mHealth Apps Market Size, Share and Trends 2026 to 2035

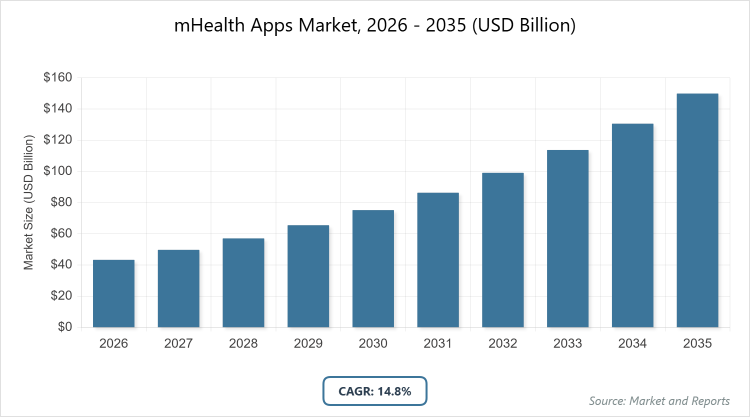

According to MarketnReports, the global mHealth Apps market size was estimated at USD 43.28 billion in 2025 and is expected to reach USD 172 billion by 2035, growing at a CAGR of 14.8% from 2026 to 2035. mHealth Apps Market is driven by increasing smartphone penetration and adoption of wearable devices.

What are the Key Insights into the mHealth Apps Market?

– The global mHealth Apps market was valued at USD 43.28 billion in 2025 and is projected to reach USD 172 billion by 2035.

- The market is expected to grow at a CAGR of 14.8% from 2026 to 2035.

- The mHealth Apps market is driven by rising smartphone usage, wearable technology adoption, and a shift toward patient-centric healthcare.

- In the type segment, the medical apps subsegment dominated with a 73.0% share due to heightened awareness among patients and healthcare professionals, coupled with frequent launches of specialized apps for disease management and monitoring.

- In the platform segment, the iOS subsegment dominated with a 39.7% share owing to its high adoption in developed markets and seamless integration with premium health devices.

- North America dominated the regional market with a 37.7% share, attributed to substantial healthcare expenditure, presence of leading tech companies, and advanced infrastructure supporting mobile health innovations.

What is the Industry Overview of the mHealth Apps Market?

The mHealth Apps market encompasses mobile applications designed to deliver health-related services through smartphones, tablets, and wearable devices, facilitating remote monitoring, diagnosis, treatment adherence, and wellness management. This market represents a convergence of healthcare and technology, where apps empower users to track personal health metrics, access medical information, and engage in virtual consultations, thereby transforming traditional healthcare delivery into more accessible, personalized, and efficient systems. Market definition refers to software applications specifically developed for mobile platforms that support health and medical functions, excluding general-purpose communication tools, and focusing on features like fitness tracking, chronic disease management, and telemedicine to improve overall health outcomes.

What are the Market Dynamics in the mHealth Apps Industry?

Growth Drivers

The growth of the mHealth Apps market is propelled by the surging penetration of smartphones globally, which enables widespread access to health monitoring tools and fosters user engagement in self-care. Additionally, the integration of advanced technologies such as AI and IoT in apps enhances functionality, allowing for real-time data analysis and personalized health recommendations. The rising prevalence of chronic diseases further accelerates demand, as apps provide convenient solutions for ongoing management and prevention, ultimately reducing healthcare costs and improving patient adherence to treatment plans. Government initiatives promoting digital health also play a crucial role, encouraging innovation and adoption across diverse populations.

Restraints

Data privacy and security concerns significantly hinder the expansion of the mHealth Apps market, as users and providers worry about potential breaches and unauthorized access to sensitive health information. Regulatory inconsistencies across regions create compliance challenges for developers, leading to delays in app launches and increased operational costs. Limited interoperability between apps and existing healthcare systems further restricts seamless integration, while the digital divide in underdeveloped areas limits market reach, excluding populations without reliable internet or device access. High development costs for secure, feature-rich apps also pose barriers for smaller players, constraining overall market innovation.

