Private Hospitals Market Size, Share and Trends 2026 to 2035

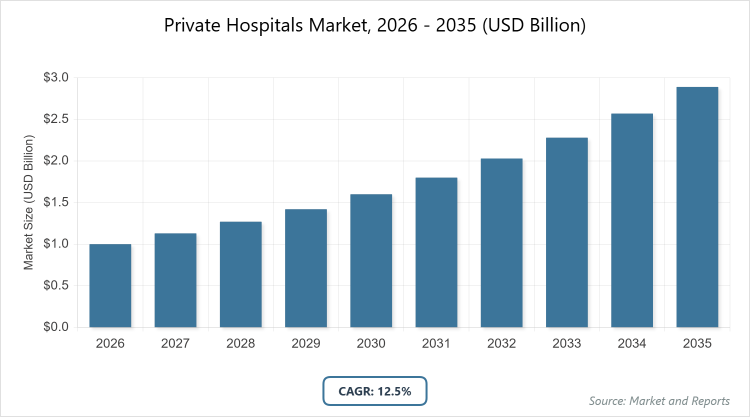

According to MarketnReports, the global Private Hospitals market size was estimated at USD 1,300 billion in 2025 and is expected to reach USD 4,100 billion by 2035, growing at a CAGR of 12.5% from 2026 to 2035. Private Hospitals Market is driven by increasing demand for specialized medical services amid rising chronic diseases and an aging population.

What are the Key Insights in the Private Hospitals Market Report?

- The global Private Hospitals market was valued at USD 1,300 billion in 2025 and is projected to reach USD 4,100 billion by 2035.

- The market is expected to grow at a CAGR of 12.5% during the forecast period from 2026 to 2035.

- The market is driven by increasing demand for medical services, an aging population, enhanced reimbursement policies, and rising chronic diseases.

- In the Type segment, Acute Care Hospitals dominate with approximately 45% market share due to the presence of numerous facilities in urban and rural areas catering to immediate medical needs and the rising incidence of contagious diseases.

- In the Hospital Capacity segment, Medium-sized hospitals (100-500 beds) dominate with about 55% market share because of the proliferation of private hospitals and clinics that balance operational efficiency with comprehensive service offerings.

- In the Location segment, Urban areas dominate with around 70% market share owing to higher disposable incomes, better infrastructure, and a strong presence of specialized healthcare facilities.

- North America dominates the regional market with approximately 35% share attributed to its vast aging population, advanced healthcare infrastructure, and increasing lifestyle-related disorders.

What is the Industry Overview of the Private Hospitals Market?

Private hospitals are healthcare facilities that are privately sponsored and managed by individuals or groups outside of government control. These institutions handle their own operations, including funding, compliance, human resources, and equipment procurement. They offer a wide array of services such as intensive medical treatment, mental health care, long-term care, and primary care, primarily funded through private medical insurance policies or out-of-pocket payments. Unlike public hospitals, private ones often cater to patients seeking shorter wait times, specialized treatments, and higher levels of personalized service, making them particularly attractive to affluent individuals. The market encompasses a fragmented landscape, especially in regions with numerous small practices owned by healthcare professionals, and is increasingly becoming more commercialized with variations in size, responsibility, and operational models across different countries.

What are the Market Dynamics in the Private Hospitals Market?

Growth Drivers

The growth of the Private Hospitals market is propelled by a surge in demand for advanced medical services, driven by an expanding elderly population that requires specialized care for age-related ailments. Enhanced reimbursement policies from insurance providers have made private healthcare more accessible, encouraging patients to opt for these facilities over public ones. The rising prevalence of chronic diseases, such as diabetes, cardiovascular conditions, and cancer, necessitates ongoing treatments that private hospitals are well-equipped to provide with state-of-the-art technology. Additionally, large-scale outsourcing of national health services to private entities, coupled with advancements in medical technology and the increasing incidence of infectious diseases, further fuels market expansion by enabling private hospitals to offer efficient, high-quality care that meets evolving patient needs.

Restraints

High service and treatment charges in private hospitals act as a significant restraint, stemming from elevated operational costs including staff salaries, maintenance, and the continuous need to invest in the latest medical equipment and technologies to maintain a competitive edge. These costs are often passed on to patients, limiting accessibility for lower-income groups and potentially deterring widespread adoption. In regions with strong public healthcare systems, the perception of private hospitals as overly expensive can hinder market penetration, especially during economic downturns when patients prioritize affordability over premium services.

