Smart Electric Meter Market Size, Share and Trends 2026 to 2035

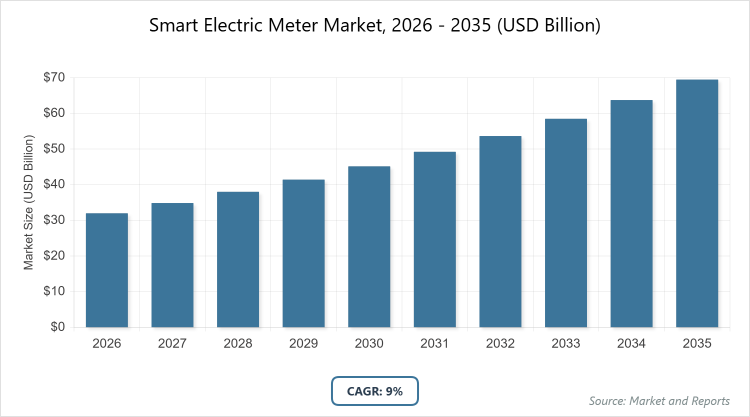

The global Smart Electric Meter Market size was estimated at USD 32 Billion in 2025 and is expected to reach USD 80 Billion by 2035, growing at a CAGR of 9% from 2026 to 2035. The Smart Electric Meter market is primarily driven by government mandates for grid modernization and the increasing global demand for energy efficiency and real-time data integration.

What are the Key Insights?

- Market Value: The Smart Electric Meter Market is projected to grow from approximately USD 32 billion in 2026 to USD 80 billion by 2035.

- CAGR: The market is expected to register a CAGR of around 9% during the forecast period from 2026 to 2035.

- Dominated Subsegment by Type: Advanced Metering Infrastructure (AMI) dominates the type segment.

- Dominated Subsegment by Phase: Three-phase meters dominate the phase segment.

- Dominated Subsegment by End-Use: Residential applications dominate the end-use segment.

- Dominated Region: Asia Pacific leads the global market.

What is the Industry Overview?

The Smart Electric Meter Market encompasses advanced metering infrastructure designed to measure, collect, and analyze electricity consumption data in real-time, replacing traditional analog meters with digital devices that enable two-way communication between utilities and consumers. These meters integrate sensors, communication modules, and data management systems to provide accurate billing, detect outages, monitor power quality, and support demand-response programs, ultimately facilitating efficient energy management and grid optimization. This market serves residential, commercial, and industrial sectors by promoting energy conservation, reducing operational costs for utilities, and enabling integration with smart grid technologies, renewable energy sources, and IoT ecosystems, thereby transforming how electricity is distributed and consumed in modern power systems.

What are the Market Dynamics?

Growth Drivers

The primary growth drivers for the Smart Electric Meter Market include increasing government mandates and incentives for smart grid deployments, rising demand for energy efficiency amid escalating global energy consumption, and the integration of renewable energy sources that require precise monitoring and management. Advancements in IoT and communication technologies, such as 5G and RF mesh networks, further propel adoption by enabling seamless data transmission and remote management, while utilities seek to minimize non-technical losses like theft and inaccuracies in billing, driving widespread implementation across developed and emerging economies.

Restraints

Key restraints in the Smart Electric Meter Market stem from high initial installation and infrastructure costs, which can deter adoption in cost-sensitive regions, alongside concerns over data privacy and cybersecurity vulnerabilities that expose meters to hacking risks and potential grid disruptions. Additionally, interoperability issues between different meter technologies and legacy systems pose integration challenges, while regulatory hurdles and varying standards across countries slow down large-scale rollouts, limiting market penetration in underdeveloped areas with inadequate supporting infrastructure.

Opportunities

Opportunities in the Smart Electric Meter Market arise from the expanding adoption of electric vehicles and distributed energy resources, creating demand for advanced meters capable of handling bidirectional power flows and vehicle-to-grid interactions. Emerging markets in Asia and Africa present untapped potential for massive deployments driven by urbanization and electrification initiatives, while innovations in AI-driven analytics and predictive maintenance open avenues for value-added services, allowing utilities to offer dynamic pricing and energy optimization solutions to consumers.

Challenges

Challenges facing the Smart Electric Meter Market include the need for skilled workforce training to handle installation and maintenance, as well as addressing consumer resistance due to perceived privacy intrusions and health concerns related to radiofrequency emissions. Supply chain disruptions for critical components like semiconductors, coupled with the complexity of upgrading existing grids without service interruptions, further complicate market expansion, requiring collaborative efforts from stakeholders to standardize protocols and ensure reliable long-term performance.