Opportunities

Opportunities in the mHealth Apps market abound with increased investments in digital health startups, fostering collaborations that drive technological advancements and expand app capabilities. The growing focus on mental health and women’s health opens niches for specialized apps, catering to underserved segments and tapping into emerging consumer demands. Expansion into emerging markets, particularly in Asia Pacific, presents vast potential due to rising smartphone adoption and healthcare digitization efforts. Integration with emerging technologies like AR/VR for immersive health experiences and partnerships with pharmaceutical companies for medication adherence tools further unlock new revenue streams and enhance market penetration.

Challenges

The mHealth Apps market faces challenges from fragmented regulations that vary by country, complicating global app distribution and requiring extensive adaptations for compliance. Cybersecurity threats, including malware and data leaks, erode user trust and necessitate continuous investment in robust protection measures. Market saturation with numerous similar apps leads to intense competition, making it difficult for new entrants to gain visibility without significant marketing efforts. Additionally, ensuring app accuracy and reliability for medical purposes demands rigorous validation, while addressing user skepticism toward digital health solutions requires ongoing education and evidence-based demonstrations of efficacy.

mHealth Apps Market: Report Scope

| Report Attributes | Report Details |

| Report Name | mHealth Apps Market |

| Market Size 2025 | USD 43.28 Billion |

| Market Forecast 2035 | USD 172 Billion |

| Growth Rate | CAGR of 14.8% |

| Report Pages | 236 |

| Key Companies Covered | Apple Inc., Google Inc., AirStrip Technologies, Inc., Samsung Electronics Co. Ltd., Veradigm LLC, Qualcomm Technologies, Inc., AT&T, Orange, Teladoc Health, Inc., AstraZeneca, Abbott, Sanofi, Johnson & Johnson Services, Inc., Novartis AG, Pfizer Inc., and Others. |

| Segments Covered | By Type, By Platform, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of the mHealth Apps?

The mHealth Apps market is segmented by type, platform, and region.

Based on Type Segment. The most dominant segment is medical apps, holding 73.0% of the market share, primarily because it addresses critical needs in disease management, remote monitoring, and patient education through features like symptom tracking and virtual consultations, which drive market growth by improving healthcare accessibility and reducing hospital visits; the second most dominant is fitness apps, which contribute significantly by promoting preventive health and lifestyle management, leveraging wearable integrations to engage users in daily activity tracking and motivation, thereby boosting overall market expansion through increased consumer adoption and data-driven health insights.

Based on Platform Segment. The most dominant segment is iOS, with a 39.7% share, due to its ecosystem’s emphasis on user privacy, high-quality app standards, and compatibility with advanced health gadgets like Apple Watch, which propels market growth by attracting premium users and enabling sophisticated features such as ECG monitoring; the second most dominant is Android, favored for its affordability and vast user base in emerging markets, driving the market through widespread accessibility and customization options that facilitate broader adoption of health apps among diverse socioeconomic groups.

What are the Recent Developments in the mHealth Apps Market?

- In August 2023, actor Suniel Shetty collaborated with Veda Rehabilitation & Wellness to launch the Let’s Get Happi app, which offers mental health support through assessment tests, meditation sessions, and therapy services, aiming to make psychological care more accessible via mobile platforms.

- In June 2024, NeuroFlow acquired Owl to strengthen its behavioral health platform, integrating advanced analytics and measurement tools to enhance patient outcomes in mental health management through data-driven insights.

- In June 2024, Ryde Group Ltd partnered with Mobile-health Network Solutions to expand telehealth services in the Asia-Pacific region, providing users with easier access to remote consultations and health monitoring features.

