K12 Education Market Size, Share and Trends 2026 to 2035

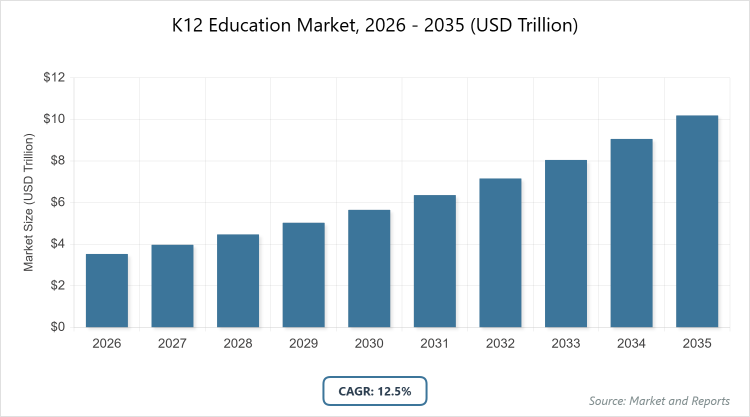

The global K12 Education Market size was estimated at USD 3.53 Trillion in 2025 and is expected to reach USD 10.2 Trillion by 2035, growing at a CAGR of 12.5% from 2026 to 2035. The K12 education market is primarily driven by the integration of AI and digital tools to facilitate personalized learning, alongside robust government funding for digital infrastructure and STEM-focused curricula.

What are the Key Insights into the K12 Education Market?

- Global K12 Education Market value projected at approximately USD 3.53 trillion in 2026, expanding to around USD 10.2 trillion by 2035.

- Compound Annual Growth Rate (CAGR) estimated at 12.5% during the forecast period from 2026 to 2035.

- Dominated subsegment in Application: High School (9-12), holding the largest share due to focus on career readiness and advanced skills.

- Second dominated subsegment in Application: Middle School (6-8), growing significantly with emphasis on foundational STEM education.

- Dominated subsegment in Institution: Public, leading with the highest revenue share owing to government funding and universal access.

- Second dominated subsegment in Institution: Private, experiencing rapid growth through demand for quality and personalized education.

- Dominated subsegment in Delivery Mode: Offline, commanding the majority share for its role in social development and established infrastructure.

- Second dominated subsegment in Delivery Mode: Online, poised for the fastest growth driven by flexibility and technological adoption.

- Dominated region: North America, accounting for the largest market share with advanced EdTech integration and high investments.

What is the Industry Overview of the K12 Education Market?

The K12 education market encompasses the comprehensive ecosystem of educational services, institutions, and technologies dedicated to delivering primary and secondary education from kindergarten through 12th grade, serving students typically aged 5 to 18 years old. This market includes both public and private schooling systems, as well as emerging digital and hybrid learning models that integrate traditional classroom instruction with innovative tools like online platforms, gamified content, and personalized adaptive learning. It covers a wide array of stakeholders, from governments funding public infrastructure and curriculum development to private entities offering specialized programs, extracurricular activities, and educational technology solutions aimed at enhancing student engagement, skill-building, and academic outcomes.

At its core, the market focuses on foundational education that builds essential knowledge in core subjects such as mathematics, science, language arts, and social studies, while also emphasizing critical thinking, problem-solving, digital literacy, and social-emotional development to prepare students for higher education, careers, and lifelong learning in an increasingly globalized and technology-driven world.

What are the Market Dynamics Shaping the K12 Education Market?

Growth Drivers

The growth of the K12 education market is propelled by the increasing adoption of advanced technologies such as artificial intelligence, virtual reality, and gamified learning platforms that personalize education, boost student engagement, and provide real-time feedback, thereby addressing diverse learning needs and improving outcomes; government initiatives worldwide are enhancing this momentum through substantial investments in infrastructure, teacher training, and digital tools, particularly in areas like STEM and vocational education, which attract more students and foster partnerships with private sectors; the shift toward hybrid learning models, accelerated by global events like the pandemic, has expanded access to quality education in remote areas, while rising parental demand for individualized and high-quality alternatives in private institutions further drives market expansion by emphasizing smaller class sizes, experienced educators, and extracurricular opportunities that align with modern skill requirements.

