Kombucha Market Size, Share and Trends 2026 to 2035

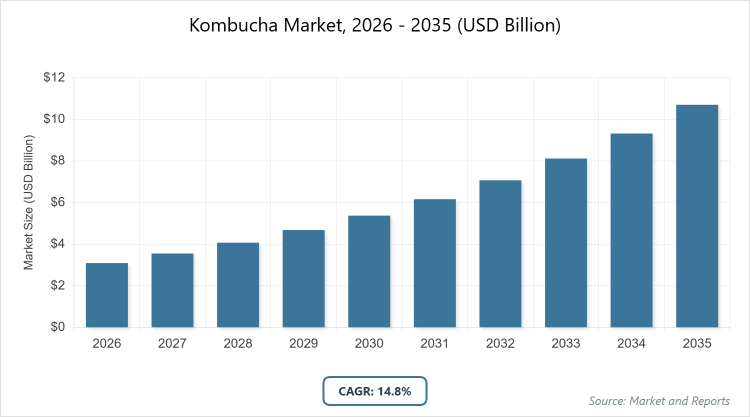

According to MarketnReports, the global Kombucha market size was estimated at USD 3.09 billion in 2025 and is expected to reach USD 12.28 billion by 2035, growing at a CAGR of 14.8% from 2026 to 2035. Rising consumer interest in probiotic-rich functional beverages.

What are the Key Insights into Kombucha Market?

- The global kombucha market size was valued at USD 3.09 billion in 2025 and is projected to reach USD 12.28 billion by 2035.

- The market is expected to grow at a CAGR of 14.8% during the forecast period from 2026 to 2035.

- The market is driven by increasing consumer preference for probiotic-rich, functional beverages and health-conscious lifestyles.

- In the flavor segment, the fruits subsegment dominated with a 61.7% share, owing to its appealing taste profiles and alignment with consumer demands for innovative, refreshing options that enhance market accessibility.

- In the type segment, the conventional subsegment held the largest share at around 80%, driven by its traditional appeal and widespread availability as a non-alcoholic health drink.

- In the distribution channel segment, the off-trade subsegment accounted for 70% of the market, primarily due to convenience in retail purchasing and growing e-commerce penetration for at-home consumption.

- North America dominated the regional market with a 33% share, attributed to high consumer awareness of health benefits, strong retail infrastructure, and presence of key brands like GT’s Living Foods.

What is the Kombucha Market?

Industry Overview

The kombucha market encompasses the production, distribution, and consumption of fermented tea beverages infused with probiotics, known for their health benefits such as improved digestion and immunity, appealing to wellness-focused consumers in both retail and foodservice channels. Market definition includes kombucha as a lightly effervescent drink made from sweetened tea fermented with a symbiotic culture of bacteria and yeast (SCOBY), available in flavored, hard, and conventional varieties, targeting health-conscious demographics through online, supermarket, and on-trade outlets to meet demands for functional, low-alcohol alternatives in the non-alcoholic beverage sector.

What are the Market Dynamics of Kombucha Market?

Growth Drivers

Growth drivers in the kombucha market are fueled by rising awareness of gut health and probiotics, prompting consumers to seek functional beverages like kombucha as alternatives to sugary sodas, with innovations in flavors enhancing appeal. The expansion of e-commerce and retail channels facilitates wider accessibility, while millennial and Gen Z preferences for natural, organic products drive demand. Government promotions of healthy lifestyles and increasing disposable incomes in emerging markets further accelerate adoption, supported by marketing campaigns highlighting kombucha’s detoxifying and immune-boosting properties.

Restraints

Restraints include high production costs due to organic ingredients and fermentation processes, limiting affordability in price-sensitive markets and hindering mass adoption. Regulatory challenges around alcohol content in hard kombucha variants create compliance issues, while short shelf life and cold chain requirements increase logistics expenses. Consumer skepticism regarding health claims and competition from other functional drinks like kefir also pose barriers to expansion.

