Bottled Water Market Size, Share and Trends 2026 to 2035

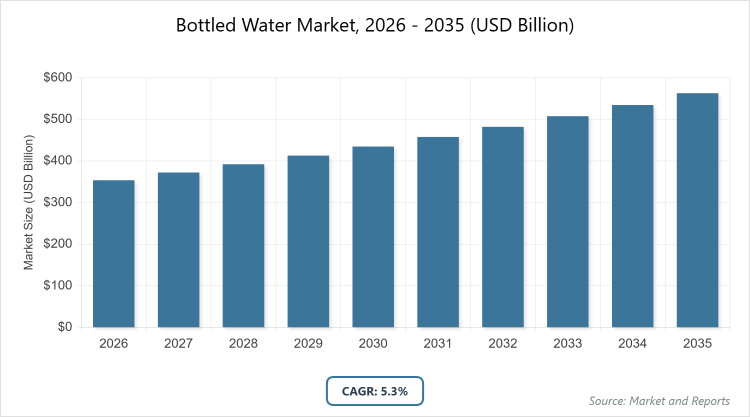

According to MarketnReports, the global Bottled Water Market size was estimated at USD 353.61 billion in 2025 and is expected to reach USD 592.51 billion by 2035, growing at a CAGR of 5.3% from 2026 to 2035. Bottled Water Market is driven by increasing health consciousness and concerns over tap water quality.What are the Key Insights of the Bottled Water Market?

- The global Bottled Water Market was valued at USD 353.61 billion in 2025 and is projected to reach USD 592.51 billion by 2035.

- The market is expected to grow at a CAGR of 5.3% during the forecast period from 2026 to 2035.

- The market is driven by rising health awareness, urbanization, and demand for convenient hydration options.

- In the Product Type segment, Still Water dominates with a 58% share due to its widespread preference for everyday hydration, affordability, and neutral taste that appeals to a broad consumer base, minimizing health risks from carbonation or additives.

- In the Packaging Type segment, PET Bottles dominates with a 77% share because of their lightweight, cost-effective, and recyclable nature, enabling efficient distribution and consumer convenience while aligning with mass-market demands.

- In the Distribution Channel segment, Supermarkets/Hypermarkets dominates with a 46% share as they offer variety, competitive pricing, and high visibility, facilitating bulk purchases and brand comparisons.

- Asia Pacific dominates the regional landscape with a 45% share, fueled by rapid urbanization, population growth, and inconsistent tap water quality in emerging economies like China and India.

What is the Industry Overview of the Bottled Water Market?

The Bottled Water Market involves the production, packaging, and distribution of purified, mineral, or flavored water in sealed containers for consumer consumption, addressing needs for safe, convenient hydration amid concerns over public water quality and lifestyle demands. It encompasses various types such as still, sparkling, and functional waters, sourced from springs, wells, or municipal supplies and treated to meet safety standards. Market definition refers to the commercial ecosystem supplying portable drinking water in bottles, driven by urbanization, health trends, and accessibility through retail channels, while facing scrutiny over environmental impact from plastic packaging.

What are the Market Dynamics of the Bottled Water Market?

Growth Drivers

The Bottled Water Market is propelled by escalating health consciousness globally, where consumers increasingly opt for safe, contaminant-free alternatives to tap water amid rising incidences of waterborne diseases and pollution concerns. Urbanization and busy lifestyles further amplify demand for convenient, on-the-go hydration solutions, while innovations in flavored and functional waters attract health-focused demographics seeking added benefits like vitamins or electrolytes. Government regulations ensuring water quality and the expansion of retail infrastructure in developing regions also contribute significantly, enabling broader accessibility and fostering market penetration as disposable incomes rise.

Restraints

Restraints in the Bottled Water Market include growing environmental backlash against single-use plastics, leading to regulatory bans and consumer shifts toward sustainable alternatives, which increase production costs for eco-friendly packaging. High competition from free tap water in developed regions with reliable public systems diminishes perceived value, while supply chain vulnerabilities, such as water sourcing limitations and transportation expenses, strain margins. Additionally, economic downturns can reduce discretionary spending on premium products, limiting growth in price-sensitive markets.

