Polymeric Membrane for Separation Market Size and Forecast 2026 to 2035

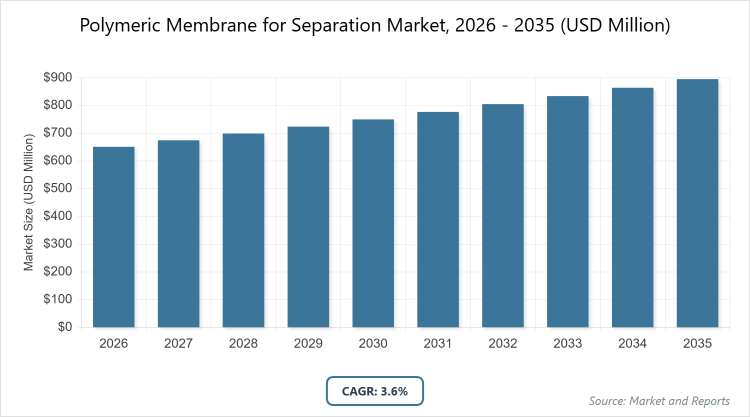

According to MarketnReports, the global Polymeric Membrane for Separation market size was estimated at USD 651 million in 2025 and is expected to reach USD 854 million by 2035, growing at a CAGR of 3.6% from 2026 to 2035. Polymeric Membrane for Separation Market is driven by the growing demand for efficient water treatment, gas separation, and energy-efficient industrial filtration processes.

What are the Key Insights?

- The global polymeric membrane for separation market is projected to grow from approximately USD 651 million in 2025 to USD 854 million in 2035, reflecting steady expansion driven by industrial applications in gas purification and energy sectors.

- The market is expected to register a CAGR of 3.6% during the forecast period from 2026 to 2035, supported by advancements in membrane materials and increasing demand for efficient separation technologies.

- In the type segmentation, the hollow fiber subsegment dominates with about 85% market share, owing to its high surface area to volume ratio that enhances separation efficiency.

- The spiral wound subsegment is the second most dominant in the type segmentation.

- In the application segmentation, isolation of inert N2 from air is the dominant subsegment, driven by widespread use in chemicals and manufacturing for inert blanketing and purging.

- H2 recovery is the second most dominant subsegment in the application segmentation.

- In the end-user segmentation, chemicals & petrochemicals dominates, as it relies heavily on gas purification and solvent recovery processes.

- Oil & gas is the second most dominant in the end-user segmentation.

- In the material composition segmentation, polyimides dominate due to their thermal stability in gas separation applications.

- Polysulfones is the second most dominant in the material composition segmentation.

- In the separation process segmentation, gas separation is the dominant subsegment, favored for its energy efficiency in nitrogen generation and biogas upgrading.

- Vapor separation is the second most dominant in the separation process segmentation.

- North America dominates the regional market with about 40% share, followed by Asia-Pacific at 30%.

What is the Industry Overview?

The polymeric membrane for separation market encompasses thin, selective barriers made from polymer materials that serve as interfaces between two phases, enabling the controlled transport of specific components from gas or liquid mixtures. These membranes are essential in various industrial processes, including gas purification, desalination, and filtration, where they provide an energy-efficient alternative to traditional separation methods by avoiding phase changes and reducing operational complexities. The market focuses on technologies that enhance selectivity, permeability, and durability, catering to sectors such as energy, chemicals, and environmental management, where precise separation is critical for optimizing resource use and minimizing waste.

What are the Market Dynamics?

Growth Drivers

The polymeric membrane for separation market is propelled by rising demand from water and wastewater treatment sectors, where these membranes enable efficient purification amid global pushes for clean water access, alongside expansion in healthcare and bioprocessing industries that require precise separation for pharmaceutical production and biopharmaceutical growth exceeding significant valuations; additionally, adoption in the energy sector for gas separation, natural gas processing, and carbon capture initiatives further accelerates market growth, complemented by developments in advanced materials like fluoropolymers and polyamide-imides that improve chemical resistance and operational efficiency across diverse applications.

Restraints

Market growth faces hurdles from volatility in raw material prices, including key polymers such as polysulfone, polyethersulfone, and polyvinylidene fluoride, which can disrupt supply chains and increase production costs; moreover, high initial capital investments required for installing membrane systems deter smaller enterprises and limit adoption in cost-sensitive regions, while technical limitations like pH stability, chlorine tolerance, and temperature constraints in certain environments further complicate widespread implementation and scalability.