Opportunities

Opportunities emerge from the growing trend toward low-alcohol and alcohol-free beverages, where hard kombucha can capture the adult non-alcoholic segment with innovative flavors. Expansion into untapped markets in Asia Pacific through localized products offers potential, as rising health consciousness creates demand. Partnerships with wellness brands for co-branded items and investments in sustainable packaging can attract eco-conscious consumers, while R&D in probiotic enhancements opens avenues for premium positioning.

Challenges

Challenges involve maintaining consistent quality during fermentation, as variations can affect taste and probiotic efficacy, requiring advanced controls. Supply chain disruptions for organic tea and SCOBY cultures impact production, while counterfeit products erode brand trust. Evolving consumer tastes demand continuous innovation, and stringent food safety regulations across regions necessitate adaptations, increasing operational complexities for global players.

Kombucha Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Kombucha Market |

| Market Size 2025 | USD 3.09 Billion |

| Market Forecast 2035 | USD 12.28 Billion |

| Growth Rate | CAGR of 14.8% |

| Report Pages | 220 |

| Key Companies Covered |

GT’s Living Foods, Health-Ade, KeVita (PepsiCo), Brew Dr. Kombucha, Humm Kombucha, and Others |

| Segments Covered | By Flavor (Fruits, Herbs & Spices, Original, Flowers, and Others), By Type (Conventional, Hard, and Others), By Distribution Channel (On-Trade, Off-Trade, Online, Supermarkets, and Others), and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Kombucha Market?

The Kombucha market is segmented by flavor, type, distribution channel, and region.

Based on Flavor Segment, the fruits subsegment is the most dominant, holding over 61.7% share, followed by herbs & spices as the second most dominant. Fruits’ dominance arises from its vibrant taste appeal and perceived health benefits, driving the market by attracting a broader consumer base seeking refreshing alternatives to traditional sodas, thereby boosting sales volumes and encouraging product diversification.

Based on Type Segment, conventional leads with approximately 80% share, with hard as the second dominant. Conventional’s leading position is due to its non-alcoholic nature and established consumer trust in probiotic benefits, propelling market growth through widespread availability in health stores and supermarkets, fostering habitual consumption among wellness enthusiasts.

Based on the Distribution Channel Segment, off-trade dominates with 70% share, followed by online. Off-trade’s supremacy stems from convenience in retail purchasing for home use, aiding market drive by enabling impulse buys and brand visibility in grocery chains, thus expanding reach to everyday consumers.

What are the Recent Developments in Kombucha Market?

- In 2025, GT’s Living Foods launched a new line of low-sugar kombucha flavors, focusing on organic ingredients to meet rising demand for healthier options.

- In late 2024, Health-Ade introduced a collaboration with a celebrity chef for limited-edition herb-infused kombucha, boosting brand visibility through social media campaigns.

- In 2025, KeVita (PepsiCo) expanded its distribution network in Asia, partnering with local retailers to introduce fruit-flavored variants tailored to regional tastes.

- In early 2026, Brew Dr. Kombucha acquired a small craft brewery to enhance its hard kombucha production, aiming to capture the growing low-alcohol segment.

- In 2025, Humm Kombucha released a sustainable packaging initiative, using recycled materials to appeal to eco-conscious consumers and reduce environmental impact.

What is the Regional Analysis of Kombucha Market?

- North America is expected to dominate the global market.

North America leads the kombucha market, holding approximately 33% share, driven by high health awareness, robust retail networks, and innovation in functional beverages. The United States dominates within the region, supported by major brands like GT’s Living Foods, widespread e-commerce, and consumer trends toward probiotics, fostering market expansion through premium positioning and diverse flavor offerings.

