Home Healthcare Market Size, Share and Trends 2026 to 2035

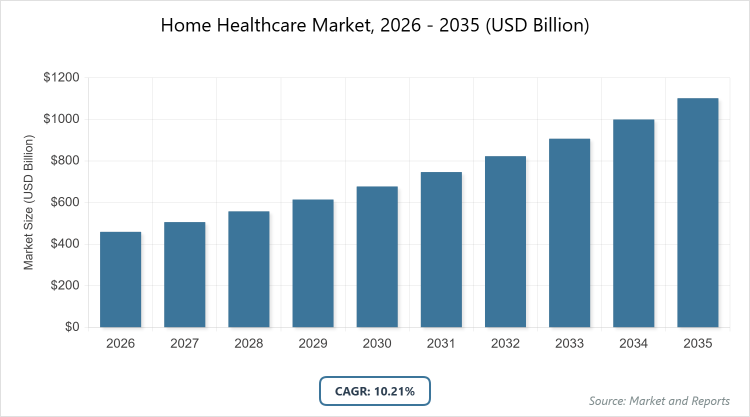

According to MarketnReports, the global Home Healthcare market size was estimated at USD 459.29 billion in 2025 and is expected to reach USD 1216 billion by 2035, growing at a CAGR of 10.21% from 2026 to 2035. Home Healthcare Market is driven by the increasing aging population and technological advancements in remote monitoring.

What are the Key Insights into the Home Healthcare Market?

- The global home healthcare market was valued at USD 459.29 billion in 2025 and is projected to reach USD 1216 billion by 2035.

- The market is anticipated to grow at a CAGR of 10.21% during the forecast period from 2026 to 2035.

- The home healthcare market is driven by the rising prevalence of chronic diseases, an aging global population, and advancements in telemedicine and remote patient monitoring technologies.

- The services subsegment dominates the component segment with an 84.1% share, primarily because of the growing demand for skilled nursing and therapeutic care that supports aging populations and chronic condition management.

- The neurological & mental disorders subsegment leads the indication segment with a 16.75% share, owing to the high incidence of conditions such as Alzheimer’s disease and the need for specialized home-based care for cognitive and neurological impairments.

- North America holds the dominant regional share of 42.47%, attributed to its advanced healthcare infrastructure, high disposable incomes, and supportive government initiatives like FDA programs promoting home-based care.

What is the Home Healthcare Industry Overview?

The home healthcare market refers to a broad spectrum of medical services and equipment delivered directly to patients in their homes, offering a viable and economical substitute for traditional hospital or clinic-based treatments. This sector includes professional nursing care, physical and occupational therapies, diagnostic testing, and the use of specialized medical devices for ongoing health management. By focusing on patient comfort and convenience, home healthcare addresses the needs of individuals with chronic illnesses, post-surgical recovery requirements, or disabilities that limit mobility, ultimately promoting independence and reducing the burden on institutional healthcare facilities. The market definition encompasses both skilled medical interventions and supportive aids that enable effective treatment outside clinical settings, driven by the goal of enhancing quality of life while controlling escalating healthcare expenses.

What are the Market Dynamics in the Home Healthcare Industry?

Growth Drivers

The growth of the home healthcare market is propelled by several key factors, including the escalating global aging population, which increases the demand for convenient and personalized care options at home. Technological innovations, such as telemedicine platforms and wearable monitoring devices, enable real-time health tracking and reduce the need for frequent hospital visits, thereby enhancing patient outcomes and accessibility. Additionally, the rising prevalence of chronic diseases like diabetes, cardiovascular conditions, and respiratory disorders necessitates ongoing management that home healthcare efficiently provides, often at a lower cost than institutional care. Government policies and initiatives, such as reimbursements for home services and programs aimed at decongesting hospitals, further accelerate market expansion by making these services more financially viable for patients and providers alike.

