Gasoline Direct Injection (GDI) System Market Size, Share and Trends 2026 to 2035

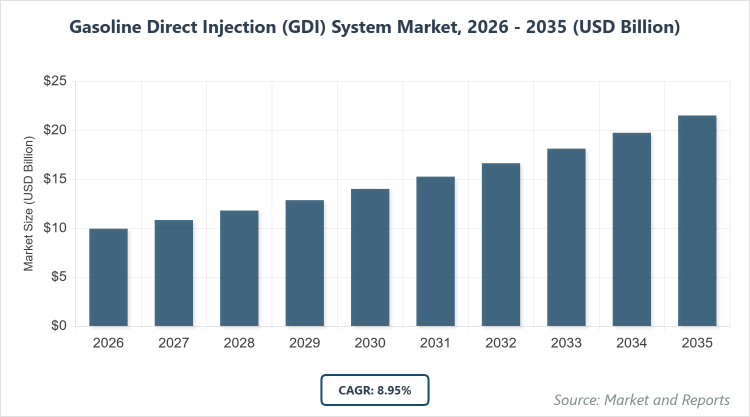

According to MarketnReports, the global gasoline direct injection (GDI) system market size was estimated at USD 9.95 billion in 2025 and is expected to reach USD 21.43 billion by 2035, growing at a CAGR of 8.95% from 2026 to 2035. Gasoline Direct Injection (GDI) System Market is driven by stringent global government regulations mandating improved vehicle fuel economy and reduced emissions, coupled with the automotive industry’s widespread adoption of engine downsizing and turbocharging strategies to enhance efficiency without sacrificing performance.

What are the Key Insights into the Gasoline Direct Injection (GDI) System Market?

- Global gasoline direct injection (GDI) system market valued at approximately USD 9.95 billion in 2026, projected to reach USD 21.43 billion by 2035.

- Expected CAGR of around 8.95% from 2026 to 2035, driven by emission regulations and engine efficiency demands.

- Dominant subsegment by component: Fuel injectors, accounting for the largest share due to critical role in precision delivery.

- Dominant subsegment by vehicle type: Passenger cars, holding over 70% market share for widespread adoption in sedans and SUVs.

- Dominant region: Asia-Pacific, contributing over 37% of global revenue with China as the leading country.

What is the Gasoline Direct Injection (GDI) System Industry Overview?

Industry Overview

Gasoline Direct Injection (GDI) systems are advanced fuel delivery technologies that inject gasoline directly into the combustion chamber of an engine at high pressure, enabling precise control over fuel-air mixture for improved efficiency, power output, and reduced emissions compared to traditional port fuel injection methods. These systems consist of components like fuel injectors, high-pressure pumps, rails, sensors, and electronic control units that work together to optimize combustion, making them essential in modern automotive engines for passenger cars, commercial vehicles, and hybrids where they enhance throttle response and fuel economy while meeting stringent environmental standards.

GDI systems are typically categorized by engine type, component, and vehicle application, emphasizing durability for high-pressure operations and integration with turbochargers for downsized engines. The industry involves raw material suppliers for precision parts, manufacturers employing advanced machining and testing for reliability, and assemblers integrating with vehicle OEMs, prioritizing innovation to address issues like carbon buildup through improved designs. This market is driven by the global push for fuel-efficient vehicles, emission regulations, and electrification trends, balancing performance gains with challenges in maintenance and cost in a competitive landscape focused on sustainability and technological convergence.

What are the Market Dynamics in the Gasoline Direct Injection (GDI) System Sector?

Growth Drivers

The gasoline direct injection (GDI) system market is propelled by stringent global emission regulations, such as Euro 7 and CAFE standards, compelling automakers to adopt GDI for better combustion efficiency and lower CO2 outputs, supported by the rise in turbocharged engines that leverage GDI for enhanced power density and fuel economy in downsized powertrains amid electrification trends.

Increasing consumer demand for high-performance vehicles with improved throttle response and mileage drives adoption in passenger cars, while government incentives for green technologies accelerate integration in hybrids and plug-ins. Technological advancements in high-pressure injectors and electronic controls reduce particulate emissions, attracting investments from OEMs, and the expansion of automotive production in emerging economies further boosts demand for cost-effective GDI solutions.

Restraints

High development and maintenance costs for GDI systems, including specialized components and cleaning to prevent carbon deposits, limit penetration in price-sensitive markets where port injection suffices for basic engines, exacerbated by supply chain issues for rare materials like piezoelectric injectors. Regulatory challenges in addressing particulate emissions require additional filters like GPF, increasing vehicle prices and complexity. Volatility in fuel quality in developing regions causes operational issues, while competition from electric powertrains diverts investments away from ICE improvements. Limited infrastructure for high-octane fuels optimal for GDI hinders full potential in some areas.