Opportunities

Emerging economies in Asia-Pacific and Latin America present substantial opportunities through circular economy initiatives and industrial expansion, where increasing investments in sustainable technologies can boost demand for advanced polymeric membranes; furthermore, innovations in membrane materials, such as novel polymers integrated with nanomaterials via mixed-matrix designs or electrospinning techniques, offer potential for enhanced selectivity, fouling resistance, and performance in high-growth areas like biogas upgrading and hydrogen production, opening avenues for market players to capture untapped segments.

Challenges

Membrane fouling remains a persistent challenge, as it diminishes efficiency over time and escalates maintenance costs, necessitating frequent cleaning or replacement in demanding industrial settings; additionally, competition from alternative technologies, including thermal distillation and ceramic membranes, poses a threat by offering superior durability in extreme conditions, while overall technical barriers such as limited stability under harsh operational parameters continue to hinder broader market penetration and innovation adoption.

Polymeric Membrane for Separation Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Polymeric Membrane for Separation Market |

| Market Size 2025 | USD 651 Million |

| Market Forecast 2035 | USD 854 Million |

| Growth Rate | CAGR of 3.6% |

| Report Pages | 224 |

| Key Companies Covered |

Air Products, Air Liquide, UBE Corporation, Evonik Industries AG, Grasys, Schlumberger, IGS (Innovative Gas Systems), Honeywell International Inc., MTR (Membrane Technology and Research), Borsig GmbH, Parker Hannifin Corporation, Tianbang, SSS (Samsung Separations Systems), TriTech |

| Segments Covered | By Type, By Application, By End-use, By Material Composition, By Separation Process, and By Region. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Market Segmented?

The Polymeric Membrane for Separation market is segmented by type, application, end-use, material composition, separation process, and region.

By Type

The hollow fiber segment dominates the polymeric membrane for separation market with approximately 85% share, primarily because its design provides a superior surface area to volume ratio, which significantly boosts separation efficiency and allows for compact module configurations ideal for large-scale industrial applications like gas purification; this dominance drives the overall market by enabling cost-effective, high-throughput processes that reduce energy consumption and operational footprints in sectors such as chemicals and energy, where scalability and performance are paramount. The spiral wound segment ranks as the second most dominant, offering advantages in liquid-based separations due to its robust structure and ease of maintenance, which supports market growth by catering to diverse applications requiring moderate pressure operations and helping to expand the technology’s reach into wastewater treatment and desalination projects.

By Application

Isolation of inert N2 from air stands out as the most dominant application segment, fueled by extensive demand in the chemicals and manufacturing industries for inert blanketing, purging, and safety processes that prevent oxidation and explosions; this segment propels market expansion by integrating seamlessly with nitrogen generation systems, lowering costs compared to cryogenic methods and enabling on-site production that enhances operational flexibility and efficiency across global industrial operations. H2 recovery emerges as the second most dominant, driven by the growing emphasis on clean energy transitions and hydrogen economy initiatives, where these membranes facilitate efficient extraction from industrial streams, contributing to market growth by supporting sustainable fuel production and reducing greenhouse gas emissions in refining and petrochemical processes.

By End User

The chemicals & petrochemicals segment is the most dominant in the end-user category, as it heavily relies on polymeric membranes for gas purification, solvent recovery, and process optimization, which are critical for maintaining product purity and compliance with environmental standards; this dominance accelerates market development by addressing the sector’s need for energy-efficient separations that minimize waste and operational costs, thereby fostering innovation in membrane technologies tailored to harsh chemical environments. Oil & gas follows as the second most dominant, utilizing these membranes for natural gas sweetening and dehydration, which drives the market forward by enabling enhanced resource recovery and meeting stringent regulatory requirements for emissions control in upstream and midstream operations.

By Material Composition

Polyimides lead as the most dominant material composition segment due to their exceptional thermal stability and chemical resistance, making them ideal for high-temperature gas separation applications such as CO2 removal and hydrogen purification; this leadership propels the market by allowing operations in demanding conditions that other materials cannot withstand, thus expanding applicability in energy and industrial sectors and promoting advancements in durable, high-performance membranes. Polysulfones is the second most dominant, valued for its mechanical strength and cost-effectiveness, which supports market growth by providing reliable solutions for a broad range of separation processes, including water treatment and vapor separation, where affordability and robustness are key to widespread adoption.

