Defoamers Market Size and Forecast 2026 to 2035

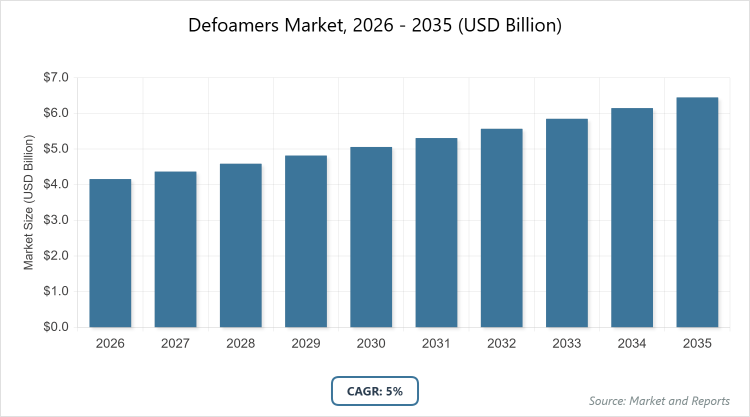

According to MarketnReports, the global Defoamers market size was estimated at USD 4.16 billion in 2025 and is expected to reach USD 6.45 billion by 2035, growing at a CAGR of 5.0% from 2026 to 2035. Defoamers Market is driven by the increasing demand from industries such as food & beverages, pharmaceuticals, wastewater treatment, and chemicals to improve process efficiency and product quality.

What are the Key Insights into the Defoamers Market?

- Market Value and CAGR: The defoamers market is projected to grow from approximately USD 4.16 billion in 2025 to USD 6.45 billion by 2035, at a CAGR of 5.0%.

- Dominated Product Subsegment: Silicone-based defoamers dominate with the largest revenue share.

- Dominated End-Use Subsegment: Paints, coatings, and inks hold the largest share, while water treatment is the fastest-growing.

- Dominated Region: Asia Pacific leads with the highest revenue share.

What is the Overview of the Defoamers Industry?

The defoamers industry encompasses the production and application of chemical agents designed to control or eliminate foam formation in various industrial processes. Defoamers are essential additives that disrupt foam stability by reducing surface tension or breaking down foam structures, thereby enhancing operational efficiency, product quality, and safety across sectors. This market serves diverse applications where foam can hinder processes, such as in manufacturing liquids, treating wastewater, or formulating agrochemicals, by providing solutions that ensure smooth operations and compliance with environmental standards. The industry is characterized by ongoing innovations to meet evolving demands for sustainability and performance, driven by the need to address foam-related challenges in industrialization and urbanization contexts.

What are the Dynamics Shaping the Defoamers Market?

Growth Drivers

The defoamers market is propelled by the escalating demand for agrochemicals such as pesticides, fertilizers, and herbicides to support global food production amid a growing population, alongside the rising necessity for advanced wastewater treatment and water purification systems due to rapid industrialization and urbanization, which heighten concerns over water quality and environmental sustainability; furthermore, the burgeoning need for high-performance coatings, inks, adhesives, and sealants in construction and manufacturing sectors requires effective foam control to ensure product consistency and application efficiency, while stricter global regulations on emissions and waste management encourage the adoption of eco-friendly defoamers, and technological advancements in defoaming formulations enhance their effectiveness across diverse pH levels and temperatures, collectively driving market expansion.

Restraints

The defoamers market faces restraints primarily from stringent regulatory frameworks that impose rigorous environmental and safety standards, compelling manufacturers to reformulate products away from traditional, potentially harmful chemicals toward more sustainable options, which can increase production costs and complicate compliance; additionally, volatility in raw material prices, particularly for silicone and oil-based components, poses challenges to profitability and supply chain stability, while the shift toward bio-based alternatives, though beneficial long-term, requires significant investment in research and development, potentially slowing adoption in cost-sensitive regions and limiting market growth in the short term.

Opportunities

The defoamers market presents opportunities through the increasing shift toward green technologies and bio-based formulations that offer environmentally safer alternatives to conventional products, aligning with global sustainability goals and opening new avenues in sectors like food and beverages, where foam control is critical in processes such as brewing and dairy production; moreover, expansion in the oil and gas industry provides prospects for specialized defoamers in drilling, production, and wastewater management, while innovations in efficient, cost-effective, and sustainable defoaming solutions can capture emerging demands in pharmaceuticals and personal care, fostering market penetration in developing economies with rising industrial activities.

Challenges

The defoamers market encounters challenges from the mounting pressure to develop and adopt greener, biodegradable solutions amid heightened environmental awareness and consumer preferences for sustainable products, necessitating continuous innovation to balance performance with eco-compliance; additionally, aligning with evolving regulatory requirements across regions demands substantial resources for testing and certification, while competition from alternative foam control methods and the need to maintain efficacy in extreme industrial conditions like high temperatures or varying pH levels further complicate product development and market positioning.

Defoamers Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Defoamers Market |

| