Electrical Insulation Materials Market Size, Share and Trends 2026 to 2035

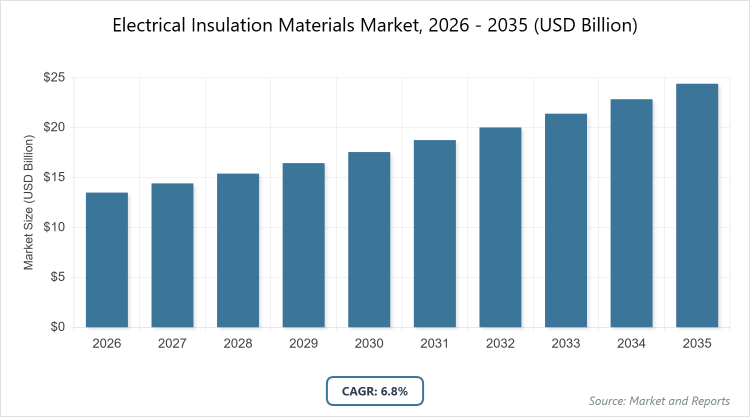

The global Electrical Insulation Materials Market size was estimated at USD 13.5 Billion in 2025 and is expected to reach USD 24 Billion by 2035, growing at a CAGR of 6.8% from 2026 to 2035.The Electrical Insulation Materials Market is primarily driven by the surging global demand for electricity, the rapid expansion of renewable energy infrastructure, and the accelerated adoption of electric vehicles requiring high-performance thermal and electrical management.

What are the Key Insights?

- Market Value in 2026: USD 13.5 billion

- Market Value in 2035: USD 24 billion

- CAGR (2026-2035): 6.8%

- Dominant Subsegment by Material Type: Thermosets

- Second Dominant Subsegment by Material Type: Thermoplastics

- Dominant Subsegment by Application: Wires & Cables

- Second Dominant Subsegment by Application: Power Systems (including Transformers and Motors)

- Dominant Subsegment by Voltage: High Voltage

- Second Dominant Subsegment by Voltage: Medium Voltage

- Dominant Subsegment by End-User: Energy and Power

- Second Dominant Subsegment by End-User: Electronics

- Dominant Region: Asia Pacific

What is the Industry Overview?

The Electrical Insulation Materials Market encompasses materials designed to prevent the unwanted flow of electric current, providing high resistivity, dielectric strength, and thermal stability to ensure safety and efficiency in electrical systems. These materials, including polymers, ceramics, and composites, are essential in applications such as wires, cables, transformers, motors, and electronic devices, supporting industries like power generation, renewable energy, automotive, and consumer electronics by isolating conductive parts and minimizing energy loss.

What are the Market Dynamics?

Growth Drivers

The growth of the Electrical Insulation Materials Market is propelled by increasing investments in energy infrastructure and grid modernization, rising demand for electric vehicles and renewable energy sources like solar and wind, which require advanced insulation for efficiency and safety, technological advancements in high-performance materials such as nanocomposites and thermoplastics that offer superior thermal and electrical resistance, stringent regulatory standards emphasizing electrical safety and environmental sustainability, and the expansion of the electronics sector driven by urbanization and industrialization in emerging markets.

Restraints

The market faces restraints from fluctuating raw material prices, including resins and petrochemicals, which increase production costs and affect profitability, intense competition from low-quality, cheap products offered by unorganized players that compromise safety and lead to higher maintenance expenses, high initial costs for advanced insulation solutions that limit adoption by smaller enterprises, and supply chain disruptions exacerbated by global events like pandemics, which delay manufacturing and distribution.

Opportunities

Opportunities in the market arise from the development of eco-friendly, bio-based, and recyclable insulation materials aligned with global sustainability goals, expansion into emerging markets with growing infrastructure needs for tailored high-voltage solutions, investments in R&D for innovative materials like halogen-free polymers and high-temperature composites suitable for electric vehicles and smart grids, and the integration of smart technologies in electrical systems that demand enhanced functionality and reliability.

Challenges

Challenges include balancing cost-effectiveness with performance requirements in developing regions where immediate infrastructure demands prioritize affordability over advanced features, navigating volatile raw material supply chains that impact pricing and availability, adhering to stringent environmental regulations that necessitate shifts to sustainable materials without compromising quality, and overcoming the presence of grey market products that undermine trust and brand reputation in competitive landscapes.

Electrical Insulation Materials Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Electrical Insulation Materials Market |

| Market Size 2025 | USD 13.5 Billion |

| Market Forecast 2035 | USD 24 Billion |

| Growth Rate | CAGR of 6.8% |

| Report Pages | 215 |

| Key Companies Covered |

DuPont, 3M, Elantas, Nitto Denko Corporation, and Siemens Energy. |

| Segments Covered | By Material Type, By Application, By Voltage, By End-User, By Region |

| Regions Covered | Asia Pacific, North America, Europe, Latin America, The Middle East and Africa |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation?

