Green Hydrogen Market Size, Share and Trends 2026 to 2035

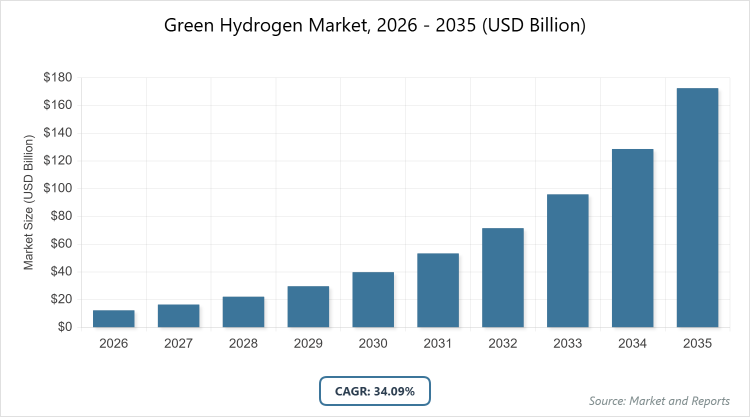

According to MarketnReports, the global Green Hydrogen Market size was estimated at USD 12.31 Billion in 2025 and is expected to reach USD 231.32 Billion by 2035, growing at a CAGR of 34.09% from 2026 to 2035. Green Hydrogen Market is driven by global decarbonization goals and increasing investments in renewable energy infrastructure.

What is the Industry Overview of the Green Hydrogen Market?

The Green Hydrogen Market involves the production, storage, and utilization of hydrogen generated through electrolysis powered by renewable energy sources, such as wind and solar, resulting in a zero-carbon emission fuel that supports the transition to sustainable energy systems. This market addresses the need for clean alternatives in hard-to-decarbonize sectors like heavy industry, transportation, and power generation, by providing a versatile energy carrier that can be used for fuel cells, chemical feedstocks, or grid balancing.

It encompasses technologies for efficient production, infrastructure for distribution, and applications that align with net-zero ambitions, driven by advancements in electrolyzer efficiency and integration with intermittent renewables. The market definition includes all processes and equipment related to green hydrogen, excluding grey or blue hydrogen variants, focusing on environmental sustainability and scalability to meet global climate targets.

What are the Key Insights into the Green Hydrogen Market?

- The global Green Hydrogen Market size was estimated at USD 12.31 Billion in 2025 and is expected to reach USD 231.32 Billion by 2035.

- Growing at a CAGR of 34.09% from 2026 to 2035.

- The Green Hydrogen Market is driven by global decarbonization goals, government incentives for renewable energy, and advancements in electrolysis technologies enabling cost reductions.

- Dominated subsegment in Technology: Alkaline Electrolyzer with 66% share, because of its mature technology, lower capital costs, and suitability for large-scale production integrated with renewables.

- Dominated subsegment in Application: Transport with 35% share, because of rising adoption in fuel cell vehicles and heavy-duty transport to reduce emissions in mobility sectors.

- Dominated subsegment in End-Use: Industrial with 45% share, because of demand for clean feedstocks in ammonia, steel, and refining to decarbonize high-emission industries.

- Dominated region: Asia Pacific with 47% share, because of massive investments in China and India for renewable-powered production and national hydrogen strategies.

What are the Market Dynamics of the Green Hydrogen Market?

Growth Drivers

The growth drivers for the Green Hydrogen Market include escalating global commitments to net-zero emissions, with governments implementing policies like subsidies and tax incentives to promote renewable-based hydrogen production as a cornerstone of energy transitions. Advancements in electrolyzer technologies, particularly in efficiency and scalability, are reducing production costs, making green hydrogen competitive with fossil fuel alternatives in sectors like transportation and industry. Integration with abundant renewable energy sources, such as solar and wind farms, enables low-cost electricity inputs, further driving economic viability. Increasing corporate sustainability goals and international agreements, such as the Paris Accord, are fostering investments in infrastructure, while the versatility of hydrogen as a storage medium for intermittent renewables supports grid stability and energy security.

Restraints

Restraints in the Green Hydrogen Market arise from high upfront capital costs for electrolysis plants and infrastructure, which require significant investments in renewable energy capacity and storage systems, limiting adoption in regions with financial constraints. Limited scalability due to reliance on variable renewable sources can lead to inconsistent production, necessitating advanced energy management solutions that add complexity and expense. Regulatory uncertainties and varying standards across countries hinder cross-border trade and project financing. Moreover, competition from cheaper grey hydrogen persists in the short term, delaying the shift until green variants achieve cost parity through technological breakthroughs.

