Plastic Films & Sheets Market Size, Share and Trends 2026 to 2035

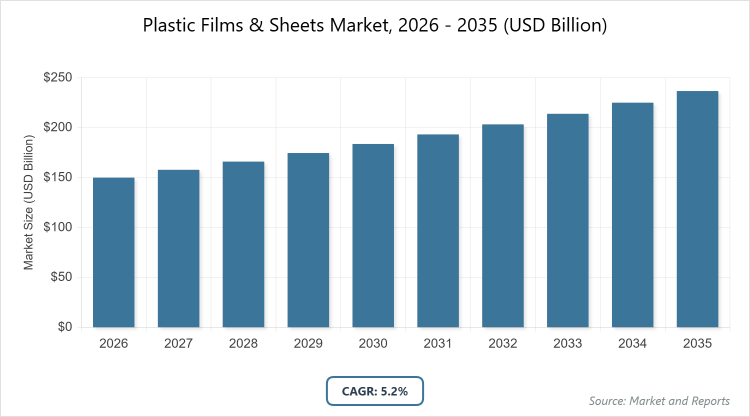

According to MarketnReports, the global Plastic Films & Sheets market size was estimated at USD 150 billion in 2025 and is expected to reach USD 250 billion by 2035, growing at a CAGR of 5.2% from 2026 to 2035. Plastic Films & Sheets Market is driven by rising demand for sustainable packaging solutions across industries.

What are the Key Insights into Plastic Films & Sheets Market?

- The global plastic films and sheets market was valued at USD 150 billion in 2025 and is projected to reach USD 250 billion by 2035.

- The market is anticipated to grow at a CAGR of 5.2% during the forecast period from 2026 to 2035.

- The market is driven by increasing demand for flexible and sustainable packaging in food, healthcare, and consumer goods sectors.

- In the product segment, LLDPE/LDPE dominates with a 40% share due to its versatility, low cost, and excellent flexibility for applications like stretch films and bags.

- In the application segment, packaging dominates with an 80% share owing to its critical role in extending shelf life and protecting goods during transportation.

- In the end-use segment, food & beverage dominates with a 45% share because of the need for barrier properties to maintain freshness and prevent contamination.

- Asia Pacific dominates the market with a 42% share, driven by rapid industrialization, population growth, and expanding manufacturing in countries like China and India.

What is the Industry Overview of Plastic Films & Sheets Market?

The plastic films and sheets market encompasses a wide array of flexible polymeric materials used for protective, barrier, and structural purposes. Plastic films are thin, continuous layers typically under 0.25 mm thick, while sheets are thicker variants offering greater rigidity. The market definition includes products derived from polymers like polyethylene, polypropylene, and polyvinyl chloride, serving as essential components in packaging to preserve product integrity, in agriculture for crop protection, and in construction for insulation and waterproofing. This industry plays a pivotal role in modern manufacturing by providing lightweight, cost-effective alternatives to traditional materials, enabling innovations in food preservation, medical sterilization, and industrial applications.

What are the Market Dynamics of Plastic Films & Sheets Market?

Growth Drivers

The primary growth drivers for the plastic films and sheets market include surging demand from the packaging industry, fueled by e-commerce expansion and consumer preference for convenient, lightweight solutions. Rapid urbanization and globalization have heightened the need for processed foods and ready-to-eat products, where these materials provide essential moisture and oxygen barriers to extend shelf life. Technological advancements in polymer science, such as multi-layer films with enhanced strength and recyclability, are accelerating adoption across sectors. Additionally, the agricultural sector’s increasing use of mulch films and greenhouse coverings to boost crop yields in emerging economies is a significant driver, supported by government initiatives for sustainable farming practices.

Restraints

Environmental concerns and stringent regulations on single-use plastics pose major restraints, as governments worldwide implement bans and taxes to curb pollution. The vulnerability to fluctuating raw material prices, particularly petroleum-based resins, increases production costs and squeezes profit margins for manufacturers. Limited recycling infrastructure for complex multi-layer films hinders circular economy efforts, leading to higher waste management expenses. Moreover, shifting consumer preferences toward eco-friendly alternatives like paper-based packaging in developed regions is eroding market share for traditional plastic films and sheets.