By Material Type

The most dominant segment is thermosets, followed by thermoplastics as the second most dominant. Thermosets dominate due to their exceptional thermal stability, durability, and high dielectric strength, making them ideal for demanding applications in power transformers and high-voltage systems where they withstand extreme temperatures and mechanical stresses, driving the market by enabling reliable performance in renewable energy and electric vehicle infrastructures that require long-lasting insulation to reduce energy losses and enhance system efficiency; thermoplastics, as the second dominant, offer flexibility, chemical resistance, and recyclability, which appeal to cost-sensitive sectors like wires and cables, contributing to market growth through their ease of processing and adaptability in expanding electronics and automotive industries, supporting broader adoption in sustainable and lightweight designs.

By Application

The most dominant segment is wires & cables, with power systems (including transformers and motors) as the second most dominant. Wires & cables lead because of the surging demand for efficient power transmission and distribution in grid modernization and electrification projects, where these materials prevent leakage and ensure safety in high-volume infrastructure developments, propelling the market by facilitating the integration of renewable energy sources and smart grids that rely on robust cabling to minimize downtime and optimize energy flow; power systems rank second due to the need for insulation in transformers and motors that handle high loads in industrial and utility settings, driving growth by supporting the refurbishment of aging electrical networks and the rise of electric vehicles, which demand high-performance materials to improve operational reliability and energy efficiency.

By Voltage

The most dominant segment is high voltage, followed by medium voltage as the second most dominant. High voltage dominates owing to its critical role in long-distance power transmission and renewable energy applications like wind and solar farms, where materials must provide superior insulation against breakdowns under extreme conditions, fueling market expansion by enabling efficient HVDC systems that reduce transmission losses and support global energy transition initiatives; medium voltage, as the second dominant, is essential for distribution networks and industrial equipment, contributing to growth through its use in urban infrastructure and manufacturing, where it balances cost and performance to drive adoption in emerging markets focused on electrification and grid upgrades.

By End-User

The most dominant segment is energy and power, with electronics as the second most dominant. Energy and power leads because of massive investments in grid infrastructure, renewable sources, and power generation facilities that require reliable insulation to ensure safety and minimize losses, accelerating market growth by addressing the global push for sustainable energy solutions and smart grid technologies; electronics ranks second due to the booming demand for consumer devices, smart appliances, and data centers, where compact and heat-resistant materials enhance component longevity, propelling the market through innovation in miniaturized systems and the integration of IoT, supporting rapid advancements in digitalization.

What are the Recent Developments?

- In May 2025, DuPont announced plans to separate into three independent companies focused on electronics, water, and diversified materials to streamline operations and accelerate growth in high-performance insulation for electric vehicles and renewables.

- In June 2025, DuPont acquired Donatelle Plastics Inc. to bolster its capabilities in healthcare and electronics, enhancing its portfolio of advanced polymer-based insulation solutions for specialized applications.

- In October 2025, 3M opened a Skills Development Center in Minnesota, aimed at training in automotive electrification, which indirectly supports innovation in EV insulation materials.

- In January 2025, Siemens Energy launched eco-friendly insulation materials for renewable energy projects, emphasizing sustainability in high-voltage applications for smart grids.

- In November 2025, Siemens Energy introduced high-voltage insulation for digital transformers, improving efficiency in power distribution networks.

- In April 2022, Von Roll expanded its site in Italy to increase production and R&D for potting resins used in automotive and electronics insulation.

- In May 2022, Krempel partnered with DuPont for exclusive production of Nomex 910, a high-quality cellulose-based insulation material strengthening its position in electrical applications.

What is the Regional Analysis?

North America exhibits steady growth driven by advanced R&D, strong regulatory frameworks for energy efficiency, and significant investments in electric vehicles and renewable energy infrastructure, with the United States dominating due to its leadership in innovation, presence of major players like 3M and DuPont, and government incentives such as EV tax credits that boost demand for high-performance insulation in smart grids and automotive sectors, while Canada contributes through its focus on sustainable power generation, overall supporting regional market expansion through technological advancements and a mature electronics industry.

Europe experiences moderate to high growth fueled by the EU Green Deal’s emphasis on sustainability, energy transition, and renewable integration, with Germany dominating as a hub for industrial manufacturing and clean energy initiatives like energiewende, where companies like Siemens and Elantas drive innovation in high-voltage insulation for wind farms and grid modernization, while France and the UK add momentum through infrastructure upgrades and EV adoption, collectively propelling the region with a focus on eco-friendly materials and stringent environmental standards that enhance market competitiveness.

Asia Pacific is the fastest-growing region, propelled by rapid industrialization, urbanization, and massive infrastructure investments in power grids and electronics, with China dominating through its vast manufacturing base, government-backed renewable energy projects, and leadership in electric vehicle production, where local players like Vitar and global firms like Nitto Denko supply cost-effective materials for wires, cables, and high-voltage applications, while India and Japan contribute via expanding automotive and telecom sectors, driving overall market surge through high demand for affordable, high-performance insulation in emerging economies.

