Lithium-Ion Battery Market Size, Share and Trends 2026 to 2035

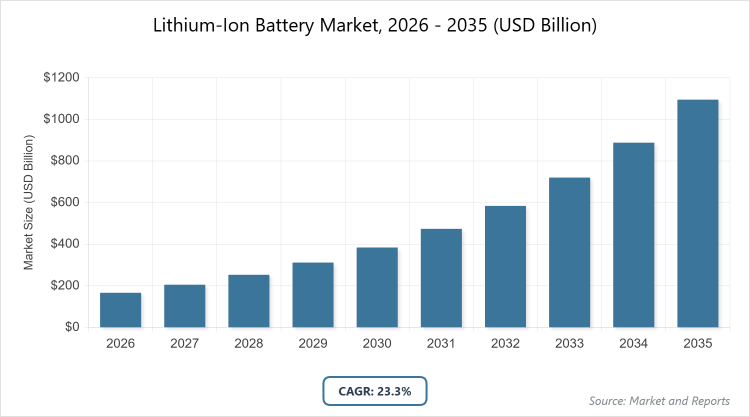

The global Lithium-Ion Battery Market size was estimated at USD 166.2 Billion in 2025 and is expected to reach USD 887.8 Billion by 2035, growing at a CAGR of 23.3% from 2026 to 2035. The Lead Acid Battery Market is primarily driven by the expanding automotive sector’s demand for SLI (Starting, Lighting, and Ignition) batteries, the rapid growth of telecommunications and data center infrastructure requiring reliable backup power, and the increasing integration of renewable energy storage solutions.

What are the Key Insights?

- Global lithium-ion battery market value is projected to grow from USD 166.2 billion in 2026 to USD 887.8 billion by 2035.

- The market is expected to register a CAGR of 23.3% during the forecast period from 2026 to 2035.

- Dominant subsegment in type: Lithium Nickel Manganese Cobalt (NMC), due to its balanced energy density and cost-effectiveness for electric vehicles.

- Second dominant subsegment in type: Lithium Iron Phosphate (LFP), valued for its safety and thermal stability in energy storage applications.

- Dominant subsegment in application: Automotive, accounting for over 50% market share driven by electric vehicle proliferation.

- Second dominant subsegment in application: Energy Storage Systems, growing rapidly with renewable energy integration.

- Dominant subsegment in capacity: >100 kWh, essential for long-range EVs and utility-scale storage.

- Second dominant subsegment in capacity: 50-100 kWh, commonly used in mid-range vehicles and commercial applications.

- Dominant region: Asia Pacific, holding approximately 55.6% market share by 2035.

What is the Lithium-Ion Battery Industry Overview?

The lithium-ion battery market refers to the global industry involved in the production, distribution, and application of rechargeable batteries that utilize lithium ions moving between the anode and cathode to store and release electrical energy through electrochemical reactions. These batteries are characterized by their high energy density, long cycle life, and relatively low self-discharge rates compared to other battery technologies, making them suitable for a wide range of uses where portability, efficiency, and reliability are essential. The market encompasses various components such as cathodes, anodes, electrolytes, and separators, and it serves diverse sectors by enabling the transition toward sustainable energy solutions, powering everyday devices, and supporting the electrification of transportation and grid systems.

What are the Market Dynamics?

Growth Drivers

The lithium-ion battery market is propelled by the surging adoption of electric vehicles worldwide, driven by governmental incentives, stricter emission regulations, and consumer preference for eco-friendly transportation options, which in turn boosts demand for high-performance batteries capable of providing longer ranges and faster charging times. Additionally, the integration of renewable energy sources like solar and wind into power grids necessitates reliable energy storage systems to manage intermittency and ensure stable supply, further accelerating market expansion. Technological advancements in battery chemistries, such as improvements in energy density and cost reductions, along with increasing investments in gigafactories and supply chain localization, contribute significantly to scaling production and meeting rising global energy needs.

