Video Streaming Software Market Size, Share and Trends 2026 to 2035

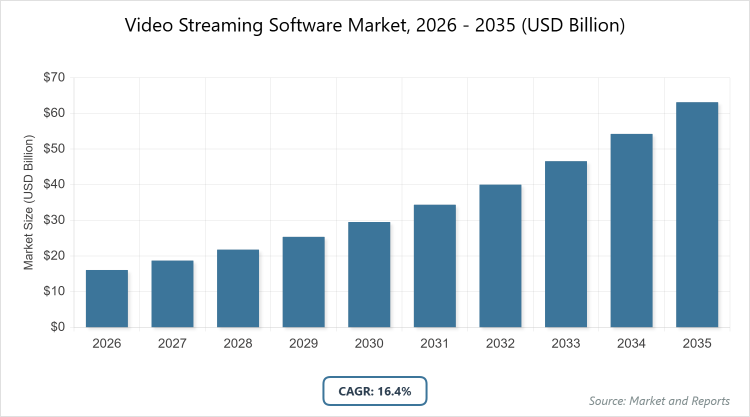

According to MarketnReports, the global Video Streaming Software market size was estimated at USD 16.1 billion in 2025 and is expected to reach USD 73 billion by 2035, growing at a CAGR of 16.4% from 2026 to 2035. The increasing demand for OTT services and live event streaming.

What are the Key Insights into the video streaming software market?

- The global video streaming software market size was valued at USD 16.1 billion in 2025 and is projected to reach USD 73 billion by 2035.

- The market is expected to grow at a CAGR of 16.4% during the forecast period from 2026 to 2035.

- The market is driven by rising adoption of cloud-based platforms, increasing demand for live and on-demand content, and advancements in 5G technology.

- In the solution type segment, the transcoding and processing subsegment dominated with a 35% share, owing to its essential role in optimizing video quality and adaptive bitrate streaming for diverse devices and networks.

- In the streaming type segment, the video-on-demand subsegment held the largest share at around 75%, driven by consumer preferences for flexible viewing and the proliferation of OTT platforms offering extensive content libraries.

- In the vertical segment, the media and entertainment subsegment accounted for 47% of the market, primarily due to high investments in content creation, live events, and monetization strategies that leverage streaming software for global reach.

- North America dominated the regional market with a 40% share, attributed to advanced digital infrastructure, presence of major tech companies, and high consumer adoption of streaming services.

What is the Video Streaming Software Market?

Industry Overview

The video streaming software market comprises platforms and tools that enable the encoding, management, delivery, and monetization of video content over the internet, catering to live and on-demand formats for diverse applications. Market definition includes software solutions that facilitate seamless video transmission, incorporating features like transcoding, analytics, security, and integration with content delivery networks, to support industries such as media, education, and healthcare in providing high-quality, scalable streaming experiences to global audiences via cloud or on-premise deployments.

What are the Market Dynamics of Video Streaming Software Market?

Growth Drivers

Growth drivers in the video streaming software market are propelled by the surge in mobile internet penetration and 5G rollout, enabling high-definition, low-latency streaming on smartphones and smart TVs. The shift toward over-the-top (OTT) platforms and subscription models boosts demand for robust software that handles content management and personalization through AI algorithms. Increasing enterprise adoption for virtual events, training, and marketing, coupled with falling cloud computing costs, accelerates market expansion, while integrations with social media enhance user engagement and content virality.

Restraints

Restraints include bandwidth limitations in developing regions, hindering seamless high-quality streaming and limiting market penetration. Piracy and content security concerns pose challenges, as unauthorized distribution erodes revenue and requires costly DRM implementations. High competition leads to pricing pressures, while interoperability issues between platforms and devices complicate deployments, potentially slowing adoption among smaller enterprises.

Opportunities

Opportunities emerge from the integration of AI and machine learning for advanced analytics, recommendation engines, and automated content moderation, enhancing user retention and monetization. Expanding into emerging markets with rising smartphone usage offers growth through affordable, localized solutions. Partnerships with telecom providers for bundled services and innovations in VR/AR streaming create new avenues for immersive experiences in education and entertainment.