Restraints

Despite its potential, the home healthcare market faces restraints primarily related to stringent regulatory requirements and compliance standards, which vary across regions and can complicate service delivery and equipment usage. High initial costs associated with advanced medical devices and technology integration pose barriers, especially in developing economies where affordability remains a challenge for both providers and patients. Moreover, a shortage of trained healthcare professionals skilled in home-based care can limit service availability and quality, leading to inconsistencies in patient experiences. Fragmented reimbursement policies and insurance coverage gaps also hinder widespread adoption, as they create financial uncertainties for stakeholders involved in the market.

Opportunities

Opportunities in the home healthcare market abound, particularly in emerging economies where underdeveloped hospital infrastructure and rising chronic disease burdens create demand for scalable home-based solutions. Innovations in portable diagnostics and AI-driven monitoring tools offer avenues for product development and market penetration, allowing companies to cater to underserved populations. Partnerships between technology firms and healthcare providers can foster integrated ecosystems, such as telehealth networks, expanding service reach. Additionally, the post-pandemic emphasis on reducing hospital admissions opens doors for “hospital-at-home” models, which can significantly cut costs and improve patient satisfaction, presenting lucrative prospects for investment and expansion.

Challenges

The home healthcare market encounters challenges stemming from its fragmented nature, with numerous local and multinational players intensifying competition and pressuring profit margins. Ensuring consistent quality of care across diverse geographic and socioeconomic settings is difficult, often requiring extensive training and certification programs for caregivers. Data privacy and security concerns arise with the increased use of digital health tools, necessitating robust cybersecurity measures to protect sensitive patient information. Furthermore, adapting to evolving patient needs amid rapid technological changes demands continuous innovation, which can strain resources for smaller providers in the market.

Home Healthcare Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Home Healthcare Market |

| Market Size 2025 | USD 459.29 Billion |

| Market Forecast 2035 | USD 1216 Billion |

| Growth Rate | CAGR of 10.21% |

| Report Pages | 221 |

| Key Companies Covered | B. Braun Melsungen AG, Abbott, Medtronic PLC, Koninklijke Philips N.V., Johnson & Johnson Services Inc., Amedisys Inc., Kindred Healthcare Inc., Brookdale Senior Living Solutions, Home Instead Inc., Genesis Healthcare Inc., and Others |

| Segments Covered | By Component, By Indication, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Home Healthcare Market Segmented?

The Home Healthcare market is segmented by component, indication, and region.

Based on Component Segment. The services subsegment is the most dominant with an 84.1% share, followed by the equipment subsegment as the second most dominant. The dominance of services stems from the essential role they play in delivering skilled nursing, therapy, and palliative care directly to patients’ homes, which is increasingly vital for managing chronic conditions and supporting the elderly population; this segment drives the market by reducing hospital readmissions and healthcare costs through personalized, ongoing support, while the equipment subsegment contributes by providing necessary tools like diagnostic monitors and mobility aids that complement services, fostering overall market growth through technological integration and improved patient independence.

Based on Indication Segment. The neurological & mental disorders subsegment is the most dominant with a 16.75% share, followed by the mobility disorders subsegment as the second most dominant due to its fastest growth rate. Neurological & mental disorders lead because of the surging prevalence of conditions like Alzheimer’s and Parkinson’s, which require specialized home care for cognitive support and daily assistance, driving the market by addressing the needs of an aging demographic and reducing institutional care burdens; mobility disorders, as the second dominant, help propel the market through demand for assistive devices and therapies that enhance quality of life for individuals with physical limitations, spurred by increasing awareness and advancements in rehabilitation technologies.

What are the Recent Developments in the Home Healthcare Market?

- In August 2024, Vivid Health entered the at-home care space to assist with assessment forms, aiming to reduce staff burnout and improve efficiency in home healthcare operations.

- In July 2024, Star Health expanded its home healthcare services to over 50 cities in India, enhancing accessibility for patients requiring ongoing medical support.

- In April 2024, the U.S. FDA launched the “Home as a Health Care Hub” initiative to promote health equity through home-based medical solutions.

- In April 2025, Aster DM Healthcare invested USD 163.9 million in India and merged with Quality Care India Ltd., strengthening its home healthcare footprint.

- In March 2023, Cue Health expanded its Cue Care platform with at-home diagnostic tests, facilitating easier remote health monitoring.

