Mobile Payments Market Size, Share and Trends 2026 to 2035

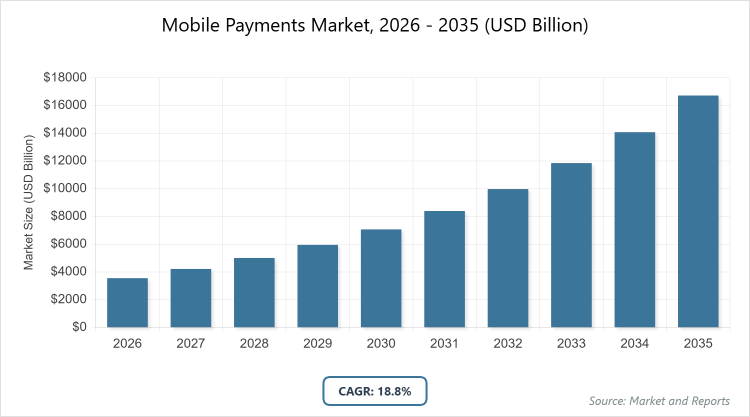

According to MarketnReports, the global mobile payments market size was estimated at USD 3547.37 billion in 2025 and is expected to reach USD 19864.19 billion by 2035, growing at a CAGR of 18.80% from 2026 to 2035. Rising smartphone penetration and e-commerce growth.

What are the Key Insights into the mobile payments market?

- Global mobile payments market size was USD 3547.37 billion in 2025 and is projected to reach USD 19864.19 billion by 2035.

- The market is anticipated to grow at a CAGR of 18.80% from 2026 to 2035.

- The market is driven by increasing smartphone adoption, contactless payment preferences, and fintech advancements.

- The digital wallets segment dominates the type with around 45% share, owing to its convenience, security features, and integration with multiple payment methods for seamless transactions.

- The NFC-based segment leads the mode with approximately 40% market share, due to its speed in contactless payments and widespread adoption in retail POS systems.

- The retail & e-commerce segment is dominant in end-user with about 35% share, as it leverages mobile payments for quick checkouts and personalized shopping experiences.

- Asia Pacific dominates the regional market with around 45% share, driven by high mobile penetration, government digital initiatives, and e-commerce boom in China and India.

What is the Mobile Payments?

Industry Overview

The mobile payments market encompasses digital transactions conducted via mobile devices, including smartphones and tablets, using technologies such as near-field communication (NFC), QR codes, digital wallets, and SMS for secure, convenient payments in retail, online shopping, peer-to-peer transfers, and bill settlements, facilitating cashless economies by integrating with banking systems, merchants, and consumers to reduce friction in financial exchanges. This industry focuses on enhancing user experience through biometric authentication, real-time processing, and integration with loyalty programs, while addressing security concerns with encryption and tokenization.

Market definition includes all platforms, apps, and services enabling mobile-initiated payments, excluding traditional card or cash transactions, and it highlights the role of fintech innovations in promoting financial inclusion and efficiency amid digital transformation.

What are the Market Dynamics Affecting Mobile Payments?

Growth Drivers

The growth drivers in the mobile payments market are significantly influenced by the proliferation of smartphones and high-speed internet, enabling seamless, on-the-go transactions that cater to consumer demands for convenience in daily purchases, with global smartphone users exceeding 6.8 billion in 2023, fostering adoption in e-commerce and P2P transfers. This is amplified by fintech innovations like biometric authentication and AI-driven fraud detection, which enhance security and trust, encouraging broader usage in emerging markets where banking access is limited. Additionally, government policies promoting digital economies, such as India’s UPI and China’s WeChat Pay, accelerate market expansion by reducing cash dependency and supporting financial inclusion through low-cost, instant payments.

Restraints

Restraints in the mobile payments market include cybersecurity threats and data breaches, which erode consumer confidence, with incidents like the 2023 MOVEit hack exposing vulnerabilities and leading to regulatory scrutiny that increases compliance costs for providers. Limited interoperability between platforms and banks in fragmented markets also hinders growth, as users face challenges in cross-border or multi-app transactions. Moreover, infrastructure gaps in rural areas, such as poor internet connectivity, restrict adoption in developing regions, exacerbating digital divides.