By Separation Process

Gas separation dominates the separation process segment, attributed to its energy efficiency in applications like nitrogen generation, biogas upgrading, and carbon capture, where polymeric membranes offer selective permeation without the need for extensive energy inputs; this dominance fuels market progression by aligning with global sustainability goals, reducing carbon footprints in industrial activities, and encouraging investments in clean energy technologies. Vapor separation is the second most dominant, benefiting from the membranes’ ability to handle organic vapors and humidity control, which contributes to market expansion by addressing needs in food processing, pharmaceuticals, and environmental protection, where precise vapor management enhances product quality and process safety.

What are the Recent Developments?

- UBE Corporation announced an expansion of its polyimide hollow fiber membrane module production at its Sakai and Ube factories in the first half of fiscal year 2025, increasing capacity by 1.8 times to meet rising demand for CO2 separation applications in natural gas processing and carbon capture initiatives.

- Membrane Technology and Research, Inc. (MTR) completed construction of the world’s largest membrane-based carbon capture plant in Gillette, Wyoming, capable of capturing over 150 tonnes of CO2 per day from Basin Electric’s Dry Fork Station coal-fired power plant, marking a significant scale-up in polymeric membrane technology for industrial emissions reduction.

- Honeywell UOP collaborated with SK Innovation and Energy on a feasibility study to retrofit a hydrogen plant with carbon capture technology, incorporating membrane systems alongside cryogenics and pressure swing adsorption to sequester 400,000 tonnes of CO2 annually, highlighting integrated solutions for the energy transition.

What is the Regional Analysis?

North America to dominate the market

North America commands the largest share of the polymeric membrane for separation market at approximately 40%, driven by a mature industrial base, significant investments in shale gas exploration, and biopharmaceutical advancements that demand high-efficiency separation technologies; the United States dominates this region as the leading country, bolstered by stringent environmental regulations promoting carbon capture and clean energy initiatives, alongside robust R&D ecosystems that foster innovations in membrane materials for applications in natural gas processing, hydrogen recovery, and wastewater treatment, thereby enhancing energy security and sustainability efforts across diverse sectors like chemicals, oil & gas, and healthcare.

Asia-Pacific holds about 30% of the global market, propelled by rapid industrial expansion, urbanization, and heavy investments in water treatment infrastructure amid growing environmental concerns; China emerges as the dominating country in this region, with its massive chemical, pharmaceutical, and electronics sectors fueling demand for polymeric membranes in gas purification and desalination, supported by government policies aimed at pollution control and resource efficiency, which in turn drive technological adoptions and market growth through large-scale projects in nitrogen isolation and CO2 removal.

Europe maintains a significant market position, influenced by EU sustainability directives and a focus on green technologies that emphasize energy-efficient separations; Germany stands out as the dominating country, leveraging its advanced manufacturing and chemical industries to lead in membrane applications for hydrogen production and biogas upgrading, where regulatory frameworks for emissions reduction and circular economy practices encourage innovations in polyimide-based membranes, contributing to regional growth in pharmaceuticals, food & beverage, and environmental management.

South America experiences gradual market growth, primarily through mining, oil & gas activities that require reliable separation solutions for resource extraction and processing; Brazil is the dominating country, with its expanding petrochemical sector and investments in natural gas infrastructure driving the adoption of hollow fiber membranes for CO2 removal and vapor separation, aided by regional efforts to improve water quality and comply with international environmental standards, thus supporting sustainable industrial development.

The Middle East & Africa region shows high-growth potential, particularly in desalination and gas processing amid arid climates and energy-rich economies; Saudi Arabia dominates, with its focus on water scarcity solutions and oil & gas enhancements utilizing polymeric membranes for natural gas sweetening and hydrogen recovery, backed by national visions for diversification and sustainability that promote large-scale projects in carbon capture and wastewater treatment, fostering market expansion in emerging African markets as well.

Who are the Key Market Players and Their Strategies?

- Air Products: As a leading player, Air Products focuses on leveraging its global presence and proprietary technologies in gas separation, investing heavily in R&D for advanced polymeric membranes tailored to nitrogen isolation and hydrogen recovery, while pursuing strategic partnerships in carbon capture to expand its market share in energy and chemical sectors.

- Air Liquide: Air Liquide employs strategies centered on integrated solutions for industrial gases, emphasizing innovation in hollow fiber membranes for CO2 removal and vapor separation, with a strong emphasis on sustainability initiatives and acquisitions to strengthen its position in healthcare and bioprocessing applications.

