EPC Market Size, Share and Trends 2026 to 2035

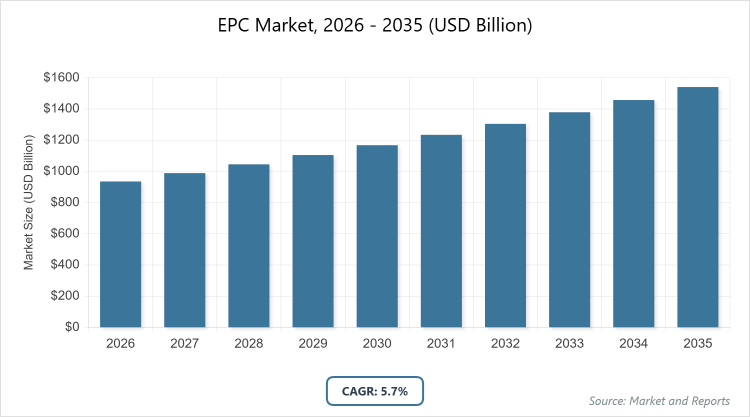

According to MarketnReports, the global EPC market size was estimated at USD 935.4 billion in 2025 and is expected to reach USD 1628 billion by 2035, growing at a CAGR of 5.7% from 2026 to 2035. Increasing infrastructure investments and energy transition initiatives.

What are the Key Insights into EPC Market?

- The global EPC market size was valued at USD 935.4 billion in 2025 and is projected to reach USD 1628 billion by 2035.

- The market is expected to grow at a CAGR of 5.7% during the forecast period from 2026 to 2035.

- The market is driven by rising investments in infrastructure, energy transition projects, and technological advancements in project management.

- In the contract type segment, the EPC subsegment dominated with a 70% share, due to its comprehensive turnkey approach that reduces client oversight and ensures fixed costs, making it ideal for large-scale projects.

- In the sector segment, the oil & gas subsegment held the largest share at around 40%, driven by ongoing exploration and upstream activities requiring specialized engineering expertise.

- In the end-user segment, the government subsegment accounted for 55% of the market, primarily because of public infrastructure initiatives and regulatory support for energy projects.

- Asia Pacific dominated the regional market with a 45% share, attributed to rapid urbanization, massive infrastructure spending, and energy demand in countries like China and India.

What is the EPC Market?

Industry Overview

The EPC market, or Engineering, Procurement, and Construction market, encompasses integrated services where firms handle the design, material sourcing, and building of large-scale projects, primarily in energy, infrastructure, and industrial sectors, ensuring turnkey solutions that minimize client risks and optimize timelines. Market definition includes contracts for comprehensive project delivery, from feasibility studies to commissioning, often under fixed-price or lump-sum agreements, catering to governments and private entities seeking efficient execution in complex environments like oil & gas fields, power plants, and transportation networks, driven by global urbanization and sustainability goals.

What are the Market Dynamics of EPC Market?

Growth Drivers

Growth drivers in the EPC market are fueled by surging global infrastructure investments, particularly in emerging economies, where governments prioritize energy, transportation, and urban development projects to support economic expansion and sustainability goals. The energy transition toward renewables, including solar and wind farms, demands specialized EPC services for efficient grid integration and storage solutions. Technological advancements like digital twins, AI-driven project management, and modular construction reduce timelines and costs, enhancing appeal for complex projects, while public-private partnerships (PPPs) provide funding stability, accelerating market adoption across sectors.

Restraints

Restraints include volatile commodity prices and geopolitical tensions disrupting supply chains, leading to cost overruns and project delays in resource-dependent sectors like oil & gas. Stringent environmental regulations increase compliance burdens, inflating expenses for permits and sustainable practices. Talent shortages in skilled engineering and procurement roles hinder execution, while economic downturns reduce capital expenditures, limiting new contracts in cyclical industries.

Opportunities

Opportunities emerge from the global push for net-zero emissions, where EPC firms can capitalize on renewable energy projects like offshore wind and hydrogen facilities through specialized expertise. Digitalization trends, including BIM and IoT for predictive maintenance, offer avenues for service differentiation. Expansion in developing regions via Belt and Road initiatives provides access to untapped markets, while retrofitting aging infrastructure in mature economies creates demand for modernization services.

Challenges

Challenges involve managing project risks amid supply chain disruptions, requiring resilient sourcing strategies to mitigate delays and cost escalations. Evolving regulatory landscapes demand adaptive compliance, increasing administrative burdens. Competition from in-house capabilities reduces outsourcing, while cybersecurity threats to digital tools pose data risks, necessitating robust protections in interconnected project environments.

EPC Market: Report Scope

| Report Attributes | Report Details |

| Report Name | EPC Market |

| Market Size 2025 | USD 935.4 Billion |

| Market Forecast 2035 | USD 1628 Billion |

| Growth Rate | CAGR of 5.7% |

| Report Pages | 220 |

| Key Companies Covered |

Bechtel, Fluor Corporation, Kiewit Corporation, Jacobs Engineering Group, Saipem, TechnipFMC, Samsung Engineering, Larsen & Toubro, China State Construction Engineering, JGC Corporation, and Others |

| Segments Covered | By Contract Type (EPC, EPCM, and Others), By Sector (Oil & Gas, Power, Infrastructure, Chemicals, and Others), By End-User (Government, Private, Industrial, and Others), and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of EPC Market?

The EPC market is segmented by contract type, sector, end-user, and region.

