Bio-Based Materials Market Size, Share and Trends 2026 to 2035

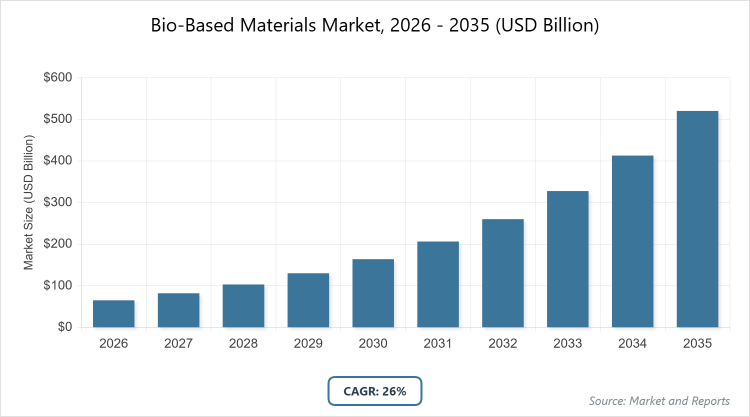

According to MarketnReports, the global Bio-Based Materials market size was estimated at USD 65 billion in 2025 and is expected to reach USD 650 billion by 2035, growing at a CAGR of 26% from 2026 to 2035. Bio-Based Materials Market is driven by favorable government policies and increasing consumer preference for eco-friendly products.

What are the Key Insights from the Bio-Based Materials Market Report?

- The global Bio-Based Materials market was valued at USD 65 billion in 2025 and is projected to reach USD 650 billion by 2035.

- The market is expected to grow at a CAGR of 26% during the forecast period from 2026 to 2035.

- The market is driven by supportive government regulations, subsidies for sustainable practices, and rising consumer demand for environmentally friendly products.

- In the product type segment, Bio-Based Polyethylene Terephthalate (PET) dominates with a 35% market share.

- Bio-Based PET dominates due to its excellent barrier properties, durability, and widespread adoption in packaging applications, which helps reduce reliance on fossil-based plastics and aligns with circular economy goals.

- In the application segment, Rigid Packaging dominates with a 30% market share.

- Rigid Packaging is dominant because of its high demand in food and beverage industries for sustainable alternatives to traditional plastics, driving market growth by enhancing product shelf life and reducing environmental impact.

- In the end-use segment, Food and Beverage dominates with a 40% market share.

- Food and Beverage is dominant owing to the sector’s focus on eco-friendly packaging solutions that comply with regulations and meet consumer preferences for sustainable materials, thereby boosting overall market expansion.

- Europe dominates the regional market with a 40% share.

- Europe dominates due to stringent environmental policies, such as the European Commission’s strategies for reducing greenhouse gas emissions, and strong investments in bio-based innovations.

What is the Industry Overview of the Bio-Based Materials Market?

Bio-based materials refer to substances derived partially or entirely from renewable biological sources, such as plants, agricultural residues, animals, and microorganisms, as opposed to fossil fuel-based alternatives. These materials play a crucial role in promoting sustainability by reducing carbon footprints, mitigating climate change through carbon sequestration, and addressing the depletion of non-renewable resources. The market encompasses a wide range of products used across various industries to replace petrochemical-derived plastics and chemicals, fostering a transition toward circular and bio-based economies. This shift is essential for overcoming environmental challenges like global warming and pollution, with materials like polylactic acid (PLA) and polyethylenefuranate (PEF) exemplifying advancements in durability, processability, and application versatility.

What are the Market Dynamics in the Bio-Based Materials Industry?

Growth Drivers

The growth of the bio-based materials market is propelled by increasing governmental support through policies, regulations, subsidies, and incentives aimed at promoting renewable resources and sustainable economic models, such as the bio-based and circular economies. This support encourages industries to adopt bio-based alternatives to combat fossil fuel depletion and global warming, which have impacted the polymer sector since the late 1990s. Additionally, rising consumer awareness of environmental issues has heightened demand for eco-friendly products, driving manufacturers to innovate and expand bio-based material applications in sectors like packaging and electronics. These drivers collectively foster market expansion by aligning economic incentives with environmental sustainability goals.