- UBE Corporation: UBE Corporation prioritizes capacity expansions and material advancements in polyimide membranes, targeting high-demand areas like natural gas processing through increased production facilities and collaborations to enhance thermal stability and selectivity for global energy transition projects.

- Evonik Industries AG: Evonik adopts a strategy of developing specialized polymer materials with enhanced chemical resistance, focusing on mixed-matrix innovations and R&D collaborations to address membrane fouling, thereby driving growth in pharmaceuticals and environmental applications.

- Grasys: Grasys concentrates on niche gas separation systems, utilizing modular designs and cost-effective polymeric membranes for inert N2 isolation, with strategies involving regional expansions and technology licensing to capture emerging markets in Asia and the Middle East.

- Schlumberger: Schlumberger integrates membrane technologies into its oil & gas services, emphasizing digitalization and hybrid systems for efficient H2 recovery and CO2 management, with a focus on strategic alliances to optimize upstream processes.

- IGS (Innovative Gas Systems): IGS pursues innovation in on-site gas generation, developing compact polymeric membrane modules for nitrogen and oxygen separation, with strategies aimed at customization and after-sales support to penetrate industrial and healthcare sectors.

- Honeywell International Inc.: Honeywell leverages its UOP division for advanced membrane systems in petrochemicals, focusing on integrated carbon capture solutions and R&D in high-permeability polymers to support clean energy transitions.

- MTR (Membrane Technology and Research): MTR specializes in large-scale carbon capture projects, investing in polarish polymeric membranes for CO2 separation, with strategies involving pilot demonstrations and partnerships to scale up industrial applications.

- Borsig GmbH: Borsig emphasizes engineering solutions for gas processing, developing robust polymeric membranes for vapor/nitrogen separation, with a focus on European market expansions and sustainability-driven innovations.

- Parker Hannifin Corporation: Parker Hannifin targets filtration and separation markets with modular membrane designs, employing acquisition strategies to broaden its portfolio in bioprocessing and food & beverage applications.

- Tianbang: Tianbang focuses on cost-competitive membranes for Asian markets, prioritizing R&D in polyimide composites for gas separation, with strategies involving local manufacturing and supply chain optimizations.

- SSS (Samsung Separations Systems): SSS invests in advanced nanotechnology for membrane enhancement, targeting electronics and pharmaceutical sectors with high-selectivity polymers, through collaborative R&D and market diversification.

- TriTech: TriTech adopts niche strategies for custom membrane solutions in environmental applications, focusing on durability improvements and regional partnerships to address water and gas purification needs.

What are the Market Trends?

- Increasing adoption of mixed-matrix membranes incorporating metal-organic frameworks (MOFs) and nanomaterials to enhance selectivity and permeability for challenging gas separations like CO2 capture and biogas upgrading.

- Growing emphasis on sustainable materials, such as thermally rearranged polymers and polyimide derivatives, to improve durability and performance in high-temperature and harsh chemical environments.

- Expansion of membrane applications in the hydrogen economy, including blue and green hydrogen production, driven by global energy transition goals and carbon capture utilization and storage (CCUS) initiatives.

- Rise in hybrid membrane systems combining polymeric and inorganic elements for extreme conditions, offering better resistance to fouling and extending operational lifespans in industrial settings.

- Advancements in two-dimensional nanosheet and surface-modified membranes, enabling precise control over gas transport and supporting emerging markets in natural gas purification and post-combustion capture.

- Consolidation among key players through capacity expansions and strategic partnerships to meet surging demand in emerging economies and regulatory-driven sectors.

What Market Segments are Covered in the Report?

By Type

- Hollow Fiber

- Spiral Wound

- Others

By Application

- Isolation of Inert N2 from Air

- H2 Recovery

- CO2 Removal from Natural Gas

- Vapor/Nitrogen Separation

- Other Applications

By End User

- Chemicals & Petrochemicals

- Oil & Gas

- Healthcare & Pharmaceuticals

- Food & Beverage

- Other Industries

By Material Composition

- Polyimides

- Polysulfones

- Cellulose Acetate

- Other Polymers

By Separation Process

- Gas Separation

- Vapor Separation

- Liquid Separation

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

1.1 Report Description and Scope1.2 Research Scope1.3 Research Methodology1.3.1 Market Research Type1.3.2 Market Research MethodologyChapter 2. Executive Summary