Smart Electric Meter Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Smart Electric Meter Market |

| Market Size 2025 | USD 32 Billion |

| Market Forecast 2035 | USD 80 Billion |

| Growth Rate | CAGR of 9% |

| Report Pages | 215 |

| Key Companies Covered |

Itron, Landis+Gyr, Siemens, Schneider Electric, Honeywell, and ABB. |

| Segments Covered | By Type, By Phase, By End-Use, By Region |

| Regions Covered | Asia Pacific, North America, Europe, Latin America, The Middle East and Africa |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation?

By type, primarily into Advanced Metering Infrastructure (AMI) and Automated Meter Reading (AMR), with AMI being the most dominant due to its two-way communication capabilities that enable real-time data exchange, remote control, and advanced analytics, driving market growth by supporting smart grid initiatives and demand-side management. The second most dominant is AMR, which offers one-way communication for automated data collection, appealing to utilities transitioning from manual readings but lacking the full interactivity of AMI; AMI’s dominance stems from its ability to reduce operational costs, enhance grid reliability, and integrate with IoT for predictive maintenance, thereby accelerating overall market expansion through improved energy efficiency and consumer engagement.

In terms of phase segmentation, three-phase meters are the most dominant, catering to commercial and industrial users with higher power demands, providing accurate measurement for complex loads and facilitating better voltage regulation, which drives the market by addressing the needs of growing industrialization and urbanization. Single-phase meters rank as the second most dominant, primarily used in residential settings for simpler household consumption tracking; three-phase’s lead is attributed to its robustness in handling large-scale applications, contributing to market growth by enabling utilities to manage diverse energy profiles and support renewable integration in high-demand sectors.

The end-use, segmentation sees residential as the most dominant, driven by widespread government rollouts for household energy monitoring, accurate billing, and conservation programs, which propel the market through mass adoption and reduced non-technical losses. Commercial follows as the second most dominant, focusing on businesses requiring detailed usage insights for cost control; residential’s prominence helps drive the market by empowering consumers with data-driven decisions, fostering energy savings, and aligning with global sustainability goals to expand utility revenues through value-added services.

What are the Recent Developments?

- In 2024, Itron announced the expansion of its intelligent connectivity platform with enhanced cybersecurity features, partnering with utilities in North America to deploy over 1 million AMI meters, aiming to improve grid resilience against cyber threats while enabling real-time outage detection and response.

- Landis+Gyr launched a new series of three-phase smart meters integrated with AI analytics in early 2025, collaborating with European energy providers to pilot programs that optimize demand response, resulting in significant energy savings and positioning the company as a leader in sustainable grid solutions.

- Siemens introduced IoT-enabled smart metering solutions in mid-2025, focusing on Asia Pacific markets through strategic alliances with local governments, facilitating large-scale installations in urban areas to support smart city initiatives and reduce carbon emissions.

- In late 2025, Schneider Electric acquired a startup specializing in RF communication technologies, enhancing its portfolio to offer hybrid AMI-AMR systems, which were deployed in pilot projects across Africa to address electrification challenges in remote regions.

- Honeywell rolled out advanced data analytics software for smart meters in 2026, integrating with existing infrastructure to provide predictive maintenance insights, and formed partnerships with U.S. utilities to upgrade aging grids, boosting operational efficiency and market penetration.

What is the Regional Analysis?

Asia Pacific dominates the Smart Electric Meter Market, driven by rapid urbanization, government-led smart grid projects, and massive investments in infrastructure, with China as the leading country due to its nationwide rollout of over a billion meters, supported by policies like the “Made in China 2025” initiative that emphasizes energy efficiency and renewable integration, enabling utilities to minimize losses and accommodate growing electricity demand from industrial and residential sectors.

North America holds a significant share in the market, fueled by regulatory mandates for energy conservation and advanced metering adoption, with the United States as the dominant country through initiatives like the Smart Grid Investment Grant program, which has led to widespread deployments by utilities to enhance grid reliability, integrate renewables, and provide consumers with real-time usage data for better management.

Europe is experiencing steady growth in the Smart Electric Meter Market, propelled by EU directives on energy efficiency and carbon reduction targets, with Germany leading the region via its Energiewende transition, involving extensive meter installations to support decentralized energy systems, smart homes, and electric vehicle charging networks, thereby reducing dependency on fossil fuels.

Latin America is emerging in the market with increasing focus on reducing non-technical losses and improving billing accuracy, where Brazil dominates through national programs like the Brazilian Smart Meter Initiative, deploying meters in urban areas to combat electricity theft and enhance service quality amid rising energy demands from economic development.