Opportunities

Emerging medical tourism presents substantial opportunities for the Private Hospitals market, as patients from developed countries seek cost-effective, high-quality treatments in emerging economies with shorter wait times. The rising demand for diagnostic therapy and specialized care, combined with strategic mergers and acquisitions, allows hospitals to expand their reach and service portfolios. Implementation of cutting-edge technologies like artificial intelligence for computer-aided diagnosis in radiology and nuclear medicine opens avenues for improved efficiency in treating neurological diseases and oncology, positioning private hospitals to capitalize on the shift towards personalized and tech-driven healthcare solutions.

Challenges

The diversity and complexity of the Private Hospitals market pose challenges in achieving universal health coverage, as variations in for-profit and non-profit statuses create conflicts of interest that lack standardized solutions across countries. Differences in ownership models, such as public versus private in primary care, require tailored policy measures to manage diverse players effectively, considering their social aims, ties, behaviors, and capacities. Furthermore, the absence of conceptual clarity on terms like “private sector” and “private sector engagement” complicates research, analysis, policy development, and decision-making, making it difficult to implement cohesive strategies that address the unique needs of this fragmented industry.

Private Hospitals Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Private Hospitals Market |

| Market Size 2025 | USD 1,300 Billion |

| Market Forecast 2035 | USD 4,100 Billion |

| Growth Rate | CAGR of 12.5% |

| Report Pages | 224 |

| Key Companies Covered | Apollo Hospitals Enterprise Ltd., Ramsay Health Care, HCA Healthcare, Fresenius SE & Co. KGaA, Fortis Healthcare Limited, Nuffield Health, Life Healthcare, Spire Healthcare Group Plc., MEOCLINIC GmbH, IASIS Healthcare |

| Segments Covered | By Type, By Hospital Capacity, By Location, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Market Segmentation Structured in the Private Hospitals Market?

The Private Hospitals market is segmented by type, hospital capacity, location, and region.

Based on Type Segment, Acute Care Hospitals emerge as the most dominant subsegment, followed by Multispecialty Hospitals as the second most dominant. Acute Care Hospitals lead due to their widespread availability in both urban and rural settings, enabling quick response to emergencies and contagious diseases, which drives market growth by addressing immediate healthcare demands and attracting a large patient base seeking prompt treatment; Multispecialty Hospitals follow closely, offering a broad range of services under one roof, which enhances patient convenience and operational synergies, contributing to overall market expansion through integrated care models that reduce the need for multiple facility visits.

Based on Hospital Capacity Segment, Medium-sized hospitals (100-500 beds) are the most dominant, with Large-sized hospitals (>500 beds) as the second most dominant. Medium-sized facilities dominate because they represent the majority of private hospitals and clinics, providing a balance between scalability and cost-effectiveness that allows for efficient service delivery and adaptability to market needs, thereby driving growth through optimized resource utilization; Large-sized hospitals, while secondary, contribute significantly by handling complex cases and high-volume patients, fostering market advancement via investments in advanced infrastructure that supports specialized treatments and attracts medical tourism.

Based on Location Segment, Urban areas are the most dominant, followed by Rural areas as the second most dominant. Urban locations lead owing to higher disposable incomes among residents, superior infrastructure, and the concentration of specialized hospitals, which propel market growth by facilitating access to premium healthcare services and encouraging investments in urban expansions; Rural areas, though less dominant, play a crucial role in extending healthcare reach to underserved populations, aiding market development through government incentives and the need to address regional health disparities with basic to intermediate care options.

What are the Recent Developments in the Private Hospitals Market?

- In September 2021, Fortis Hospital launched a specialized Bone Marrow Unit in Central Mumbai, aimed at providing advanced bone marrow transplant services to patients requiring intensive hematological care. This development enhances the hospital’s capabilities in oncology and transplant medicine, positioning it as a key player in specialized treatments and contributing to improved patient outcomes in the region.

- In November 2021, Quirónsalud, a subsidiary of Fresenius Helios, acquired Clínica Clofán and Centro Oncológico de Antioquia (COA) in Colombia, strengthening its presence in Latin America. This strategic acquisition expands Quirónsalud’s oncology services and market footprint, allowing for greater access to high-quality cancer care and fostering growth through international expansion and service integration.