2.1 Global Polymeric Membrane for Separation Market, (2026 - 2035) (USD Million)2.2 Global Polymeric Membrane for Separation Market: SnapshotChapter 3. Global Polymeric Membrane for Separation Market - Industry Analysis

3.1 Polymeric Membrane for Separation Market: Market Dynamics3.2 Market Drivers3.2.1 The polymeric membrane for separation market is driven by growing water and wastewater treatment needs, expanding healthcare and bioprocessing, rising energy-sector applications, and advances in high-performance membrane materials.3.3 Market Restraints3.3.1 The market is hindered by volatile polymer raw material prices, high initial system costs, and technical limitations in stability and tolerance that restrict adoption and scalability.3.4 Market Opportunities3.4.1 Opportunities are emerging in Asia-Pacific and Latin America through industrial growth and circular economy initiatives, supported by innovations in advanced and nanocomposite polymeric membranes for high-growth energy and sustainability applications.3.5 Market Challenges3.5.1 The market faces challenges from membrane fouling, high maintenance needs, competition from durable alternatives like ceramic membranes, and limited stability under harsh operating conditions.3.6 Porter’s Five Forces Analysis3.7 Market Attractiveness Analysis3.7.1 Market Attractiveness Analysis By Type3.7.2 Market Attractiveness Analysis By Application3.7.3 Market Attractiveness Analysis By End User3.7.4 Market Attractiveness Analysis By Material Composition3.7.5 Market Attractiveness Analysis By Separation ProcessChapter 4. Global Polymeric Membrane for Separation Market- Competitive Landscape

4.1 Company Market Share Analysis4.1.1 Global Polymeric Membrane for Separation Market: Company Market Share, 20254.2 Strategic Development4.2.1 Acquisitions & mergers4.2.2 New Product launches4.2.3 Agreements, partnerships, collaborations, and joint ventures4.2.4 Research and development and regional expansion4.3 Price Trend AnalysisChapter 5. Global Polymeric Membrane for Separation Market - Type Analysis

5.1 Global Polymeric Membrane for Separation Market Overview: Type5.1.1 Global Polymeric Membrane for Separation Market share, By Type, 2025 and 20355.2 Hollow Fiber5.2.1 Global Polymeric Membrane for Separation Market by Hollow Fiber, 2026 - 2035 (USD Million)5.3 Spiral Wound5.3.1 Global Polymeric Membrane for Separation Market by Spiral Wound, 2026 - 2035 (USD Million)5.4 Others5.4.1 Global Polymeric Membrane for Separation Market by Others, 2026 - 2035 (USD Million)Chapter 6. Global Polymeric Membrane for Separation Market - Application Analysis

6.1 Global Polymeric Membrane for Separation Market Overview: Application6.1.1 Global Polymeric Membrane for Separation Market Share, By Application, 2025 and 20356.2 Isolation of Inert N2 from Air6.2.1 Global Polymeric Membrane for Separation Market by Isolation of Inert N2 from Air, 2026 - 2035 (USD Million)6.3 H2 Recovery6.3.1 Global Polymeric Membrane for Separation Market by H2 Recovery, 2026 - 2035 (USD Million)6.4 CO2 Removal from Natural Gas6.4.1 Global Polymeric Membrane for Separation Market by CO2 Removal from Natural Gas, 2026 - 2035 (USD Million)6.5 Vapor/Nitrogen Separation6.5.1 Global Polymeric Membrane for Separation Market by Vapor/Nitrogen Separation, 2026 - 2035 (USD Million)6.6 Other Applications6.6.1 Global Polymeric Membrane for Separation Market by Other Applications, 2026 - 2035 (USD Million)Chapter 7. Global Polymeric Membrane for Separation Market - End User Analysis

7.1 Global Polymeric Membrane for Separation Market Overview: End User7.1.1 Global Polymeric Membrane for Separation Market Share, By End User, 2025 and 20357.2 Chemicals & Petrochemicals7.2.1 Global Polymeric Membrane for Separation Market by Chemicals & Petrochemicals, 2026 - 2035 (USD Million)7.3 Oil & Gas7.3.1 Global Polymeric Membrane for Separation Market by Oil & Gas, 2026 - 2035 (USD Million)7.4 Healthcare & Pharmaceuticals7.4.1 Global Polymeric Membrane for Separation Market by Healthcare & Pharmaceuticals, 2026 - 2035 (USD Million)7.5 Food & Beverage7.5.1 Global Polymeric Membrane for Separation Market by Food & Beverage, 2026 - 2035 (USD Million)7.6 Other Industries7.6.1 Global Polymeric Membrane for Separation Market by Other Industries, 2026 - 2035 (USD Million)Chapter 8. Global Polymeric Membrane for Separation Market - Material Composition Analysis

