Rodenticides Market Size, Share and Trends 2026 to 2035

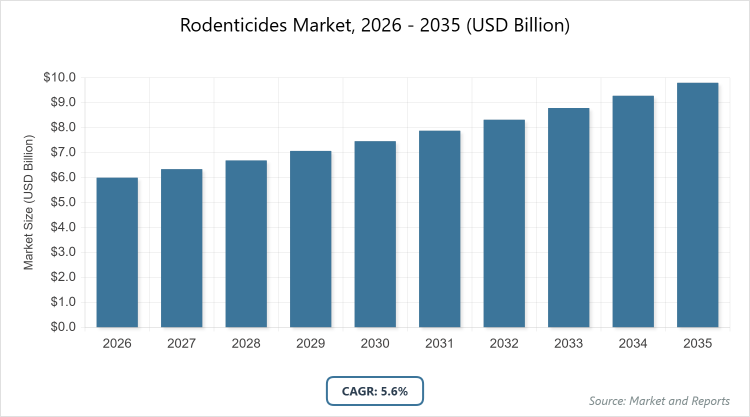

According to MarketnReports, the global Rodenticides market size was estimated at USD 6.0 billion in 2025 and is expected to reach USD 10.3 billion by 2035, growing at a CAGR of 5.6% from 2026 to 2035. Rodenticides Market is driven by increasing rodent populations and rising demand for effective pest control in urban and agricultural settings.

What are the Key Insights of Rodenticides Market?

- Market size in 2025: USD 6.0 Billion, Forecast 2035: USD 10.3 Billion

- CAGR: 5.6% from 2026 to 2035

- Market is driven by surging rodent populations due to urbanization, climate change, and increasing demand for pest management in agriculture and public health sectors

- Dominated subsegment in type: Anticoagulant rodenticides with 66% share, due to their high efficacy against resistant rodent strains and lower required dosage for effective control

- Dominated subsegment in form: Blocks with 45% share, as they offer tamper-resistant, weatherproof application suitable for both indoor and outdoor use, reducing secondary poisoning risks

- Dominated subsegment in application: Agricultural fields with 40% share, owing to the need to protect crops from rodent damage and ensure food security in large-scale farming operations

- Dominated subsegment in end-user: Pest control companies with 38% share, driven by professional services handling complex infestations in commercial and urban environments

- Dominated region: North America with 34% share, attributed to high urbanization rates, stringent public health regulations, and widespread residential and commercial construction leading to increased rodent infestations

What is the Rodenticides Industry Overview?

The rodenticides market encompasses the production, distribution, and application of chemical or biological agents designed to control and eliminate rodent populations, such as rats and mice, which pose significant threats to public health, agriculture, and infrastructure. This market includes a variety of products ranging from anticoagulant-based formulations that disrupt blood clotting in rodents to non-anticoagulant options that target neurological or other physiological systems for rapid lethality. The market definition refers to all substances and solutions specifically formulated for rodent management, excluding general pesticides or traps, and it serves sectors like farming, urban pest control, and food storage to prevent disease transmission, crop damage, and property destruction caused by rodents.

What are the Market Dynamics in Rodenticides Industry?

Growth Drivers

The primary growth drivers in the rodenticides market include rapid urbanization and climate change, which have led to a surge in rodent populations in densely populated areas and extended breeding seasons. This escalation heightens the risk of disease transmission, such as leptospirosis and hantavirus, prompting greater demand for effective rodent control solutions. Additionally, the expansion of agricultural activities globally necessitates robust pest management to safeguard crops and stored grains from substantial economic losses, estimated in billions annually. Innovations in eco-friendly and low-toxicity formulations further fuel market growth by addressing regulatory pressures and consumer preferences for safer alternatives, enabling manufacturers to tap into new segments like residential and organic farming.

Restraints

Key restraints impacting the rodenticides market revolve around stringent environmental regulations and bans on highly toxic second-generation anticoagulants in regions like Europe and North America, which limit product availability and increase compliance costs for manufacturers. Rodent resistance to traditional chemical rodenticides has also emerged as a significant barrier, reducing the effectiveness of established products and requiring ongoing research investments. Moreover, concerns over secondary poisoning of non-target wildlife, including birds of prey and domestic animals, have led to public backlash and restricted use in sensitive ecosystems, constraining market expansion in environmentally conscious markets.

Opportunities

Opportunities in the rodenticides market are abundant with the rising adoption of bio-based and natural rodenticides, driven by global shifts toward sustainable pest control practices. Emerging economies in Asia-Pacific and Latin America present untapped potential due to increasing agricultural output and urban development, where rodent infestations are intensifying without adequate infrastructure. Technological advancements, such as IoT-enabled smart bait stations and fertility control agents, offer avenues for differentiation and premium pricing, allowing companies to capture market share in high-growth sectors like integrated pest management services.

Challenges

Challenges in the rodenticides market include the development of rodent resistance to multiple active ingredients, which complicates product efficacy and necessitates frequent reformulations, escalating R&D expenses. Balancing potency with safety remains a hurdle, as efforts to minimize environmental impact often result in less effective alternatives that fail to meet user expectations in severe infestation scenarios. Supply chain disruptions, particularly for raw materials like anticoagulants, and varying regulatory frameworks across regions further complicate global operations and market penetration for key players.

