Battery Manufacturing Equipment Market Size, Share and Trends 2026 to 2035

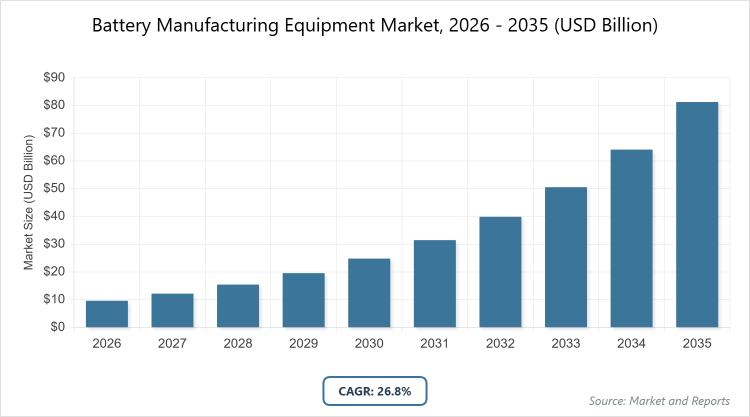

According to MarketnReports, the global Battery Manufacturing Equipment Market size was estimated at USD 9.59 billion in 2025 and is expected to reach USD 103.04 billion by 2035, growing at a CAGR of 26.8% from 2026 to 2035. Battery Manufacturing Equipment Market is driven by the surging demand for electric vehicles and renewable energy storage solutions.What are the Key Insights into the Battery Manufacturing Equipment Market?

- The global battery manufacturing equipment market was valued at USD 9.59 billion in 2025 and is projected to reach USD 103.04 billion by 2035.

- The market is expected to grow at a CAGR of 26.8% from 2026 to 2035.

- The market is driven by rising electric vehicle adoption, expanding renewable energy storage, and advancements in battery technologies.

- Coating machines dominate the machine type segment with approximately 25% share due to their essential role in electrode preparation for high-capacity batteries.

- Lithium-ion batteries lead the battery type segment with around 43% share owing to their widespread use in EVs and electronics.

- Automotive batteries represent the dominant application with about 50% share attributed to the booming EV industry.

- Battery manufacturers hold the largest end-user share at roughly 60% as they scale up production for gigafactories.

- Asia-Pacific commands the largest regional share at about 65% thanks to manufacturing hubs in China, government incentives, and supply chain dominance.

What is the Industry Overview of the Battery Manufacturing Equipment Market?

The battery manufacturing equipment market involves machinery and systems used in the production of various battery types, from mixing raw materials to final assembly and testing, ensuring efficiency, quality, and scalability in battery fabrication. Market definition encompasses the global industry dedicated to designing, producing, and supplying equipment such as coaters, mixers, calendars, and slitters, which are critical for manufacturing lithium-ion, lead-acid, and emerging battery technologies. This market caters to the growing need for high-performance batteries in electric vehicles, consumer electronics, and energy storage, while incorporating automation, precision engineering, and sustainable practices to meet environmental standards and optimize production costs amid the transition to clean energy.

What are the Market Dynamics of the Battery Manufacturing Equipment Market?

Growth Drivers

The battery manufacturing equipment market is accelerating due to the global shift toward electrification, particularly in transportation, where electric vehicle production demands high-volume, precise equipment for lithium-ion cell assembly. Government policies promoting clean energy, such as subsidies for EV manufacturing and renewable integration, are spurring investments in gigafactories, thereby increasing the need for advanced machinery like automated coaters and calendars that enhance yield and reduce defects. Technological innovations, including AI-driven quality control and modular production lines, are improving efficiency and enabling faster scaling, while the rising demand for energy storage systems to support grid stability further amplifies equipment requirements. Additionally, collaborations between equipment suppliers and battery makers are fostering customized solutions, driving overall market growth through optimized processes and cost reductions.

Restraints

Market expansion is constrained by high initial capital costs for sophisticated equipment, which can deter small-scale manufacturers and slow adoption in emerging economies with limited funding. Supply chain disruptions for critical components like precision robotics and specialized materials exacerbate delays and inflate prices, particularly amid geopolitical tensions affecting rare earth supplies. Regulatory complexities around environmental compliance and safety standards for battery production add layers of approval processes, increasing time-to-market for new equipment. Moreover, the rapid evolution of battery chemistries, such as from lithium-ion to solid-state, requires frequent equipment upgrades, posing obsolescence risks and financial burdens for operators.