Asia Pacific is the fastest-growing region, with a projected CAGR of 14.2%, attributed to urbanization, rising middle-class incomes, and cultural affinity for fermented drinks. China leads as the dominant country, fueled by e-commerce growth, local flavor adaptations, and health campaigns promoting gut health amid increasing wellness focus.

Europe exhibits strong growth at a CAGR of 13%, bolstered by sustainability trends and organic preferences. Germany is the leading country, driven by strict quality standards, craft brewery integrations, and demand for low-sugar variants aligning with health regulations.

Latin America shows emerging potential, with growth from increasing health consciousness and retail expansion. Brazil dominates, thanks to tropical flavor innovations and rising disposable incomes supporting premium kombucha adoption.

The Middle East and Africa region holds about 10% share, with gradual expansion through tourism and urban development. The United Arab Emirates leads, propelled by luxury retail and wellness tourism requiring diverse, health-focused beverages.

Who are the Key Market Players in Kombucha Market?

- GT’s Living Foods focuses on organic, raw kombucha production, emphasizing probiotic benefits and flavor innovation to maintain market leadership.

- Health-Ade employs artisanal brewing techniques, prioritizing transparency in ingredients and partnerships for limited-edition flavors to enhance consumer loyalty.

- KeVita (PepsiCo) leverages distribution networks for widespread availability, focusing on functional variants with added vitamins to appeal to health-conscious demographics.

- Brew Dr. Kombucha integrates tea expertise with fermentation, emphasizing no-added-sugar options and expansions into hard kombucha for diversified revenue.

- Humm Kombucha develops low-calorie, bold-flavored products, using sustainable practices and e-commerce strategies to target younger consumers.

What are the Market Trends in the Kombucha Market?

- Increasing demand for low-sugar and organic variants aligns with health-conscious preferences.

- Rise of hard kombucha as a low-alcohol alternative in social settings.

- Expansion of flavored options incorporating exotic fruits and herbs for taste innovation.

- Growth in e-commerce sales for convenient home delivery and subscription models.

- Focus on sustainable packaging to attract eco-friendly consumers.

- Integration of functional ingredients like adaptogens for added health benefits.

- Partnerships with wellness influencers for marketing and brand visibility.

- Adoption of craft brewing techniques for premium positioning.

What are the Market Segments and their Subsegments Covered in the Kombucha Report?

By Flavor

- Fruits

- Herbs & Spices

- Original

- Flowers

- Others

By Type

- Conventional

- Hard

- Others

By Distribution Channel

- On-Trade

- Off-Trade

- Online

- Supermarkets

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Kombucha Market - Industry Analysis

Chapter 4. Global Kombucha Market- Competitive Landscape

Chapter 5. Global Kombucha Market - Flavor Analysis

Chapter 6. Global Kombucha Market - Type Analysis

Chapter 7. Global Kombucha Market - Distribution Channel Analysis

Chapter 8. Kombucha Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Kombucha is a fermented tea beverage rich in probiotics, made from sweetened tea and a SCOBY culture, offering health benefits like improved digestion.

Key factors include probiotic demand, flavor innovations, e-commerce growth, and health trends.

The market is projected to grow from USD 3.52 billion in 2026 to USD 12.28 billion by 2035.

The CAGR is expected to be 14.8% from 2026 to 2035.

North America will contribute notably, holding around 33% of the market value due to high awareness and retail presence.

Major players include GT’s Living Foods, Health-Ade, KeVita (PepsiCo), Brew Dr. Kombucha, and Humm Kombucha.

The report provides comprehensive analysis including market size, trends, segmentation, regional insights, key players, growth drivers, restraints, opportunities, challenges, and forecasts from 2026 to 2035.

The value chain includes ingredient sourcing, fermentation production, flavoring and bottling, distribution, retail sales, and consumer consumption.

Trends are shifting toward low-sugar and functional variants, while consumers prefer organic, flavored options for health benefits.

Regulations on alcohol content and labeling promote compliance, while environmental sustainability drives eco-friendly packaging.