- In January 2024, JD Health introduced an elderly care channel in China, focusing on apps tailored for senior users to manage chronic conditions, medication reminders, and virtual family connections.

- In February 2024, the “Health On Us” app was launched in India, offering home-based and center-based healthcare services to improve convenience for patients with mobility issues.

- In August 2023, MedWorks debuted a new health app in Florida, U.S., designed to streamline patient-provider interactions and support remote monitoring for chronic diseases.

What is the Regional Analysis of the mHealth Apps Market?

- North America to dominate the global market

North America The North American region leads the mHealth Apps market, driven by high smartphone penetration, substantial investments in digital health, and a robust ecosystem of tech innovators; the United States dominates within this region due to its advanced healthcare infrastructure, government support through initiatives like telehealth expansions, and the presence of major companies developing cutting-edge apps, which collectively enhance adoption rates and contribute to improved patient outcomes amid rising chronic disease prevalence.

Europe exhibits strong growth in the mHealth Apps market, fueled by stringent data protection regulations like GDPR that build user trust and encourage app development; Germany stands out as the dominating country, owing to its emphasis on digital health strategies, aging population requiring remote care solutions, and collaborations between tech firms and healthcare providers, which drive innovation in areas such as mental health and chronic management apps.

Asia Pacific region is poised for the fastest expansion in the mHealth Apps market, supported by rapid urbanization, increasing internet access, and government pushes for digital healthcare; China dominates this region with its massive user base, investments in AI-integrated apps, and initiatives like elderly care platforms, enabling widespread adoption and addressing the needs of a large population with rising chronic illnesses.

Latin America shows promising growth in the mHealth Apps market, aided by improving mobile infrastructure and efforts to bridge healthcare gaps in remote areas; Brazil is the dominating country, leveraging its large population and telemedicine policies to promote apps for disease prevention and management, which help reduce healthcare disparities and support economic development through tech-driven solutions.

Middle East and Africa region is emerging in the mHealth Apps market, propelled by government digital health agendas and increasing smartphone usage; Saudi Arabia dominates, with high mobile penetration rates and investments in AI and wearables, facilitating apps for remote consultations and chronic care that align with Vision 2030 goals to modernize healthcare delivery.

Who are the Key Market Players in the mHealth Apps and Their Strategies?

Apple Inc. focuses on ecosystem integration, leveraging its iOS platform and devices like the Apple Watch to offer health features such as ECG monitoring and fitness tracking, with strategies centered on partnerships with healthcare providers and continuous software updates to enhance user privacy and app functionality, driving market leadership through innovation and user loyalty.

Google Inc. emphasizes Android’s open-source nature to expand reach in emerging markets, developing tools like Google Fit for health data aggregation and collaborating with wearable manufacturers, while its strategies include AI advancements for personalized health insights and acquisitions to bolster cloud-based health solutions, fostering broad adoption and competitive edge.

Samsung Electronics Co. Ltd. integrates mHealth apps with its Galaxy ecosystem, including smartwatches for biometric tracking, and pursues strategies like global partnerships for telehealth and R&D in biosensor technology to address chronic diseases, positioning itself as a key player in wearable-driven health management.

Teladoc Health, Inc. Teladoc Health, Inc. specializes in telemedicine apps, expanding through acquisitions and international collaborations to offer virtual care services, with strategies focused on data analytics for personalized treatment and compliance with global regulations to scale operations and improve accessibility in underserved areas.

Johnson & Johnson Services Inc. develops apps for medication adherence and disease education, employing strategies such as pharmaceutical partnerships and clinical trials integration to validate app efficacy, enhancing market presence by combining medical expertise with digital tools for patient empowerment.

Pfizer Inc. invests in apps for vaccine tracking and health education, with strategies involving collaborations with tech firms for AI-enhanced features and global launches to support public health campaigns, strengthening its role in preventive care through data-driven insights.

What are the Market Trends in the mHealth Apps?

- Integration of AI and machine learning for personalized health recommendations and predictive analytics.