Challenges

Challenges involve ensuring low-latency delivery for live streaming amid varying network conditions, demanding continuous technological upgrades. Data privacy regulations like GDPR require compliant software designs, increasing development costs. Rapid content volume growth overwhelms storage and processing capacities, while evolving consumer preferences for interactive features necessitate ongoing innovation to maintain competitiveness.

Video Streaming Software Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Video Streaming Software Market |

| Market Size 2025 | USD 16.1 Billion |

| Market Forecast 2035 | USD 73 Billion |

| Growth Rate | CAGR of 16.4% |

| Report Pages | 220 |

| Key Companies Covered |

Brightcove Inc., IBM Corporation, Kaltura Inc., Haivision Systems Inc., Wowza Media Systems LLC, Panopto Inc., Qumu Corporation, Vbrick Systems Inc., and Others |

| Segments Covered | By Solution Type (Transcoding and Processing, Video Management, Video Delivery and Distribution, Video Analytics, Video Security, and Others), By Streaming Type (Live Streaming, Video-on-Demand Streaming, and Others), By Vertical (Media and Entertainment, BFSI, Academia and Education, Healthcare, Government, and Others), and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Video Streaming Software Market?

The Video Streaming Software market is segmented by solution type, streaming type, vertical, and region.

Based on the Solution Type Segment, the transcoding and processing subsegment is the most dominant, holding over 35% share, followed by video management as the second most dominant. Transcoding and processing’s dominance arises from its critical function in adapting video formats for optimal playback across devices, driving the market by enabling efficient bandwidth usage and high-quality delivery, which supports scalability for OTT platforms and boosts overall adoption in content-heavy industries.

Based on the Streaming Type Segment, video-on-demand leads with approximately 75% share, with live streaming as the second dominant. Video-on-demand’s leading position is fueled by consumer demand for on-the-go access to vast libraries, propelling market growth through subscription revenues and personalized recommendations that increase viewer engagement and encourage platform loyalty.

Based on Vertical Segment, media and entertainment dominate with 47% share, followed by education. Media and entertainment’s supremacy stems from extensive content production and global distribution needs, aiding market drive by leveraging software for monetization via ads and subscriptions, thus expanding reach and revenue streams in a digital-first entertainment landscape.

What are the Recent Developments in Video Streaming Software Market?

- In October 2024, Amazon acquired MX Player to strengthen its presence in India’s streaming market, enhancing local content offerings and complementing Prime Video.

- In August 2024, Apple TV+ updated its interface for better navigation and voice search, aiming to improve user experience in competitive streaming environments.

- In April 2024, Accedo and Brightcove launched Iraq’s first SVOD platform with Al Sharqiya Group, expanding premium content access in the region.

- In February 2025, Tencent Cloud partnered with Begin to enhance global streaming services, focusing on scalability and cloud-based delivery.

- In April 2025, Vimeo introduced Vimeo Streaming, enabling creators to launch branded apps with advanced monetization and analytics features.

What is the Regional Analysis of Video Streaming Software Market?

- North America is expected to dominate the global market.

North America leads the video streaming software market, holding approximately 40% share, driven by robust technological infrastructure, high broadband penetration, and innovative content strategies. The United States dominates within the region, supported by major players like Netflix and Amazon, extensive investments in 5G, and consumer preferences for diverse OTT platforms, fostering advancements in AI personalization and live streaming capabilities.

Asia Pacific is the fastest-growing region, with a projected CAGR of 20%, attributed to rapid digitalization, smartphone proliferation, and government initiatives for broadband expansion. China leads as the dominant country, fueled by massive user bases on platforms like iQIYI, investments in cloud infrastructure, and rising demand for localized content amid e-commerce integrations.

Europe exhibits strong growth at a CAGR of 15%, bolstered by regulatory support for digital content and privacy standards. The United Kingdom is the leading country, driven by BBC and Sky partnerships, focus on hybrid cloud deployments, and consumer shifts toward ad-supported models for cost-effective streaming.

Latin America shows emerging potential, with growth from increasing internet access and mobile streaming. Brazil dominates, thanks to Globo and Netflix expansions, investments in local productions, and adoption in education and entertainment amid economic digital shifts.

