Cyber Security in Healthcare Market Size, Share and Trends 2026 to 2035

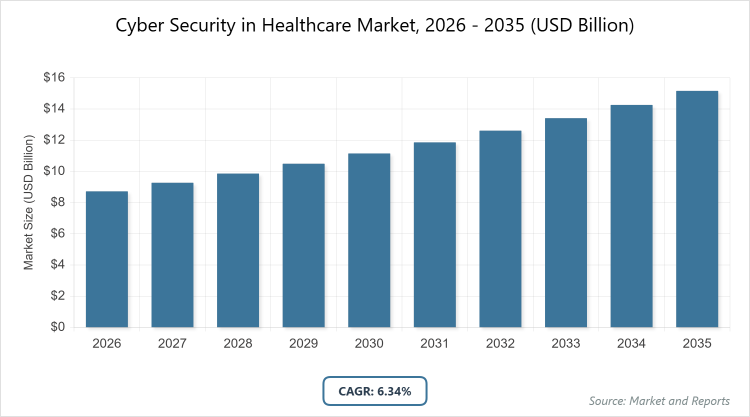

According to MarketnReports, the global Cyber Security in Healthcare market size was estimated at USD 8.72 billion in 2025 and is expected to reach USD 16.18 billion by 2035, growing at a CAGR of 6.34% from 2026 to 2035. Cyber Security in Healthcare Market is driven by increasing digitization of patient data, escalating cyber threats, regulatory pressures, telehealth adoption, and reliance on cloud-based systems.

What are the Key Insights of Cyber Security in Healthcare Market?

- The global Cyber Security in Healthcare market size was estimated at USD 8.72 billion in 2025 and is expected to reach USD 16.18 billion by 2035.

- The market is projected to grow at a CAGR of 6.34% from 2026 to 2035.

- The market is driven by the surge in cyberattacks targeting sensitive patient data, increasing adoption of telemedicine, and growing regulatory requirements for data protection and compliance.

- In the Security Solutions segment, Network Security Platforms dominate with a 39.4% share.

- Network Security Platforms dominate due to their foundational role in safeguarding hospital networks, devices, and communication channels against data breaches and ransomware attacks.

- In the Threat Type segment, Ransomware dominates with the largest share.

- Ransomware dominates because of the alarming rise in targeted attacks on hospitals and clinics, causing operational disruptions and financial losses, with healthcare seen as soft targets due to critical nature and legacy systems.

- In the Deployment segment, Cloud-Based dominates with the largest share.

- Cloud-Based dominates attributed to scalability, cost-efficiency, and centralized management, prominent with digitization, telemedicine, and cloud-hosted EHRs.

- In the End-User segment, Hospitals dominate with an estimated 45% share.

- Hospitals dominate as they handle the largest volume of sensitive patient data and connected devices, making them prime targets for cyber threats and requiring robust security measures.

- North America dominates the market with a 42.1% share.

- North America dominates due to highly digitized healthcare infrastructure, stringent data privacy regulations such as HIPAA, and a strong presence of leading cyber security providers.

What is the Industry Overview of Cyber Security in Healthcare Market?

Cyber security in healthcare involves the protection of electronic health records, medical devices, and hospital infrastructure from unauthorized access and cyber threats. It encompasses a range of solutions and services designed to safeguard sensitive patient information and ensure the integrity of healthcare operations in an increasingly digital environment. The market definition highlights its critical role in addressing vulnerabilities arising from the expansion of connected healthcare technologies, including telehealth platforms, cloud-based systems, and IoT-enabled medical devices, in both clinical and non-clinical settings. This industry is essential for maintaining patient privacy, preventing data breaches, and supporting regulatory compliance amid rising cyber risks.

What are the Market Dynamics of Cyber Security in Healthcare?

Growth Drivers

The primary growth drivers for the Cyber Security in Healthcare market include the rising cyber threat landscape and rapid healthcare digitalization. This encompasses the increasing frequency and sophistication of cyberattacks, the surge in remote consultations, the adoption of cloud-based electronic health records (EHRs), and the proliferation of connected medical devices. Additionally, stringent compliance requirements, such as HIPAA in the U.S. and GDPR in Europe, compel healthcare organizations to upgrade their security measures to avoid substantial penalties. The growing reliance on third-party vendors, telehealth platforms, and mobile health applications further expands the threat surface, necessitating advanced security solutions. Regulatory initiatives, like the U.S. Department of Health and Human Services’ efforts to enhance hospital cybersecurity through funding, also propel market expansion by encouraging investments in robust defenses.

