Breast Implants Market Size, Share and Trends 2026 to 2035

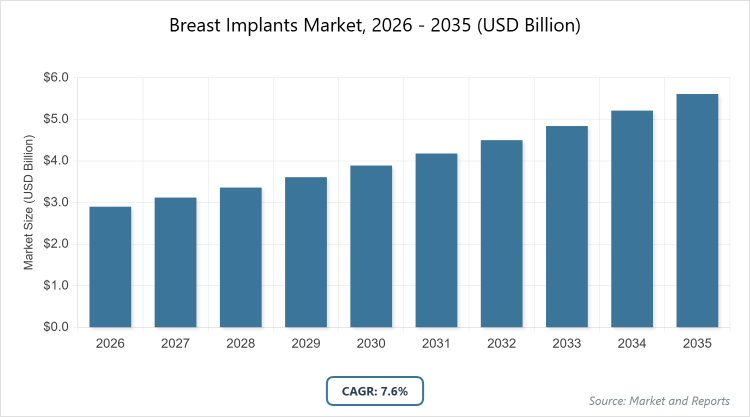

According to MarketnReports, the global Breast Implants market size was estimated at USD 2.9 billion in 2025 and is expected to reach USD 6.0 billion by 2035, growing at a CAGR of 7.6% from 2026 to 2035. Breast Implants Market is driven by increasing demand for cosmetic and reconstructive surgeries.

What are the Key Insights into the Breast Implants Market?

- The global breast implants market was valued at USD 2.9 billion in 2025 and is projected to reach USD 6.0 billion by 2035.

- The market is expected to grow at a CAGR of 7.6% during the forecast period from 2026 to 2035.

- The market is driven by rising demand for cosmetic enhancements, increasing breast cancer incidences requiring reconstruction, and technological advancements in implant materials.

- Silicone implants dominate the product segment with an 83.7% share due to their natural feel and durability, while saline implants hold the second position with better adjustability and lower cost; round implants lead the shape segment with an 80.4% share owing to their versatility and lower complication rates, with anatomical implants as the next prominent for providing a more natural teardrop contour.

- North America dominates the regional landscape with a 31.2% share, attributed to advanced healthcare infrastructure, high disposable incomes, and a large number of cosmetic procedures performed annually.

What is the Breast Implants Industry Overview?

The breast implants market encompasses the development, manufacturing, and distribution of medical devices designed to enhance or reconstruct the size, shape, and contour of breasts through surgical implantation. This market serves both aesthetic purposes, where individuals seek to improve body image and confidence, and medical needs, particularly for breast reconstruction following mastectomies due to cancer or other conditions. Breast implants are typically filled with silicone gel or saline solution and come in various shapes and textures to meet diverse patient preferences and surgical requirements. The industry is characterized by a focus on safety, innovation in materials to mimic natural tissue, and adherence to stringent regulatory standards to minimize risks such as rupture or capsular contracture. It intersects with the broader cosmetic and reconstructive surgery sectors, influenced by cultural perceptions of beauty, advancements in minimally invasive techniques, and growing acceptance of elective procedures worldwide.

What are the Market Dynamics in the Breast Implants Industry?

Growth Drivers

The primary growth drivers in the breast implants market include the surging popularity of cosmetic surgeries driven by social media influence and evolving beauty standards, which encourage more women to opt for augmentation procedures to achieve desired aesthetics. Additionally, the rising incidence of breast cancer globally has heightened the need for reconstructive surgeries, with implants playing a crucial role in restoring physical appearance and psychological well-being post-mastectomy. Technological innovations, such as highly cohesive silicone gels and textured surfaces that reduce risks like rotation or rippling, further propel market expansion by improving safety and patient outcomes. Favorable reimbursement policies in developed regions for reconstructive procedures, coupled with increasing disposable incomes in emerging economies, enable greater accessibility to these surgeries.

Restraints

Market growth faces restraints from potential health risks associated with implants, including complications like implant rupture, capsular contracture, and breast implant illness, which can lead to additional surgeries and deter potential patients. Stringent regulatory approvals and ongoing scrutiny from bodies like the FDA, often resulting in recalls or warnings, increase manufacturing costs and delay product launches. High procedure costs, particularly in regions without insurance coverage for cosmetic applications, limit adoption among price-sensitive demographics. Moreover, negative media coverage and public awareness campaigns about long-term safety concerns contribute to hesitation and slower market penetration in conservative societies.