Opportunities

Opportunities abound in the Bottled Water Market with the surge in demand for premium, functional variants infused with natural flavors, minerals, or health-boosting additives, targeting wellness-oriented consumers in affluent and emerging markets. Sustainable packaging innovations, like biodegradable materials or refillable systems, offer differentiation amid environmental regulations, while e-commerce and subscription models expand reach in underserved areas. Expanding into untapped rural regions through affordable formats and partnerships with local distributors presents avenues for volume growth, supported by rising global awareness of hydration's role in preventive health.

Challenges

Challenges in the Bottled Water Market encompass stringent regulations on water sourcing and labeling, which vary by region and increase compliance costs, potentially hindering small players' entry. Plastic waste management remains a persistent issue, with public campaigns and bans pressuring brands to invest in alternatives without passing on higher prices to consumers. Counterfeit products erode trust in quality, while fluctuating raw material costs for packaging and transportation amid global supply disruptions pose operational risks, complicating consistent profitability.

Bottled Water Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Bottled Water Market |

| Market Size 2025 | USD 353.61 Billion |

| Market Forecast 2035 | USD 592.51 Billion |

| Growth Rate | CAGR of 5.3% |

| Report Pages | 220 |

| Key Companies Covered |

Nestlé, Danone, The Coca-Cola Company, PepsiCo, Nongfu Spring, FIJI Water, Primo Water Corporation, and Others. |

| Segments Covered | By Product Type, By Packaging Type, By Distribution Channel, and By Region. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 - 2024 |

| Forecast Year | 2026 - 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of the Bottled Water Market?

The Bottled Water Market is segmented by product type, packaging type, distribution channel, and region.By Product Type Segment, Still Water emerges as the most dominant subsegment, followed by Sparkling Water as the second most dominant. Still Water leads due to its universal appeal for daily hydration without carbonation, driving market growth by catering to health-conscious consumers seeking pure, calorie-free options; this dominance arises from its affordability, widespread availability, and alignment with global trends toward simple, natural beverages, reducing reliance on sugary drinks and supporting overall wellness initiatives.

By Packaging Type Segment, PET Bottles is the most dominant subsegment, with Glass Bottles as the second most dominant. PET Bottles dominate owing to their durability, low cost, and lightweight design, propelling the market by enabling efficient global distribution and consumer portability; this is driven by manufacturing scalability and recycling advancements, which address environmental concerns while maintaining accessibility for mass consumption.

By Distribution Channel Segment, Supermarkets/Hypermarkets is the most dominant subsegment, followed by Convenience Stores as the second most dominant. Supermarkets/Hypermarkets lead as they provide extensive product variety and promotional opportunities, fueling market expansion through high-volume sales and brand visibility; their dominance stems from strategic locations in urban areas, bulk purchasing incentives, and integration with everyday shopping habits, enhancing impulse buys and loyalty programs.

What are the Recent Developments in the Bottled Water Market?

- In March 2025, PepsiCo announced the nationwide rollout of SodaStream Professional Hydration Stations in corporate offices and gyms, promoting customizable flavored water with refillable bottles to enhance sustainability and consumer engagement.

- In February 2025, Liquid Death launched its first flavored still water line, including variants like mango chainsaw and berry it alive, targeting premium markets with innovative packaging and marketing to appeal to younger demographics.

- In January 2025, Nestlé Waters North America expanded its rPET packaging initiative across all spring water brands, committing to 100% recycled bottles by 2027, addressing environmental concerns and strengthening brand loyalty.

What is the Regional Analysis of the Bottled Water Market?

Asia Pacific to dominate the global market.Asia Pacific commands the leading position in the Bottled Water Market, driven by rapid urbanization, population density, and inconsistent public water infrastructure, leading to high reliance on packaged alternatives. China dominates within the region, with massive consumption fueled by industrial growth, health awareness campaigns, and government initiatives to improve water safety standards, resulting in widespread adoption of affordable purified and mineral waters through extensive retail networks.

North America exhibits steady growth, supported by health trends and premium product preferences, with a focus on functional and sustainable options. The United States leads here, where consumer shifts from sugary beverages to hydration-focused choices, coupled with innovations in flavored and alkaline waters, drive demand amid robust e-commerce and convenience store channels.

Europe maintains a mature market with emphasis on environmental regulations and premium sourcing, promoting recycled packaging and natural mineral waters. Germany dominates, leveraging its strong tradition of spa waters and eco-conscious consumers, who favor glass-bottled products and support EU-wide sustainability mandates for reduced plastic use.