Restraints

The K12 education market faces restraints primarily from the persistent digital divide in rural and low-income regions, where limited access to reliable internet, devices, and electricity hinders the adoption of online and tech-integrated learning, exacerbating educational inequalities; concerns over data privacy, online safety, and regulatory compliance add complexity, as schools must navigate stringent laws while ensuring accreditation, which can slow the integration of new technologies; additionally, teacher resistance to rapid technological changes, coupled with inadequate training and fragmented procurement processes in public systems, limits effective implementation, while financial barriers for families to afford private or online options reinforce the dominance of traditional offline modes and constrain overall market penetration in underserved areas.

Opportunities

Opportunities in the K12 education market abound with the rapid expansion of EdTech solutions in emerging regions, where increasing internet penetration and mobile device usage enable scalable, affordable access to personalized learning platforms, specialized courses, and immersive experiences like AR/VR, particularly in populous countries seeking to modernize curricula and bridge skill gaps; government mandates for digitization and equity-focused funding create pipelines for partnerships between public institutions and private tech firms, fostering innovations in AI-driven tutoring and micro-credentialing for career readiness; moreover, the rise of hybrid models offers flexibility for diverse learners, while mergers and acquisitions among EdTech companies allow for broader product portfolios, enhanced distribution, and targeted solutions that cater to evolving demands for mental health support, project-based learning, and global collaboration in education.

Challenges

Challenges in the K12 education market include ensuring equitable access amid historical inequalities, requiring inclusive policies for special needs students, language minorities, and anti-discrimination measures, while adapting teaching methods from rote memorization to skill-focused, project-based approaches demands ongoing professional development for educators; the lack of direct substitutes for foundational K12 education underscores the need for standardized quality in curriculum, teacher qualifications, and outcomes, yet fragmented systems and end-user concentration on young students necessitate strategies to maintain engagement and attention; furthermore, privacy litigations, high innovation costs, and the need for sustained infrastructure maintenance in developing areas pose ongoing hurdles, especially as rapid technological advancements outpace regulatory frameworks and teacher preparedness globally.

K12 Education Market: Report Scope

| Report Attributes | Report Details |

| Report Name | K12 Education Market |

| Market Size 2025 | USD 3.53 Trillion |

| Market Forecast 2035 | USD 10.2 Trillion |

| Growth Rate | CAGR of 12.5% |

| Report Pages | 215 |

| Key Companies Covered |

Pearson plc, McGraw-Hill Education, Microsoft Corporation, Adobe Inc., and BYJU’S. |

| Segments Covered | By Application, By Institution, By Delivery Mode, By Region |

| Regions Covered | Asia Pacific, North America, Europe, Latin America, The Middle East and Africa |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the K12 Education Market Segmented?

By application category, is High School (9-12), which leads due to its critical role in preparing students for college and careers through specialized programs, standardized testing, internships, and a focus on advanced skills like critical thinking and communication, driving the market by aligning education with workforce demands and attracting government investments in STEM and vocational training that enhance overall student outcomes and economic productivity. The second most dominant segment is Middle School (6-8), which is growing prominently as it bridges elementary foundations with high school rigor, emphasizing early STEM exposure, quality academic transitions, and parental awareness of its importance in building strong educational pathways, thereby contributing to market growth by fostering long-term engagement and addressing skill gaps that support broader adoption of innovative teaching methods.

By institution category, is Public, which holds the largest share because of extensive government initiatives for universal access, equity, and standardized curricula, coupled with increased funding for infrastructure and teacher training that make it accessible to diverse populations, driving the market through large-scale implementations of EdTech and reforms that improve quality and attract partnerships for resource enhancement. The second most dominant segment is Private, which is expanding rapidly owing to rising demand for superior quality, smaller class sizes, experienced faculty, and tailored learning experiences including extracurriculars and flexible schedules, propelling market growth by integrating advanced technologies and individualized approaches that meet parental expectations for premium education and skill development.

By delivery mode category is Offline, which commands the majority due to its essential contribution to social-emotional development, hands-on interactions, and peer relationships, supported by established infrastructure, parental preferences for structure, and concerns over online safety, driving the market by maintaining traditional engagement while gradually incorporating tech to enhance in-person experiences. The second most dominant segment is Online, which is forecasted for substantial growth thanks to surging internet penetration, affordability, and awareness of its benefits like personalization, convenience, and diverse course offerings accelerated by global shifts, boosting the market through expanded access for remote learners and specialized programs that complement offline methods in hybrid setups.