Opportunities

Opportunities in the mobile payments market stem from the integration of blockchain and cryptocurrencies for secure, borderless transactions, appealing to tech-savvy users and enabling low-fee remittances in high-migration corridors like Asia to Europe. The rise of embedded finance in apps like ride-sharing or social media offers avenues for seamless in-app payments, expanding reach to unbanked populations. Furthermore, partnerships with retailers for loyalty-linked payments can drive innovation, while AI personalization enhances user engagement, creating premium service models.

Challenges

Challenges in the mobile payments market involve regulatory inconsistencies across regions, requiring providers to navigate diverse compliance frameworks like PSD2 in Europe and PCI DSS globally, which can delay expansions and increase operational complexities. Fraudulent activities, such as SIM swapping, pose ongoing risks, demanding continuous investment in advanced security measures. Additionally, consumer privacy concerns amid data collection for personalization create trust issues, potentially slowing adoption if not addressed through transparent practices.

Mobile Payments Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Mobile Payments Market |

| Market Size 2025 | USD 3547.37 Billion |

| Market Forecast 2035 | USD 19864.19 Billion |

| Growth Rate | CAGR of 18.80% |

| Report Pages | 220 |

| Key Companies Covered |

Alphabet (Google Pay), Apple Inc., Samsung Electronics (Samsung Pay), PayPal Holdings, Amazon Pay, and Others |

| Segments Covered | By Type, By Mode, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Mobile Payments Market Segmented?

The Mobile Payments market is segmented by type, mode, end-user, and region.

Based on Type Segment, the digital wallets subsegment is the most dominant, holding around 45% share, due to its user-friendly interface, storage of multiple cards, and features like rewards tracking, which drives the market by simplifying transactions and encouraging repeat usage in e-commerce. The NFC-based subsegment is the second most dominant, with approximately 30% share, as it enables quick tap-and-pay at POS terminals, contributing to market growth by promoting contactless habits post-pandemic.

Based on Mode Segment, the NFC-based subsegment is the most dominant, capturing about 40% share, attributed to its speed and security for in-store payments, which propels the market by integrating with wearables and reducing checkout times. The QR code-based subsegment is the second most dominant, with around 25% share, owing to its low-cost implementation in emerging markets, helping to drive the market through accessibility for small merchants.

Based on End-User Segment, the retail & e-commerce subsegment is the most dominant, with roughly 35% share, facilitated by seamless online and in-app purchases, driving the market by meeting consumer demands for fast delivery and personalized offers. The BFSI subsegment is the second most dominant, holding about 25% share, propelled by mobile banking apps, which contribute to market expansion by enhancing financial services accessibility.

What are the Recent Developments in the Mobile Payments Market?

- In September 2025, McKinsey released its Global Payments Report, highlighting AI and digital assets as key drivers for mobile payments evolution.

- In December 2025, Mastercard predicted dynamic, customizable payment tools for 2026, focusing on personalized spending behaviors.

- In November 2025, G+D Spotlight identified instant payments and hyper-personalized cards as major trends shaping 2025.

- In September 2025, Decta outlined innovations like CBDCs and embedded payments for 2025.

How Does Regional Analysis Impact Mobile Payments Market?

- Asia Pacific to dominate the global market.

Asia Pacific dominates the mobile payments market with the largest share, fueled by high smartphone penetration and government-backed digital initiatives; China stands as the dominating country, where platforms like Alipay and WeChat Pay handle trillions in transactions annually, driving growth through widespread adoption in daily commerce and financial inclusion.

North America maintains a strong position, supported by advanced fintech ecosystems and consumer preferences for contactless payments; the United States dominates this region, with Apple Pay and Google Pay leading, contributing to expansion via e-commerce integration and security features.

