Lithium Ion Battery Separator Market Size, Share and Trends 2026 to 2035

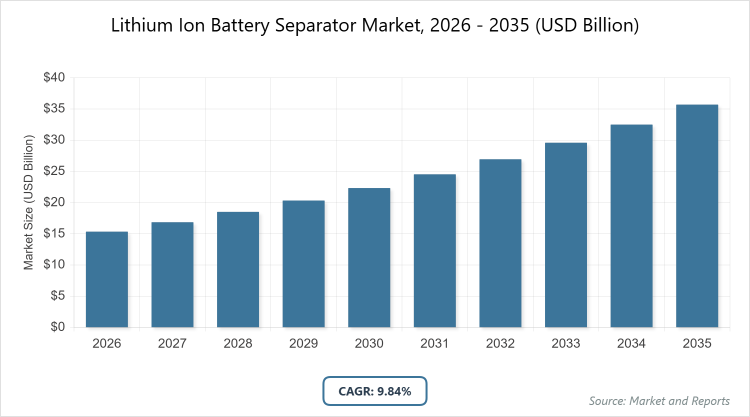

According to MarketnReports, the global Lithium Ion Battery Separator Market size was estimated at USD 15.34 Billion in 2025 and is expected to reach USD 39.23 Billion by 2035, growing at a CAGR of 9.84% from 2026 to 2035. Lithium Ion Battery Separator Market is driven by increasing demand for electric vehicles and renewable energy storage solutions.

What is the Industry Overview of Lithium Ion Battery Separator Market?

The lithium ion battery separator market encompasses the production and distribution of specialized membranes that play a critical role in lithium-ion batteries by preventing direct contact between the anode and cathode while allowing ionic flow to enable energy transfer. These separators are essential components in rechargeable batteries, ensuring safety, efficiency, and longevity by mitigating risks such as short circuits and thermal runaway. Market definition refers to the global ecosystem involving manufacturers, suppliers, and end-users focused on porous polymeric or ceramic materials designed for high-performance energy storage applications across various industries.

What are the Key Insights into Lithium Ion Battery Separator Market?

- The global lithium ion battery separator market was valued at USD 15.34 billion in 2025 and is projected to reach USD 39.23 billion by 2035.

- The market is expected to grow at a CAGR of 9.84% during the forecast period from 2026 to 2035.

- The market is driven by surging adoption of electric vehicles, advancements in battery technology, and growing demand for energy storage systems.

- In the material segment, polypropylene dominates with a 48% share due to its excellent thermal stability, low cost, and high porosity that enhances ion conductivity and battery performance.

- In the application segment, electric vehicles dominate with a 50% share owing to the rapid expansion of the EV industry, government incentives for green transportation, and the need for high-safety battery components.

- In the end-use segment, automotive holds the largest share at 45% because of the integration of lithium-ion batteries in hybrid and electric vehicles, driving demand for reliable separators to ensure vehicle safety and efficiency.

- Asia Pacific dominates the regional landscape with a 50% share, attributed to its robust manufacturing infrastructure, presence of key battery producers in China, Japan, and South Korea, and supportive policies for electric mobility.

What are the Market Dynamics of Lithium Ion Battery Separator Market?

Growth Drivers

The primary growth drivers for the lithium ion battery separator market include the exponential rise in electric vehicle adoption worldwide, fueled by stringent emission regulations and consumer shift towards sustainable transportation. Additionally, the increasing integration of renewable energy sources necessitates efficient energy storage solutions, where advanced separators enhance battery durability and performance. Technological innovations, such as thinner and more heat-resistant materials, further propel market expansion by improving battery safety and energy density, catering to the demands of high-power applications like grid storage and portable electronics.

Restraints

Key restraints in the lithium ion battery separator market stem from the high production costs associated with advanced materials like ceramic-coated separators, which limit accessibility for smaller manufacturers and emerging markets. Supply chain disruptions, particularly in raw materials such as polyethylene and polypropylene, exacerbate price volatility and hinder scalable production. Moreover, environmental concerns over the disposal and recycling of battery components pose regulatory hurdles, potentially slowing market growth as governments enforce stricter sustainability standards.

Opportunities

Opportunities abound in the lithium ion battery separator market with the advent of solid-state batteries, which require innovative separator designs to achieve higher energy densities and safer operations. Expanding investments in research for bio-based and recyclable separators open avenues for eco-friendly alternatives, aligning with global sustainability goals. Emerging markets in developing regions present untapped potential through infrastructure development for electric vehicles and renewable energy, creating demand for cost-effective, high-performance separators.