Restraints

Despite the advantages, the bio-based materials market faces restraints from challenges in material properties, such as the need for enhancements in physical durability, stability, and processability for products like PLA. Competition from established fossil-based materials, which often have lower initial costs and mature supply chains, hinders widespread adoption. Furthermore, fluctuations in raw material availability from biomass sources and higher production costs due to technological limitations restrain market growth, particularly in price-sensitive regions. These factors create barriers to scaling up production and achieving cost parity with conventional alternatives.

Opportunities

Opportunities in the bio-based materials market arise from expanding applications across diverse industries, including packaging, construction, and electronics, where demand for sustainable solutions is surging. The development of new product lines by key players, coupled with advancements in material science, opens avenues for innovation in high-performance bio-polymers. Regional growth in areas like Asia Pacific, driven by increasing electronic gadget usage and consumer preference for green products, presents significant expansion potential. Additionally, global shifts toward eco-friendly policies and collaborations offer opportunities for market players to capture emerging markets and diversify portfolios.

Challenges

The market encounters challenges related to improving the inherent properties of bio-based materials to match or exceed those of fossil-based counterparts, such as in barrier performance and thermal stability. Supply chain vulnerabilities, including dependency on agricultural feedstocks that are subject to seasonal variations and geopolitical factors, pose risks to consistent production. Moreover, navigating complex regulatory landscapes and achieving certifications for bio-based claims add operational hurdles. These challenges require ongoing research and development investments to ensure long-term viability and competitiveness in the global materials landscape.

Bio-Based Materials Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Bio-Based Materials Market |

| Market Size 2025 | USD 65 Billion |

| Market Forecast 2035 | USD 650 Billion |

| Growth Rate | CAGR of 26% |

| Report Pages | 224 |

| Key Companies Covered | Anellotech Inc, Arkema, Avantium, BASF SE, Braskem, Clariant, Corbion, DSM, Dupont, Eastman Chemical Company. |

| Segments Covered | By Product Type, By Application, By End-Use, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of the Bio-Based Materials Market?

The Bio-Based Materials market is segmented by type, application, end-user, and region.

Based on Type Segment, Bio-Based Polyethylene Terephthalate (PET) is the most dominant subsegment, holding approximately 35% of the market share, followed by Bio-Based Polyethylene (PE) as the second most dominant with around 25%. Bio-Based PET leads due to its superior gas barrier properties and compatibility with existing recycling infrastructure, making it ideal for beverage bottles and food packaging, which drives market growth by enabling seamless replacement of fossil-based PET and supporting sustainability initiatives; meanwhile, Bio-Based PE’s dominance stems from its versatility in flexible packaging and films, contributing to market expansion through reduced environmental impact and alignment with consumer demands for recyclable materials.

Based on Application Segment, Rigid Packaging is the most dominant subsegment, capturing about 30% of the market, with Flexible Packaging as the second most dominant at roughly 20%. Rigid Packaging dominates because of its critical role in protecting goods during transport and storage, particularly in food and beverage sectors, where bio-based options like PLA enhance shelf life and reduce plastic waste, thereby propelling overall market growth; Flexible Packaging follows closely, driven by its lightweight and adaptable nature for consumer goods, helping to drive the market by offering eco-friendly alternatives that meet regulatory standards and consumer preferences for sustainable wrapping solutions.

Based on End-User Segment, Food and Beverage is the most dominant subsegment with a 40% share, followed by Automotive as the second most dominant at 15%. Food and Beverage leads owing to the industry’s emphasis on sustainable packaging to comply with environmental regulations and appeal to eco-conscious consumers, driving market growth through innovations that extend product freshness and minimize carbon emissions; Automotive’s position is bolstered by the integration of bio-based materials in lightweight components for fuel efficiency, contributing to market advancement by supporting the shift toward greener transportation and reducing dependency on petroleum-derived parts.