Europe exhibits steady growth, influenced by regulatory frameworks like PSD2 promoting open banking; Germany is the dominating country, leveraging strong infrastructure for SEPA instant payments, supporting market progress through cross-border efficiency.

Latin America shows emerging potential, boosted by mobile banking for unbanked populations; Brazil dominates here, with Pix system revolutionizing real-time transfers, aiding development via financial accessibility.

The Middle East and Africa represent nascent opportunities, driven by mobile money services; Kenya dominates in this region, with M-Pesa pioneering peer-to-peer payments, propelling growth through inclusion in rural areas.

Who are the Key Market Players in Mobile Payments?

- Alphabet (Google Pay) focuses on Android integration for seamless NFC payments, employing strategies like partnerships with banks and AI for fraud detection to expand in emerging markets.

- Apple Inc. specializes in secure wallet ecosystems with Apple Pay, utilizing hardware encryption and ecosystem lock-in for user loyalty and global retail acceptance.

- Samsung Electronics (Samsung Pay) targets wearable compatibility, adopting magnetic secure transmission for broader POS use and collaborations for rewards programs.

- PayPal Holdings offers versatile P2P and merchant solutions, with strategies involving Venmo acquisitions and cryptocurrency integration for cross-border transactions.

- Amazon Pay emphasizes e-commerce synergies, employing one-click payments and voice-activated features via Alexa to enhance customer retention.

What are the Market Trends Shaping Mobile Payments?

- Rise of instant and real-time payments for seamless transactions.

- Integration of AI for personalized financial tools and fraud prevention.

- Growth in embedded and invisible payments within apps.

- Expansion of CBDCs and tokenized deposits for secure digital currencies.

- Adoption of biometric and voice-activated authentication methods.

- Focus on hyper-personalized and dynamic payment experiences.

- Increase in cross-border interoperability through global rails.

What Market Segments and Subsegments are Covered in the Mobile Payments Report?

By Type

- Proximity Payments

- Remote Payments

- NFC-based

- QR Code-based

- SMS-based

- USSD-based

- Digital Wallets

- P2P Transfers

- Mobile POS

- In-App Payments

- Others

By Mode

- Mobile Web Payments

- Near-Field Communication

- SMS/Direct Carrier Billing

- Digital Wallets

- Contactless Cards

- Biometric Payments

- Voice-Activated Payments

- Wearable Payments

- Blockchain-based

- AI-Integrated

- Others

By End-User

- BFSI

- Retail & E-commerce

- Healthcare

- Media & Entertainment

- IT & Telecom

- Hospitality & Tourism

- Transportation

- Energy & Utilities

- Education

- Government

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Mobile Payments Market - Industry Analysis

Chapter 4. Global Mobile Payments Market- Competitive Landscape

Chapter 5. Global Mobile Payments Market - Type Analysis

Chapter 6. Global Mobile Payments Market - Mode Analysis

Chapter 7. Global Mobile Payments Market - End-User Analysis

Chapter 8. Mobile Payments Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Mobile payments are digital transactions conducted via mobile devices like smartphones, using technologies such as NFC or digital wallets for secure, convenient financial exchanges.

Key factors include smartphone proliferation, fintech innovations, regulatory support for digital economies, and e-commerce expansion.

The mobile payments market is projected to grow from approximately USD 4700 billion in 2026 to USD 19864.19 billion by 2035.

The CAGR value is expected to be 18.80% during 2026-2035.

Asia Pacific will contribute notably, driven by high adoption in China and India.

Major players include Alphabet (Google Pay), Apple Inc., Samsung Electronics (Samsung Pay), PayPal Holdings, and Amazon Pay.

The report provides comprehensive analysis on market size, trends, segments, regional insights, key players, and forecasts from 2026 to 2035.

Stages include technology development, platform integration, merchant onboarding, transaction processing, security compliance, and consumer adoption.

Trends are evolving toward instant, personalized payments with AI, while consumers prefer secure, contactless options integrated into daily apps.

Regulatory factors include data protection laws like GDPR, while environmental factors involve sustainable digital infrastructures reducing paper-based transactions.