- In October 2023, Elara Caring acquired American Family Home Health, expanding its service portfolio in the U.S. market.

- In September 2023, Merago partnered with Portea Medical to offer comprehensive home healthcare services in India.

- In August 2024, LG partnered with Amwell to launch the Carepoint TV Kit, integrating telehealth into home environments.

- In January 2023, Omron Healthcare launched the Viso app in the UK for managing chronic conditions at home.

- In November 2023, the CSA BrainHealth program opened in Germany, focusing on home-based care for neurological health.

What is the Regional Analysis of the Home Healthcare Market?

- North America to dominate the global market.

North America holds the largest market share, driven by its robust healthcare infrastructure, high prevalence of chronic diseases, and favorable reimbursement policies; the dominating country is the United States, where initiatives like the FDA’s “Home as a Health Care Hub” and a large geriatric population fuel demand for home-based services and equipment, contributing to reduced healthcare costs and improved patient outcomes.

Europe exhibits steady growth, supported by increasing cardiovascular disease burdens and technological integrations; Germany dominates the region with programs like CSA BrainHealth and a focus on innovative home monitoring solutions, while the UK advances through apps like Omron Viso, addressing chronic condition management amid aging demographics.

Asia Pacific is the fastest-growing region, attributed to underdeveloped hospital systems, rising chronic diseases, and a burgeoning elderly population; China and Japan lead, with Japan emphasizing advanced technologies from companies like Medtronic and Panasonic, and China benefiting from rapid urbanization and government efforts to expand home care accessibility.

Latin America shows promising expansion due to shifts from family caregiving to professional services and post-COVID adaptations; Brazil dominates with government initiatives such as the National Development Strategy for Health Economic-Industrial Complex, promoting home healthcare to alleviate public system pressures.

The Middle East and Africa region is emerging, propelled by chronic disease prevalence and aging populations; South Africa leads with expansions by providers like Life Healthcare, focusing on managing conditions like diabetes and hypertension through home-based interventions.

Who are the Key Market Players in the Home Healthcare Industry?

B. Braun Melsungen AG focuses on providing healthcare solutions for emergency and surgical care, emphasizing innovation in medical devices and expanding its portfolio through strategic partnerships to enhance home infusion and therapy offerings.

Abbott leverages its expertise in diagnostics and monitoring equipment, investing in R&D for portable devices like blood glucose monitors, and pursuing acquisitions to strengthen its presence in the home healthcare equipment segment.

Medtronic PLC drives growth through advanced remote monitoring technologies and insulin delivery systems, adopting strategies like product launches and collaborations to address chronic disease management in home settings.

Koninklijke Philips N.V. emphasizes telemedicine and respiratory equipment, utilizing digital health platforms and M&A activities to expand geographical reach and integrate AI for personalized home care solutions.

Johnson & Johnson Services Inc. concentrates on wound care and mobility aids, employing innovation and supply chain optimizations to meet the demands of home-based rehabilitation and daily living assistance.

Amedisys Inc. specializes in skilled nursing and hospice services, focusing on acquisitions and service expansions to cover more regions and improve patient-centric care delivery.

Kindred Healthcare Inc. operates extensive home health and hospice networks, strategizing through partnerships and technology adoption to enhance operational efficiency and patient outcomes.

Brookdale Senior Living Solutions targets elderly care with assisted living integrations, using expansion strategies and staff training programs to dominate the senior home healthcare market.

Home Instead Inc. provides non-medical home care services, emphasizing franchise growth and caregiver training to address daily living needs and companionship for aging populations.

Genesis Healthcare Inc. focuses on post-acute and long-term care, implementing cost-control measures and digital tools to optimize home healthcare services across its facilities.

What are the Market Trends in Home Healthcare?

- Increasing adoption of telemedicine and remote patient monitoring technologies to enable real-time health tracking and reduce hospital visits.

- Shift towards cost-effective “hospital-at-home” models post-COVID, emphasizing patient comfort and lower readmission rates.

- Rising focus on personalized care solutions driven by AI and smart sensors for chronic disease management.

- Expansion of services in emerging markets with emphasis on elderly care and rehabilitation amid aging demographics.