Restraints

Key restraints in the Cyber Security in Healthcare market revolve around budget constraints and a shortage of skilled cybersecurity talent, particularly affecting small and rural healthcare facilities. Surveys indicate that a significant portion of providers face barriers due to limited financial resources and staffing issues, hindering the implementation of comprehensive security systems. Moreover, the complexity of managing cybersecurity in highly regulated environments requires ongoing compliance monitoring, audits, and specialized expertise, which many organizations struggle to maintain. Fragmented healthcare IT systems and outdated legacy infrastructure further complicate the uniform deployment of security measures, leading to vulnerabilities. The perception of cybersecurity as a cost center rather than a strategic investment often results in delayed upgrades and insufficient proactive measures.

Opportunities

Opportunities in the Cyber Security in Healthcare market are abundant with the rise of advanced technologies in cyber defense, such as AI and machine learning for real-time threat detection and automated response. The increasing adoption of telehealth services creates demand for scalable, secure solutions tailored to remote care models, enabling providers to expand their offerings safely. Emerging markets in regions like Asia-Pacific present growth potential through government initiatives promoting healthcare digitization and cybersecurity awareness. Partnerships between cybersecurity firms and healthcare institutions can foster innovative, industry-specific solutions, while the integration of zero-trust frameworks offers enhanced protection against evolving threats. Overall, these opportunities allow for the development of cost-effective, compliant security ecosystems that address the expanding digital footprint in healthcare.

Challenges

Challenges in the Cyber Security in Healthcare market include the evolving nature of cyber threats, which require continuous adaptation of security protocols and technologies. The integration of legacy systems with modern digital infrastructure poses significant hurdles, as older equipment often lacks built-in security features, making it susceptible to exploits. Additionally, ensuring user awareness and training among healthcare staff remains a persistent issue, as human error, such as falling for phishing attempts, accounts for a large portion of breaches. Regulatory variations across regions complicate global standardization, while the high cost of advanced security tools can strain budgets. Balancing security with operational efficiency, such as minimizing downtime during updates, further exacerbates these challenges in a sector where uninterrupted service is critical.

Cyber Security in Healthcare Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Cyber Security in Healthcare Market |

| Market Size 2025 | USD 8.72 Billion |

| Market Forecast 2035 | USD 16.18 Billion |

| Growth Rate | CAGR of 6.34% |

| Report Pages | 218 |

| Key Companies Covered | IBM, Palo Alto Networks, Fortinet, Cisco, Trend Micro, Lockheed Martin Corporation, Check Point Software Technologies Ltd., CyberArk Software Ltd., F5 Inc., and FireEye Inc. |

| Segments Covered | By Security Solutions, By Threat Type, By Deployment, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Cyber Security in Healthcare?

The Cyber Security in Healthcare market is segmented by security solutions, threat type, deployment, end-user, and region.

Based on Security Solutions Segment. The most dominant segment is Network Security Platforms, holding a 39.4% share, due to its essential function in protecting internal networks, EHR systems, and cloud databases through tools like intrusion prevention systems, secure VPNs, and firewalls; this dominance drives the market by providing a foundational layer of defense against widespread threats like data breaches and ransomware, enabling secure data exchange and compliance with regulations. The second most dominant is Application Security Tools, which supports market growth by securing software applications and APIs used in healthcare, preventing vulnerabilities that could lead to unauthorized access and contributing to overall system resilience.

Based on Threat Type Segment. The most dominant segment is Ransomware, leading due to its prevalence in targeting healthcare facilities with disruptive attacks that halt operations and demand ransoms, driven by the sector’s critical data and legacy systems; this drives the market by necessitating specialized detection and recovery solutions, boosting investments in backup systems and AI-based prevention. The second most dominant is Phishing, which grows rapidly through sophisticated social engineering tactics, compelling the adoption of email security and employee training programs that enhance overall cybersecurity posture and market expansion.

Based on Deployment Segment. The most dominant segment is Cloud-Based, prevailing because of its scalability, cost-efficiency, and ease of management for digitized healthcare services like telemedicine and cloud-hosted EHRs; it drives the market by facilitating remote access and data sharing while integrating advanced security features, attracting more providers to cloud environments. The second most dominant is On-Premises, which aids market growth in settings requiring strict data control and sovereignty, supporting customized security implementations that complement hybrid models.