Restraints

Market growth faces hurdles from supply chain vulnerabilities, including geopolitical tensions and raw material shortages for key elements like lithium, cobalt, and nickel, which lead to price fluctuations and potential delays in production. Environmental concerns related to mining practices, such as high water usage and habitat disruption, coupled with inadequate recycling infrastructure, pose regulatory and sustainability challenges that could increase operational costs and slow down expansion in certain regions. Moreover, the high initial investment required for advanced manufacturing facilities and the risk of battery safety issues, like thermal runaway, necessitate stringent quality controls and certifications, which can restrain smaller players from entering or expanding in the market.

Opportunities

Emerging opportunities lie in the development of next-generation technologies, including solid-state batteries and silicon anodes, which promise higher energy densities, improved safety, and longer lifespans, opening new avenues for applications in high-demand sectors like aerospace and medical devices. The push toward circular economy practices, such as enhanced recycling methods to recover valuable materials, presents a chance to reduce dependency on virgin resources and lower environmental impacts while creating new revenue streams. Expanding markets in developing economies, supported by localization initiatives and partnerships, offer potential for growth in underserved areas where demand for affordable energy storage and electrification is rapidly increasing.

Challenges

The industry grapples with the need to balance rapid innovation with safety and regulatory compliance, as evolving standards for battery performance and environmental impact require continuous R&D investments that can strain resources. Intense competition among manufacturers to achieve cost parity while maintaining quality leads to pricing pressures and potential overcapacity in certain segments. Furthermore, the complexity of global supply chains, exacerbated by trade restrictions and logistical issues, challenges the ability to ensure timely delivery and consistent quality across international markets.

Lithium-Ion Battery Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Lithium-Ion Battery Market |

| Market Size 2025 | USD 166.2 Billion |

| Market Forecast 2035 | USD 887.8 Billion |

| Growth Rate | CAGR of 23.3% |

| Report Pages | 215 |

| Key Companies Covered |

Contemporary Amperex Technology Co. Ltd. (CATL), LG Energy Solution, Ltd., Panasonic Energy Co., Ltd., BYD Company Ltd., Samsung SDI Co., Ltd., and SK On. |

| Segments Covered | By Type, By Application, By Capacity, By Region |

| Regions Covered | Asia Pacific, North America, Europe, Latin America, The Middle East and Africa |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Market Segmented?

By type, is Lithium Nickel Manganese Cobalt (NMC), which leads due to its superior energy density, longer cycle life, and optimal balance between power output and cost, making it ideal for high-performance applications like electric vehicles where range and efficiency are critical; this dominance drives the market by enabling the widespread adoption of EVs through better battery performance that reduces range anxiety and supports faster charging, ultimately accelerating the shift from fossil fuels to sustainable transportation and contributing to global emission reduction goals. The second most dominant segment is Lithium Iron Phosphate (LFP), favored for its enhanced safety features, resistance to thermal runaway, and lower production costs stemming from the absence of expensive cobalt, which positions it strongly in energy storage and budget-conscious EV markets; it helps drive the market by providing reliable, cost-effective solutions for grid stabilization and renewable integration, fostering greater accessibility to clean energy technologies and expanding market penetration in price-sensitive regions.

By application, is Automotive, which commands the largest share owing to the explosive growth in electric vehicle sales fueled by government subsidies, infrastructure development, and consumer demand for zero-emission mobility, allowing batteries to power everything from passenger cars to commercial fleets; this dominance propels the overall market by catalyzing investments in charging networks and battery innovation, thereby creating economies of scale that lower costs and enable broader electrification across transportation sectors, significantly contributing to decarbonization efforts worldwide. The second most dominant segment is Energy Storage Systems, driven by the need to store intermittent renewable energy from sources like solar and wind, ensuring grid reliability and enabling off-grid solutions in remote areas; it drives the market by facilitating the transition to sustainable energy systems, reducing reliance on traditional power plants, and opening opportunities for utility-scale projects that enhance energy security and support the global push toward net-zero emissions.