Opportunities

Opportunities abound in emerging markets across Asia Pacific and Latin America, where rising middle-class populations and medical tourism hubs offer untapped potential for affordable, high-quality procedures. Innovations in bioresorbable materials and 3D-printed customized implants present avenues for differentiation, addressing patient demands for safer, more personalized options that minimize long-term risks. Partnerships between manufacturers and healthcare providers to expand training programs for surgeons can enhance procedure efficacy and boost adoption rates. Additionally, the growing focus on male breast implants for gender affirmation surgeries opens new niche segments, supported by increasing societal acceptance and specialized product developments.

Challenges

Challenges in the breast implants market stem from evolving regulatory landscapes that demand rigorous clinical trials and post-market surveillance, escalating operational costs for manufacturers and potentially slowing innovation cycles. Supply chain disruptions, particularly for raw materials like medical-grade silicone, can affect production timelines and pricing stability. Patient education remains a hurdle, as misconceptions about safety and efficacy persist, requiring robust marketing efforts to build trust. Intense competition among key players necessitates continuous R&D investment, while economic downturns may reduce elective spending on cosmetic procedures, impacting overall demand.

Breast Implants Market: Report Scope: Report Scope

| Report Attributes | Report Details |

| Report Name | Breast Implants Market |

| Market Size 2025 | USD 2.9 Billion |

| Market Forecast 2035 | USD 6.0 Billion |

| Growth Rate | CAGR of 7.6% |

| Report Pages | 250 |

| Key Companies Covered |

Allergan (AbbVie), Mentor Worldwide LLC (Johnson & Johnson), Sientra, Inc., GC Aesthetics, Establishment Labs Holdings Inc., POLYTECH Health & Aesthetics GmbH, and Others |

| Segments Covered | By Product (Silicone Implants, Saline Implants), By Shape (Round, Anatomical), By Application (Cosmetic Surgery, Reconstructive Surgery), By End-Use (Hospitals, Clinics, Ambulatory Surgical Centers, Others), and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Breast Implants Market Segmented?

The Breast Implants market is segmented by product, shape, application, end-use, and region.

Based on Product Segment, silicone implants emerge as the most dominant subsegment, commanding an 83.7% share, primarily because they offer a more natural texture and appearance compared to alternatives, driving market growth through higher patient satisfaction and surgeon preference for aesthetic outcomes. Saline implants rank as the second most dominant, valued for their safety in case of rupture—where the body harmlessly absorbs the saline—and adjustability during surgery, which helps in achieving symmetrical results and supports overall market expansion by catering to cost-conscious consumers seeking lower-risk options.

Based on Shape Segment, round implants dominate with an 80.4% share, favored for their ability to provide fullness and cleavage while being less prone to rotation issues, thereby accelerating market growth as they suit a wide range of body types and procedural goals. Anatomical implants are the second most dominant, excelling in delivering a teardrop shape that mimics natural breast contours, contributing to market drive by appealing to patients desiring subtle enhancements and reconstructive accuracy.

Based on Application Segment, cosmetic surgery leads as the dominant subsegment with approximately 65% share, propelled by cultural shifts toward body positivity and aesthetic ideals, fueling market growth through increased elective procedures worldwide. Reconstructive surgery follows as the second dominant, essential for post-cancer recovery and trauma cases, aiding market expansion by integrating with oncology care and improving quality of life for affected individuals.

Based on End-Use Segment, clinics represent the most dominant with around 55% share, as they offer specialized, outpatient-focused environments that enhance accessibility and reduce costs, driving market growth via efficient procedure volumes. Hospitals are the second most dominant, providing comprehensive care for complex cases like reconstructions, supporting market progression through advanced facilities and multidisciplinary teams.

What are the Recent Developments in the Breast Implants Market?

- In May 2025, Johnson & Johnson MedTech launched the MENTOR MemoryGel Enhance Breast Implants in the U.S., designed specifically for post-mastectomy reconstruction, emphasizing safety, comfort, and aesthetic appeal to address unmet needs in breast cancer care.

- In September 2024, Establishment Labs Holdings Inc. received FDA approval for its Motiva SmoothSilk Ergonomix and Motiva SmoothSilk Round breast implants, enabling their use in primary and revision augmentations, marking a significant advancement in providing differentiated technology backed by extensive research.

- In January 2022, Mentor Worldwide LLC obtained FDA approval for the MENTOR MemoryGel BOOST breast implant, targeted at women aged 22 and older for augmentation, enhancing options with improved projection and fullness.

- In December 2022, Sientra, Inc. secured regulatory approval from the United Arab Emirates Ministry of Health and Prevention to commercialize its silicone gel breast implants, expanding its global footprint in the Middle East.

How is the Regional Analysis of the Breast Implants Market Conducted?

North America to dominate the global market.