The Middle East and Africa region holds about 6% share, with gradual expansion through smart city initiatives and mobile networks. The United Arab Emirates leads, propelled by Etisalat collaborations, luxury content platforms, and tourism-driven live events requiring secure, high-quality streaming solutions.

Who are the Key Market Players in Video Streaming Software Market?

- Brightcove Inc. focuses on cloud-based platforms for video hosting and monetization, emphasizing integrations with e-commerce and social media to enhance audience engagement.

- IBM Corporation leverages Watson AI for video analytics and personalization, partnering with enterprises for secure, scalable streaming solutions in hybrid environments.

- Kaltura Inc. develops open-source platforms for education and corporate training, prioritizing interoperability and API integrations to support customized workflows.

- Haivision Systems Inc. specializes in low-latency live streaming for broadcast and defense, focusing on hardware-software hybrids for mission-critical applications.

- Wowza Media Systems LLC offers flexible streaming engines for developers, emphasizing real-time analytics and multi-protocol support to optimize delivery costs.

- Panopto Inc. targets academic and corporate sectors with video management tools, integrating AI for searchable transcripts to improve knowledge accessibility.

- Qumu Corporation provides enterprise video platforms with strong security features, collaborating on compliance solutions for regulated industries like finance.

- Vbrick Systems Inc. advances Rev platform for internal communications, focusing on edge caching and analytics to ensure reliable delivery in large organizations.

What are the Market Trends in Video Streaming Software Market?

- Integration of AI for personalized content recommendations and automated moderation.

- Adoption of 5G for low-latency live streaming and enhanced mobile experiences.

- Growth in cloud deployments for scalability and cost efficiency.

- Rise of interactive and shoppable video features in e-commerce.

- Emphasis on data privacy and DRM to combat piracy.

- Expansion of ad-supported models for broader accessibility.

- Partnerships for bundled services with telecom providers.

- Innovations in VR/AR for immersive streaming applications.

What are the Market Segments and their Subsegments Covered in the Video Streaming Software Report?

By Solution Type

- Transcoding and Processing

- Video Management

- Video Delivery and Distribution

- Video Analytics

- Video Security

- Others

By Streaming Type

- Live Streaming

- Video-on-Demand Streaming

- Others

By Vertical

- Media and Entertainment

- BFSI

- Academia and Education

- Healthcare

- Government

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Video Streaming Software Market - Industry Analysis

Chapter 4. Global Video Streaming Software Market- Competitive Landscape

Chapter 5. Global Video Streaming Software Market - Solution Type Analysis

Chapter 6. Global Video Streaming Software Market - Streaming Type Analysis

Chapter 7. Global Video Streaming Software Market - Vertical Analysis

Chapter 8. Video Streaming Software Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Video streaming software are tools and platforms that enable the encoding, management, delivery, and analysis of video content over the internet for live and on-demand viewing.

Key factors include 5G adoption, AI advancements, rising OTT demand, cloud migration, and expanding applications in education and enterprises.

The market is projected to grow from USD 18.6 billion in 2026 to USD 73 billion by 2035.

The CAGR is expected to be 16.4% from 2026 to 2035.

North America will contribute notably, holding around 40% of the market value due to technological advancements and high adoption.

Major players include Brightcove Inc., IBM Corporation, Kaltura Inc., Haivision Systems Inc., Wowza Media Systems LLC, Panopto Inc., Qumu Corporation, and Vbrick Systems Inc.

The report provides comprehensive analysis including market size, trends, segmentation, regional insights, key players, growth drivers, restraints, opportunities, challenges, and forecasts from 2026 to 2035.

The value chain includes content creation, encoding/transcoding, content management, delivery via CDNs, monetization, and analytics/end-user consumption.

Trends are shifting toward AI personalization, low-latency live streams, and ad-supported models, while consumers prefer seamless, multi-device access and interactive content.

Regulations on data privacy (e.g., GDPR) and net neutrality influence secure, compliant solutions, while environmental concerns drive energy-efficient cloud infrastructures.