What are the Recent Developments in the Bio-Based Materials Market?

- In early 2025, BASF SE announced a partnership with a leading biomass supplier to expand production of bio-based polyamides, focusing on enhancing material strength for automotive applications and aiming to capture a larger share in the sustainable materials sector.

- Avantium launched a new commercial-scale plant for polyethylenefuranate (PEF) in late 2024, targeting the packaging industry with improved barrier properties, which is expected to accelerate adoption in beverage containers and reduce plastic pollution.

- Corbion introduced an advanced polylactic acid (PLA) variant in 2025, optimized for electronics packaging, addressing durability challenges and supporting the growing demand for eco-friendly consumer electronics components.

- DSM collaborated with Toyota Tsusho Corporation in 2025 to develop bio-based polycarbonates for construction materials, emphasizing regional expansion in Asia Pacific to meet rising infrastructure needs with sustainable alternatives.

What is the Regional Analysis of the Bio-Based Materials Market?

- Europe to dominate the global market

Europe exhibits strong dominance in the bio-based materials market, driven by robust policy frameworks like the European Commission’s Europe 2020 strategy aimed at reducing greenhouse gas emissions and promoting a circular economy. The region’s emphasis on innovation, with countries like Germany leading in research and development for bio-polymers, supports widespread adoption across packaging and automotive sectors. Germany, as the dominating country, contributes significantly through its advanced manufacturing capabilities and subsidies for renewable materials, fostering market growth by encouraging investments in sustainable technologies and aligning with EU-wide environmental targets.

Asia Pacific is poised for rapid growth, fueled by increasing demand for sustainable products in electronics and packaging amid rising environmental awareness. The region’s expanding industrial base, particularly in China, drives adoption of bio-based materials to address pollution concerns and comply with emerging green regulations. China dominates within the region due to its massive manufacturing sector and government incentives for bio-economy initiatives, propelling market expansion by integrating bio-materials into consumer goods and automotive production, thus enhancing export capabilities and reducing fossil fuel dependency.

North America shows steady progress, supported by consumer preferences for eco-friendly products and investments in bio-based innovations. The U.S. leads the region with initiatives like subsidies for biomass utilization and collaborations between tech firms and material producers. As the dominating country, the U.S. accelerates market growth through advancements in applications like construction and textiles, driven by regulatory pressures to lower carbon footprints and a strong focus on sustainable supply chains.

Latin America experiences emerging growth, primarily from agricultural biomass availability and efforts to diversify economies away from fossil fuels. Brazil dominates the region, leveraging its abundant sugarcane resources for bio-based polyethylene production, which supports market development by exporting sustainable materials and aligning with global trends toward renewable alternatives in packaging and consumer goods.

Middle East and Africa (MEA) lags but holds potential through investments in bio-based projects to mitigate oil dependency. South Africa emerges as a key player, focusing on bio-materials for construction and agriculture, driving gradual market growth via partnerships with international firms and local policies promoting environmental sustainability.

Who are the Key Market Players in the Bio-Based Materials Market?

Anellotech, Inc. focuses on developing innovative catalytic processes for converting biomass into bio-based chemicals, emphasizing research and development to expand its product portfolio and form strategic partnerships for regional market penetration.

Arkema employs strategies centered on mergers and acquisitions to enhance its bio-based polyamide offerings, investing in technology advancements to improve material performance and target high-growth applications in automotive and electronics.

Avantium prioritizes new technology launches, such as its PEF production, through joint ventures and collaborations to scale up commercial operations and address sustainability demands in packaging.

BASF SE leverages extensive research and development, along with regional expansions and agreements, to dominate in bio-based polycarbonates and polyamides, focusing on sustainable innovations for diverse industries.