Opportunities

Opportunities abound in the development of bio-based and biodegradable films derived from renewable sources like starch and PLA, aligning with global sustainability goals and opening new markets in eco-conscious regions. Emerging economies in Asia Pacific and Latin America present untapped potential due to rising disposable incomes and expanding industrial sectors. Innovations in smart films incorporating nanotechnology for antimicrobial properties or temperature control offer growth in healthcare and food preservation applications. Partnerships between manufacturers and recycling firms to improve post-consumer recovery rates can create competitive advantages and meet regulatory demands.

Challenges

The market faces challenges from inadequate recycling facilities, especially for specialized films, resulting in low recovery rates and environmental backlash. Volatility in supply chains, exacerbated by geopolitical tensions and energy crises, disrupts raw material availability and increases operational risks. Intense competition from alternative materials like aluminum foils and glass in high-barrier applications adds pressure on pricing strategies. Finally, educating end-users on the benefits of advanced, sustainable plastic options remains a hurdle in price-sensitive markets.

Plastic Films & Sheets Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Plastic Films & Sheets Market |

| Market Size 2025 | USD 150 Billion |

| Market Forecast 2035 | USD 250 Billion |

| Growth Rate | CAGR of 5.2% |

| Report Pages | 210 |

| Key Companies Covered |

Amcor PLC, Berry Global Group, Inc., SABIC, Toray Industries, Inc., Sealed Air Corporation, Uflex Limited, Toyobo Co., Ltd., Jindal Poly Films Limited, DuPont Teijin Films, Oben Holding Group, and Others |

| Segments Covered | By Product, By Application, By End-Use, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Plastic Films & Sheets Market?

The Plastic Films & Sheets market is segmented by product, application, end-use, and region.

Based on Product Segment: LLDPE/LDPE is the most dominant subsegment, holding approximately 40% market share, due to its superior flexibility, puncture resistance, and cost-effectiveness, which drive its widespread use in packaging films and agricultural mulches to enhance efficiency and reduce material waste. HDPE is the second most dominant, with around 20% share, valued for its high strength-to-density ratio and chemical resistance, enabling it to propel market growth in construction sheeting and industrial liners by providing durable, weatherproof solutions.

Based on Application Segment: Packaging is the most dominant subsegment, capturing about 80% market share, as it offers essential protection against contaminants and extends product shelf life, fueling market expansion through innovations in flexible pouches and wraps for food and consumer goods. Non-packaging is the second most dominant, with roughly 20% share, driven by applications in agriculture and construction where films provide crop protection and insulation, contributing to market growth by improving yield efficiency and building durability.

Based on End-Use Segment: Food & beverage is the most dominant subsegment, accounting for nearly 45% market share, owing to the need for hygienic, barrier-enhanced packaging that preserves freshness, thereby driving overall market advancement in global supply chains. Healthcare is the second most dominant, with about 15% share, supported by sterile films for medical devices and pharmaceuticals, which bolster market growth through compliance with stringent safety standards and rising demand for disposable products.

What are the Recent Developments in Plastic Films & Sheets Market?

- In February 2025, IPG launched a new American brand of plastic sheeting, featuring ultra and performance films designed for enhanced surface protection in industrial applications.

- In November 2024, Sumitomo Bakelite introduced a mono-material film for medical device packaging, with mass production planned for 2025, emphasizing sustainability and recyclability.

- In June 2024, Sigma Plastics Group acquired a Georgia facility to expand its film production capacity, aiming to improve quality and meet growing demand in the market.

What is the Regional Analysis of Plastic Films & Sheets Market?

Asia Pacific to dominate the global market.

Asia Pacific leads the plastic films and sheets market, driven by rapid industrialization and a booming packaging sector in China, which accounts for the largest share due to its massive manufacturing base and export-oriented economy supporting food and consumer goods industries.

North America follows as a key region, with the United States dominating through advanced technological innovations in sustainable films and strong demand from e-commerce and healthcare sectors, emphasizing recyclable materials to comply with environmental regulations.

Europe exhibits steady growth, led by Germany, where stringent sustainability policies and a focus on circular economy practices drive adoption of bio-based films in packaging and automotive applications for reduced carbon footprints.

Latin America is emerging, with Brazil at the forefront, fueled by agricultural expansion using mulch films to enhance crop yields and packaging needs for its growing food export market.