Opportunities

Opportunities in the Green Hydrogen Market are emerging through international collaborations and funding initiatives, such as the EU’s Hydrogen Strategy and bilateral agreements for hydrogen trade corridors, enabling export-oriented production in renewable-rich regions. Innovations in hybrid systems combining electrolysis with offshore wind or solar PV open new avenues for cost-effective, large-scale output. Expansion into emerging applications like synthetic fuels for aviation and maritime transport presents high-growth potential, supported by R&D in efficient conversion processes. Government-backed pilot projects and public-private partnerships are accelerating commercialization, while the integration of AI for optimized production and distribution creates efficiencies that attract further investments.

Challenges

Challenges in the Green Hydrogen Market include achieving cost reductions to compete with conventional fuels, as current electrolysis expenses remain high due to platinum and iridium dependencies in catalysts, requiring material innovations for affordability. Infrastructure gaps for storage, transportation, and refueling stations pose logistical hurdles, especially in remote or densely populated areas. Water scarcity in some renewable hubs limits electrolysis feasibility, demanding sustainable sourcing solutions. Additionally, skill shortages in specialized engineering and safety protocols for hydrogen handling complicate workforce development, while fluctuating policy support can disrupt long-term planning and investor confidence.

Green Hydrogen Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Green Hydrogen Market |

| Market Size 2025 | USD 12.31 Billion |

| Market Forecast 2035 | USD 231.32 Billion |

| Growth Rate | CAGR of 34.09% |

| Report Pages | 220 |

| Key Companies Covered |

Air Liquide, Linde Plc, Siemens Energy, Plug Power Inc., Nel ASA, ITM Power, Cummins Inc., Ballard Power Systems, Hydrogenics (Cummins), Toshiba Energy Systems, and Others |

| Segments Covered | By Technology, By Application, By End-Use, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Market Segmentation Structured in the Green Hydrogen Market?

The Green Hydrogen Market is segmented by technology, application, end-use, and region.

Based on Technology Segment, The most dominant segment is Alkaline Electrolyzer, which holds the largest market share due to its established reliability, lower operational costs, and ability to handle large-scale operations with fluctuating renewable inputs; this dominance drives the market by enabling affordable mass production that supports widespread adoption in industrial decarbonization and accelerates global capacity expansions. The second most dominant segment is Proton Exchange Membrane Electrolyzer, favored for its high efficiency and rapid response to variable power; it contributes to market growth by facilitating integration with intermittent renewables, enhancing flexibility in transport applications, and attracting investments in advanced tech hubs.

Based on Application Segment, The most dominant segment is Transport, leading due to government mandates for zero-emission vehicles and the scalability of hydrogen fuel cells in heavy-duty sectors like trucks and buses; this drives market expansion by reducing reliance on batteries for long-range needs, promoting infrastructure buildouts, and generating demand for international supply chains. The second most dominant segment is Power Generation, driven by its role in energy storage and grid balancing; it propels growth by enabling renewable integration, supporting peak demand management, and fostering hybrid power plants that enhance energy security.

Based on End-Use Segment, The most dominant segment is Industrial, commanding the majority share owing to the need for clean alternatives in emission-intensive processes like steel and ammonia production; this dominance fuels market growth by aligning with corporate ESG goals, leading to large-scale projects that lower costs through economies of scale. The second most dominant segment is Mobility, driven by fuel cell advancements in automotive and aviation; it aids expansion by addressing range anxiety, encouraging fleet transitions, and stimulating R&D in efficient refueling systems.

What are the Recent Developments in the Green Hydrogen Market?

- In November 2025, Air Liquide announced a partnership with Siemens Energy to develop a gigawatt-scale electrolyzer plant in Europe, aiming to produce 200,000 tons of green hydrogen annually by 2028 for industrial applications.

- In October 2025, Linde expanded its green hydrogen production facility in the U.S. with a new 100 MW electrolyzer, supported by federal incentives, to supply the mobility sector.

- In September 2025, Plug Power acquired a startup specializing in solid oxide electrolysis, enhancing its portfolio for high-temperature applications in power generation.

How Does Regional Analysis Impact the Green Hydrogen Market?

- Asia Pacific to dominate the global market.

Asia Pacific, valued at USD 5.84 billion in 2025 and projected to reach USD 112.79 billion by 2035 at a CAGR of 34.46%, dominates with over 47% revenue share due to aggressive national strategies in China, where subsidies exceed billions for electrolyzer manufacturing and renewable integration, alongside India’s National Hydrogen Mission targeting 5 million tons by 2030; Japan and South Korea contribute through tech exports and fuel cell leadership, with China as the dominating country via its dominance in solar PV supply chains and state-owned enterprises scaling production to meet domestic and export demands.

Europe exhibits strong growth, fueled by the EU’s Hydrogen Strategy allocating over EUR 40 billion for 40 GW of electrolyzers by 2030, emphasizing cross-border pipelines and industrial clusters; collaborations like the Hydrogen Valley projects enhance innovation, with Germany as the dominating country through its H2Global initiative and automotive giants like BMW advancing mobility applications.