North America holds the largest share at 31.2%, driven by robust healthcare systems, high awareness of cosmetic options, and a surge in procedures, with the United States as the dominating country due to its concentration of skilled surgeons, favorable regulations, and cultural emphasis on aesthetics, contributing significantly to regional leadership through innovation and reimbursement for reconstructions.

Europe follows as a key region, benefiting from advanced medical technologies and increasing acceptance of aesthetic surgeries, with Germany dominating owing to its strong manufacturing base, high procedure volumes, and supportive policies that foster market stability and growth in reconstructive applications.

Asia Pacific is the fastest-growing region, fueled by rising disposable incomes, medical tourism, and shifting beauty norms, where South Korea leads as the dominating country with its world-renowned cosmetic surgery hubs, attracting international patients and driving expansion through affordable yet high-quality implant procedures.

Latin America shows promising growth, supported by cultural focus on body enhancement and improving infrastructure, with Brazil as the dominating country renowned for its high rate of cosmetic surgeries, bolstering the region through established clinics and cost-effective options that appeal to both local and foreign clients.

The Middle East and Africa region experiences gradual adoption, hindered by cultural factors but boosted by emerging markets, with the United Arab Emirates dominating through investments in luxury healthcare facilities and approvals for international products, enhancing access to advanced implants and supporting niche growth in aesthetics.

Who are the Key Market Players and Their Strategies in the Breast Implants Industry?

- Allergan (AbbVie) focuses on expanding its portfolio through acquisitions and innovative launches, such as the Natrelle line, emphasizing safety features and patient education campaigns to maintain market dominance and address regulatory concerns.

- Mentor Worldwide LLC (Johnson & Johnson) prioritizes R&D for advanced gel technologies and FDA approvals, like the MemoryGel series, while forming strategic partnerships with surgeons to enhance training and adoption rates globally.

- Sientra, Inc. employs market expansion strategies via international approvals and acquisitions, such as its high-strength cohesive implants, aiming to differentiate through quality and resilience in competitive landscapes.

- GC Aesthetics pursues product innovation with launches like PERLE implants, coupled with geographic diversification in emerging markets to capture growth in medical tourism and aesthetic demands.

- Establishment Labs Holdings Inc. leverages technology-driven approaches, including Motiva implants with RFID tracking, and focuses on clinical data to secure approvals and build trust in safety-oriented segments.

- POLYTECH Health & Aesthetics GmbH adopts customization and quality assurance strategies, collaborating on research for bio-compatible materials to strengthen its position in Europe and expand into Asia.

What are the Market Trends in the Breast Implants Industry?

- Increasing preference for highly cohesive silicone gels that offer natural movement and reduced rippling.

- Rise in minimally invasive insertion techniques to minimize scarring and recovery time.

- Growing demand for customizable implants using 3D imaging for personalized fits.

- Shift toward bioresorbable options to address long-term safety concerns.

- Expansion of male and non-binary applications in gender affirmation surgeries.

- Integration of digital tools like AI for pre-surgical simulations and outcome predictions.

- Emphasis on sustainable manufacturing practices with eco-friendly materials.

- Surge in reconstructive procedures linked to rising breast cancer awareness campaigns.

What Market Segments and Their Subsegments are Covered in the Breast Implants Report?

- By Product

- Silicone Implants

- Saline Implants

- By Shape

- Round

- Anatomical

- By Application

- Cosmetic Surgery

- Reconstructive Surgery

- By End-Use

- Hospitals

- Clinics

- Ambulatory Surgical Centers

- Others

- By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Breast implants are medical devices surgically placed to enhance or reconstruct breast size and shape, typically filled with silicone gel or saline, used in cosmetic or reconstructive procedures.

Key factors include rising cosmetic surgery demand, technological advancements in implant safety, increasing breast cancer reconstructions, and expanding access in emerging markets.

The market is projected to grow from over USD 2.9 billion in 2025 to USD 6.0 billion by 2035.

The CAGR is expected to be 7.6% from 2026 to 2035.

North America will contribute notably, holding the largest share due to advanced infrastructure and high procedure volumes.

Major players include Allergan (AbbVie), Mentor Worldwide LLC (Johnson & Johnson), Sientra, Inc., GC Aesthetics, and Establishment Labs Holdings Inc.

The report provides comprehensive analysis including market size, trends, segmentation, regional insights, key players, and forecasts.

Stages include raw material sourcing, manufacturing, quality testing, regulatory approval, distribution, surgical implantation, and post-operative care.

Trends are shifting toward natural-feeling implants, customization via technology, and safety-focused innovations, with consumers preferring minimally invasive options and bio-compatible materials.

Stringent FDA regulations on safety and approvals, along with environmental concerns over non-biodegradable materials, influence growth by driving innovation in sustainable and compliant products.