Based on End-User Segment. The most dominant segment is Hospitals, with an estimated 45% share, as they manage vast amounts of patient data and connected devices, making them high-risk targets and driving demand for comprehensive security; this dominance propels the market by prioritizing investments in endpoint and network protection, setting standards for the industry. The second most dominant is Pharmaceutical Companies, which contributes by securing intellectual property and supply chains against espionage, fostering innovation in tailored cybersecurity solutions.

What are the Recent Developments in Cyber Security in Healthcare Market?

- In April 2023, IBM launched an AI-driven threat detection feature in its IBM Security QRadar Suite specifically for healthcare applications, allowing for early identification of anomalies in networks and EHR systems to prevent potential breaches. This development focuses on providing industry-specific solutions with real-time analytics and automated compliance reporting, enhancing the ability of healthcare providers to respond swiftly to emerging threats.

- In March 2023, Palo Alto Networks entered into a partnership with NHS Digital in the U.K. to bolster cybersecurity infrastructure across various healthcare trusts, implementing next-generation firewalls and advanced endpoint protection to combat ransomware and other attacks. This collaboration emphasizes building collaborative defense mechanisms, sharing threat intelligence, and ensuring seamless integration with existing systems to improve overall resilience in public health networks.

- In February 2023, Fortinet introduced a Zero Trust Network Access (ZTNA) framework tailored for the healthcare sector, focusing on secure remote access for telemedicine and mobile health applications. The framework integrates multi-factor authentication, device health checks, and granular application access controls, reflecting a shift towards adaptive security models that address the dynamic nature of healthcare delivery and protect against insider and external threats.

- In February 2023, Cisco deployed its SecureX platform in several hospitals across Southeast Asia, offering unified visibility, threat hunting, and automation capabilities to manage cybersecurity in rapidly digitalizing environments. This initiative supports scalable infrastructure protection, real-time monitoring, and incident response, helping healthcare organizations maintain operational continuity amid increasing cyber incidents.

- In January 2023, Trend Micro collaborated with the Philippine General Hospital to implement advanced endpoint protection and data loss prevention measures, securing sensitive patient information in cloud-based systems. This partnership highlights the importance of public-private collaborations in emerging markets, providing customized solutions that address local regulatory requirements and the growing use of digital health tools.

What is the Regional Analysis of Cyber Security in Healthcare Market?

- North America to dominate the global market

North America is poised to maintain its dominance in the Cyber Security in Healthcare market, holding a 42.1% revenue share, driven by its highly digitized healthcare infrastructure, stringent regulations like HIPAA, and the presence of leading cybersecurity providers. The region benefits from advanced adoption of AI-based threat detection and cloud security solutions, with significant investments in protecting electronic health records and connected devices. The United States stands as the dominating country, accounting for 82.3% of the regional share, fueled by rapid EHR adoption, frequent ransomware threats, and rigorous enforcement of data privacy laws, which encourage continuous innovation and compliance-driven upgrades.

Europe is expected to expand at a substantial CAGR, propelled by GDPR compliance, rising cyberattacks, and the digitization of healthcare services through cloud-based EHRs and infrastructure enhancements. Cross-border data sharing initiatives further necessitate robust security measures. The United Kingdom anticipates a noteworthy CAGR, with the NHS’s digital transformation, increasing cyber incidents, and policies emphasizing data security and cloud adoption in telemedicine. Germany is another key player, with government commitments to digital health infrastructure, integration of EHRs and telemedicine, strict data privacy standards, and responses to growing cyber threats driving market growth.

Asia-Pacific is set for the fastest growth with a CAGR of 25.4% from 2026 to 2035, attributed to rapid digital transformation in countries like China, India, and Japan, alongside escalating cyberattacks, supportive regulations, and the surge in telehealth. Expanding healthcare IT investments and awareness of data protection are key factors. India holds the largest share in the region, driven by rapid digitalization, threat awareness, the National Digital Health Mission, expanding hospital networks, cybersecurity startups, and adoption of cloud, identity, and endpoint solutions amid rising patient data volumes and wearable technologies. Japan is gaining momentum through technological innovations, data privacy emphasis, cyber resilience, AI-driven solutions, zero-trust frameworks, and government efforts to modernize healthcare IT for an aging population.

Latin America experiences steady growth, supported by increasing healthcare digitization and awareness of cyber risks, though challenged by infrastructure limitations. Brazil emerges as the dominating country, with investments in telehealth and EHR systems, regulatory pushes for data security, and collaborations with global cybersecurity firms to address rising threats in public and private healthcare sectors.