Braskem adopts partnerships and investments in bio-based polyethylene production, utilizing Brazil’s biomass resources to drive exports and comply with global environmental standards.

Clariant emphasizes product portfolio diversification through technology advancements and collaborations, targeting consumer goods and construction sectors with eco-friendly additives.

Corbion pursues agreements and research initiatives to enhance PLA formulations, expanding into electronics and packaging via strategic alliances.

DSM focuses on joint ventures and mergers to advance bio-based materials for automotive and textiles, prioritizing sustainability and market share growth.

Dupont invests in new launches and partnerships for bio-polymers, aiming at electrics and consumer goods with a focus on circular economy principles.

Eastman Chemical Company employs regional expansion and technology investments to develop bio-based alternatives, targeting flexible packaging and building applications.

What are the Market Trends in the Bio-Based Materials Industry?

- Increasing integration of bio-based materials in packaging solutions, such as PEF and PLA, to improve barrier properties and reduce environmental impact.

- Shift toward circular economy models, with emphasis on recyclable and biodegradable alternatives to fossil-based plastics.

- Rising consumer preference for sustainable products in electronics and automotive sectors, driving innovation in lightweight bio-composites.

- Policy-driven advancements in Europe, focusing on greenhouse gas reduction and bio-economy incentives.

- Growth in Asia Pacific through demand for eco-friendly gadgets and materials in construction.

- Development of high-performance bio-polymers to overcome durability challenges in industrial applications.

- Collaborations between key players for technology sharing and market expansion.

What Market Segments and their Subsegments are Covered in the Bio-Based Materials Report?

By Product Type

- Bio-Based Polyethylene Terephthalate (PET)

- Bio-Based Polyethylene (PE)

- Bio-Polycarbonate

- Bio-Polyamide

- Bio-Polypropylene (PP)

By Application

- Rigid Packaging

- Flexible Packaging

- Textiles

- Automotive and Transport

- Consumer Goods

- Building and Construction

- Electrics and Electronics

- Others

By End-Use

- Food and Beverage

- Healthcare

- Automotive

- Textiles

- Electronics

- Construction

- Consumer Goods

- Packaging

- Agriculture

- Industrial

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

1.1 Report Description and Scope1.2 Research Scope1.3 Research Methodology1.3.1 Market Research Type1.3.2 Market Research MethodologyChapter 2. Executive Summary

2.1 Global Bio-Based Materials Market, (2026 - 2035) (USD Billion)2.2 Global Bio-Based Materials Market: SnapshotChapter 3. Global Bio-Based Materials Market - Industry Analysis

3.1 Bio-Based Materials Market: Market Dynamics3.2 Market Drivers3.2.1 The bio-based materials market is driven by strong government support for sustainable policies, rising environmental awareness, and growing demand for eco-friendly alternatives across industries such as packaging and electronics.3.3 Market Restraints3.3.1 The bio-based materials market is restrained by performance limitations, higher production costs, raw material supply fluctuations, and strong competition from lower-cost, fossil-based materials with established supply chains.3.4 Market Opportunities3.4.1 The bio-based materials market presents opportunities through expanding applications across industries, innovation in high-performance bio-polymers, strong growth in Asia Pacific, and rising global adoption of eco-friendly policies and collaborations.3.5 Market Challenges3.5.1 The bio-based materials market faces challenges in enhancing material performance, managing supply chain vulnerabilities, navigating complex regulations, and securing certifications, requiring continuous R&D investment for competitiveness.3.6 Porter’s Five Forces Analysis3.7 Market Attractiveness Analysis3.7.1 Market Attractiveness Analysis By Product Type3.7.2 Market Attractiveness Analysis By Application3.7.3 Market Attractiveness Analysis By End-UseChapter 4. Global Bio-Based Materials Market- Competitive Landscape