North America is advancing, supported by the U.S. Inflation Reduction Act providing USD 3 per kg tax credits, driving projects in California and Texas; focus on blue-to-green transitions aids scalability, with the United States as the dominating country via DOE-funded hubs and partnerships with Canada for cross-border trade.

Latin America shows potential, driven by abundant renewables in Chile and Brazil for export-oriented production; international investments fund pilot plants, with Chile as the dominating country through its Green Hydrogen Roadmap aiming for lowest-cost production globally.

The Middle East and Africa are emerging, leveraging solar resources for exports via projects in Saudi Arabia’s NEOM; diversification from oil supports growth, with Saudi Arabia as the dominating country through Vision 2030 investments in 4 GW capacity by 2030.

Who are the Key Market Players in the Green Hydrogen Market?

Air Liquide. Air Liquide focuses on large-scale electrolysis projects, with strategies including joint ventures for renewable integration and investments in pipeline infrastructure to supply industrial clients.

Linde Plc. Linde Plc emphasizes end-to-end solutions, strategizing through acquisitions of electrolyzer tech and partnerships with utilities for grid-connected production.

Siemens Energy. Siemens Energy develops PEM electrolyzers, employing strategies like digital optimization for efficiency and collaborations for gigafactories in Europe.

Plug Power Inc. Plug Power Inc. targets mobility, with strategies involving fuel cell stacks and vertical integration for cost reductions.

Nel ASA. Nel ASA specializes in alkaline systems, strategizing via R&D for megawatt-scale units and expansions in North America.

ITM Power. ITM Power focuses on modular PEM, with strategies including UK government-funded pilots for transport.

Cummins Inc. Cummins Inc. integrates hydrogen engines, employing strategies like acquisitions for electrolysis and focus on heavy-duty vehicles.

Ballard Power Systems. Ballard Power Systems provides fuel cells, strategizing through OEM partnerships for buses and trucks.

Hydrogenics (Cummins). Hydrogenics advances water electrolysis, with strategies centered on industrial decarbonization.

Toshiba Energy Systems. Toshiba Energy Systems offers solid oxide tech, strategizing via Asian market expansions for power applications.

What are the Market Trends in the Green Hydrogen Market?

- Surging government subsidies and policies for net-zero targets accelerating electrolysis deployments.

- Advancements in electrolyzer efficiency reducing costs below USD 2 per kg by 2030.

- Growing international hydrogen trade corridors, especially from renewable-rich regions to Europe and Japan.

- Integration with AI for predictive maintenance and optimized renewable energy utilization.

- Expansion in synthetic fuels for aviation and shipping to decarbonize long-haul transport.

What Market Segments and their Subsegments are Covered in the Green Hydrogen Report?

By Technology

-

- Alkaline Electrolyzer

- Proton Exchange Membrane Electrolyzer

- Solid Oxide Electrolyzer

- Anion Exchange Membrane

- Microbial Electrolysis

- Photoelectrochemical

- Thermochemical

- Biophotolysis

- Dark Fermentation

- High-Temperature Electrolysis

- Others

By Application

-

- Power Generation

- Transport

- Heating

- Chemical Feedstock

- Ammonia Production

- Methanol Production

- Steel Production

- Cement Production

- Glass Production

- Petroleum Refining

- Others

By End-Use

-

- Food & Beverages

- Medical

- Chemical

- Petrochemicals

- Electronics

- Glass

- Mining

- Mobility

- Utilities

- Industrial

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Green Hydrogen Market - Industry Analysis

Chapter 4. Global Green Hydrogen Market- Competitive Landscape

Chapter 5. Global Green Hydrogen Market - Technology Analysis

Chapter 6. Global Green Hydrogen Market - Application Analysis

Chapter 7. Global Green Hydrogen Market - End-Use Analysis

Chapter 8. Green Hydrogen Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Electrical enclosures are protective housings for electrical components, but in the context of green hydrogen, they safeguard control systems and power electronics in electrolysis plants from environmental hazards.

Key factors include policy support for decarbonization, declining renewable energy costs, electrolyzer innovations, and demand from industrial and transport sectors.

The market is projected to grow from USD 12.31 billion in 2025 to USD 231.32 billion by 2035.

The CAGR is expected to be 34.09% during 2026-2035.

Asia Pacific will contribute notably, holding 47% share, driven by investments in China.

Major players include Air Liquide, Linde Plc, Siemens Energy, Plug Power Inc., Nel ASA, and ITM Power, among others.

The report provides comprehensive analysis including market size, forecasts, segmentation, dynamics, regional insights, key players, trends, and strategic recommendations.

The value chain includes raw material sourcing (metals, seals), manufacturing, assembly with electrical components, distribution, installation in hydrogen systems, and maintenance.

Trends emphasize cost-effective production and sustainable applications, with preferences shifting towards green alternatives for emissions reduction.

Regulatory factors include subsidies and emission targets, while environmental factors involve renewable integration to minimize carbon footprints.