The Middle East and Africa (MEA) shows emerging potential, driven by government initiatives in digital health and rising investments in cybersecurity to protect expanding hospital networks and patient data. The United Arab Emirates (UAE) is the dominating country, with advanced healthcare infrastructure, adoption of cloud-based solutions, and strict regulations promoting secure telemedicine and EHRs, positioning it as a regional leader in cyber defense.

Who are the Key Market Players in Cyber Security in Healthcare?

IBM focuses on AI-powered threat detection solutions, such as the QRadar Suite, tailored for healthcare to enable real-time anomaly identification and compliance with regulations like HIPAA, enhancing proactive defense against breaches through machine learning and analytics integration.

Palo Alto Networks emphasizes partnerships with healthcare organizations, like NHS Digital, to deploy next-generation firewalls and endpoint protection, strategies that involve threat intelligence sharing and seamless system integration to combat ransomware and improve infrastructure resilience.

Fortinet adopts Zero Trust Network Access frameworks for secure remote access in telemedicine, incorporating multi-factor authentication and device checks, with a focus on adaptive security models that address evolving threats in connected healthcare environments.

Cisco deploys unified platforms like SecureX for visibility and automation in hospital settings, prioritizing scalable solutions that support digitalization while providing real-time monitoring and incident response to maintain operational continuity.

Trend Micro engages in collaborations with hospitals for endpoint protection and data loss prevention, customizing solutions for cloud systems and regulatory compliance, highlighting public-private partnerships to secure patient data in emerging markets.

Lockheed Martin Corporation leverages defense expertise to offer comprehensive cybersecurity services, including risk assessments and managed security, aimed at protecting critical healthcare infrastructure from advanced persistent threats.

Check Point Software Technologies Ltd. provides multi-layered security platforms with a focus on preventing phishing and malware, using AI to enhance threat prevention in healthcare networks and ensuring compliance through encrypted communications.

CyberArk Software Ltd. specializes in identity and access management, implementing privileged access controls to safeguard sensitive health data, with strategies centered on reducing insider risks and supporting zero-trust architectures.

F5 Inc. offers application security tools that protect web and API interfaces in healthcare applications, emphasizing DDoS mitigation and bot defense to ensure secure digital patient interactions.

FireEye Inc. (now part of Mandiant) focuses on advanced threat intelligence and incident response services, helping healthcare providers detect and remediate sophisticated attacks through forensic analysis and proactive hunting.

What are the Market Trends in Cyber Security in Healthcare?

- Increasing implementation of AI and machine learning for real-time threat detection, response, and prevention, enabling predictive analysis and automatic responses to safeguard patient data and ensure regulatory compliance.

- Growing adoption of cloud-integrated security solutions for centralized monitoring and scalability, particularly in telemedicine and EHR systems, with providers like IBM and Palo Alto offering healthcare-specific tools.

- Shift towards zero-trust frameworks that emphasize identity verification, device checks, and granular access controls, addressing the dynamic nature of remote care and connected medical devices.

- Emphasis on employee training and awareness programs to combat phishing and social engineering attacks, as human error remains a significant vulnerability in healthcare settings.

- Rise in partnerships between cybersecurity firms and healthcare institutions for tailored solutions, including public-private collaborations to enhance resilience in developing regions.

- Integration of cybersecurity with IoT and medical device management, focusing on endpoint detection and response to protect against vulnerabilities in connected health technologies.

- Focus on regulatory compliance through automated tools that support HIPAA, GDPR, and other standards, reducing the burden of audits and penalties.

- Emergence of blockchain for secure data sharing and integrity in healthcare supply chains, offering tamper-proof records for patient information and pharmaceutical tracking.

- Adoption of managed security services for organizations lacking in-house expertise, providing cost-effective outsourcing for monitoring and incident management.

- Increasing use of big data analytics for threat intelligence, allowing healthcare providers to anticipate and mitigate risks based on global cyber trends.

What are the Market Segments and their Subsegments Covered in the Cyber Security in Healthcare Report?