Rodenticides Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Rodenticides Market |

| Market Size 2025 | USD 6.0 Billion |

| Market Forecast 2035 | USD 10.3 Billion |

| Growth Rate | CAGR of 5.6% |

| Report Pages | 260 |

| Key Companies Covered |

BASF SE, Bayer AG, Syngenta AG, Rentokil Initial plc, Neogen Corporation, Bell Laboratories, Liphatech Inc., PelGar International, Ecolab, UPL Limited, and Others |

| Segments Covered | By Type, By Form, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Rodenticides?

The Rodenticides market is segmented by type, form, application, end-user, and region.

Based on Type Segment. The anticoagulant rodenticides segment is the most dominant, holding approximately 66% market share, primarily because of its proven effectiveness in causing internal bleeding in rodents with minimal bait consumption, making it ideal for large-scale control; this dominance drives the market by addressing resistance issues in rodent populations and ensuring reliable outcomes in agriculture and urban settings. The non-anticoagulant rodenticides segment is the second most dominant, with around 34% share, owing to its faster-acting mechanism that targets the nervous system for quick lethality, which is preferred in scenarios requiring immediate results; it contributes to market growth by offering alternatives in regulated environments where anticoagulants are restricted, thus expanding application versatility.

Based on Form Segment. The blocks segment is the most dominant, capturing about 45% market share, due to its durability, ease of placement in bait stations, and resistance to environmental degradation, which ensures prolonged efficacy in outdoor and industrial applications; this leads market growth by minimizing waste and enhancing safety against non-target exposure. The pellets segment is the second most dominant, with roughly 30% share, as it allows for precise dosing and widespread scattering in infested areas like fields; it supports overall market expansion by providing cost-effective solutions for high-volume agricultural use, improving rodent control efficiency.

Based on Application Segment. The agricultural fields segment is the most dominant, accounting for around 40% market share, driven by the critical need to protect crops from rodent damage that can result in significant yield losses; its dominance propels the market forward by integrating with global food production demands and sustainable farming practices. The urban centers segment is the second most dominant, with about 25% share, due to rising rodent issues in densely populated cities from waste accumulation; it aids market growth by aligning with public health initiatives and urban infrastructure development.

Based on End-User Segment. The pest control companies segment is the most dominant, holding approximately 38% market share, as these professionals handle complex, large-scale infestations requiring specialized expertise and equipment; this drives the market by fostering innovation in service-based solutions and compliance with regulations. The agriculture segment is the second most dominant, with around 30% share, owing to farmers’ direct reliance on rodenticides for crop protection; it contributes to market advancement by linking with agricultural expansion and food security efforts.

What are the Recent Developments in Rodenticides Market?

- In October 2024, BASF SE relaunched its Neosorexa rodenticide brand with flocoumafen as the new active ingredient, aiming to enhance effectiveness against various rodent species while ensuring regulatory compliance and improving rodent control solutions.

- In July 2023, Syngenta launched Talon Soft XT, an innovative rodenticide based on their brodifacoum formula, designed to combat resistance issues and meet regulatory requirements with exceptional efficacy.

- In May 2023, World Pest Control partnered with Rentokil North America to enhance pest control services, leveraging Rentokil’s extensive network and expertise to expand market reach and strengthen offerings.

- In April 2023, Target Specialty Products introduced Strike MAX CITO Paste, a fast-acting commercial rodenticide paste featuring brodifacoum, suitable for indoor and outdoor use with user-friendly application.

- In February 2024, Syngenta introduced SecureChoice, a flexible rodent management solution for various building environments, focusing on adaptability and effectiveness in diverse settings.

What is the Regional Analysis of Rodenticides Market?

North America to dominate the global market.

North America holds the largest share in the rodenticides market, primarily driven by high urbanization and rodent infestations in residential and commercial areas, with the United States as the dominating country due to its extensive agricultural sector, strict public health standards, and widespread adoption of professional pest control services that ensure effective management of diseases like hantavirus.

Europe represents a significant portion of the market, influenced by regulatory emphasis on eco-friendly products and integrated pest management, with Germany as the dominating country owing to its advanced chemical industry, robust farming practices, and proactive measures against rodent-borne threats in urban centers like Berlin.

Asia-Pacific is the fastest-growing region, fueled by rapid urbanization, agricultural expansion, and climate-induced rodent surges, with China as the dominating country because of its massive population density, extensive crop production in regions like the Yangtze River basin, and increasing investments in pest control to protect food supplies and public health.

Latin America shows steady growth, supported by agricultural demands and tropical climates favoring rodent proliferation, with Brazil as the dominating country due to its vast farmland in the Amazon and Cerrado regions, where rodenticides are essential for safeguarding soybean and sugarcane crops from economic losses.

The Middle East and Africa exhibit emerging potential, driven by urban development and food storage needs in arid environments, with South Africa as the dominating country attributed to its commercial agriculture in areas like the Western Cape and efforts to control rodent vectors for diseases in growing cities like Johannesburg.