- Rising adoption of wearable devices for real-time health monitoring and data synchronization with apps.

- Emphasis on mental health apps with features like meditation and therapy sessions amid growing awareness.

- Expansion of telehealth functionalities for remote consultations and virtual doctor visits.

- Focus on data security enhancements to comply with regulations and build user trust.

- Growth in women’s health-specific apps for tracking menstrual cycles, pregnancy, and menopause.

- Increasing use of AR/VR for immersive health education and rehabilitation programs.

- Partnerships between tech giants and pharmaceutical companies for medication management tools.

- Shift toward patient-centric models empowering users with access to personal health records.

- Emergence of apps tailored for elderly care, including fall detection and medication reminders.

What are the Market Segments and Their Subsegments Covered in the mHealth Apps Report?

By Type

-

Medical Apps

-

Women’s Health

- Fitness & Nutrition

- Menstrual Health

- Pregnancy Tracking & Postpartum Care

- Disease Management

- Menopause

- Others

-

Chronic Disease Management Apps

- Obesity Management

- Mental Health

- Diabetes Management

- Blood Pressure and ECG Monitoring

- Cancer Management

- Other Chronic Disease Management

-

Personal Health Record Apps

-

Medication Management Apps

-

Diagnostic Apps

-

Remote Monitoring Apps

-

Others (Pill Reminder, Medical Reference, Professional Networking, Healthcare Education)

-

-

Fitness Apps

By Platform

-

- Android

- iOS

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

1.1 Report Description and Scope1.2 Research Scope1.3 Research Methodology1.3.1 Market Research Type1.3.2 Market Research MethodologyChapter 2. Executive Summary

2.1 Global mHealth Apps Market, (2026 - 2035) (USD Billion)2.2 Global mHealth Apps Market: SnapshotChapter 3. Global mHealth Apps Market - Industry Analysis

3.1 mHealth Apps Market: Market Dynamics3.2 Market Drivers3.2.1 The mHealth apps market is driven by widespread smartphone adoption, AI and IoT integration, rising chronic disease prevalence, demand for cost-effective self-care solutions, and supportive government digital health initiatives.3.3 Market Restraints3.3.1 The mHealth apps market is constrained by data privacy and security concerns, regulatory inconsistencies, limited interoperability with healthcare systems, digital divide issues, and high development costs.3.4 Market Opportunities3.4.1 The mHealth apps market offers opportunities through digital health investments, growth in mental and women’s health apps, expansion in emerging markets, and integration with advanced technologies and pharmaceutical partnerships.3.5 Market Challenges3.5.1 The mHealth apps market faces challenges from fragmented regulations, cybersecurity risks, intense market competition, stringent validation requirements, and the need to build user trust through proven accuracy and effectiveness.3.6 Porter’s Five Forces Analysis3.7 Market Attractiveness Analysis3.7.1 Market Attractiveness Analysis By Type3.7.2 Market Attractiveness Analysis By PlatformChapter 4. Global mHealth Apps Market- Competitive Landscape

4.1 Company Market Share Analysis4.1.1 Global mHealth Apps Market: Company Market Share, 20254.2 Strategic Development4.2.1 Acquisitions & mergers4.2.2 New Product launches4.2.3 Agreements, partnerships, collaborations, and joint ventures4.2.4 Research and development and regional expansion4.3 Price Trend AnalysisChapter 5. Global mHealth Apps Market - Type Analysis

5.1 Global mHealth Apps Market Overview: Type5.1.1 Global mHealth Apps Market share, By Type, 2025 and 20355.2 Medical Apps5.2.1 Global mHealth Apps Market by Medical Apps, 2026 - 2035 (USD Billion)5.3 Fitness Apps5.3.1 Global mHealth Apps Market by Fitness Apps, 2026 - 2035 (USD Billion)Chapter 6. Global mHealth Apps Market - Platform Analysis