Challenges

Challenges facing the lithium ion battery separator market include ensuring consistent quality and safety standards amid rapid technological advancements, as defects can lead to battery failures and recalls. Intense competition from alternative battery technologies, such as sodium-ion, threatens market share by offering potentially cheaper options. Furthermore, geopolitical tensions affecting raw material sourcing from key regions like Asia Pacific complicate supply chains, increasing operational risks for global players.

Lithium Ion Battery Separator Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Lithium Ion Battery Separator Market |

| Market Size 2025 | USD 15.34 Billion |

| Market Forecast 2035 | USD 39.23 Billion |

| Growth Rate | CAGR of 9.84% |

| Report Pages | 220 |

| Key Companies Covered |

Asahi Kasei Corporation, Toray Industries Inc., SK Innovation Co. Ltd., Celgard, Mitsubishi Chemical, Sumitomo Chemical Co. Ltd., Teijin Limited, and Others |

| Segments Covered | By Material, By Application, By End-Use, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Lithium Ion Battery Separator Market?

The Lithium Ion Battery Separator Market is segmented by material, application, end-use, and region. All the segments have been analyzed based on present and future trends and the market is estimated from 2026 to 2035.

Based on Material Segment: Polypropylene emerges as the most dominant subsegment with a 48% share, followed by polyethylene as the second most dominant at 30%. Polypropylene’s dominance stems from its superior mechanical strength, chemical resistance, and affordability, which optimize battery efficiency and reduce manufacturing costs; this drives the market by enabling mass production of high-performance batteries for electric vehicles and consumer electronics, while polyethylene supports growth through its flexibility and high ionic conductivity in diverse applications.

Based on Application Segment: Electric vehicles lead as the most dominant subsegment with a 50% share, with consumer electronics as the second most dominant at 25%. The EV segment’s dominance is driven by global electrification trends and policy incentives, where separators ensure safety and longevity in high-voltage systems, propelling overall market expansion; consumer electronics contribute by demanding compact, reliable batteries for devices like smartphones, fostering innovation in thinner separator technologies.

Based on End-Use Segment: Automotive is the most dominant subsegment holding 45%, followed by electronics manufacturers at 20%. Automotive’s leading position arises from the surge in hybrid and electric vehicle production, where separators enhance battery reliability and range, significantly boosting market demand; electronics manufacturers drive growth through continuous miniaturization and power efficiency needs in portable gadgets.

What are the Recent Developments in Lithium Ion Battery Separator Market?

- In November 2024, Microporous announced a USD 1.35 billion investment in a new lithium-ion battery separator manufacturing facility in South Virginia, USA, aiming to expand production capacity for automotive and stationary power applications while leveraging expertise in lead battery separators.

- Asahi Kasei Corporation revealed plans in early 2025 to collaborate with a major EV manufacturer on developing next-generation ceramic-coated separators, focusing on improving thermal stability for high-energy-density batteries.

- Toray Industries expanded its production line in Japan in mid-2025, introducing eco-friendly bio-based separators to meet rising demand for sustainable materials in the European market.

What is the Regional Analysis of Lithium Ion Battery Separator Market?

Asia Pacific to dominate the global market.

Asia Pacific holds the largest share at 50%, driven by China’s dominance as the world’s leading battery producer, supported by extensive supply chains, government subsidies for EV manufacturing, and rapid industrialization that accelerates demand for separators in electric vehicles and energy storage.

North America follows with significant growth, led by the United States through investments in domestic battery production facilities and incentives under the Inflation Reduction Act, emphasizing advancements in separator technology for automotive and renewable applications to reduce reliance on imports.

Europe exhibits robust expansion, with Germany at the forefront due to its strong automotive sector transitioning to electrification, stringent environmental regulations promoting sustainable battery components, and collaborations between manufacturers for innovative separator materials.

Latin America shows emerging potential, primarily in Brazil, where increasing adoption of renewable energy projects and growing EV markets drive demand, though limited by infrastructure challenges and reliance on imported technologies.

The Middle East and Africa remain nascent, with South Africa leading through mining resources for battery materials and pilot projects in energy storage, but growth is tempered by economic constraints and underdeveloped manufacturing capabilities.