Latin America shows promising expansion through increasing disposable incomes and tourism, with a rise in flavored variants. Brazil leads the region, where hot climates and urban expansion boost on-the-go consumption, aided by local brands offering affordable options and investments in distribution to combat water quality issues.

The Middle East and Africa region is emerging, propelled by arid climates and infrastructure challenges, with growth in imported premium brands. South Africa dominates, driven by health initiatives and retail modernization, where consumers increasingly choose bottled water for safety, supported by foreign investments in local bottling facilities.

What are the Key Market Players and Strategies in the Bottled Water Market?

Nestlé emphasizes sustainability through recycled packaging and water stewardship programs, focusing on premium brands like Perrier and San Pellegrino to capture health-conscious consumers via global distribution networks and digital marketing.

Danone pursues innovation in functional waters with added minerals and flavors, leveraging acquisitions and partnerships to expand in emerging markets while committing to carbon-neutral operations for eco-friendly appeal.

The Coca-Cola Company integrates bottled water into its beverage portfolio with brands like Dasani, investing in purification technologies and e-commerce to enhance accessibility and promote hydration campaigns.

PepsiCo drives growth via Aquafina and LIFEWTR, adopting lightweight bottles and subscription models to reduce environmental impact and target younger demographics through influencer collaborations.

Nongfu Spring focuses on natural sourcing and affordable pricing in Asia, utilizing extensive local supply chains and branding as pure mountain water to dominate regional volumes.

FIJI Water highlights artisanal sourcing and premium positioning, employing celebrity endorsements and luxury partnerships to build brand prestige in high-end retail and hospitality sectors.

Primo Water Corporation specializes in bulk and dispenser solutions, emphasizing home delivery services and eco-refills to cater to residential and office needs with cost-effective strategies.

What are the Market Trends in the Bottled Water Market?

- Rising demand for functional waters infused with vitamins, electrolytes, or CBD for health benefits.

- Shift toward sustainable packaging like biodegradable plastics and aluminum cans to reduce environmental impact.

- Growth in premium and artisanal brands emphasizing natural sourcing and unique mineral profiles.

- Expansion of flavored variants with natural fruits and herbs to attract younger consumers.

- Increased adoption of alkaline and pH-balanced waters for wellness and detoxification claims.

- Surge in online sales and subscription services for convenient home delivery.

- Focus on zero-calorie, sugar-free options amid anti-obesity trends.

- Integration of smart packaging with QR codes for traceability and consumer engagement.

- Emphasis on local sourcing to minimize carbon footprints and support community initiatives.

- Partnerships with fitness brands for co-branded hydration products.

What Market Segments and their Subsegments are Covered in the Bottled Water Market Report?

Product Type- Still Water

- Sparkling Water

- Mineral Water

- Purified Water

- Functional Water

- Flavored Water

- Spring Water

- Alkaline Water

- Distilled Water

- Artesian Water

- Others

- PET Bottles

- Glass Bottles

- Metal Cans

- Cartons

- Pouches

- Tetra Packs

- Biodegradable Plastics

- Aluminum Bottles

- Bulk Containers

- Dispensers

- Others

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail

- Grocery Stores

- Specialty Stores

- Vending Machines

- Wholesale/Bulk Sales

- Direct Sales

- HoReCa

- Institutional Sales

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

The Bottled Water Market encompasses the global industry involved in sourcing, purifying, packaging, and distributing sealed water products for safe consumption, including various types like still, sparkling, and functional variants.

Key factors include rising health awareness, urbanization, concerns over tap water safety, innovations in functional waters, and sustainable packaging trends.

The market is projected to grow from approximately USD 353.61 billion in 2026 to USD 592.51 billion by 2035.

The CAGR is expected to be 5.3% during the forecast period.

Asia Pacific will contribute notably, holding around 45% of the market share due to population growth and urbanization.

Major players include Nestlé, Danone, The Coca-Cola Company, PepsiCo, Nongfu Spring, and FIJI Water.

The report offers in-depth analysis of market size, trends, segmentation, regional insights, key players, drivers, restraints, and forecasts.

The value chain includes water sourcing, purification and treatment, bottling and packaging, distribution and logistics, retail sales, and end-consumer usage with recycling.

Trends are moving toward sustainable, functional, and premium products, with consumers preferring eco-friendly packaging, health-enhanced options, and convenient formats.

Regulatory factors include strict quality standards and plastic bans, while environmental factors involve sustainability demands and water resource management.