Opportunities

Opportunities emerge from the development of next-generation equipment tailored for emerging battery technologies like solid-state and sodium-ion, which promise higher energy densities and safer profiles, attracting R&D investments. Expanding markets in regions like Latin America and Africa offer potential through infrastructure development and off-grid energy needs, creating demand for affordable, adaptable manufacturing lines. Strategic partnerships with AI and IoT firms can lead to smart factories that predict maintenance and optimize energy use, enhancing competitiveness. Furthermore, sustainability-focused innovations, such as equipment for battery recycling integration, align with circular economy goals and open new revenue streams amid growing e-waste regulations.

Challenges

Challenges include addressing skilled labor shortages for operating and maintaining complex automated systems, necessitating extensive training programs that raise operational costs. Intense competition from low-cost Asian manufacturers pressures pricing and margins for global players, while intellectual property concerns in technology sharing hinder collaborations. Environmental impacts from equipment production, such as high energy consumption during manufacturing, require greener designs to meet ESG criteria. Additionally, fluctuating raw material prices for equipment components like steel and electronics create budgeting uncertainties, complicating long-term planning in a volatile market.

| Report Attributes | Report Details |

| Report Name | Battery Manufacturing Equipment Market |

| Market Size 2025 | USD 9.59 Billion |

| Market Forecast 2035 | USD 103.04 Billion |

| Growth Rate | CAGR of 26.8% |

| Report Pages | 220 |

| Key Companies Covered |

Wuxi Lead Intelligent Equipment Co., Ltd., Dürr Group, Sovema Group, Schuler Group, Manz AG, and Others. |

| Segments Covered | By Machine Type, By Battery Type, By Application, By End-User, and By Region. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 - 2024 |

| Forecast Year | 2026 - 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Market Segmentation of the Battery Manufacturing Equipment Market?

The Battery Manufacturing Equipment Market is segmented by machine type, battery type, application, end-user, and region.By Machine Type Segment: The coating machines segment is the most dominant, holding approximately 25% market share, followed by mixing machines as the second most dominant. Coating machines dominate due to their critical function in applying uniform electrode layers essential for battery performance and capacity, driving the market by enabling high-throughput production for EV batteries; mixing machines follow, ensuring homogeneous material blends that prevent defects, contributing to overall growth through improved cell quality and efficiency in large-scale operations.

By Battery Type Segment: Lithium-ion batteries lead as the most dominant segment with around 43% share, with lead-acid batteries as the second most dominant. Lithium-ion's dominance stems from its high energy density and versatility in EVs and renewables, propelling market growth via demand for specialized equipment; lead-acid batteries support this by serving cost-sensitive applications like industrial backups, maintaining steady equipment needs and aiding diversification.

By Application Segment: Automotive batteries represent the most dominant with about 50% share, while energy storage systems are the second most dominant. Automotive dominates owing to the EV boom requiring scalable production lines, fueling market expansion through investments in gigafactories; energy storage contributes by addressing grid needs, increasing equipment demand for large-format cells and supporting sustainable energy transitions.

By End-User Segment: Battery manufacturers are the most dominant end-user with roughly 60% share, whereas automotive OEMs are the second most dominant. Battery manufacturers lead due to their focus on vertical integration and capacity expansion, driving market growth via bulk equipment procurement; automotive OEMs aid by integrating in-house production, enhancing supply chain control and accelerating innovation in battery tech.

What are the Recent Developments in the Battery Manufacturing Equipment Market?

- In September 2025, Dürr Group expanded its portfolio with the acquisition of BBS Automation, enhancing its capabilities in automated assembly lines for battery modules and packs.

- In November 2025, Wuxi Lead Intelligent Equipment launched a new high-speed coating machine designed for solid-state batteries, improving efficiency by 20% for next-gen EV production.

- In October 2025, Sovema Group partnered with a major Chinese gigafactory to supply advanced electrode stacking equipment, supporting a 50 GWh annual capacity increase.

- In December 2025, Schuler Group introduced AI-integrated calendaring machines that reduce material waste by 15%, targeting sustainable manufacturing practices.

- In August 2025, Manz AG received a major order from a European EV manufacturer for formation and testing equipment, valued at over EUR 100 million.

How is the Regional Analysis of the Battery Manufacturing Equipment Market?

Asia-Pacific to dominate the global market.Asia-Pacific dominates the battery manufacturing equipment market, driven by massive investments in gigafactories and supportive policies for clean energy; China leads the region with over 70% share, bolstered by its control over the lithium-ion supply chain, government subsidies like the Made in China 2025 initiative, and home to major producers scaling to meet global EV demand.