Opportunities

Opportunities emerge from the hybridization trend, with GDI enabling efficient Atkinson cycles in HEVs and PHEVs for extended range, supported by R&D funding for multi-injection strategies to minimize emissions. Expansion into alternative fuels like biofuels and hydrogen blends presents growth in sustainable mobility, while partnerships for localized manufacturing in Asia reduce costs. Innovations in dual-injection systems combining GDI with port injection open niches in performance vehicles, and government subsidies for low-emission tech unlock bulk contracts in Europe and North America. Digital twins for system optimization enable faster development, fostering competitive edges.

Challenges

Achieving consistent performance across fuel qualities and climates poses challenges, requiring robust designs to prevent injector fouling amid varying standards. Navigating emission regulations demands continuous R&D for particulate reduction, while intellectual property disputes in injector tech slow innovations. Supply dependencies on critical minerals for components expose vulnerabilities to geopolitical risks, and talent shortages for advanced engineering demand training. Balancing fuel efficiency with power in downsized engines remains a hurdle amid consumer expectations.

Gasoline Direct Injection (GDI) System Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Gasoline Direct Injection (GDI) System Market |

| Market Size 2025 | USD 9.95 billion |

| Market Forecast 2035 | USD 21.43 billion |

| Growth Rate | CAGR of 8.95% |

| Report Pages | 235 |

| Key Companies Covered | Robert Bosch GmbH, Denso Corporation, Continental AG, Delphi Technologies, Magneti Marelli, Hitachi Astemo, and Stanadyne LLC. |

| Segments Covered | By Component, Vehicle Type, and Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Gasoline Direct Injection (GDI) System Market Segmented?

The Gasoline Direct Injection (GDI) System market is segmented by component, vehicle type, and region.

By Component, The fuel injectors segment dominates the GDI system market, primarily because of their essential function in high-pressure fuel delivery for optimal atomization and combustion, making them indispensable for efficiency and emission control where precision engineering ensures performance in modern engines, supported by advancements in multi-hole designs. This dominance drives the market by enabling compliance with stringent regulations, fostering innovations in durability against deposits, and attracting OEM investments for customized solutions, thereby expanding adoption across vehicle types through enhanced reliability.

The electronic control units segment ranks second, crucial for real-time monitoring and adjustment of injection timing, helping to propel market growth by integrating with sensors for adaptive strategies, improving fuel economy in hybrids, and supporting software updates in connected vehicles.

By Vehicle Type, Passenger cars lead the vehicle type segment, as GDI systems optimize fuel efficiency and power in compact engines, driven by consumer demand for eco-friendly sedans and SUVs where downsizing trends require advanced injection for performance. This subsegment drives the market by aligning with global electrification, promoting turbo-GDI combinations for better mileage, and complying with emission norms, thus increasing demand in mass production. Commercial vehicles follow as the second dominant, essential for heavy-duty efficiency in trucks where GDI reduces operating costs, contributing to market expansion through fleet modernizations, enhancing durability under loads, and tapping into logistics growth.

What are the Recent Developments in the Gasoline Direct Injection (GDI) System Market?

- In January 2024, Standard Motor Products, Inc. launched a new GDI unit Fuel Injection Program, expanding its aftermarket offerings with high-pressure injectors designed for durability and performance, targeting repair shops in North America to meet growing demand for replacement parts in aging GDI vehicles.

- In July 2023, Stanadyne LLC introduced its patented Goliath 350-bar GDI performance fuel injector to the aftermarket, featuring enhanced flow rates and atomization for high-performance engines, strengthening its position in specialty markets and addressing emission challenges in turbocharged applications.

- In December 2023, Stanadyne LLC expanded its performance portfolio with the Goliath 350-bar GDI durability fuel injector, optimized for long-term reliability in commercial vehicles, boosting adoption in fleet operations across Europe and Asia.

- In March 2025, Honda Motor Corporation developed a new naturally aspirated in-line 4-cylinder direct injection gasoline engine, incorporating advanced GDI for improved efficiency, aimed at hybrid models to enhance fuel economy and reduce emissions in global markets.

What is the Regional Analysis of the Gasoline Direct Injection (GDI) System Market?

- Asia-Pacific to dominate the market

Asia-Pacific dominates the global gasoline direct injection (GDI) system market, driven by massive automotive production, stringent emission norms, and rapid EV hybridization, with China as the dominating country due to its vast manufacturing base producing over 25 million vehicles annually, government policies like the New Energy Vehicle mandate promoting efficient ICE tech, and leadership in exports through companies like Denso and Bosch local operations.

The region’s growth is supported by India’s fuel efficiency standards and Japan’s turbo-GDI advancements; South Korea’s hybrid focus contributes, but China’s dominance stems from its integrated supply chains, low-cost innovations, and policy-driven subsidies, boosting revenue through high-volume passenger and commercial vehicle applications amid urbanization and air quality concerns.