- Integration of digital health apps for chronic condition monitoring, such as those for diabetes and cardiovascular diseases.

- Growing partnerships between tech companies and healthcare providers to innovate home-based diagnostic tools.

- Emphasis on data privacy and cybersecurity in digital home healthcare platforms to protect patient information.

- Surge in demand for mobility aids and assistive devices to support independent living for individuals with disabilities.

- Government initiatives promoting home care to alleviate public health system burdens and control expenditures.

- Trend towards sustainable and portable medical equipment to enhance accessibility in underserved regions.

What Market Segments and Subsegments are Covered in the Home Healthcare Report?

By Component

-

Services

-

Skilled

- Physician Primary Care

- Nursing

- Physical/Occupational/Speech Therapy

- Nutritional Support

- Infusion Therapy

- Hospice & Palliative Care

- Others

-

Unskilled Home Healthcare Services

-

-

Equipment

-

Therapeutic

- Home Respiratory Therapy Equipment

- Insulin Delivery Devices

- Home IV Pumps

- Home Dialysis Equipment

- Others

-

Diagnostic

- Diabetic Care Unit

- BP Monitors

- Multi-Para Diagnostic Monitors

- Home Pregnancy and Fertility Kits

- Apnea and Sleep Monitors

- Holter Monitors

- Heart Rate Monitors

- Others

-

Mobility Assist

- Wheelchair

- Home Medical Furniture

- Walking Assist Devices

-

By Indication

- Neurological & Mental Disorders

- Cardiovascular Disorder & Hypertension

- Diabetes & Kidney Disorders

- Respiratory Disease & COPD

- Maternal Disorders

- Mobility Disorders

- Cancer

- Wound Care

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

1.1 Report Description and Scope1.2 Research Scope1.3 Research Methodology1.3.1 Market Research Type1.3.2 Market Research MethodologyChapter 2. Executive Summary

2.1 Global Home Healthcare Market, (2026 - 2035) (USD Billion)2.2 Global Home Healthcare Market: SnapshotChapter 3. Global Home Healthcare Market - Industry Analysis

3.1 Home Healthcare Market: Market Dynamics3.2 Market Drivers3.2.1 The home healthcare market is driven by an aging population, rising chronic diseases, technological advancements like telemedicine and wearables, cost-effective home care, and supportive government reimbursement policies.3.3 Market Restraints3.3.1 The home healthcare market is restrained by complex regulatory requirements, high technology costs, workforce shortages, and fragmented reimbursement and insurance coverage across regions.3.4 Market Opportunities3.4.1 Opportunities in the home healthcare market are driven by demand in emerging economies, innovations in portable diagnostics and AI monitoring, tech–provider partnerships, and growth of hospital-at-home models post-pandemic.3.5 Market Challenges3.5.1 The home healthcare market faces challenges from intense competition and fragmentation, quality consistency issues, data privacy and cybersecurity risks, and the need for continuous innovation amid rapid technological change.3.6 Porter’s Five Forces Analysis3.7 Market Attractiveness Analysis3.7.1 Market Attractiveness Analysis By Component3.7.2 Market Attractiveness Analysis By IndicationChapter 4. Global Home Healthcare Market- Competitive Landscape

4.1 Company Market Share Analysis4.1.1 Global Home Healthcare Market: Company Market Share, 20254.2 Strategic Development4.2.1 Acquisitions & mergers4.2.2 New Product launches4.2.3 Agreements, partnerships, collaborations, and joint ventures4.2.4 Research and development and regional expansion4.3 Price Trend AnalysisChapter 5. Global Home Healthcare Market - Component Analysis

5.1 Global Home Healthcare Market Overview: Component5.1.1 Global Home Healthcare Market share, By Component, 2025 and 20355.2 Services5.2.1 Global Home Healthcare Market by Services, 2026 - 2035 (USD Billion)5.3 Equipment5.3.1 Global Home Healthcare Market by Equipment, 2026 - 2035 (USD Billion)5.4 Others5.4.1 Global Home Healthcare Market by Others, 2026 - 2035 (USD Billion)Chapter 6. Global Home Healthcare Market - Indication Analysis