What are the Recent Developments in the K12 Education Market?

- In November 2023, Arada, a UAE-based property developer, collaborated with Innoventures Education to establish a new K-12 international school in Sharjah, designed to accommodate up to 2,000 students and offering American and International Baccalaureate curricula, aiming to enhance educational options in the region through modern facilities and diverse learning pathways.

- In November 2023, VIBGYOR Group of Schools in India partnered with Bank of Baroda to provide K-12 education benefits for employees’ children across its 36 schools affiliated with CISCE, CBSE, and CAIE boards, facilitating streamlined admissions and supporting workforce retention by addressing family educational needs.

- In September 2023, Adobe Inc. teamed up with India’s Union Education Ministry to offer free Adobe Express Premium access to all K-12 schools, empowering students and teachers with tools for creativity, digital skill-building, and dynamic material creation, while including professional development to integrate these resources effectively.

- In June 2025, a U.S. executive order mandated that school districts submit AI implementation plans within 18 months, establishing national guidelines to promote equitable and ethical use of artificial intelligence in K-12 education for improved student outcomes.

- In May 2025, IXL Learning acquired UK-based MyTutor, gaining access to 200,000 families and 40% of UK secondary schools, expanding its personalized tutoring and learning platform offerings to strengthen its global presence in adaptive education solutions.

How Does Regional Analysis Impact the K12 Education Market?

North America dominates the K12 education market with the largest revenue share, driven by cutting-edge technological integrations such as interactive tools and adaptive software, substantial EdTech investments through venture capital and government funding, and high internet penetration that enables seamless online learning and collaboration; the United States stands as the dominating country, bolstered by federal stimulus programs linking grants to equity, innovative pilots in AI tutoring, and a robust ecosystem of partnerships that enhance curriculum and teacher training across diverse districts.

Asia Pacific is the fastest-growing region in the K12 education market, fueled by its vast population in countries like India and China, a surge in internet and mobile penetration post-pandemic, and government investments in digital infrastructure, curriculum modernization, and teacher training to improve access and quality; China emerges as the dominating country, with massive EdTech revenues, AI literacy initiatives, and large-scale digitization efforts that cater to millions of students and drive innovations in personalized platforms and hybrid models.

Europe contributes significantly to the K12 education market through its emphasis on privacy standards, standardized quality, and inclusive policies that support special needs and multilingual education, with ongoing shifts toward project-based learning and digital literacy; Germany is the dominating country, leveraging strong regulatory frameworks, investments in STEM programs, and collaborations for AI-driven tools that ensure equitable access and high educational outcomes across the region.

Latin America shows promising growth in the K12 education market, supported by increasing adoption of hybrid learning to address remote access challenges and government efforts to enhance infrastructure and equity; Brazil leads as the dominating country, with initiatives for broadband expansion, EdTech partnerships, and curriculum reforms that focus on vocational training and personalized learning to bridge educational gaps in urban and rural areas.

The Middle East and Africa region is evolving in the K12 education market amid rising demand for quality alternatives and technological integration, though challenged by infrastructure limitations; the United Arab Emirates dominates, through ambitious projects like new international schools, AI implementations, and partnerships that promote innovative curricula and global standards to attract investments and improve regional educational landscapes.

Who are the Key Market Players and What are Their Strategies in the K12 Education Market?

- Pearson plc: This key player focuses on partnerships for AI-driven coursework and content delivery, such as collaborations with Microsoft on Azure to provide interactive, analytics-ready educational materials that enhance personalized learning and expand market reach through digital transformations in curricula.

- McGraw-Hill Education (Platinum Equity): The company emphasizes transforming traditional content into interactive formats integrated with learning management systems, pursuing mergers and acquisitions to consolidate platforms and offer full-suite solutions that address teacher needs for adaptive assessments and student outcomes.

- Microsoft Corporation: Microsoft employs strategies centered on bundling education tools like Teams and AI collaborations with entities such as Khan Academy, aiming to provide comprehensive ecosystems for collaborative learning, real-time feedback, and security certifications to meet government mandates and scale in public systems.