8.1 Global Polymeric Membrane for Separation Market Overview: Material Composition8.1.1 Global Polymeric Membrane for Separation Market Share, By Material Composition, 2025 and 20358.2 Polyimides8.2.1 Global Polymeric Membrane for Separation Market by Polyimides, 2026 - 2035 (USD Million)8.3 Polysulfones8.3.1 Global Polymeric Membrane for Separation Market by Polysulfones, 2026 - 2035 (USD Million)8.4 Cellulose Acetate8.4.1 Global Polymeric Membrane for Separation Market by Cellulose Acetate, 2026 - 2035 (USD Million)8.5 Other Polymers8.5.1 Global Polymeric Membrane for Separation Market by Other Polymers, 2026 - 2035 (USD Million)Chapter 9. Global Polymeric Membrane for Separation Market - Separation Process Analysis

9.1 Global Polymeric Membrane for Separation Market Overview: Separation Process9.1.1 Global Polymeric Membrane for Separation Market Share, By Separation Process, 2025 and 20359.2 Gas Separation9.2.1 Global Polymeric Membrane for Separation Market by Gas Separation, 2026 - 2035 (USD Million)9.3 Vapor Separation9.3.1 Global Polymeric Membrane for Separation Market by Vapor Separation, 2026 - 2035 (USD Million)9.4 Liquid Separation9.4.1 Global Polymeric Membrane for Separation Market by Liquid Separation, 2026 - 2035 (USD Million)Chapter 10. Polymeric Membrane for Separation Market - Regional Analysis