By Security Solutions

- Antivirus Software

- Firewalls

- Intrusion Detection Systems

- Encryption Tools

- Identity Access Management

- Endpoint Protection

- Network Security Platforms

- Application Security Tools

- Cloud Security Solutions

- Device Security Systems

- Others

By Threat Type

- Ransomware

- Malware

- Spyware

- DDoS

- Phishing

- Spear-Phishing

- Advanced Persistent Threats

- Insider Threats

- Data Breaches

- Zero-Day Attacks

- Others

By Deployment

- Cloud-Based

- On-Premises

- Others

By End-User

- Hospitals

- Clinics

- Pharmaceutical Companies

- Health Insurance Providers

- Medical Device Manufacturers

- Research Institutions

- Telehealth Providers

- Diagnostic Centers

- Ambulatory Surgical Centers

- Government Health Agencies

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

1.1 Report Description and Scope1.2 Research Scope1.3 Research Methodology1.3.1 Market Research Type1.3.2 Market Research MethodologyChapter 2. Executive Summary

2.1 Global Cyber Security in Healthcare Market, (2026 - 2035) (USD Billion)2.2 Global Cyber Security in Healthcare Market: SnapshotChapter 3. Global Cyber Security in Healthcare Market - Industry Analysis

3.1 Cyber Security in Healthcare Market: Market Dynamics3.2 Market Drivers3.2.1 The Cyber Security in Healthcare market is driven by rising cyber threats, rapid digitalization of healthcare systems, stringent regulatory compliance requirements, increased use of cloud EHRs, connected medical devices, telehealth platforms, and government initiatives promoting stronger cybersecurity investments.3.3 Market Restraints3.3.1 The Cyber Security in Healthcare market is restrained by budget limitations, shortages of skilled cybersecurity professionals, complex compliance demands, fragmented and legacy IT systems, and the perception of cybersecurity as a cost rather than a strategic investment.3.4 Market Opportunities3.4.1 The Cyber Security in Healthcare market offers strong opportunities through AI- and ML-based threat detection, expanding telehealth adoption, growth in emerging markets, strategic partnerships, and the implementation of zero-trust security frameworks to protect expanding digital healthcare ecosystems.3.5 Market Challenges3.5.1 The Cyber Security in Healthcare market faces challenges from evolving cyber threats, legacy system integration issues, human error risks, regulatory variations, high security costs, and the need to balance strong protection with uninterrupted healthcare operations.3.6 Porter’s Five Forces Analysis3.7 Market Attractiveness Analysis3.7.1 Market Attractiveness Analysis By Security Solutions3.7.2 Market Attractiveness Analysis By Threat Type3.7.3 Market Attractiveness Analysis By Deployment3.7.4 Market Attractiveness Analysis By End-UserChapter 4. Global Cyber Security in Healthcare Market- Competitive Landscape

4.1 Company Market Share Analysis4.1.1 Global Cyber Security in Healthcare Market: Company Market Share, 20254.2 Strategic Development4.2.1 Acquisitions & mergers4.2.2 New Product launches4.2.3 Agreements, partnerships, collaborations, and joint ventures4.2.4 Research and development and regional expansion4.3 Price Trend AnalysisChapter 5. Global Cyber Security in Healthcare Market - Security Solutions Analysis

5.1 Global Cyber Security in Healthcare Market Overview: Security Solutions5.1.1 Global Cyber Security in Healthcare Market share, By Security Solutions, 2025 and 20355.2 Antivirus Software5.2.1 Global Cyber Security in Healthcare Market by Antivirus Software, 2026 - 2035 (USD Billion)5.3 Firewalls5.3.1 Global Cyber Security in Healthcare Market by Firewalls, 2026 - 2035 (USD Billion)5.4 Intrusion Detection Systems5.4.1 Global Cyber Security in Healthcare Market by Intrusion Detection Systems, 2026 - 2035 (USD Billion)5.5 Encryption Tools5.5.1 Global Cyber Security in Healthcare Market by Encryption Tools, 2026 - 2035 (USD Billion)5.6 Identity Access Management5.6.1 Global Cyber Security in Healthcare Market by Identity Access Management, 2026 - 2035 (USD Billion)5.7 Endpoint Protection5.7.1 Global Cyber Security in Healthcare Market by Endpoint Protection, 2026 - 2035 (USD Billion)5.8 Network Security Platforms5.8.1 Global Cyber Security in Healthcare Market by Network Security Platforms, 2026 - 2035 (USD Billion)5.9 Application Security Tools5.9.1 Global Cyber Security in Healthcare Market by Application Security Tools, 2026 - 2035 (USD Billion)5.10 Cloud Security Solutions5.10.1 Global Cyber Security in Healthcare Market by Cloud Security Solutions, 2026 - 2035 (USD Billion)5.11 Device Security Systems5.11.1 Global Cyber Security in Healthcare Market by Device Security Systems, 2026 - 2035 (USD Billion)Chapter 6. Global Cyber Security in Healthcare Market - Threat Type Analysis

