Residential Security Market Size, Share and Forecast 2026 to 2035

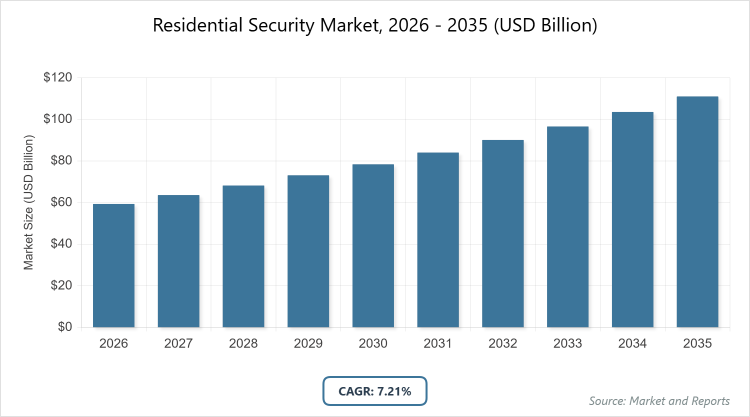

According to our latest research, the global residential security market is projected to grow from approximately USD 59.34 billion in 2026 to USD 116.51 billion by 2035, growing at a CAGR is estimated at 7.21% during 2026-2035. The Residential Security Market is primarily driven by the integration of AI-enabled smart home ecosystems and the rising demand for DIY, mobile-accessible security solutions, which allow homeowners to transition from passive monitoring to proactive, real-time threat detection and home automation.

What are the Key Insights into the Residential Security Market?

- Global market value projected to reach USD 116.51 billion by 2035 from approximately USD 59.34 billion in 2026 (estimated based on 2025 value and CAGR).

- Compound Annual Growth Rate (CAGR) estimated at 7.21% during 2026-2035.

- Infrared cameras dominate the product segment.

- Commercial applications dominate the application segment (though residential-focused, commercial overlaps in trends).

- North America dominates the regional market.

What is the Residential Security Market?

Industry Overview

The residential security market encompasses systems and solutions designed to protect homes and properties from threats such as burglary, fire, and environmental hazards, including smart cameras, alarms, sensors, access controls, and integrated platforms that leverage IoT, AI, and cloud technology for real-time monitoring and response. These products enable homeowners to safeguard their residences through features like remote access via apps, video surveillance, motion detection, and automated alerts, serving urban and suburban households seeking convenience and peace of mind.

The market involves manufacturers, service providers, and integrators focused on user-friendly, scalable solutions that comply with privacy regulations and integrate with smart home ecosystems. It is driven by rising crime rates, technological advancements, and consumer demand for connected living, transforming traditional locks and alarms into intelligent networks that enhance safety while addressing challenges in affordability and interoperability in a growing digital home landscape.

What are the Market Dynamics in the Residential Security Market?

Growth Drivers

The residential security market is propelled by increasing crime rates and home invasions, which heighten consumer demand for advanced surveillance systems like IP cameras and smart alarms equipped with AI for real-time threat detection, alongside the rise of smart homes and IoT integrations that offer seamless remote monitoring via mobile apps. Government initiatives promoting smart city infrastructure and subsidies for home security in urban areas further accelerate adoption, while technological advancements in wireless and cloud-based solutions reduce installation costs and enhance user convenience. The expansion of e-commerce for DIY security kits and partnerships between tech firms and insurers offering discounts for installed systems also drive growth, catering to tech-savvy millennials and aging populations seeking easy-to-use protection.

Restraints

Restraints in the residential security market include high initial costs for premium systems like AI-powered cameras and integrated platforms, which deter budget-conscious consumers in developing regions, compounded by concerns over data privacy and cybersecurity vulnerabilities that erode trust in connected devices. Complex installation requirements for wired systems and interoperability issues with existing home setups add to adoption barriers, while regulatory variations across countries complicate compliance and increase operational expenses for manufacturers. Additionally, market saturation in mature regions and competition from low-cost, unbranded products undermine quality standards and profitability for established players.

Opportunities

Opportunities abound with the integration of AI and machine learning for predictive security features, such as facial recognition and anomaly detection in IP cameras, appealing to premium segments, while emerging markets in Asia offer growth through urbanization and rising disposable incomes for affordable wireless systems. The expansion of 5G networks enables high-definition video streaming and low-latency alerts, opening avenues for smart home ecosystems, and partnerships with insurers for bundled services can incentivize adoption. Sustainable designs using energy-efficient components align with eco-conscious trends, fostering innovation in solar-powered devices for off-grid homes.

Challenges

Challenges include addressing cybersecurity threats to connected devices, which require constant updates and could lead to breaches if not managed, alongside the need for standardized protocols to ensure interoperability among diverse brands. High maintenance costs for advanced systems and a lack of technical knowledge among consumers pose hurdles, while regulatory delays in approving new AI features slow innovation. Economic fluctuations affecting consumer spending and supply chain disruptions for components like sensors add uncertainty, necessitating resilient strategies to maintain market momentum.

Residential Security Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Residential Security Market |

| Market Size 2025 | USD 59.34 Billion |

| Market Forecast 2035 | USD 116.51 Billion |

| Growth Rate | CAGR of 7.21% |

| Report Pages | 220 |

| Key Companies Covered | Honeywell, Bosch, ADT, Hikvision, Dahua, Axis Communications |

| Segments Covered | By Product, By Application, By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation Analysis for the Residential Security Market?