6.1 Global mHealth Apps Market Overview: Platform6.1.1 Global mHealth Apps Market Share, By Platform, 2025 and 20356.2 Android6.2.1 Global mHealth Apps Market by Android, 2026 - 2035 (USD Billion)6.3 iOS6.3.1 Global mHealth Apps Market by iOS, 2026 - 2035 (USD Billion)6.4 Others6.4.1 Global mHealth Apps Market by Others, 2026 - 2035 (USD Billion)Chapter 7. mHealth Apps Market - Regional Analysis

7.1 Global mHealth Apps Market Regional Overview7.2 Global mHealth Apps Market Share, by Region, 2025 & 2035 (USD Billion)7.3 North America7.3.1 North America mHealth Apps Market, 2026 - 2035 (USD Billion)7.3.1.1 North America mHealth Apps Market, by Country, 2026 - 2035 (USD Billion)7.3.2 North America mHealth Apps Market, by Type, 2026 - 20357.3.2.1 North America mHealth Apps Market, by Type, 2026 - 2035 (USD Billion)7.3.3 North America mHealth Apps Market, by Platform, 2026 - 20357.3.3.1 North America mHealth Apps Market, by Platform, 2026 - 2035 (USD Billion)7.4 Europe7.4.1 Europe mHealth Apps Market, 2026 - 2035 (USD Billion)7.4.1.1 Europe mHealth Apps Market, by Country, 2026 - 2035 (USD Billion)7.4.2 Europe mHealth Apps Market, by Type, 2026 - 20357.4.2.1 Europe mHealth Apps Market, by Type, 2026 - 2035 (USD Billion)7.4.3 Europe mHealth Apps Market, by Platform, 2026 - 20357.4.3.1 Europe mHealth Apps Market, by Platform, 2026 - 2035 (USD Billion)7.5 Asia Pacific7.5.1 Asia Pacific mHealth Apps Market, 2026 - 2035 (USD Billion)7.5.1.1 Asia Pacific mHealth Apps Market, by Country, 2026 - 2035 (USD Billion)7.5.2 Asia Pacific mHealth Apps Market, by Type, 2026 - 20357.5.2.1 Asia Pacific mHealth Apps Market, by Type, 2026 - 2035 (USD Billion)7.5.3 Asia Pacific mHealth Apps Market, by Platform, 2026 - 20357.5.3.1 Asia Pacific mHealth Apps Market, by Platform, 2026 - 2035 (USD Billion)7.6 Latin America7.6.1 Latin America mHealth Apps Market, 2026 - 2035 (USD Billion)7.6.1.1 Latin America mHealth Apps Market, by Country, 2026 - 2035 (USD Billion)7.6.2 Latin America mHealth Apps Market, by Type, 2026 - 20357.6.2.1 Latin America mHealth Apps Market, by Type, 2026 - 2035 (USD Billion)7.6.3 Latin America mHealth Apps Market, by Platform, 2026 - 20357.6.3.1 Latin America mHealth Apps Market, by Platform, 2026 - 2035 (USD Billion)7.7 The Middle-East and Africa7.7.1 The Middle-East and Africa mHealth Apps Market, 2026 - 2035 (USD Billion)7.7.1.1 The Middle-East and Africa mHealth Apps Market, by Country, 2026 - 2035 (USD Billion)7.7.2 The Middle-East and Africa mHealth Apps Market, by Type, 2026 - 20357.7.2.1 The Middle-East and Africa mHealth Apps Market, by Type, 2026 - 2035 (USD Billion)7.7.3 The Middle-East and Africa mHealth Apps Market, by Platform, 2026 - 20357.7.3.1 The Middle-East and Africa mHealth Apps Market, by Platform, 2026 - 2035 (USD Billion)Chapter 8. Company Profiles