6.1 Global Cyber Security in Healthcare Market Overview: Threat Type6.1.1 Global Cyber Security in Healthcare Market Share, By Threat Type, 2025 and 20356.2 Ransomware6.2.1 Global Cyber Security in Healthcare Market by Ransomware, 2026 - 2035 (USD Billion)6.3 Malware6.3.1 Global Cyber Security in Healthcare Market by Malware, 2026 - 2035 (USD Billion)6.4 Spyware6.4.1 Global Cyber Security in Healthcare Market by Spyware, 2026 - 2035 (USD Billion)6.5 DDoS6.5.1 Global Cyber Security in Healthcare Market by DDoS, 2026 - 2035 (USD Billion)6.6 Phishing6.6.1 Global Cyber Security in Healthcare Market by Phishing, 2026 - 2035 (USD Billion)6.7 Spear-Phishing6.7.1 Global Cyber Security in Healthcare Market by Spear-Phishing, 2026 - 2035 (USD Billion)6.8 Advanced Persistent Threats6.8.1 Global Cyber Security in Healthcare Market by Advanced Persistent Threats, 2026 - 2035 (USD Billion)6.9 Insider Threats6.9.1 Global Cyber Security in Healthcare Market by Insider Threats, 2026 - 2035 (USD Billion)6.10 Data Breaches6.10.1 Global Cyber Security in Healthcare Market by Data Breaches, 2026 - 2035 (USD Billion)6.11 Zero-Day Attacks6.11.1 Global Cyber Security in Healthcare Market by Zero-Day Attacks, 2026 - 2035 (USD Billion)Chapter 7. Global Cyber Security in Healthcare Market - Deployment Analysis

7.1 Global Cyber Security in Healthcare Market Overview: Deployment7.1.1 Global Cyber Security in Healthcare Market Share, By Deployment, 2025 and 20357.2 Cloud-Based7.2.1 Global Cyber Security in Healthcare Market by Cloud-Based, 2026 - 2035 (USD Billion)7.3 On-Premises7.3.1 Global Cyber Security in Healthcare Market by On-Premises, 2026 - 2035 (USD Billion)7.4 Others7.4.1 Global Cyber Security in Healthcare Market by Others, 2026 - 2035 (USD Billion)Chapter 8. Global Cyber Security in Healthcare Market - End-User Analysis

8.1 Global Cyber Security in Healthcare Market Overview: End-User8.1.1 Global Cyber Security in Healthcare Market Share, By End-User, 2025 and 20358.2 Hospitals8.2.1 Global Cyber Security in Healthcare Market by Hospitals, 2026 - 2035 (USD Billion)8.3 Clinics8.3.1 Global Cyber Security in Healthcare Market by Clinics, 2026 - 2035 (USD Billion)8.4 Pharmaceutical Companies8.4.1 Global Cyber Security in Healthcare Market by Pharmaceutical Companies, 2026 - 2035 (USD Billion)8.5 Health Insurance Providers8.5.1 Global Cyber Security in Healthcare Market by Health Insurance Providers, 2026 - 2035 (USD Billion)8.6 Medical Device Manufacturers8.6.1 Global Cyber Security in Healthcare Market by Medical Device Manufacturers, 2026 - 2035 (USD Billion)8.7 Research Institutions8.7.1 Global Cyber Security in Healthcare Market by Research Institutions, 2026 - 2035 (USD Billion)8.8 Telehealth Providers8.8.1 Global Cyber Security in Healthcare Market by Telehealth Providers, 2026 - 2035 (USD Billion)8.9 Diagnostic Centers8.9.1 Global Cyber Security in Healthcare Market by Diagnostic Centers, 2026 - 2035 (USD Billion)8.10 Ambulatory Surgical Centers8.10.1 Global Cyber Security in Healthcare Market by Ambulatory Surgical Centers, 2026 - 2035 (USD Billion)8.11 Government Health Agencies8.11.1 Global Cyber Security in Healthcare Market by Government Health Agencies, 2026 - 2035 (USD Billion)Chapter 9. Cyber Security in Healthcare Market - Regional Analysis