North America exhibits strong growth, fueled by onshoring efforts and incentives from the Inflation Reduction Act; the United States dominates, with initiatives like battery manufacturing tax credits and partnerships with firms like Tesla, enabling rapid capacity builds in states like Nevada and Texas.

Europe focuses on sustainable production and regulatory compliance under the EU Battery Regulation; Germany holds prominence, supported by automotive giants like Volkswagen investing in local gigafactories and R&D for advanced equipment to reduce import dependency.

Latin America shows emerging potential through resource-rich lithium reserves; Chile leads, leveraging mining partnerships and export-oriented manufacturing to supply equipment for regional battery production amid growing EV adoption in Brazil.

The Middle East and Africa offer niche opportunities via renewable energy projects; South Africa dominates, driven by its mining sector and initiatives for local battery assembly to support solar storage, with UAE contributing through diversification into clean tech hubs.

Who are the Key Market Players in the Battery Manufacturing Equipment Market?

Wuxi Lead Intelligent Equipment Co., Ltd. Wuxi Lead Intelligent Equipment Co., Ltd. employs strategies centered on R&D for high-speed production lines and global expansions, such as customizing equipment for lithium-ion gigafactories, to capture EV-driven demand and enhance market leadership.

Dürr Group. Dürr Group focuses on acquisitions like BBS Automation and sustainable tech integrations, aiming to optimize assembly processes and support eco-friendly battery manufacturing for automotive clients.

Sovema Group. Sovema Group pursues partnerships with gigafactories and innovations in electrode processing, strengthening its position in lead-acid and lithium segments through efficient, scalable solutions.

Schuler Group. Schuler Group leverages AI and automation in pressing and forming equipment, targeting waste reduction and precision to drive growth in high-volume EV battery production.

Manz AG. Manz AG adopts modular designs and contract manufacturing strategies, securing large orders for CIGS and lithium equipment to expand in renewables and electronics applications.

What are the Market Trends in the Battery Manufacturing Equipment Market?

- Increasing adoption of AI and IoT for predictive maintenance and quality control in production lines.

- Shift toward modular and flexible equipment to accommodate diverse battery chemistries like solid-state.

- Growing emphasis on sustainable manufacturing with energy-efficient and low-waste machinery.

- Expansion of gigafactories driving demand for high-throughput automated systems.

- Integration of robotics for precision assembly and handling to reduce human error.

- Rise in recycling-compatible equipment to support circular economy initiatives.

- Preference for localized supply chains to mitigate geopolitical risks.

What Market Segments and their Subsegments are Covered in the Battery Manufacturing Equipment Market Report?

By Machine Type- Mixing Machines

- Coating Machines

- Calendaring Machines

- Slitting Machines

- Electrode Stacking Machines

- Assembly Machines

- Formation Machines

- Testing Machines

- Drying Machines

- Laminating Machines

- Others

- Lithium-Ion Batteries

- Lead-Acid Batteries

- Nickel-Metal Hydride Batteries

- Nickel-Cadmium Batteries

- Flow Batteries

- Lithium Iron Phosphate Batteries

- Nickel Cobalt Aluminum Batteries

- Nickel Manganese Cobalt Batteries

- Solid-State Batteries

- Sodium-Ion Batteries

- Others

- Automotive Batteries

- Industrial Batteries

- Portable Batteries

- Energy Storage Systems

- Consumer Electronics

- Renewable Energy

- Medical Devices

- Marine Applications

- Aerospace

- Telecommunications

- Others

- Battery Manufacturers

- Automotive OEMs

- Electronics Companies

- Energy Companies

- Research Institutions

- Gigafactories

- Recycling Facilities

- Startups

- Government Labs

- Universities

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

The battery manufacturing equipment market comprises machinery used for producing batteries, including mixing, coating, assembly, and testing systems.

Key factors include EV proliferation, renewable energy expansion, technological advancements, and government incentives for clean tech.

The market is expected to grow from approximately USD 11.9 billion in 2026 to USD 103.04 billion by 2035.

The CAGR is projected to be 26.8% during the forecast period.

Asia-Pacific will contribute notably, led by manufacturing dominance and policy support.

Major players include Wuxi Lead Intelligent Equipment Co., Ltd., Dürr Group, Sovema Group, Schuler Group, and Manz AG.

The report offers detailed analysis on size, trends, segments, regions, key players, and forecasts.

Stages include raw material sourcing, equipment design, manufacturing, distribution, installation, and after-sales service.

Trends favor automation and sustainability, with preferences shifting to flexible systems for advanced batteries.

Stringent emissions regulations and ESG requirements are pushing for eco-friendly, efficient equipment designs.