How Does the Regional Analysis Look in the Private Hospitals Market?

- North America to dominate the global market

North America: This region leads the Private Hospitals market due to its large aging population and the high prevalence of lifestyle-related disorders such as obesity and diabetes, which drive demand for specialized care. The United States dominates within North America, supported by advanced healthcare infrastructure, favorable reimbursement policies, and a strong emphasis on private insurance models that encourage utilization of private facilities. Rapid technological adoption and investments in medical innovations further bolster growth, making the region a hub for premium healthcare services.

Asia Pacific: As the fastest-growing region, Asia Pacific is propelled by large patient pools, increasing healthcare awareness, and rising costs that shift demand from overburdened public systems to private ones. India and China dominate, with India’s growth fueled by medical tourism and affordable high-quality care, while China’s expansion is driven by urbanization and government reforms allowing more private investments. Resource shortages in public sectors create opportunities for private hospitals to fill gaps, leading to accelerated market development through expansions and partnerships.

Europe: Europe exhibits steady growth in the Private Hospitals market, supported by a mix of public-private partnerships and demand for shorter wait times in countries like the United Kingdom and Germany. Germany leads the region with its robust healthcare system and emphasis on specialized treatments, while the Nordic countries contribute through innovative care models. Rising chronic diseases and aging demographics drive adoption, with mergers and technological integrations enhancing service quality and market competitiveness.

Latin America: This region experiences moderate growth, driven by improving economic conditions and increasing private insurance penetration in countries like Brazil and Argentina. Brazil dominates due to its large population and investments in healthcare infrastructure, addressing gaps in public services. Medical tourism and acquisitions by international players, such as in Colombia, support expansion, though challenges like economic volatility impact overall progress.

Middle East & Africa: The Middle East & Africa region is emerging, with growth led by investments in healthcare tourism and infrastructure in the UAE and Saudi Arabia. The UAE dominates through its world-class facilities attracting international patients, while South Africa contributes in Africa with advanced private networks. Government initiatives to diversify economies and improve health access propel the market, despite challenges from resource limitations in parts of Africa.

Who are the Key Market Players in the Private Hospitals Market?

Apollo Hospitals Enterprise Ltd.: As a leading player, Apollo focuses on expansion through multispecialty facilities and medical tourism, employing strategies like partnerships and technology integration to enhance service quality and reach a broader patient base in Asia and beyond.

Ramsay Health Care: This company emphasizes global acquisitions and operational efficiency, leveraging its network to provide acute care and specialty services, with strategies centered on cost management and patient-centric innovations to maintain market leadership.

HCA Healthcare: HCA adopts growth through mergers and investments in advanced technologies, focusing on urban acute care hospitals to drive revenue, with strategies including data analytics for improved outcomes and expansion in high-demand regions like North America.

Fresenius SE & Co. KGaA: Through subsidiaries like Quirónsalud, Fresenius pursues international acquisitions to strengthen its oncology and specialty care offerings, employing strategies of market entry into emerging economies and integration of AI for diagnostic advancements.

Fortis Healthcare Limited: Fortis concentrates on specialized units like bone marrow transplants and network expansions in India, with strategies involving collaborations and focus on chronic disease management to capitalize on growing healthcare demands.

Nuffield Health: This non-profit player prioritizes patient care through integrated wellness and hospital services in the UK, using strategies like community partnerships and technology adoption to enhance accessibility and service standards.

Life Healthcare: Operating primarily in Africa, Life Healthcare focuses on capacity building and specialty services, with strategies including sustainable practices and digital health solutions to address regional healthcare challenges.

Spire Healthcare Group Plc.: Spire employs growth via private insurance partnerships and orthopedic specialties in the UK, with strategies centered on quality accreditation and patient experience enhancements to attract affluent clients.

MEOCLINIC GmbH: Based in Germany, MEOCLINIC specializes in premium personalized care, using strategies like international patient services and cutting-edge treatments to position itself in the luxury healthcare segment.

IASIS Healthcare: IASIS focuses on urban hospital management in the US, with strategies involving cost-effective operations and community health programs to sustain growth in competitive markets.

What are the Market Trends in the Private Hospitals Market?