By capacity, is >100 kWh, which prevails because it caters to the requirements of long-range electric vehicles and large-scale energy storage installations where high energy output is essential for extended operation without frequent recharging; this dominance fuels market growth by supporting the expansion of EV models with competitive ranges and enabling utility-grade storage that balances power supply fluctuations, thus encouraging investments in infrastructure and advancing the adoption of clean energy technologies on a massive scale. The second most dominant segment is 50-100 kWh, popular for mid-range vehicles, commercial applications, and residential energy storage due to its balance of performance and affordability, offering sufficient capacity without excessive costs; it contributes to market drive by bridging the gap for consumers and businesses transitioning to electrification, promoting wider accessibility and stimulating demand in emerging markets where cost-effectiveness is key to adoption.

What are the Recent Developments?

- In July 2025, Kalmar introduced its second-generation lithium-ion battery for electric equipment, featuring increased capacity and improved thermal stability, which enhances performance in heavy-duty applications like cargo handling and supports global sustainability goals by reducing emissions in industrial operations.

- In July 2025, Panasonic Energy commenced mass production at its new Kansas factory, targeting an annual capacity of 32 GWh to bolster U.S. domestic manufacturing and meet rising demand for electric vehicle batteries through localized supply chains.

- In February 2025, Clarios achieved a milestone by producing its one millionth lithium-ion 12-volt battery, signaling a shift toward chemistry-agnostic solutions that improve efficiency in electrified vehicles and underscore the company’s commitment to innovation in low-voltage systems.

- In June 2024, Toshiba, in collaboration with Sojitz and CBMM, developed a next-generation lithium-ion battery with a niobium titanium oxide anode, promising faster charging times and higher energy density for applications in electric vehicles and energy storage.

- In April 2025, ITEN launched a solid-state battery capable of operating at 200°C with high discharge rates, targeted at IoT devices to enable reliable performance in extreme environments and expand the scope of connected technologies.

What is the Regional Analysis?

The Asia Pacific region dominates the lithium-ion battery market, driven by robust manufacturing ecosystems, extensive raw material availability, and aggressive government policies promoting electric vehicles and renewable energy, with China as the dominating country due to its massive EV sales exceeding 11 million units annually, integrated supply chains from mining to assembly, and leadership in battery production capacity that accounts for over half of global output, enabling cost advantages and rapid innovation that fuel regional and global market expansion.

North America exhibits strong growth through significant investments in domestic production and recycling initiatives, supported by federal incentives and a focus on supply chain resilience, with the United States as the dominating country owing to its surging EV adoption reaching 18.7% market share, major gigafactory developments, and technological advancements in next-gen batteries that position it as a key player in reducing import dependency and advancing sustainable mobility.

Europe focuses on stringent environmental regulations and localization efforts to build a self-sufficient battery industry, emphasizing recycling and sustainable sourcing, with Germany as the dominating country thanks to its automotive heritage, high EV penetration supported by subsidies, and collaborations among manufacturers like Volkswagen and Northvolt that drive innovation in high-performance batteries for premium vehicles.

Latin America is emerging with opportunities in lithium mining and export, bolstered by natural resource abundance and partnerships for processing facilities, with Chile as the dominating country due to its vast lithium reserves in the Lithium Triangle, government initiatives for value-added production, and increasing foreign investments that aim to integrate the region into global supply chains while addressing local energy needs.

The Middle East and Africa region is gradually expanding through renewable energy projects and electrification in mining operations, with South Africa as the dominating country leveraging its cobalt and manganese resources, growing solar storage demand, and initiatives like battery manufacturing hubs to support regional energy transitions and economic diversification.

Who are the Key Market Players and Their Strategies?

Contemporary Amperex Technology Co. Ltd. (CATL) focuses on scaling production through gigafactory expansions and vertical integration across the supply chain, while investing in R&D for advanced chemistries like sodium-ion batteries to maintain cost leadership and secure long-term OEM partnerships in the EV sector.

LG Energy Solution, Ltd. emphasizes global collaborations with automakers such as Tesla, GM, and Hyundai, alongside heavy investments in gigafactories in North America and Europe to localize production and enhance supply chain resilience, driving innovation in high-energy-density cells for premium vehicles.

Panasonic Energy Co., Ltd. pursues mass production efficiencies and strategic alliances, particularly with Tesla, by developing advanced cylindrical cells and expanding U.S.-based facilities to meet surging EV demand while focusing on sustainability through recycled materials.