North America holds a substantial share in the gasoline direct injection (GDI) system market, characterized by high adoption in performance vehicles and regulatory focus on CAFE standards, with the United States as the dominating country owing to its EPA emission rules, consumer demand for efficient SUVs, and major players like Delphi and Stanadyne driving aftermarket innovations for over 17 million annual vehicle sales. The region benefits from Canada’s resource sectors; the U.S. leads with investments in hybrid GDI, enhancing market expansion via premium integrations in trucks and sedans.

Europe exhibits steady growth in the gasoline direct injection (GDI) system market, focused on Euro 7 compliance and sustainable mobility, with Germany as the dominating country due to its automotive heritage, EU Green Deal initiatives, and firms like Bosch and Continental advancing turbo-GDI for low-emission engines in luxury brands. The region is propelled by the UK’s electrification and France’s diesel shift; Germany’s leadership arises from exports and R&D in composites, fostering market development by addressing decarbonization.

The Rest of the World shows emerging potential in the gasoline direct injection (GDI) system market, with Brazil dominating in Latin America through ethanol blends and flex-fuel vehicles, while UAE leads in the Middle East with luxury imports. Growth is driven by Africa’s fleet modernizations; the region’s progress relies on foreign investments, increasing share in commercial sectors.

Who are the Key Market Players and Their Strategies in the Gasoline Direct Injection (GDI) System Industry?

Robert Bosch GmbH: Focuses on high-pressure injection innovations, expanding through R&D for turbo-GDI and acquisitions to lead in emission-compliant systems.

Denso Corporation: Emphasizes hybrid integrations, investing in Asia expansions and sensor tech for precise control in passenger cars.

Continental AG: Prioritizes ECU advancements, pursuing partnerships for EV-compatible GDI to dominate electronic controls.

Delphi Technologies: Concentrates on aftermarket injectors, leveraging durability designs for commercial vehicles through global supply chains.

Magneti Marelli: Adopts cost-effective strategies, focusing on European exports for multi-cylinder engines.

Hitachi Astemo: Utilizes performance-oriented tech, investing in 350-bar systems for high-efficiency applications.

Stanadyne LLC: Employs durability-focused innovations, launching Goliath injectors for aftermarket growth.

What are the Current Market Trends in the Gasoline Direct Injection (GDI) System Sector?

- Integration of GDI with turbocharging for downsized engines to boost efficiency and power.

- Adoption in hybrids and PHEVs for extended range and emission reduction.

- Advancements in high-pressure injectors (up to 350-bar) for better atomization.

- Focus on dual-injection systems to mitigate carbon buildup.

- Compatibility with alternative fuels like biofuels and hydrogen blends.

- Emphasis on particulate filters (GPF) for regulatory compliance.

What Market Segments are Covered in the Report?

By Component

-

- Fuel Injectors

- Electronic Control Units

- Sensors

- Fuel Pumps

By Vehicle Type

-

- Passenger Cars

- Commercial Vehicles

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Gasoline Direct Injection (GDI) System Market - Industry Analysis

Chapter 4. Global Gasoline Direct Injection (GDI) System Market- Competitive Landscape

Chapter 5. Global Gasoline Direct Injection (GDI) System Market - Component Analysis

Chapter 6. Global Gasoline Direct Injection (GDI) System Market - Vehicle Type Analysis

Chapter 7. Gasoline Direct Injection (GDI) System Market - Regional Analysis

Chapter 8. Company Profiles

Frequently Asked Questions

Gasoline Direct Injection (GDI) systems are fuel delivery technologies that inject gasoline directly into engine combustion chambers for improved efficiency and emissions.

Key factors include emission regulations, engine downsizing, hybrid adoption, and technological advancements in injectors.

The gasoline direct injection (GDI) system market is projected to grow from approximately USD 9.95 billion in 2026 to USD 21.43 billion by 2035.

The CAGR for the gasoline direct injection (GDI) system market during 2026-2035 is expected to be around 8.95%, driven by automotive demands.

Asia-Pacific will contribute notably, accounting for over 37% of the market value, led by production in China.

Major players include Robert Bosch GmbH, Denso Corporation, Continental AG, Delphi Technologies, Magneti Marelli, Hitachi Astemo, and Stanadyne LLC.

The global gasoline direct injection (GDI) system market report provides insights into size, segmentation, dynamics, regional analysis, players, trends, and forecasts.

The value chain includes component sourcing, manufacturing assembly, system integration, distribution to OEMs, and after-sales support.

Market trends are evolving toward hybrid compatibility and high-pressure systems, with preferences shifting to efficient, low-emission engines.

Regulatory factors include emission standards like Euro 7, while environmental factors involve sustainability mandates, driving innovations but increasing costs.