- Increasing utilization of private medical services due to growing demand for faster and specialized care.

- Advent of advanced technologies and treatments, including AI integration in diagnostics and radiology.

- Growth in medical tourism, attracting patients from developed countries to cost-effective destinations.

- Large-scale outsourcing of national health services to private entities for efficiency gains.

- Commercialization and fragmentation with a rise in small, physician-owned practices.

- Emphasis on mergers and acquisitions to expand market presence and service portfolios.

- Shift towards personalized medicine and chronic disease management amid rising healthcare awareness.

What Market Segments and Their Subsegments are Covered in the Private Hospitals Market Report?

By Type

- Acute Care Hospitals

- Children’s Hospitals

- Multispecialty Hospitals

- Specialty Hospitals

- Others

By Hospital Capacity

- Small (<100 beds)

- Medium (100-500 beds)

- Large (>500 beds)

- Others

By Location

- Rural

- Urban

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

1.1 Report Description and Scope1.2 Research Scope1.3 Research Methodology1.3.1 Market Research Type1.3.2 Market Research MethodologyChapter 2. Executive Summary

2.1 Global Private Hospitals Market, (2026 - 2035) (USD Billion)2.2 Global Private Hospitals Market: SnapshotChapter 3. Global Private Hospitals Market - Industry Analysis

3.1 Private Hospitals Market: Market Dynamics3.2 Market Drivers3.2.1 The private hospitals market is driven by rising demand for advanced healthcare from an aging population, better insurance coverage, growing chronic and infectious diseases, outsourcing of public health services, and rapid medical technology advancements.3.3 Market Restraints3.3.1 The private hospitals market is restrained by high treatment costs driven by elevated operational and technology expenses, limiting affordability, accessibility, and adoption, especially during economic downturns.3.4 Market Opportunities3.4.1 The private hospitals market offers strong opportunities through growing medical tourism, rising demand for specialized care, strategic mergers, and adoption of advanced technologies like AI for personalized and efficient healthcare.3.5 Market Challenges3.5.1 The private hospitals market faces challenges from structural diversity, conflicting ownership models, lack of standardization, and unclear definitions, hindering cohesive policy-making and universal health coverage efforts.3.6 Porter’s Five Forces Analysis3.7 Market Attractiveness Analysis3.7.1 Market Attractiveness Analysis By Type3.7.2 Market Attractiveness Analysis By Hospital Capacity3.7.3 Market Attractiveness Analysis By LocationChapter 4. Global Private Hospitals Market- Competitive Landscape

4.1 Company Market Share Analysis4.1.1 Global Private Hospitals Market: Company Market Share, 20254.2 Strategic Development4.2.1 Acquisitions & mergers4.2.2 New Product launches4.2.3 Agreements, partnerships, collaborations, and joint ventures4.2.4 Research and development and regional expansion4.3 Price Trend AnalysisChapter 5. Global Private Hospitals Market - Type Analysis

5.1 Global Private Hospitals Market Overview: Type5.1.1 Global Private Hospitals Market share, By Type, 2025 and 20355.2 Acute Care Hospitals5.2.1 Global Private Hospitals Market by Acute Care Hospitals, 2026 - 2035 (USD Billion)5.3 Children's Hospitals5.3.1 Global Private Hospitals Market by Children's Hospitals, 2026 - 2035 (USD Billion)5.4 Multispecialty Hospitals5.4.1 Global Private Hospitals Market by Multispecialty Hospitals, 2026 - 2035 (USD Billion)5.5 Specialty Hospitals5.5.1 Global Private Hospitals Market by Specialty Hospitals, 2026 - 2035 (USD Billion)5.6 Others5.6.1 Global Private Hospitals Market by Others, 2026 - 2035 (USD Billion)Chapter 6. Global Private Hospitals Market - Hospital Capacity Analysis

6.1 Global Private Hospitals Market Overview: Hospital Capacity6.1.1 Global Private Hospitals Market Share, By Hospital Capacity, 2025 and 20356.2 Small6.2.1 Global Private Hospitals Market by Small, 2026 - 2035 (USD Billion)6.3 Medium6.3.1 Global Private Hospitals Market by Medium, 2026 - 2035 (USD Billion)6.4 Large6.4.1 Global Private Hospitals Market by Large, 2026 - 2035 (USD Billion)6.5 Others6.5.1 Global Private Hospitals Market by Others, 2026 - 2035 (USD Billion)Chapter 7. Global Private Hospitals Market - Location Analysis

