulations, and cross-border collaborations for standardized diagnostic protocols.

Latin America shows emerging potential with about 5% share, through gradual improvements in healthcare access driven by government programs to expand public hospitals and diagnostic services, increasing private investments in urban medical facilities, and rising awareness of early disease detection for conditions like respiratory infections and fractures. Brazil dominates, with public hospitals adopting affordable blue-sensitive films for general radiography in high-volume settings to serve its large population. Mexico benefits from cross-border trade with the US and growing dental applications in both public and private sectors. Regional expansions in rental models for imaging equipment and international aid for healthcare upgrades present opportunities for greater film demand.

The Middle East and Africa hold around 5% share, driven by infrastructure projects funded by oil revenues and international aid, improving diagnostic capabilities in urban centers and refugee camps, and rising trauma and infectious disease cases from conflicts and urbanization requiring basic X-ray films. Saudi Arabia leads with Vision 2030 healthcare upgrades, incorporating analog films in new hospitals for cost-effective imaging in orthopedics and chest diagnostics. South Africa contributes via private and public diagnostics for orthopedic and chest X-rays, supported by university hospitals and research initiatives. International aid from organizations like the WHO and NGOs, along with partnerships for local distribution, enhances penetration in conflict zones and rural areas.

What are the Key Market Players in Carbon Black?

- Cabot Corporation focuses on specialty grades, expanding through sustainable innovations like REPLASBLAK for recycled applications.

- Birla Carbon pursues capacity expansions and new grades like BC1060 for tires, targeting Asia-Pacific growth.

- Orion Engineered Carbons adopts green production, investing in low-emission technologies for EU compliance.

- Mitsubishi Chemical concentrates on high-purity specialty black for batteries and electronics.

- PCBL Limited emphasizes Indian market leadership, with new plants and recovered black lines like Terrablack.

What are the Carbon Black Market Trends?

- Rise in recovered carbon black for sustainability.

- Growth in specialty grades for EV batteries.

- Shift to bio-based feedstocks reducing emissions.

- Expansion in conductive polymers and inks.

- Capacity additions in Asia for tire demand.

- Focus on low-PAH grades for regulations.

- Integration of AI in dispersion control.

What are the Market Segments and Subsegments Covered in Medical X-ray Film Report?

By Process

-

- Furnace Black

- Thermal Black

- Acetylene Black

- Others

By Grade

-

- Standard Grade

- Specialty Grade

- Others

By Application

-

- Tires

- Plastics

- Paints & Coatings

- Rubber Products

- Inks & Toners

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Carbon black is a fine black powder produced from hydrocarbons, used as a filler, pigment, and conductive agent in tires, plastics, and coatings.

Factors include tire industry growth, EV battery demand, and sustainable production advancements.

The market is projected to grow from USD 29.4 billion in 2026 to USD 52.7 billion by 2035.

The CAGR is expected to be 6.0% from 2026 to 2035.

Asia Pacific will contribute notably, driven by manufacturing hubs.

Major players include Cabot Corporation, Birla Carbon, Orion Engineered Carbons, Mitsubishi Chemical, and PCBL Limited.

The report provides detailed size, trends, segmentation, regional insights, key players, and forecasts.

Stages include feedstock sourcing, production, processing, distribution, and end-use application.

Trends favor sustainable, specialty grades, with preferences for low-emission products.

Regulations on emissions and sustainability drive green innovations.