What are the Key Market Players and Strategies in Rodenticides?

- BASF SE. As a leading player, BASF SE focuses on innovation through product relaunches like Neosorexa with advanced active ingredients and investments in sustainable formulations to comply with global regulations, while expanding its market presence via strategic partnerships in agriculture and urban pest control.

- Bayer AG. Bayer AG employs strategies centered on research and development of eco-friendly rodenticides, including acquisitions to bolster its portfolio, and emphasizes integrated pest management solutions to address resistance issues, targeting growth in emerging markets like Asia-Pacific.

- Syngenta AG. Syngenta AG prioritizes product launches such as Talon Soft XT and SecureChoice, alongside acquisitions of bio-based technologies, to enhance efficacy and safety, with a focus on collaborating with governments for public health initiatives and expanding in high-demand agricultural sectors.

- Rentokil Initial plc. Rentokil Initial plc leverages mergers and acquisitions, such as with Vector Disease Acquisition, to strengthen its service network, while investing in digital monitoring tools like IoT bait stations to offer comprehensive, tech-driven rodent control services globally.

- Neogen Corporation. Neogen Corporation adopts strategies involving the development of non-toxic alternatives and diagnostic tools for rodent resistance, with emphasis on R&D collaborations and market expansion in North America and Europe to meet regulatory and consumer demands for safer products.

- Bell Laboratories. Bell Laboratories focuses on innovative bait formulations like Contrac California Bromethalin, prioritizing tamper-resistant designs and environmental safety, while pursuing global distribution partnerships to capture share in residential and commercial applications.

- Liphatech Inc. Liphatech Inc. emphasizes low-toxicity anticoagulant innovations and custom solutions for agriculture, with strategies including targeted marketing in regulated markets and investments in research to combat rodent resistance.

- PelGar International. PelGar International pursues growth through export expansions and product diversification into natural rodenticides, with a focus on sustainability certifications to appeal to eco-conscious consumers in Europe and beyond.

- Ecolab. Ecolab integrates rodenticides into broader hygiene services, using data analytics for predictive pest control, and expands via acquisitions to dominate commercial sectors like food processing.

- UPL Limited. UPL Limited concentrates on affordable, high-efficacy products for emerging markets, with strategies involving local manufacturing and farmer education programs to drive adoption in agriculture-heavy regions like India.

What are the Market Trends in Rodenticides?

- Shift toward eco-friendly and bio-based rodenticides using natural ingredients to reduce environmental impact and meet regulatory standards

- Adoption of digital technologies like IoT-enabled smart bait stations for real-time monitoring and efficient pest management

- Increasing focus on non-anticoagulant formulations to address rodent resistance and minimize secondary poisoning risks

- Growth in integrated pest management (IPM) practices combining rodenticides with traps and sanitation for sustainable control

- Rising demand for ready-to-use bait products in residential sectors for convenience and safety

- Expansion of fertility control agents as humane alternatives to traditional lethal methods

- Emphasis on regulatory compliance with restrictions on second-generation anticoagulants driving innovation in low-toxicity options

What Market Segments and their Subsegments are Covered in the Rodenticides Report?

- BY Type

- Anticoagulant Rodenticides

- Non-Anticoagulant Rodenticides

- Others

- By Form

- Pellets

- Blocks

- Powders

- Sprays

- Others

- By Application

- Agricultural Fields

- Warehouses

- Urban Centers

- Residential

- Commercial

- Others

- By End-User

- Agriculture

- Pest Control Companies

- Households

- Others

- By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Rodenticides are chemical or biological substances formulated to kill or control rodent populations, such as rats and mice, by disrupting their physiological functions, commonly used in agriculture, urban areas, and food storage to prevent damage and disease spread.

Key factors include urbanization-driven rodent infestations, climate change extending breeding seasons, rising agricultural demands for crop protection, regulatory shifts toward safer products, and technological advancements in eco-friendly formulations.

The market is projected to grow from approximately USD 6.3 billion in 2026 to USD 10.3 billion by 2035.

The CAGR is expected to be 5.6% during the forecast period.

North America will contribute notably, holding around 34% share, due to high urbanization, strict health regulations, and extensive pest control adoption.

Major players include BASF SE, Bayer AG, Syngenta AG, Rentokil Initial plc, Neogen Corporation, Bell Laboratories, Liphatech Inc., PelGar International, Ecolab, and UPL Limited.

The report provides comprehensive analysis including market size, trends, segmentation, regional insights, key players, growth drivers, restraints, opportunities, and forecasts from 2026 to 2035.

The value chain includes raw material sourcing (active ingredients like anticoagulants), manufacturing and formulation, distribution through suppliers and retailers, application by end-users such as pest control services, and end-of-life disposal or recycling.

Trends are shifting toward sustainable, non-toxic bio-based products, with consumers preferring eco-friendly options that minimize wildlife harm, alongside integrated digital monitoring for efficient, humane control.

Regulations restricting toxic anticoagulants in regions like Europe and the US, along with environmental concerns over secondary poisoning, are pushing innovation in low-toxicity and biodegradable alternatives, impacting growth by increasing compliance costs but opening opportunities for green products.