4.1 Company Market Share Analysis4.1.1 Global Bio-Based Materials Market: Company Market Share, 20254.2 Strategic Development4.2.1 Acquisitions & mergers4.2.2 New Product launches4.2.3 Agreements, partnerships, collaborations, and joint ventures4.2.4 Research and development and regional expansion4.3 Price Trend AnalysisChapter 5. Global Bio-Based Materials Market - Product Type Analysis

5.1 Global Bio-Based Materials Market Overview: Product Type5.1.1 Global Bio-Based Materials Market share, By Product Type, 2025 and 20355.2 Bio-Based Polyethylene Terephthalate (PET)5.2.1 Global Bio-Based Materials Market by Bio-Based Polyethylene Terephthalate (PET), 2026 - 2035 (USD Billion)5.3 Bio-Based Polyethylene (PE)5.3.1 Global Bio-Based Materials Market by Bio-Based Polyethylene (PE), 2026 - 2035 (USD Billion)5.4 Bio-Polycarbonate5.4.1 Global Bio-Based Materials Market by Bio-Polycarbonate, 2026 - 2035 (USD Billion)5.5 Bio-Polyamide5.5.1 Global Bio-Based Materials Market by Bio-Polyamide, 2026 - 2035 (USD Billion)5.6 Bio-Polypropylene (PP)5.6.1 Global Bio-Based Materials Market by Bio-Polypropylene (PP), 2026 - 2035 (USD Billion)5.7 Others5.7.1 Global Bio-Based Materials Market by Others, 2026 - 2035 (USD Billion)Chapter 6. Global Bio-Based Materials Market - Application Analysis

6.1 Global Bio-Based Materials Market Overview: Application6.1.1 Global Bio-Based Materials Market Share, By Application, 2025 and 20356.2 Rigid Packaging6.2.1 Global Bio-Based Materials Market by Rigid Packaging, 2026 - 2035 (USD Billion)6.3 Flexible Packaging6.3.1 Global Bio-Based Materials Market by Flexible Packaging, 2026 - 2035 (USD Billion)6.4 Textiles6.4.1 Global Bio-Based Materials Market by Textiles, 2026 - 2035 (USD Billion)6.5 Automotive & Transport6.5.1 Global Bio-Based Materials Market by Automotive & Transport, 2026 - 2035 (USD Billion)6.6 Consumer Goods6.6.1 Global Bio-Based Materials Market by Consumer Goods, 2026 - 2035 (USD Billion)6.7 Building & Construction6.7.1 Global Bio-Based Materials Market by Building & Construction, 2026 - 2035 (USD Billion)6.8 Electrics & Electronics6.8.1 Global Bio-Based Materials Market by Electrics & Electronics, 2026 - 2035 (USD Billion)6.9 Others6.9.1 Global Bio-Based Materials Market by Others, 2026 - 2035 (USD Billion)Chapter 7. Global Bio-Based Materials Market - End-Use Analysis

7.1 Global Bio-Based Materials Market Overview: End-Use7.1.1 Global Bio-Based Materials Market Share, By End-Use, 2025 and 20357.2 Food & Beverage7.2.1 Global Bio-Based Materials Market by Food & Beverage, 2026 - 2035 (USD Billion)7.3 Healthcare7.3.1 Global Bio-Based Materials Market by Healthcare, 2026 - 2035 (USD Billion)7.4 Automotive7.4.1 Global Bio-Based Materials Market by Automotive, 2026 - 2035 (USD Billion)7.5 Textiles7.5.1 Global Bio-Based Materials Market by Textiles, 2026 - 2035 (USD Billion)7.6 Electronics7.6.1 Global Bio-Based Materials Market by Electronics, 2026 - 2035 (USD Billion)7.7 Construction7.7.1 Global Bio-Based Materials Market by Construction, 2026 - 2035 (USD Billion)7.8 Consumer Goods7.8.1 Global Bio-Based Materials Market by Consumer Goods, 2026 - 2035 (USD Billion)7.9 Packaging7.9.1 Global Bio-Based Materials Market by Packaging, 2026 - 2035 (USD Billion)7.10 Agriculture7.10.1 Global Bio-Based Materials Market by Agriculture, 2026 - 2035 (USD Billion)7.11 Industrial7.11.1 Global Bio-Based Materials Market by Industrial, 2026 - 2035 (USD Billion)Chapter 8. Bio-Based Materials Market - Regional Analysis