BYD Company Ltd. leverages vertical integration from raw materials to vehicle assembly, prioritizing LFP chemistry for cost-effective and safe batteries, and expands internationally through mergers and localized manufacturing to capture market share in emerging economies.

Samsung SDI Co., Ltd. concentrates on premium EV segments with prismatic and pouch cells, employing product launches and R&D in solid-state technologies, while forming joint ventures to strengthen its position in Europe and North America.

SK On adopts acquisition strategies and partnerships to boost capacity, focusing on NMC chemistries for high-performance applications and investing in recycling technologies to ensure sustainable growth amid raw material constraints.

What are the Market Trends?

- Increasing shift toward solid-state batteries for improved safety and energy density in IoT and automotive applications.

- Growing emphasis on recycling and circular economy practices to mitigate raw material shortages and environmental impacts.

- Rapid expansion of gigafactories globally to meet escalating demand from electric vehicles and renewable storage.

- Diversification of battery chemistries, such as LFP for cost-sensitive markets and NMC for high-performance needs.

- Integration with renewable energy systems, driven by rising energy storage obligations and grid modernization efforts.

- Rising governmental incentives and regulations promoting EV adoption and sustainable manufacturing.

What Market Segments are Covered in the Report?

By Type

- Lithium Iron Phosphate (LFP)

- Lithium Cobalt Oxide (LCO)

- Lithium Nickel Manganese Cobalt (NMC)

- Lithium Nickel Cobalt Aluminum (NCA)

- Lithium Manganese Oxide (LMO)

- Lithium Titanate (LTO)

- Others

By Application

- Automotive

- Consumer Electronics

- Industrial

- Energy Storage Systems

- Others

By Capacity

- <50 kWh

- 50-100 kWh

- 100 kWh

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Lithium-Ion Battery Market - Industry Analysis

Chapter 4. Global Lithium-Ion Battery Market- Competitive Landscape

Chapter 5. Global Lithium-Ion Battery Market - Type Analysis

Chapter 6. Global Lithium-Ion Battery Market - Application Analysis

Chapter 7. Global Lithium-Ion Battery Market - Capacity Analysis

Chapter 8. Lithium-Ion Battery Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

The lithium-ion battery market is the global industry focused on the development, manufacturing, and deployment of rechargeable batteries that use lithium ions for energy storage, serving applications in electric vehicles, consumer electronics, and renewable energy systems to enable efficient and sustainable power solutions.

Key factors include the rising adoption of electric vehicles, integration of renewable energy sources requiring storage, technological advancements in battery efficiency and cost reduction, governmental incentives for sustainability, and expansions in manufacturing capacity through gigafactories.

The market is projected to grow from USD 166.2 billion in 2026 to USD 887.8 billion by 2035.

The CAGR is expected to be 23.3% during the period from 2026 to 2035.

Asia Pacific will contribute notably, holding approximately 55.6% of the market share by 2035, driven by strong manufacturing bases and high EV adoption.

Major players include Contemporary Amperex Technology Co. Ltd. (CATL), LG Energy Solution, Ltd., Panasonic Energy Co., Ltd., BYD Company Ltd., Samsung SDI Co., Ltd., and SK On, which drive growth through innovation, expansions, and strategic partnerships.

The report provides comprehensive insights into market size, growth forecasts, segmentation, drivers, restraints, opportunities, challenges, regional analysis, key players, recent developments, trends, and value chain dynamics.

The value chain includes raw material extraction and processing of lithium, cobalt, nickel, and graphite; precursor refining and component manufacturing like cathodes and anodes; cell and pack assembly with electrolytes and separators; integration into end-use applications; and recycling for material recovery.

Market trends are shifting toward safer and higher-density technologies like solid-state batteries, with consumers preferring cost-effective, long-lasting options for EVs and renewables, influenced by sustainability concerns and affordability in emerging markets.

Regulatory factors include emission standards and incentives for EVs, while environmental factors involve raw material mining impacts, recycling mandates like Europe's Battery Regulation, and efforts to reduce carbon footprints through sustainable sourcing and circular practices.