- Adobe Inc.: Adobe’s approach involves free access partnerships, like with India’s Education Ministry for Adobe Express, to foster creativity and digital skills, while investing in professional development to integrate tools seamlessly into K-12 environments and drive innovation in teaching materials.

- BYJU’S: As a prominent player, BYJU’S leverages mobile apps for tailored content across K-12 grades, focusing on adaptive learning phases and global expansions through acquisitions of EdTech startups to diversify offerings and penetrate emerging markets with personalized, engaging educational experiences.

What are the Market Trends in the K12 Education Market?

- Increasing integration of AI and AR/VR technologies for personalized tutoring, immersive experiences, and continuous feedback to enhance student engagement and address diverse learning styles.

- Shift toward hybrid learning models that blend in-person and virtual instruction, offering flexibility for remote areas and niche electives while maintaining social development.

- Rising emphasis on project-based learning, critical thinking, digital literacy, and social-emotional skills, moving away from rote memorization to prepare students for future careers.

- Government mandates and funding for digitization, equity, and AI literacy, creating opportunities for EdTech procurement and partnerships in infrastructure development.

- Growth in private sector innovation diffusing to public systems through pilots, licensing, and M&A activities to expand adaptive platforms and market share.

- Surge in mobile-first solutions in emerging markets, driven by smartphone proliferation and low-bandwidth needs for accessible, affordable education.

- Focus on data privacy and security certifications amid litigations, influencing technology adoption and compliance in global K-12 systems.

What Market Segments are Covered in the K12 Education Market Report?

By Application

- High School (9-12)

- Middle School (6-8)

- Elementary School (K-5)

By Institution

- Public

- Private

By Delivery Mode

- Offline

- Online

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global K12 Education Market - Industry Analysis

Chapter 4. Global K12 Education Market- Competitive Landscape

Chapter 5. Global K12 Education Market - Application Analysis

Chapter 6. Global K12 Education Market - Institution Analysis

Chapter 7. Global K12 Education Market - Delivery Mode Analysis

Chapter 8. K12 Education Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

The K12 education market refers to the global industry encompassing educational services, institutions, and technologies for students from kindergarten to 12th grade, focusing on foundational learning, skill development, and preparation for higher education or careers through public, private, online, and hybrid models.

Key factors include technological advancements like AI and AR/VR integration, government investments in infrastructure and digitization, rising demand for personalized and hybrid learning, increasing internet penetration in emerging regions, and partnerships between public and private sectors to enhance equity and innovation.

The K12 education market is projected to grow from approximately USD 3.53 trillion in 2026 to around USD 10.2 trillion by 2035, reflecting sustained expansion driven by EdTech adoption and educational reforms.

The compound annual growth rate (CAGR) for the K12 education market is estimated at 12.5% from 2026 to 2035, supported by technological innovations and increasing global access to quality education.

North America will contribute notably to the K12 education market value, holding the largest share due to advanced EdTech integrations, high investments, and robust infrastructure in countries like the United States.

Major players include Pearson plc, McGraw-Hill Education, Microsoft Corporation, Adobe Inc., and BYJU’S, which drive growth through innovations in AI-driven tools, partnerships for content delivery, and expansions in personalized learning platforms.

The global K12 education market report can be expected to provide comprehensive insights into market size, growth projections, segmentation analysis, regional dynamics, key players' strategies, trends, drivers, restraints, opportunities, challenges, and recent developments to guide stakeholders in decision-making.

The value chain includes curriculum development and content creation, technology integration and platform provision, institutional delivery through public and private schools, teacher training and support services, student assessment and feedback mechanisms, and end-user engagement via online or offline modes.

Market trends are evolving toward AI-personalized learning, hybrid models, and emphasis on skills like digital literacy and mental health, while consumer preferences shift to flexible, engaging, and equitable education options that prioritize quality, accessibility, and career readiness.

Regulatory factors include data privacy laws, accreditation standards, and government mandates for AI implementation and equity, while environmental factors involve sustainable infrastructure investments and adaptations to climate-related disruptions in education delivery, influencing growth by ensuring compliance and inclusivity.