The Middle East and Africa region shows potential for growth amid electrification efforts and smart city developments, with South Africa as the key player through Eskom’s smart metering projects aimed at addressing power outages and load shedding, integrating meters with renewable sources to stabilize grids in resource-constrained environments.

Who are the Key Market Players and Their Strategies?

- Itron focuses on innovation through its Gen5 Riva platform, emphasizing edge intelligence and distributed computing to enable real-time analytics, while expanding via acquisitions and partnerships with utilities for large-scale AMI deployments.

- Landis+Gyr employs strategies centered on sustainability, developing modular meters with renewable integration capabilities, and pursuing global collaborations to enter emerging markets, enhancing its portfolio with cloud-based management systems.

- Siemens leverages digitalization strategies, integrating smart meters with its MindSphere IoT platform for predictive maintenance, and invests in R&D for cybersecurity, forming alliances with governments for smart grid projects.

- Schneider Electric adopts a strategy of ecosystem building, offering end-to-end solutions via its EcoStruxure platform, acquiring tech firms to bolster communication technologies, and targeting industrial sectors for energy optimization.

- Honeywell prioritizes data-driven strategies, incorporating AI in its metering solutions for demand forecasting, and expands through strategic joint ventures in high-growth regions to provide integrated building management systems.

- ABB focuses on electrification strategies, developing meters with advanced power quality monitoring, and collaborates with utilities on pilot programs to demonstrate efficiency gains in renewable-heavy grids.

What are the Market Trends?

- Integration of AI and machine learning for predictive analytics and anomaly detection in energy consumption patterns.

- Rising adoption of IoT-enabled meters for seamless connectivity with smart home devices and electric vehicles.

- Shift towards hybrid communication technologies combining RF, PLC, and cellular for improved reliability in diverse terrains.

- Emphasis on cybersecurity features to protect against increasing threats to grid infrastructure.

- Growing focus on sustainability with meters supporting bidirectional flows for renewable energy integration.

- Expansion of demand-response programs enabling dynamic pricing and consumer participation in energy management.

- Increasing use of cloud-based platforms for data storage and remote meter management.

What Market Segments are Covered in the Report?

- By Type

- Advanced Metering Infrastructure (AMI)

- Automated Meter Reading (AMR)

- By Phase

- Single-Phase

- Three-Phase

- By End-Use

- Residential

- Commercial

- Industrial

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Smart Electric Meter Market - Industry Analysis

Chapter 4. Global Smart Electric Meter Market- Competitive Landscape

Chapter 5. Global Smart Electric Meter Market - Type Analysis

Chapter 6. Global Smart Electric Meter Market - Phase Analysis

Chapter 7. Global Smart Electric Meter Market - End-Use Analysis

Chapter 8. Smart Electric Meter Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

The Smart Electric Meter Market refers to the industry involved in the production, distribution, and deployment of digital meters that measure electricity usage in real-time, enabling two-way communication for efficient energy management, accurate billing, and grid optimization.

Key factors include government regulations promoting smart grids, rising energy efficiency demands, integration with renewables and EVs, advancements in IoT and AI technologies, and efforts to reduce non-technical losses, all driving adoption across sectors.

The market is projected to grow from approximately USD 32 billion in 2026 to around USD 80 billion by 2035, reflecting steady expansion through technological advancements and global deployments.

The CAGR is expected to be around 9% during 2026-2035, fueled by increasing investments in smart infrastructure and energy management solutions.

Asia Pacific will contribute notably, driven by rapid urbanization, large-scale government initiatives, and high energy demand in countries like China and India.

Major players include Itron, Landis+Gyr, Siemens, Schneider Electric, Honeywell, and ABB, who drive growth through innovation, strategic partnerships, and expansion into emerging markets.

The report provides comprehensive insights into market size, growth drivers, segmentation, regional analysis, key players, trends, and forecasts, offering stakeholders actionable data for decision-making.

The value chain includes component manufacturing (sensors, chips), meter assembly, software development for data management, distribution and installation by utilities, and end-user services like maintenance and analytics.

Trends are shifting towards AI-integrated meters for predictive insights, while consumers prefer user-friendly apps for real-time monitoring, energy savings tips, and integration with smart homes, emphasizing sustainability and convenience.

Regulatory factors include mandates for smart meter rollouts and energy efficiency standards, while environmental factors involve carbon reduction goals and renewable integration, both accelerating growth by promoting sustainable energy practices.