The Middle East and Africa show potential, dominated by South Africa, where infrastructure development and increasing consumer goods consumption boost demand for construction sheeting and protective films.

What are the Key Market Players in Plastic Films & Sheets Market?

- Amcor PLC: Amcor focuses on sustainable packaging innovations, including recyclable films and collaborations for circular economy solutions, enhancing its global footprint through acquisitions and R&D in barrier technologies.

- Berry Global Group, Inc.: Berry emphasizes lightweight, high-performance sheets with a strong push toward recycled content, leveraging mergers to expand production capacity and meet demands in food and industrial sectors.

- SABIC: SABIC invests in advanced polymer resins for films, prioritizing bio-based materials and partnerships to develop ocean-bound plastic solutions, driving growth in Asia and the Middle East.

- Toray Industries, Inc.: Toray specializes in high-tech films like BOPP and PET, with strategies centered on nanotechnology for smart applications and sustainability initiatives to reduce environmental impact.

- Sealed Air Corporation: Sealed Air advances cryogenic and vacuum films for food preservation, focusing on automation and eco-friendly designs to optimize supply chains and minimize waste.

- Uflex Limited: Uflex pursues flexible packaging excellence through vertical integration and innovations in holographic films, targeting emerging markets with cost-effective, customizable solutions.

- Toyobo Co., Ltd.: Toyobo develops functional films for electronics and medical uses, with strategies involving R&D in breathable materials and global expansions for specialized applications.

- Jindal Poly Films Limited: Jindal focuses on BOPP and CPP films, employing capacity expansions and quality certifications to capture shares in packaging and labeling markets.

- DuPont Teijin Films: DuPont Teijin innovates in polyester films for industrial and solar applications, with a strategy of joint ventures and sustainability-focused product lines.

- Oben Holding Group: Oben targets Latin American growth with multi-layer films, emphasizing efficiency and partnerships to enhance barrier properties for food and beverage sectors.

What are the Market Trends in Plastic Films & Sheets Market?

- Shift toward sustainable and bio-based films to meet regulatory and consumer demands for eco-friendly materials.

- Adoption of nanotechnology for smart films offering antimicrobial and self-healing properties.

- Growth in multi-layer barrier structures for enhanced food preservation and shelf life extension.

- Increasing use of recycled content and mono-materials to support circular economy initiatives.

- Expansion of AI-driven manufacturing for precision and waste reduction in film production.

- Rising demand for lightweight films in automotive and aerospace for fuel efficiency.

- Integration of digital printing on films for customized and on-demand packaging.

- Focus on high-performance films for medical and pharmaceutical applications amid health crises.

What are the Market Segments and their Subsegments Covered in the Plastic Films & Sheets Report?

-

By Product

- LLDPE/LDPE

- HDPE

- BOPP

- CPP

- PVC

- PET

- PA

- Others

-

By Application

- Packaging

- Non-Packaging

-

By End-Use

- Food & Beverage

- Healthcare

- Agriculture

- Construction

- Consumer Goods

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

Plastic films and sheets are thin polymeric materials used for packaging, protection, and structural applications, offering flexibility, barrier properties, and durability across industries like food, agriculture, and construction.

Key factors include rising demand for sustainable packaging, technological advancements in bio-based materials, e-commerce growth, and expanding applications in agriculture and healthcare.

The market is projected to grow from USD 150 billion in 2025 to USD 250 billion by 2035.

The market is expected to register a CAGR of 5.2% over the forecast period.

Asia Pacific will contribute the most, driven by industrialization in China and India.

Major players include Amcor PLC, Berry Global Group, Inc., SABIC, Toray Industries, Inc., and Sealed Air Corporation.

The report provides comprehensive analysis of market size, trends, segmentation, key players, regional insights, and forecasts from 2026 to 2035.

The value chain includes raw material sourcing (polymers), extrusion and manufacturing, distribution, end-use application, and recycling or disposal.

Trends are shifting toward recyclable and bio-based films, with consumers preferring eco-friendly, lightweight options that reduce environmental impact.

Regulations on single-use plastics and mandates for recyclability are pushing innovation in sustainable materials, while environmental concerns drive demand for low-carbon alternatives.