9.1 Global Cyber Security in Healthcare Market Regional Overview9.2 Global Cyber Security in Healthcare Market Share, by Region, 2025 & 2035 (USD Billion)9.3 North America9.3.1 North America Cyber Security in Healthcare Market, 2026 - 2035 (USD Billion)9.3.1.1 North America Cyber Security in Healthcare Market, by Country, 2026 - 2035 (USD Billion)9.3.2 North America Cyber Security in Healthcare Market, by Security Solutions, 2026 - 20359.3.2.1 North America Cyber Security in Healthcare Market, by Security Solutions, 2026 - 2035 (USD Billion)9.3.3 North America Cyber Security in Healthcare Market, by Threat Type, 2026 - 20359.3.3.1 North America Cyber Security in Healthcare Market, by Threat Type, 2026 - 2035 (USD Billion)9.3.4 North America Cyber Security in Healthcare Market, by Deployment, 2026 - 20359.3.4.1 North America Cyber Security in Healthcare Market, by Deployment, 2026 - 2035 (USD Billion)9.3.5 North America Cyber Security in Healthcare Market, by End-User, 2026 - 20359.3.5.1 North America Cyber Security in Healthcare Market, by End-User, 2026 - 2035 (USD Billion)9.4 Europe9.4.1 Europe Cyber Security in Healthcare Market, 2026 - 2035 (USD Billion)9.4.1.1 Europe Cyber Security in Healthcare Market, by Country, 2026 - 2035 (USD Billion)9.4.2 Europe Cyber Security in Healthcare Market, by Security Solutions, 2026 - 20359.4.2.1 Europe Cyber Security in Healthcare Market, by Security Solutions, 2026 - 2035 (USD Billion)9.4.3 Europe Cyber Security in Healthcare Market, by Threat Type, 2026 - 20359.4.3.1 Europe Cyber Security in Healthcare Market, by Threat Type, 2026 - 2035 (USD Billion)9.4.4 Europe Cyber Security in Healthcare Market, by Deployment, 2026 - 20359.4.4.1 Europe Cyber Security in Healthcare Market, by Deployment, 2026 - 2035 (USD Billion)9.4.5 Europe Cyber Security in Healthcare Market, by End-User, 2026 - 20359.4.5.1 Europe Cyber Security in Healthcare Market, by End-User, 2026 - 2035 (USD Billion)9.5 Asia Pacific9.5.1 Asia Pacific Cyber Security in Healthcare Market, 2026 - 2035 (USD Billion)9.5.1.1 Asia Pacific Cyber Security in Healthcare Market, by Country, 2026 - 2035 (USD Billion)9.5.2 Asia Pacific Cyber Security in Healthcare Market, by Security Solutions, 2026 - 20359.5.2.1 Asia Pacific Cyber Security in Healthcare Market, by Security Solutions, 2026 - 2035 (USD Billion)9.5.3 Asia Pacific Cyber Security in Healthcare Market, by Threat Type, 2026 - 20359.5.3.1 Asia Pacific Cyber Security in Healthcare Market, by Threat Type, 2026 - 2035 (USD Billion)9.5.4 Asia Pacific Cyber Security in Healthcare Market, by Deployment, 2026 - 20359.5.4.1 Asia Pacific Cyber Security in Healthcare Market, by Deployment, 2026 - 2035 (USD Billion)9.5.5 Asia Pacific Cyber Security in Healthcare Market, by End-User, 2026 - 20359.5.5.1 Asia Pacific Cyber Security in Healthcare Market, by End-User, 2026 - 2035 (USD Billion)9.6 Latin America9.6.1 Latin America Cyber Security in Healthcare Market, 2026 - 2035 (USD Billion)9.6.1.1 Latin America Cyber Security in Healthcare Market, by Country, 2026 - 2035 (USD Billion)9.6.2 Latin America Cyber Security in Healthcare Market, by Security Solutions, 2026 - 20359.6.2.1 Latin America Cyber Security in Healthcare Market, by Security Solutions, 2026 - 2035 (USD Billion)9.6.3 Latin America Cyber Security in Healthcare Market, by Threat Type, 2026 - 20359.6.3.1 Latin America Cyber Security in Healthcare Market, by Threat Type, 2026 - 2035 (USD Billion)9.6.4 Latin America Cyber Security in Healthcare Market, by Deployment, 2026 - 20359.6.4.1 Latin America Cyber Security in Healthcare Market, by Deployment, 2026 - 2035 (USD Billion)9.6.5 Latin America Cyber Security in Healthcare Market, by End-User, 2026 - 20359.6.5.1 Latin America Cyber Security in Healthcare Market, by End-User, 2026 - 2035 (USD Billion)9.7 The Middle-East and Africa9.7.1 The Middle-East and Africa Cyber Security in Healthcare Market, 2026 - 2035 (USD Billion)9.7.1.1 The Middle-East and Africa Cyber Security in Healthcare Market, by Country, 2026 - 2035 (USD Billion)9.7.2 The Middle-East and Africa Cyber Security in Healthcare Market, by Security Solutions, 2026 - 20359.7.2.1 The Middle-East and Africa Cyber Security in Healthcare Market, by Security Solutions, 2026 - 2035 (USD Billion)9.7.3 The Middle-East and Africa Cyber Security in Healthcare Market, by Threat Type, 2026 - 20359.7.3.1 The Middle-East and Africa Cyber Security in Healthcare Market, by Threat Type, 2026 - 2035 (USD Billion)9.7.4 The Middle-East and Africa Cyber Security in Healthcare Market, by Deployment, 2026 - 20359.7.4.1 The Middle-East and Africa Cyber Security in Healthcare Market, by Deployment, 2026 - 2035 (USD Billion)9.7.5 The Middle-East and Africa Cyber Security in Healthcare Market, by End-User, 2026 - 20359.7.5.1 The Middle-East and Africa Cyber Security in Healthcare Market, by End-User, 2026 - 2035 (USD Billion)Chapter 10. Company Profiles