The residential security market is segmented by product, application, and region.

By product segment, infrared cameras emerge as the most dominant subsegment, followed by fixed cameras as the second most dominant. Infrared cameras lead with a 44.21% market share, owing to their superior night vision and discreet monitoring capabilities, essential for residential security in low-light areas like backyards and garages, driven by consumer demand for reliable surveillance; this dominance drives the market by enabling AI integrations for motion detection, attracting investments in durable, weather-resistant designs, and facilitating smart home compatibility that expands adoption, thereby increasing revenue through premium features and service subscriptions.

By application segment, Commercial is the most dominant subsegment in the application segment, followed by residential as the second most dominant. Commercial dominates with 67% market share, due to the need for robust, scalable security in businesses like retail and offices, where features like remote accessibility and AI analytics ensure comprehensive protection; this leadership propels the market by generating high-volume demand for integrated systems, fostering innovations in cloud-based surveillance, and enabling partnerships that spill over to residential use, thus driving overall growth through technology transfer and economies of scale.

What are the Recent Developments in the Residential Security Market?

- In February 2025, Traverse City police launched a private security camera partnership program for homeowners, allowing voluntary registration of cameras to aid investigations and enhance community safety.

- In October 2024, Consistent launched the Night Hawk IP outdoor surveillance camera line, featuring advanced night vision and weather resistance for residential use.

- In December 2024, Vicon partnered with Hailo for an AI-enhanced modular camera system, improving edge processing for home security applications.

What is the Regional Analysis of the Residential Security Market?

- North America to dominate the market

North America dominates the residential security market with a projected higher CAGR, driven by smart security demands, AI-powered surveillance, government investments, and regulations; the United States leads as the dominating country through tech hubs like Silicon Valley, companies such as Honeywell and ADT, and high adoption of IP cameras for home monitoring, supported by insurance discounts for installed systems that address rising burglary rates in urban areas.

Asia Pacific holds the largest share at 50.63%, fueled by urbanization, industrialization, and key players like Sony and Hikvision; China dominates with innovations in AI cameras and rapid smart home growth in cities like Shanghai, while India contributes through affordable wireless systems for middle-class households.

Europe shows steady expansion with a focus on privacy under GDPR, led by Germany through Bosch’s integrated solutions for residential complexes, supported by the UK’s emphasis on CCTV for crime prevention.

Who are the Key Market Players and Their Strategies in the Residential Security Market?

- Honeywell employs strategies focused on smart home integrations and AI enhancements, expanding through acquisitions to capture premium residential segments.

- Bosch leverages its engineering expertise for durable cameras, pursuing partnerships for IoT interoperability in Europe.

- ADT prioritizes subscription-based monitoring services, investing in app-based controls for user convenience.

- Hikvision focuses on cost-effective IP cameras, expanding in Asia through localized manufacturing and night vision innovations.

- Dahua adopts AI-powered analytics, targeting residential markets with weather-resistant designs for global distribution.

- Axis Communications concentrates on high-resolution systems, forming alliances for cybersecurity features.

What are the Market Trends in the Residential Security Market?

- Increasing integration of AI for motion tracking, face recognition, and object detection in cameras.

- Rise of smart home compatibility with voice assistants like Alexa for seamless control.

- Adoption of wireless and battery-powered cameras for easy installation.

- Growth in two-way audio and PTZ technology for interactive monitoring.

- Emphasis on cloud storage and encryption for data privacy.

- Expansion of 5G-enabled cameras for high-speed streaming.

What Market Segments are Covered in the Residential Security Market Report?

By Product

- Fixed Cameras

- Infrared CamerasPan-Tilt-Zoom (PTZ) Cameras

By Application

- Residential

- Commercial

- Government

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Residential Security Market - Industry Analysis

Chapter 4. Global Residential Security Market- Competitive Landscape

Chapter 5. Global Residential Security Market - Product Analysis

Chapter 6. Global Residential Security Market - Application Analysis

Chapter 7. Residential Security Market - Regional Analysis

Chapter 8. Company Profiles

Frequently Asked Questions

Residential security refers to systems like cameras, alarms, and sensors designed to protect homes from threats, often integrated with smart technology for remote monitoring and alerts.

Key factors include rising crime rates, smart home adoption, AI advancements in surveillance, government regulations for safety, and insurance incentives for installed systems.

The market is projected to grow from approximately USD 59.34 billion in 2026 to USD 116.51 billion by 2035.

The CAGR is estimated at 7.21% during 2026-2035.

North America will contribute notably, with high adoption of AI-powered systems.

Major players include Honeywell, Bosch, ADT, Hikvision, Dahua, Axis Communications.

The report provides insights into market size, forecasts, segmentation, regional analysis, key players, trends, dynamics, and developments.

The value chain includes component manufacturing (cameras, sensors), system integration, distribution through retail/e-commerce, installation services, and after-sales maintenance.

Trends are evolving toward AI and IoT integrations, with consumers preferring wireless, app-controlled systems for convenience and privacy.

Regulatory factors include data privacy laws like GDPR, while environmental factors involve energy-efficient designs to reduce carbon footprints in smart devices.