10.1 Global Polymeric Membrane for Separation Market Regional Overview10.2 Global Polymeric Membrane for Separation Market Share, by Region, 2025 & 2035 (USD Million)10.3 North America10.3.1 North America Polymeric Membrane for Separation Market, 2026 - 2035 (USD Million)10.3.1.1 North America Polymeric Membrane for Separation Market, by Country, 2026 - 2035 (USD Million)10.3.2 North America Polymeric Membrane for Separation Market, by Type, 2026 - 203510.3.2.1 North America Polymeric Membrane for Separation Market, by Type, 2026 - 2035 (USD Million)10.3.3 North America Polymeric Membrane for Separation Market, by Application, 2026 - 203510.3.3.1 North America Polymeric Membrane for Separation Market, by Application, 2026 - 2035 (USD Million)10.3.4 North America Polymeric Membrane for Separation Market, by End User, 2026 - 203510.3.4.1 North America Polymeric Membrane for Separation Market, by End User, 2026 - 2035 (USD Million)10.3.5 North America Polymeric Membrane for Separation Market, by Material Composition, 2026 - 203510.3.5.1 North America Polymeric Membrane for Separation Market, by Material Composition, 2026 - 2035 (USD Million)10.3.6 North America Polymeric Membrane for Separation Market, by Separation Process, 2026 - 203510.3.6.1 North America Polymeric Membrane for Separation Market, by Separation Process, 2026 - 2035 (USD Million)10.4 Europe10.4.1 Europe Polymeric Membrane for Separation Market, 2026 - 2035 (USD Million)10.4.1.1 Europe Polymeric Membrane for Separation Market, by Country, 2026 - 2035 (USD Million)10.4.2 Europe Polymeric Membrane for Separation Market, by Type, 2026 - 203510.4.2.1 Europe Polymeric Membrane for Separation Market, by Type, 2026 - 2035 (USD Million)10.4.3 Europe Polymeric Membrane for Separation Market, by Application, 2026 - 203510.4.3.1 Europe Polymeric Membrane for Separation Market, by Application, 2026 - 2035 (USD Million)10.4.4 Europe Polymeric Membrane for Separation Market, by End User, 2026 - 203510.4.4.1 Europe Polymeric Membrane for Separation Market, by End User, 2026 - 2035 (USD Million)10.4.5 Europe Polymeric Membrane for Separation Market, by Material Composition, 2026 - 203510.4.5.1 Europe Polymeric Membrane for Separation Market, by Material Composition, 2026 - 2035 (USD Million)10.4.6 Europe Polymeric Membrane for Separation Market, by Separation Process, 2026 - 203510.4.6.1 Europe Polymeric Membrane for Separation Market, by Separation Process, 2026 - 2035 (USD Million)10.5 Asia Pacific10.5.1 Asia Pacific Polymeric Membrane for Separation Market, 2026 - 2035 (USD Million)10.5.1.1 Asia Pacific Polymeric Membrane for Separation Market, by Country, 2026 - 2035 (USD Million)10.5.2 Asia Pacific Polymeric Membrane for Separation Market, by Type, 2026 - 203510.5.2.1 Asia Pacific Polymeric Membrane for Separation Market, by Type, 2026 - 2035 (USD Million)10.5.3 Asia Pacific Polymeric Membrane for Separation Market, by Application, 2026 - 203510.5.3.1 Asia Pacific Polymeric Membrane for Separation Market, by Application, 2026 - 2035 (USD Million)10.5.4 Asia Pacific Polymeric Membrane for Separation Market, by End User, 2026 - 203510.5.4.1 Asia Pacific Polymeric Membrane for Separation Market, by End User, 2026 - 2035 (USD Million)10.5.5 Asia Pacific Polymeric Membrane for Separation Market, by Material Composition, 2026 - 203510.5.5.1 Asia Pacific Polymeric Membrane for Separation Market, by Material Composition, 2026 - 2035 (USD Million)10.5.6 Asia Pacific Polymeric Membrane for Separation Market, by Separation Process, 2026 - 203510.5.6.1 Asia Pacific Polymeric Membrane for Separation Market, by Separation Process, 2026 - 2035 (USD Million)10.6 Latin America10.6.1 Latin America Polymeric Membrane for Separation Market, 2026 - 2035 (USD Million)10.6.1.1 Latin America Polymeric Membrane for Separation Market, by Country, 2026 - 2035 (USD Million)10.6.2 Latin America Polymeric Membrane for Separation Market, by Type, 2026 - 203510.6.2.1 Latin America Polymeric Membrane for Separation Market, by Type, 2026 - 2035 (USD Million)10.6.3 Latin America Polymeric Membrane for Separation Market, by Application, 2026 - 203510.6.3.1 Latin America Polymeric Membrane for Separation Market, by Application, 2026 - 2035 (USD Million)10.6.4 Latin America Polymeric Membrane for Separation Market, by End User, 2026 - 203510.6.4.1 Latin America Polymeric Membrane for Separation Market, by End User, 2026 - 2035 (USD Million)10.6.5 Latin America Polymeric Membrane for Separation Market, by Material Composition, 2026 - 203510.6.5.1 Latin America Polymeric Membrane for Separation Market, by Material Composition, 2026 - 2035 (USD Million)10.6.6 Latin America Polymeric Membrane for Separation Market, by Separation Process, 2026 - 203510.6.6.1 Latin America Polymeric Membrane for Separation Market, by Separation Process, 2026 - 2035 (USD Million)10.7 The Middle-East and Africa10.7.1 The Middle-East and Africa Polymeric Membrane for Separation Market, 2026 - 2035 (USD Million)10.7.1.1 The Middle-East and Africa Polymeric Membrane for Separation Market, by Country, 2026 - 2035 (USD Million)10.7.2 The Middle-East and Africa Polymeric Membrane for Separation Market, by Type, 2026 - 203510.7.2.1 The Middle-East and Africa Polymeric Membrane for Separation Market, by Type, 2026 - 2035 (USD Million)10.7.3 The Middle-East and Africa Polymeric Membrane for Separation Market, by Application, 2026 - 203510.7.3.1 The Middle-East and Africa Polymeric Membrane for Separation Market, by Application, 2026 - 2035 (USD Million)10.7.4 The Middle-East and Africa Polymeric Membrane for Separation Market, by End User, 2026 - 203510.7.4.1 The Middle-East and Africa Polymeric Membrane for Separation Market, by End User, 2026 - 2035 (USD Million)10.7.5 The Middle-East and Africa Polymeric Membrane for Separation Market, by Material Composition, 2026 - 203510.7.5.1 The Middle-East and Africa Polymeric Membrane for Separation Market, by Material Composition, 2026 - 2035 (USD Million)10.7.6 The Middle-East and Africa Polymeric Membrane for Separation Market, by Separation Process, 2026 - 203510.7.6.1 The Middle-East and Africa Polymeric Membrane for Separation Market, by Separation Process, 2026 - 2035 (USD Million)Chapter 11. Company Profiles