8.1 Global Bio-Based Materials Market Regional Overview8.2 Global Bio-Based Materials Market Share, by Region, 2025 & 2035 (USD Billion)8.3 North America8.3.1 North America Bio-Based Materials Market, 2026 - 2035 (USD Billion)8.3.1.1 North America Bio-Based Materials Market, by Country, 2026 - 2035 (USD Billion)8.3.2 North America Bio-Based Materials Market, by Product Type, 2026 - 20358.3.2.1 North America Bio-Based Materials Market, by Product Type, 2026 - 2035 (USD Billion)8.3.3 North America Bio-Based Materials Market, by Application, 2026 - 20358.3.3.1 North America Bio-Based Materials Market, by Application, 2026 - 2035 (USD Billion)8.3.4 North America Bio-Based Materials Market, by End-Use, 2026 - 20358.3.4.1 North America Bio-Based Materials Market, by End-Use, 2026 - 2035 (USD Billion)8.4 Europe8.4.1 Europe Bio-Based Materials Market, 2026 - 2035 (USD Billion)8.4.1.1 Europe Bio-Based Materials Market, by Country, 2026 - 2035 (USD Billion)8.4.2 Europe Bio-Based Materials Market, by Product Type, 2026 - 20358.4.2.1 Europe Bio-Based Materials Market, by Product Type, 2026 - 2035 (USD Billion)8.4.3 Europe Bio-Based Materials Market, by Application, 2026 - 20358.4.3.1 Europe Bio-Based Materials Market, by Application, 2026 - 2035 (USD Billion)8.4.4 Europe Bio-Based Materials Market, by End-Use, 2026 - 20358.4.4.1 Europe Bio-Based Materials Market, by End-Use, 2026 - 2035 (USD Billion)8.5 Asia Pacific8.5.1 Asia Pacific Bio-Based Materials Market, 2026 - 2035 (USD Billion)8.5.1.1 Asia Pacific Bio-Based Materials Market, by Country, 2026 - 2035 (USD Billion)8.5.2 Asia Pacific Bio-Based Materials Market, by Product Type, 2026 - 20358.5.2.1 Asia Pacific Bio-Based Materials Market, by Product Type, 2026 - 2035 (USD Billion)8.5.3 Asia Pacific Bio-Based Materials Market, by Application, 2026 - 20358.5.3.1 Asia Pacific Bio-Based Materials Market, by Application, 2026 - 2035 (USD Billion)8.5.4 Asia Pacific Bio-Based Materials Market, by End-Use, 2026 - 20358.5.4.1 Asia Pacific Bio-Based Materials Market, by End-Use, 2026 - 2035 (USD Billion)8.6 Latin America8.6.1 Latin America Bio-Based Materials Market, 2026 - 2035 (USD Billion)8.6.1.1 Latin America Bio-Based Materials Market, by Country, 2026 - 2035 (USD Billion)8.6.2 Latin America Bio-Based Materials Market, by Product Type, 2026 - 20358.6.2.1 Latin America Bio-Based Materials Market, by Product Type, 2026 - 2035 (USD Billion)8.6.3 Latin America Bio-Based Materials Market, by Application, 2026 - 20358.6.3.1 Latin America Bio-Based Materials Market, by Application, 2026 - 2035 (USD Billion)8.6.4 Latin America Bio-Based Materials Market, by End-Use, 2026 - 20358.6.4.1 Latin America Bio-Based Materials Market, by End-Use, 2026 - 2035 (USD Billion)8.7 The Middle-East and Africa8.7.1 The Middle-East and Africa Bio-Based Materials Market, 2026 - 2035 (USD Billion)8.7.1.1 The Middle-East and Africa Bio-Based Materials Market, by Country, 2026 - 2035 (USD Billion)8.7.2 The Middle-East and Africa Bio-Based Materials Market, by Product Type, 2026 - 20358.7.2.1 The Middle-East and Africa Bio-Based Materials Market, by Product Type, 2026 - 2035 (USD Billion)8.7.3 The Middle-East and Africa Bio-Based Materials Market, by Application, 2026 - 20358.7.3.1 The Middle-East and Africa Bio-Based Materials Market, by Application, 2026 - 2035 (USD Billion)8.7.4 The Middle-East and Africa Bio-Based Materials Market, by End-Use, 2026 - 20358.7.4.1 The Middle-East and Africa Bio-Based Materials Market, by End-Use, 2026 - 2035 (USD Billion)Chapter 9. Company Profiles