6.1 Global Home Healthcare Market Overview: Indication6.1.1 Global Home Healthcare Market Share, By Indication, 2025 and 20356.2 Neurological & Mental Disorders6.2.1 Global Home Healthcare Market by Neurological & Mental Disorders, 2026 - 2035 (USD Billion)6.3 Cardiovascular Disorder & Hypertension6.3.1 Global Home Healthcare Market by Cardiovascular Disorder & Hypertension, 2026 - 2035 (USD Billion)6.4 Diabetes & Kidney Disorders6.4.1 Global Home Healthcare Market by Diabetes & Kidney Disorders, 2026 - 2035 (USD Billion)6.5 Respiratory Disease & COPD6.5.1 Global Home Healthcare Market by Respiratory Disease & COPD, 2026 - 2035 (USD Billion)6.6 Maternal Disorders6.6.1 Global Home Healthcare Market by Maternal Disorders, 2026 - 2035 (USD Billion)6.7 Mobility Disorders6.7.1 Global Home Healthcare Market by Mobility Disorders, 2026 - 2035 (USD Billion)6.8 Cancer6.8.1 Global Home Healthcare Market by Cancer, 2026 - 2035 (USD Billion)6.9 Wound Care6.9.1 Global Home Healthcare Market by Wound Care, 2026 - 2035 (USD Billion)6.10 Others6.10.1 Global Home Healthcare Market by Others, 2026 - 2035 (USD Billion)Chapter 7. Home Healthcare Market - Regional Analysis

7.1 Global Home Healthcare Market Regional Overview7.2 Global Home Healthcare Market Share, by Region, 2025 & 2035 (USD Billion)7.3 North America7.3.1 North America Home Healthcare Market, 2026 - 2035 (USD Billion)7.3.1.1 North America Home Healthcare Market, by Country, 2026 - 2035 (USD Billion)7.3.2 North America Home Healthcare Market, by Component, 2026 - 20357.3.2.1 North America Home Healthcare Market, by Component, 2026 - 2035 (USD Billion)7.3.3 North America Home Healthcare Market, by Indication, 2026 - 20357.3.3.1 North America Home Healthcare Market, by Indication, 2026 - 2035 (USD Billion)7.4 Europe7.4.1 Europe Home Healthcare Market, 2026 - 2035 (USD Billion)7.4.1.1 Europe Home Healthcare Market, by Country, 2026 - 2035 (USD Billion)7.4.2 Europe Home Healthcare Market, by Component, 2026 - 20357.4.2.1 Europe Home Healthcare Market, by Component, 2026 - 2035 (USD Billion)7.4.3 Europe Home Healthcare Market, by Indication, 2026 - 20357.4.3.1 Europe Home Healthcare Market, by Indication, 2026 - 2035 (USD Billion)7.5 Asia Pacific7.5.1 Asia Pacific Home Healthcare Market, 2026 - 2035 (USD Billion)7.5.1.1 Asia Pacific Home Healthcare Market, by Country, 2026 - 2035 (USD Billion)7.5.2 Asia Pacific Home Healthcare Market, by Component, 2026 - 20357.5.2.1 Asia Pacific Home Healthcare Market, by Component, 2026 - 2035 (USD Billion)7.5.3 Asia Pacific Home Healthcare Market, by Indication, 2026 - 20357.5.3.1 Asia Pacific Home Healthcare Market, by Indication, 2026 - 2035 (USD Billion)7.6 Latin America7.6.1 Latin America Home Healthcare Market, 2026 - 2035 (USD Billion)7.6.1.1 Latin America Home Healthcare Market, by Country, 2026 - 2035 (USD Billion)7.6.2 Latin America Home Healthcare Market, by Component, 2026 - 20357.6.2.1 Latin America Home Healthcare Market, by Component, 2026 - 2035 (USD Billion)7.6.3 Latin America Home Healthcare Market, by Indication, 2026 - 20357.6.3.1 Latin America Home Healthcare Market, by Indication, 2026 - 2035 (USD Billion)7.7 The Middle-East and Africa7.7.1 The Middle-East and Africa Home Healthcare Market, 2026 - 2035 (USD Billion)7.7.1.1 The Middle-East and Africa Home Healthcare Market, by Country, 2026 - 2035 (USD Billion)7.7.2 The Middle-East and Africa Home Healthcare Market, by Component, 2026 - 20357.7.2.1 The Middle-East and Africa Home Healthcare Market, by Component, 2026 - 2035 (USD Billion)7.7.3 The Middle-East and Africa Home Healthcare Market, by Indication, 2026 - 20357.7.3.1 The Middle-East and Africa Home Healthcare Market, by Indication, 2026 - 2035 (USD Billion)Chapter 8. Company Profiles