11.1 Air Products11.1.1 Overview11.1.2 Financials11.1.3 Product Portfolio11.1.4 Business Strategy11.1.5 Recent Developments11.2 Air Liquide11.2.1 Overview11.2.2 Financials11.2.3 Product Portfolio11.2.4 Business Strategy11.2.5 Recent Developments11.3 UBE Corporation11.3.1 Overview11.3.2 Financials11.3.3 Product Portfolio11.3.4 Business Strategy11.3.5 Recent Developments11.4 Evonik Industries AG11.4.1 Overview11.4.2 Financials11.4.3 Product Portfolio11.4.4 Business Strategy11.4.5 Recent Developments11.5 Grasys11.5.1 Overview11.5.2 Financials11.5.3 Product Portfolio11.5.4 Business Strategy11.5.5 Recent Developments11.6 Schlumberger11.6.1 Overview11.6.2 Financials11.6.3 Product Portfolio11.6.4 Business Strategy11.6.5 Recent Developments11.7 IGS (Innovative Gas Systems)11.7.1 Overview11.7.2 Financials11.7.3 Product Portfolio11.7.4 Business Strategy11.7.5 Recent Developments11.8 Honeywell International Inc.11.8.1 Overview11.8.2 Financials11.8.3 Product Portfolio11.8.4 Business Strategy11.8.5 Recent Developments11.9 MTR (Membrane Technology and Research)11.9.1 Overview11.9.2 Financials11.9.3 Product Portfolio11.9.4 Business Strategy11.9.5 Recent Developments11.10 Borsig GmbH11.10.1 Overview11.10.2 Financials11.10.3 Product Portfolio11.10.4 Business Strategy11.10.5 Recent Developments11.11 Parker Hannifin Corporation11.11.1 Overview11.11.2 Financials11.11.3 Product Portfolio11.11.4 Business Strategy11.11.5 Recent Developments11.12 Tianbang11.12.1 Overview11.12.2 Financials11.12.3 Product Portfolio11.12.4 Business Strategy11.12.5 Recent Developments11.13 SSS (Samsung Separations Systems)11.13.1 Overview11.13.2 Financials11.13.3 Product Portfolio11.13.4 Business Strategy11.13.5 Recent Developments11.14 TriTech11.14.1 Overview11.14.2 Financials11.14.3 Product Portfolio11.14.4 Business Strategy11.14.5 Recent Developments

- North America

Frequently Asked Questions

Polymeric membranes for separation are thin, selective barriers crafted from polymer materials that function as interfaces between phases, allowing controlled passage of specific components in gas or liquid mixtures while offering energy-efficient solutions for processes like filtration, gas purification, and desalination without requiring phase changes.

Key influencing factors include rising demand in water treatment and healthcare sectors, advancements in membrane materials for better durability and selectivity, regulatory pressures for environmental sustainability, expansion in emerging economies, and innovations in hydrogen and carbon capture technologies, though tempered by raw material volatility and competition from alternatives.

The market value is projected to increase from approximately USD 651 million in 2025 to USD 854 million by 2035, driven by steady industrial adoption and technological improvements.

The CAGR is expected to be 3.6% during the period from 2026 to 2035.

North America will contribute notably, holding about 40% of the global market value, primarily due to its advanced industrial infrastructure and focus on energy and environmental applications.

The major players include Air Products, Air Liquide, UBE Corporation, Evonik Industries AG, and Grasys, which together hold about 75% market share and drive growth through R&D, capacity expansions, and specialized gas separation solutions.

The report provides comprehensive insights into market size, growth trends, segmentation analysis, regional outlooks, competitive landscape, technology trends, market dynamics including drivers and challenges, opportunities, and recommendations for stakeholders.

The value chain includes upstream raw material sourcing (e.g., polysulfone and polyimide polymers), membrane manufacturing and module assembly, distribution through suppliers and agents, downstream integration into end-user applications like gas processing and water treatment, and after-sales services for maintenance and optimization.

Market trends are shifting toward sustainable and high-performance materials like mixed-matrix and thermally rearranged polymers, while consumer preferences favor energy-efficient, fouling-resistant membranes that support green initiatives in hydrogen production and carbon capture, with increasing demand for customizable solutions in industrial sectors.

Regulatory factors include stringent emissions standards and sustainability directives promoting carbon capture and clean water access, while environmental concerns like climate change drive adoption for CO2 removal and wastewater treatment, though challenges arise from raw material sustainability and waste management in production.