8.1 Apple Inc.8.1.1 Overview8.1.2 Financials8.1.3 Product Portfolio8.1.4 Business Strategy8.1.5 Recent Developments8.2 Google Inc.8.2.1 Overview8.2.2 Financials8.2.3 Product Portfolio8.2.4 Business Strategy8.2.5 Recent Developments8.3 AirStrip Technologies Inc.8.3.1 Overview8.3.2 Financials8.3.3 Product Portfolio8.3.4 Business Strategy8.3.5 Recent Developments8.4 Samsung Electronics Co. Ltd.8.4.1 Overview8.4.2 Financials8.4.3 Product Portfolio8.4.4 Business Strategy8.4.5 Recent Developments8.5 Veradigm LLC8.5.1 Overview8.5.2 Financials8.5.3 Product Portfolio8.5.4 Business Strategy8.5.5 Recent Developments8.6 Qualcomm Technologies Inc.8.6.1 Overview8.6.2 Financials8.6.3 Product Portfolio8.6.4 Business Strategy8.6.5 Recent Developments8.7 AT&T8.7.1 Overview8.7.2 Financials8.7.3 Product Portfolio8.7.4 Business Strategy8.7.5 Recent Developments8.8 Orange8.8.1 Overview8.8.2 Financials8.8.3 Product Portfolio8.8.4 Business Strategy8.8.5 Recent Developments8.9 Teladoc Health Inc.8.9.1 Overview8.9.2 Financials8.9.3 Product Portfolio8.9.4 Business Strategy8.9.5 Recent Developments8.10 AstraZeneca8.10.1 Overview8.10.2 Financials8.10.3 Product Portfolio8.10.4 Business Strategy8.10.5 Recent Developments8.11 Abbott8.11.1 Overview8.11.2 Financials8.11.3 Product Portfolio8.11.4 Business Strategy8.11.5 Recent Developments8.12 Sanofi8.12.1 Overview8.12.2 Financials8.12.3 Product Portfolio8.12.4 Business Strategy8.12.5 Recent Developments8.13 Johnson & Johnson Services Inc.8.13.1 Overview8.13.2 Financials8.13.3 Product Portfolio8.13.4 Business Strategy8.13.5 Recent Developments8.14 Novartis AG8.14.1 Overview8.14.2 Financials8.14.3 Product Portfolio8.14.4 Business Strategy8.14.5 Recent Developments8.15 Pfizer Inc.8.15.1 Overview8.15.2 Financials8.15.3 Product Portfolio8.15.4 Business Strategy8.15.5 Recent Developments

Frequently Asked Questions

mHealth Apps are mobile software applications that deliver health services, including monitoring vital signs, managing medications, providing fitness guidance, and facilitating remote consultations via smartphones and wearables.

Key factors include rising smartphone penetration, advancements in wearable technology, increasing chronic disease prevalence, government support for digital health, and a shift toward personalized patient care.

The mHealth Apps market is projected to grow from over USD 43.28 billion in 2025 to USD 172 billion by 2035.

The CAGR value is expected to be 14.8% during 2026-2035.

North America will contribute notably, holding the largest share due to advanced infrastructure and high adoption rates.

Major players include Apple Inc., Google Inc., Samsung Electronics Co. Ltd., Teladoc Health, Inc., Johnson & Johnson Services, Inc., and Pfizer Inc.

The report provides comprehensive analysis, including market size, forecasts, segmentation, drivers, restraints, regional insights, key players, trends, and competitive strategies.

Stages include research and development of app features, software coding and testing, platform integration and deployment, marketing and distribution through app stores, user data collection and analysis, and ongoing updates for compliance and enhancements.

Trends are evolving toward AI-driven personalization, mental health focus, and wearable integration, while consumers prefer user-friendly, privacy-secure apps that offer real-time insights and seamless health data sharing.

Regulatory factors like FDA approvals, HIPAA, and GDPR for data privacy impact development timelines, while environmental factors such as the digital divide and sustainability concerns in device manufacturing influence accessibility and adoption.