Who are the Key Market Players in Lithium Ion Battery Separator Market?

Asahi Kasei Corporation focuses on innovation through R&D investments in ceramic-coated separators, strategic partnerships with battery makers, and expansion of production facilities in Asia to capture the growing EV market while emphasizing sustainability.

Toray Industries Inc. employs vertical integration strategies, developing high-porosity polypropylene separators, and collaborates with global automakers to enhance battery safety, alongside mergers to strengthen its supply chain presence.

SK Innovation Co. Ltd. prioritizes technological advancements in wet-process separators, joint ventures for localized production in Europe and North America, and sustainability initiatives like recyclable materials to drive market leadership.

Celgard leverages its expertise in microporous membranes, pursuing acquisitions to broaden its portfolio and investing in R&D for thinner separators to meet demands in consumer electronics and energy storage.

Mitsubishi Chemical adopts cost-optimization strategies, expanding into ceramic composites, and forms alliances with renewable energy firms to address grid storage needs while focusing on eco-friendly production processes.

Sumitomo Chemical Co. Ltd. emphasizes diversification through non-woven separator development, global expansion via subsidiaries, and R&D in high-temperature resistant materials for industrial applications.

Teijin Limited implements innovation-driven approaches, including aramid-based separators for enhanced durability, and strategic collaborations with tech firms to integrate smart features into batteries.

What are the Market Trends in Lithium Ion Battery Separator Market?

- Shift towards ceramic-coated separators for improved thermal stability and safety in high-power applications like electric vehicles.

- Adoption of thinner separators (below 20µm) to increase energy density and extend battery life in portable devices.

- Growing emphasis on sustainable and bio-based materials to reduce environmental impact and comply with regulations.

- Integration of nanotechnology for enhanced porosity and ion conductivity, boosting overall battery efficiency.

- Rise in solid-state battery compatibility, driving demand for advanced composite separators.

What Market Segments and Subsegments are Covered in the Lithium Ion Battery Separator Report?

- By Material

- Polypropylene (PP)

- Polyethylene (PE)

- Ceramic-Coated

- Nylon

- Cellulose

- Aramid

- PVDF

- Polyimide (PI)

- Polyethersulfone (PES)

- Composite

- Others

- By Application

- Consumer Electronics

- Electric Vehicles

- Energy Storage Systems

- Power Tools

- Medical Devices

- Aerospace

- Marine

- E-Bikes

- Industrial Equipment

- Grid Storage

- Others

- By End-Use

- Automotive

- Electronics Manufacturers

- Industrial Sector

- Utilities

- Healthcare

- Defense

- Transportation

- Consumer Goods

- Renewable Energy Providers

- Telecommunication

- Others

- By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Lithium Ion Battery Separator Market - Industry Analysis

Chapter 4. Global Lithium Ion Battery Separator Market- Competitive Landscape

Chapter 5. Global Lithium Ion Battery Separator Market - Material Analysis

Chapter 6. Global Lithium Ion Battery Separator Market - Application Analysis

Chapter 7. Global Lithium Ion Battery Separator Market - End-Use Analysis

Chapter 8. Lithium Ion Battery Separator Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

The lithium ion battery separator market encompasses the production and distribution of specialized membranes that play a critical role in lithium-ion batteries by preventing direct contact between the anode and cathode while allowing ionic flow to enable energy transfer.

Rising EV adoption, technological advancements in battery safety, increasing renewable energy storage needs, and government policies promoting green energy will significantly influence market growth during this period.

The market is projected to grow from approximately USD 15.34 billion in 2026 to USD 39.23 billion by 2035.

The CAGR is expected to be 9.84% over the forecast period from 2026 to 2035.

Asia Pacific will contribute the most, holding around 50% of the market value due to its manufacturing dominance and EV growth.

Major players include Asahi Kasei Corporation, Toray Industries Inc., SK Innovation Co. Ltd., Celgard, and Mitsubishi Chemical, driving growth through innovation and expansion.

The report provides comprehensive analysis including market size, trends, segmentation, regional insights, key players, and forecasts from 2026 to 2035.

Trends are shifting towards sustainable materials and ceramic coatings, while consumers prefer high-safety, efficient separators for longer-lasting batteries in EVs and electronics.

Stringent safety regulations, environmental mandates for recyclable materials, and policies on reducing carbon emissions are positively impacting growth by encouraging innovation in eco-friendly separators.