10.1 IBM10.1.1 Overview10.1.2 Financials10.1.3 Product Portfolio10.1.4 Business Strategy10.1.5 Recent Developments10.2 Palo Alto Networks10.2.1 Overview10.2.2 Financials10.2.3 Product Portfolio10.2.4 Business Strategy10.2.5 Recent Developments10.3 Fortinet10.3.1 Overview10.3.2 Financials10.3.3 Product Portfolio10.3.4 Business Strategy10.3.5 Recent Developments10.4 Cisco10.4.1 Overview10.4.2 Financials10.4.3 Product Portfolio10.4.4 Business Strategy10.4.5 Recent Developments10.5 Trend Micro10.5.1 Overview10.5.2 Financials10.5.3 Product Portfolio10.5.4 Business Strategy10.5.5 Recent Developments10.6 Lockheed Martin Corporation10.6.1 Overview10.6.2 Financials10.6.3 Product Portfolio10.6.4 Business Strategy10.6.5 Recent Developments10.7 Check Point Software Technologies Ltd.10.7.1 Overview10.7.2 Financials10.7.3 Product Portfolio10.7.4 Business Strategy10.7.5 Recent Developments10.8 CyberArk Software Ltd.10.8.1 Overview10.8.2 Financials10.8.3 Product Portfolio10.8.4 Business Strategy10.8.5 Recent Developments10.9 F5 Inc.10.9.1 Overview10.9.2 Financials10.9.3 Product Portfolio10.9.4 Business Strategy10.9.5 Recent Developments10.10 FireEye Inc.10.10.1 Overview10.10.2 Financials10.10.3 Product Portfolio10.10.4 Business Strategy10.10.5 Recent Developments

Frequently Asked Questions

Cyber security in healthcare refers to the practices, technologies, and processes designed to protect electronic health records, medical devices, and healthcare infrastructure from cyber threats, unauthorized access, and data breaches, ensuring patient privacy and operational integrity.

Key factors include the rising frequency of cyberattacks, rapid digitalization of healthcare systems, stringent regulatory requirements like HIPAA and GDPR, adoption of telehealth and cloud-based solutions, and the proliferation of connected medical devices, all driving demand for advanced security measures.

The market is expected to grow from an estimated USD 8.72 billion in 2025 to USD 16.18 billion by 2035.

The CAGR is projected to be 6.34% during 2026-2035.

North America will contribute notably, holding a 42.1% share, due to advanced infrastructure and regulatory frameworks.

Major players include IBM, Palo Alto Networks, Fortinet, Cisco, Trend Micro, Lockheed Martin Corporation, Check Point Software Technologies Ltd., CyberArk Software Ltd., F5, Inc., and FireEye Inc.

The report provides comprehensive analysis including market size, trends, segmentation, drivers, restraints, opportunities, challenges, regional insights, key players, recent developments, and forecasts, along with value-added data like PESTLE and Porter's analyses.

The value chain includes research and development of security technologies, manufacturing and distribution of solutions, implementation and integration in healthcare systems, ongoing maintenance and managed services, and end-user training and compliance monitoring.

Trends are shifting towards AI-driven threat detection, cloud integration, zero-trust models, and managed services, with preferences favoring scalable, compliant solutions that minimize disruptions and address remote care needs.

Regulatory factors like HIPAA, GDPR, and national digital health policies enforce data protection standards, while environmental factors include the global rise in cyber threats and the need for sustainable, energy-efficient security infrastructure in data centers.