7.1 Global Private Hospitals Market Overview: Location7.1.1 Global Private Hospitals Market Share, By Location, 2025 and 20357.2 Rural7.2.1 Global Private Hospitals Market by Rural, 2026 - 2035 (USD Billion)7.3 Urban7.3.1 Global Private Hospitals Market by Urban, 2026 - 2035 (USD Billion)7.4 Others7.4.1 Global Private Hospitals Market by Others, 2026 - 2035 (USD Billion)Chapter 8. Private Hospitals Market - Regional Analysis

8.1 Global Private Hospitals Market Regional Overview8.2 Global Private Hospitals Market Share, by Region, 2025 & 2035 (USD Billion)8.3 North America8.3.1 North America Private Hospitals Market, 2026 - 2035 (USD Billion)8.3.1.1 North America Private Hospitals Market, by Country, 2026 - 2035 (USD Billion)8.3.2 North America Private Hospitals Market, by Type, 2026 - 20358.3.2.1 North America Private Hospitals Market, by Type, 2026 - 2035 (USD Billion)8.3.3 North America Private Hospitals Market, by Hospital Capacity, 2026 - 20358.3.3.1 North America Private Hospitals Market, by Hospital Capacity, 2026 - 2035 (USD Billion)8.3.4 North America Private Hospitals Market, by Location, 2026 - 20358.3.4.1 North America Private Hospitals Market, by Location, 2026 - 2035 (USD Billion)8.4 Europe8.4.1 Europe Private Hospitals Market, 2026 - 2035 (USD Billion)8.4.1.1 Europe Private Hospitals Market, by Country, 2026 - 2035 (USD Billion)8.4.2 Europe Private Hospitals Market, by Type, 2026 - 20358.4.2.1 Europe Private Hospitals Market, by Type, 2026 - 2035 (USD Billion)8.4.3 Europe Private Hospitals Market, by Hospital Capacity, 2026 - 20358.4.3.1 Europe Private Hospitals Market, by Hospital Capacity, 2026 - 2035 (USD Billion)8.4.4 Europe Private Hospitals Market, by Location, 2026 - 20358.4.4.1 Europe Private Hospitals Market, by Location, 2026 - 2035 (USD Billion)8.5 Asia Pacific8.5.1 Asia Pacific Private Hospitals Market, 2026 - 2035 (USD Billion)8.5.1.1 Asia Pacific Private Hospitals Market, by Country, 2026 - 2035 (USD Billion)8.5.2 Asia Pacific Private Hospitals Market, by Type, 2026 - 20358.5.2.1 Asia Pacific Private Hospitals Market, by Type, 2026 - 2035 (USD Billion)8.5.3 Asia Pacific Private Hospitals Market, by Hospital Capacity, 2026 - 20358.5.3.1 Asia Pacific Private Hospitals Market, by Hospital Capacity, 2026 - 2035 (USD Billion)8.5.4 Asia Pacific Private Hospitals Market, by Location, 2026 - 20358.5.4.1 Asia Pacific Private Hospitals Market, by Location, 2026 - 2035 (USD Billion)8.6 Latin America8.6.1 Latin America Private Hospitals Market, 2026 - 2035 (USD Billion)8.6.1.1 Latin America Private Hospitals Market, by Country, 2026 - 2035 (USD Billion)8.6.2 Latin America Private Hospitals Market, by Type, 2026 - 20358.6.2.1 Latin America Private Hospitals Market, by Type, 2026 - 2035 (USD Billion)8.6.3 Latin America Private Hospitals Market, by Hospital Capacity, 2026 - 20358.6.3.1 Latin America Private Hospitals Market, by Hospital Capacity, 2026 - 2035 (USD Billion)8.6.4 Latin America Private Hospitals Market, by Location, 2026 - 20358.6.4.1 Latin America Private Hospitals Market, by Location, 2026 - 2035 (USD Billion)8.7 The Middle-East and Africa8.7.1 The Middle-East and Africa Private Hospitals Market, 2026 - 2035 (USD Billion)8.7.1.1 The Middle-East and Africa Private Hospitals Market, by Country, 2026 - 2035 (USD Billion)8.7.2 The Middle-East and Africa Private Hospitals Market, by Type, 2026 - 20358.7.2.1 The Middle-East and Africa Private Hospitals Market, by Type, 2026 - 2035 (USD Billion)8.7.3 The Middle-East and Africa Private Hospitals Market, by Hospital Capacity, 2026 - 20358.7.3.1 The Middle-East and Africa Private Hospitals Market, by Hospital Capacity, 2026 - 2035 (USD Billion)8.7.4 The Middle-East and Africa Private Hospitals Market, by Location, 2026 - 20358.7.4.1 The Middle-East and Africa Private Hospitals Market, by Location, 2026 - 2035 (USD Billion)Chapter 9. Company Profiles