9.1 Anellotech Inc9.1.1 Overview9.1.2 Financials9.1.3 Product Portfolio9.1.4 Business Strategy9.1.5 Recent Developments9.2 Arkema9.2.1 Overview9.2.2 Financials9.2.3 Product Portfolio9.2.4 Business Strategy9.2.5 Recent Developments9.3 Avantium9.3.1 Overview9.3.2 Financials9.3.3 Product Portfolio9.3.4 Business Strategy9.3.5 Recent Developments9.4 BASF SE9.4.1 Overview9.4.2 Financials9.4.3 Product Portfolio9.4.4 Business Strategy9.4.5 Recent Developments9.5 Braskem9.5.1 Overview9.5.2 Financials9.5.3 Product Portfolio9.5.4 Business Strategy9.5.5 Recent Developments9.6 Clariant9.6.1 Overview9.6.2 Financials9.6.3 Product Portfolio9.6.4 Business Strategy9.6.5 Recent Developments9.7 Corbion9.7.1 Overview9.7.2 Financials9.7.3 Product Portfolio9.7.4 Business Strategy9.7.5 Recent Developments9.8 DSM9.8.1 Overview9.8.2 Financials9.8.3 Product Portfolio9.8.4 Business Strategy9.8.5 Recent Developments9.9 Dupont9.9.1 Overview9.9.2 Financials9.9.3 Product Portfolio9.9.4 Business Strategy9.9.5 Recent Developments9.10 Eastman Chemical Company9.10.1 Overview9.10.2 Financials9.10.3 Product Portfolio9.10.4 Business Strategy9.10.5 Recent Developments

Frequently Asked Questions

Bio-based materials are substances derived from renewable biological sources like plants, agricultural byproducts, and microorganisms, offering sustainable alternatives to fossil fuel-based products to reduce environmental impact.

Key factors include favorable government policies, rising consumer awareness for eco-friendly products, advancements in material technologies, and expanding applications across industries like packaging and automotive.

The market is projected to grow from USD 65 billion in 2025 to USD 650 billion by 2035.

The CAGR is expected to be 26% during the forecast period.

Europe will contribute notably, holding a dominant 40% share due to strong regulatory support and innovation in sustainable materials.

Major players include Anellotech Inc., Arkema, Avantium, BASF SE, Braskem, Clariant, Corbion, DSM, Dupont, and Eastman Chemical Company, among others, driving growth through innovations and strategic partnerships.

The report provides comprehensive analysis including market size, trends, segmentation, regional insights, key players, and forecasts to guide strategic decisions.

The value chain includes feedstock sourcing from biomass, production and processing of bio-polymers, distribution and supply to manufacturers, and end-use integration in products like packaging.

Trends are shifting toward recyclable and high-performance materials, with consumers preferring eco-friendly options that align with sustainability goals and reduce plastic waste.

Factors include government subsidies for renewables, emission reduction policies like Europe's 2020 strategy, and environmental regulations promoting circular economies and bio-based alternatives.