8.1 B. Braun Melsungen AG8.1.1 Overview8.1.2 Financials8.1.3 Product Portfolio8.1.4 Business Strategy8.1.5 Recent Developments8.2 Abbott8.2.1 Overview8.2.2 Financials8.2.3 Product Portfolio8.2.4 Business Strategy8.2.5 Recent Developments8.3 Medtronic PLC8.3.1 Overview8.3.2 Financials8.3.3 Product Portfolio8.3.4 Business Strategy8.3.5 Recent Developments8.4 Koninklijke Philips N.V.8.4.1 Overview8.4.2 Financials8.4.3 Product Portfolio8.4.4 Business Strategy8.4.5 Recent Developments8.5 Johnson & Johnson Services Inc.8.5.1 Overview8.5.2 Financials8.5.3 Product Portfolio8.5.4 Business Strategy8.5.5 Recent Developments8.6 Amedisys Inc.8.6.1 Overview8.6.2 Financials8.6.3 Product Portfolio8.6.4 Business Strategy8.6.5 Recent Developments8.7 Kindred Healthcare Inc.8.7.1 Overview8.7.2 Financials8.7.3 Product Portfolio8.7.4 Business Strategy8.7.5 Recent Developments8.8 Brookdale Senior Living Solutions8.8.1 Overview8.8.2 Financials8.8.3 Product Portfolio8.8.4 Business Strategy8.8.5 Recent Developments8.9 Home Instead Inc.8.9.1 Overview8.9.2 Financials8.9.3 Product Portfolio8.9.4 Business Strategy8.9.5 Recent Developments8.10 Genesis Healthcare Inc.8.10.1 Overview8.10.2 Financials8.10.3 Product Portfolio8.10.4 Business Strategy8.10.5 Recent Developments8.11 Others8.11.1 Overview8.11.2 Financials8.11.3 Product Portfolio8.11.4 Business Strategy8.11.5 Recent Developments

Frequently Asked Questions

Home healthcare involves medical services and equipment provided in patients' residences, including nursing, therapy, diagnostics, and monitoring, as a cost-effective alternative to hospital care for managing chronic conditions and daily assistance.

Key factors include the aging population, technological advancements in telemedicine, rising chronic diseases, government initiatives for cost reduction, and shifts towards home-based care post-COVID.

The market is projected to grow from USD 459.29 billion in 2025 to USD 1216 billion by 2035.

The CAGR is expected to be 10.21% during the forecast period.

North America will contribute notably, holding over 42.47% of the market share due to advanced infrastructure and high geriatric population.

Major players include B. Braun Melsungen AG, Abbott, Medtronic PLC, Koninklijke Philips N.V., Johnson & Johnson Services Inc., Amedisys Inc., Kindred Healthcare Inc., Brookdale Senior Living Solutions, Home Instead Inc., and Genesis Healthcare Inc.

The report provides comprehensive analysis including market size, forecasts, segmentation, drivers, restraints, regional insights, key players, trends, and strategic recommendations.

The value chain includes raw material suppliers, manufacturers of equipment and devices, service providers (nursing and therapy), distribution channels, and end-users such as patients and caregivers.

Trends are shifting towards digital health solutions, personalized care, and remote monitoring, with consumers preferring convenient, tech-enabled home services that enhance independence and reduce costs.

Regulatory factors include licensing, reimbursement policies, and FDA initiatives; environmental factors involve sustainable device manufacturing and data privacy regulations impacting digital tool adoption.