Based on Contract Type Segment, the EPC subsegment is the most dominant, holding over 70% share, followed by EPCM as the second most dominant. EPC’s dominance results from its all-inclusive model that minimizes client involvement and guarantees fixed pricing, driving the market by enabling efficient delivery of large-scale projects, reducing uncertainties, and attracting investments in high-risk sectors like energy.

Based on Sector Segment, oil & gas leads with approximately 40% share, with power as the second dominant. Oil & gas’s leading position is due to ongoing global energy demands and exploration activities, propelling market growth through specialized contracts that support resource extraction and refining, fostering economic development in resource-rich regions.

Based on the End-User Segment, the government dominates with 55% share, followed by the private. Government’s supremacy stems from public funding for infrastructure and energy security, aiding market drive by initiating mega-projects that stimulate private participation and technological advancements.

What are the Recent Developments in EPC Market?

- In April 2025, Saipem S.p.A. secured offshore contracts worth USD 720 million in the Middle East and Guyana, utilizing advanced vessels for execution.

- In 2025, Hitachi Energy was awarded an EPC contract for a ±800 kV HVDC system to transmit 6 GW from renewable grids in India.

- In May 2023, Technip Energies NV formed a joint venture with Consolidated Contractors Company for an EPCC contract in Qatar’s North Field South Project.

What is the Regional Analysis of EPC Market?

- Asia Pacific to dominate the global market.

Asia Pacific leads the EPC market, holding approximately 45% share, driven by rapid industrialization, massive infrastructure projects, and energy demand. China dominates within the region, supported by Belt and Road initiatives, state-led investments, and renewable transitions, enabling large-scale executions in power and transportation.

North America exhibits strong growth at a CAGR of 4%, bolstered by energy independence efforts and infrastructure upgrades. The United States leads as the dominant country, fueled by shale gas developments, data center booms, and federal funding for grids, fostering innovation in digital EPC.

Europe shows steady expansion with a CAGR of 3.5%, focused on sustainability and EU green deals. Germany is the leading country, driven by Energiewende policies, offshore wind projects, and industrial retrofits requiring advanced EPC expertise.

Latin America demonstrates emerging potential, with growth from resource extraction and urbanization. Brazil dominates, thanks to oil field developments and infrastructure PPPs amid economic recovery.

The Middle East and Africa region holds about 15% share, with expansion through oil revenues and diversification. The United Arab Emirates leads, propelled by Vision 2030 projects, renewable integrations, and mega-infrastructure requiring global EPC partnerships.

Who are the Key Market Players in EPC Market?

- Bechtel focuses on integrated project delivery, emphasizing sustainability and digital tools for complex energy and infrastructure projects.

- Fluor Corporation specializes in modular construction, prioritizing safety and cost efficiency in oil & gas and power sectors.

- Kiewit Corporation offers end-to-end services, leveraging in-house capabilities for transportation and mining executions.

- Jacobs Engineering Group advances digital twins and AI, focusing on resilient infrastructure for government clients.

- Saipem excels in offshore EPC, collaborating on renewable transitions in energy hotspots.

- TechnipFMC integrates subsea technologies, emphasizing energy transition for sustainable oil & gas solutions.

- Samsung Engineering targets petrochemicals, utilizing advanced procurement for Asian expansions.

- Larsen & Toubro dominates infrastructure, focusing on Indian mega-projects with cost-effective models.

- China State Construction Engineering scales massive developments, prioritizing Belt and Road international ventures.

- JGC Corporation specializes in LNG, emphasizing Japanese precision for global energy contracts.

What are the Market Trends in EPC Market?

- Integration of AI and digital twins for predictive project management.

- Shift toward renewable energy EPC with focus on solar and wind integrations.

- Adoption of modular and prefabricated construction for faster timelines.

- Emphasis on sustainability and ESG compliance in contracts.

- Growth in data center and AI infrastructure projects.

- Rise of public-private partnerships for funding large-scale initiatives.

- Focus on cybersecurity in digital EPC platforms.

- Expansion of EPCM models for flexible client involvement.

What are the Market Segments and their Subsegments Covered in the EPC Report?

By Contract Type

- EPC

- EPCM

- Others

By Sector

- Oil & Gas

- Power

- Infrastructure

- Chemicals

- Others

By End-User

- Government

- Private

- Industrial

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global EPC Market - Industry Analysis

Chapter 4. Global EPC Market- Competitive Landscape

Chapter 5. Global EPC Market - Contract Type Analysis

Chapter 6. Global EPC Market - Sector Analysis

Chapter 7. Global EPC Market - End-User Analysis

Chapter 8. EPC Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

EPC refers to Engineering, Procurement, and Construction services providing integrated project delivery for infrastructure and energy developments.

Key factors include infrastructure investments, energy transitions, digital advancements, and sustainability mandates.

The market is projected to grow from USD 988.7 billion in 2026 to USD 1628 billion by 2035.

The CAGR is expected to be 5.7% from 2026 to 2035.

Asia Pacific will contribute notably, holding around 45% of the market value due to rapid development.

Major players include Bechtel, Fluor Corporation, Kiewit Corporation, Jacobs Engineering Group, Saipem, TechnipFMC, Samsung Engineering, Larsen & Toubro, China State Construction Engineering, and JGC Corporation.

The report provides comprehensive analysis including market size, trends, segmentation, regional insights, key players, growth drivers, restraints, opportunities, challenges, and forecasts from 2026 to 2035.

The value chain includes project planning, engineering design, procurement sourcing, construction execution, commissioning, and maintenance services.

Trends are moving toward digitalization and renewables, while preferences favor sustainable, cost-efficient project models.

Regulations on emissions and safety promote green EPC, while environmental sustainability drives renewable focus.