Latin America shows promising growth with increasing electrification and renewable energy adoption, particularly in non-hydro sources, with Brazil dominating due to its large-scale grid expansions, investments in solar and wind projects, and industrial demand for insulation in power systems, supported by players focusing on regional partnerships, while Mexico adds value through its proximity to North American supply chains and automotive manufacturing, fostering market development amid economic recovery and infrastructure modernization efforts.

The Middle East & Africa region registers higher potential growth from infrastructure investments and energy diversification, with the UAE dominating through ambitious projects in smart cities and renewable energy like solar farms, where insulation materials ensure reliability in harsh environments, supported by collaborations with global players, while South Africa contributes via power sector reforms and grid upgrades, overall advancing the market by addressing capacity shortages and promoting electrical safety standards in untapped markets.

Who are the Key Market Players and Their Strategies?

DuPont: Focuses on R&D for eco-friendly polymers and expansions like polyimide film production for EVs, alongside acquisitions to enhance electronics capabilities and partnerships for sustainable solutions.

3M: Emphasizes high-performance materials for energy efficiency, with strategies including partnerships for EV insulation and investments in training centers to drive innovation in automotive and renewable applications.

Elantas: Pursues technological advancements in resins and varnishes, with a focus on regulatory compliance and expansions in high-voltage markets through joint ventures.

Nitto Denko Corporation: Leads in cost-effective innovations, localizing manufacturing in Asia and investing in R&D for temperature-resistant films used in electronics and power systems.

Siemens Energy: Expands manufacturing for high-voltage materials, launches eco-friendly products for smart grids, and forms alliances to optimize supply chains in renewables.

General Electric: Integrates digital transformation in insulation solutions, focusing on smart grid technologies and reliability for power generation.

Von Roll: Invests in site expansions for potting resins, targeting automotive and electronics growth through enhanced production and customer experience centers.

Krempel GmbH: Engages in exclusive partnerships like with DuPont for specialized cellulose materials, strengthening its position in electrical grade insulation.

ABB: Optimizes digital solutions and supply chains, securing contracts for grid projects with advanced insulation.

Mitsubishi Electric: Innovates for regional demands in high-reliability systems, expanding in Asia for EV and telecom applications.

What are the Market Trends?

- Shift towards sustainable, bio-based, and halogen-free materials to meet environmental regulations and reduce carbon footprints.

- Increasing adoption of nanocomposites and high-temperature polymers for enhanced performance in renewable energy and EVs.

- Growth in EV-specific insulation for batteries and motors, driven by rising electric vehicle sales globally.

- Integration of smart grid technologies requiring advanced, flexible insulation for efficiency and reliability.

- Expansion of wires & cables segment due to grid modernization and electrification in developing regions.

- Focus on recyclability and energy-efficient materials to align with global sustainability goals.

- Rising demand from data centers and telecommunications for compact, heat-resistant insulation.

- Technological advancements in ceramics with properties like superconductivity and piezoelectricity for specialized applications.

What Market Segments are Covered in the Report?

- By Material Type

- Thermoplastics

- Thermosets

- Ceramics

- Composites

- Fiber Glass

- Mica

- Others

- By Application

- Wires & Cables

- Power Systems (Transformers, Motors, Generators)

- Electronics Appliances

- Switchgears

- Batteries

- Others

- By Voltage

- Low Voltage

- Medium Voltage

- High Voltage

- By End-User

- Energy and Power

- Electronics

- Automotive

- Aerospace

- Construction

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Electrical Insulation Materials Market - Industry Analysis

Chapter 4. Global Electrical Insulation Materials Market- Competitive Landscape

Chapter 5. Global Electrical Insulation Materials Market - Material Type Analysis

Chapter 6. Global Electrical Insulation Materials Market - Application Analysis

Chapter 7. Global Electrical Insulation Materials Market - Voltage Analysis

Chapter 8. Global Electrical Insulation Materials Market - End-User Analysis

Chapter 9. Electrical Insulation Materials Market - Regional Analysis

Chapter 10. Company Profiles

Frequently Asked Questions

The Electrical Insulation Materials Market refers to the industry involved in producing and distributing materials that prevent electrical conduction, ensuring safety and efficiency in systems like power grids, electronics, and vehicles.

Key factors include rising demand for EVs and renewables, grid modernization, technological advancements in sustainable materials, regulatory standards for safety, and expansion in emerging markets.

The market is projected to grow from USD 13.5 billion in 2026 to USD 24 billion by 2035.

The CAGR is expected to be 6.8% during 2026-2035.

Asia Pacific will contribute notably, driven by industrialization and infrastructure growth.

Major players include DuPont, 3M, Elantas, Nitto Denko Corporation, and Siemens Energy.

The report provides comprehensive insights into market size, segmentation, dynamics, regional analysis, key players, trends, and forecasts.

The value chain includes raw material sourcing, manufacturing, distribution, end-use application, and recycling or disposal.

Trends are shifting towards eco-friendly and high-performance materials, with consumers preferring sustainable, recyclable options for EVs and renewables.

Stringent safety standards, environmental regulations promoting halogen-free and bio-based materials, and incentives for energy efficiency are key influencers.