9.1 Apollo Hospitals Enterprise Ltd.9.1.1 Overview9.1.2 Financials9.1.3 Product Portfolio9.1.4 Business Strategy9.1.5 Recent Developments9.2 Ramsay Health Care9.2.1 Overview9.2.2 Financials9.2.3 Product Portfolio9.2.4 Business Strategy9.2.5 Recent Developments9.3 HCA Healthcare9.3.1 Overview9.3.2 Financials9.3.3 Product Portfolio9.3.4 Business Strategy9.3.5 Recent Developments9.4 Fresenius SE & Co. KGaA9.4.1 Overview9.4.2 Financials9.4.3 Product Portfolio9.4.4 Business Strategy9.4.5 Recent Developments9.5 Fortis Healthcare Limited9.5.1 Overview9.5.2 Financials9.5.3 Product Portfolio9.5.4 Business Strategy9.5.5 Recent Developments9.6 Nuffield Health9.6.1 Overview9.6.2 Financials9.6.3 Product Portfolio9.6.4 Business Strategy9.6.5 Recent Developments9.7 Life Healthcare9.7.1 Overview9.7.2 Financials9.7.3 Product Portfolio9.7.4 Business Strategy9.7.5 Recent Developments9.8 Spire Healthcare Group Plc.9.8.1 Overview9.8.2 Financials9.8.3 Product Portfolio9.8.4 Business Strategy9.8.5 Recent Developments9.9 MEOCLINIC GmbH9.9.1 Overview9.9.2 Financials9.9.3 Product Portfolio9.9.4 Business Strategy9.9.5 Recent Developments9.10 IASIS Healthcare9.10.1 Overview9.10.2 Financials9.10.3 Product Portfolio9.10.4 Business Strategy9.10.5 Recent Developments

Frequently Asked Questions

Private hospitals are privately sponsored healthcare facilities managed and funded by individuals or groups, offering services like intensive medical treatment, mental care, long-term care, and primary care, primarily through private insurance or out-of-pocket payments.

Key factors include an aging population, rising chronic diseases, enhanced reimbursement policies, advancements in medical technology, increasing medical tourism, and the outsourcing of national health services to private providers.

The market is projected to grow from approximately USD 1,300 billion in 2025 to USD 4,100 billion by 2035.

The CAGR is expected to be 12.5% during the forecast period.

North America will contribute notably, holding the largest share due to its advanced infrastructure and high demand for private healthcare.

Major players include Apollo Hospitals Enterprise Ltd., Ramsay Health Care, HCA Healthcare, Fresenius SE & Co. KGaA, Fortis Healthcare Limited, Nuffield Health, Life Healthcare, Spire Healthcare Group Plc., MEOCLINIC GmbH, and IASIS Healthcare.

The report provides comprehensive insights into market size, trends, segmentation, drivers, restraints, opportunities, challenges, regional analysis, key players, and forecasts to aid strategic decision-making.

The value chain includes patient admission and registration, diagnostic and treatment services, surgical and therapeutic interventions, post-care monitoring and rehabilitation, billing and insurance processing, and discharge with follow-up care.

Trends are shifting towards personalized and tech-driven care, with consumers preferring shorter wait times, specialized treatments, and digital health solutions like telemedicine amid growing awareness of preventive healthcare.

Regulatory factors include reimbursement policies, licensing requirements, and data privacy laws like HIPAA, while environmental factors encompass sustainability initiatives, waste management from increased diagnostics, and adaptations to pandemics like COVID-19 through hygiene protocols.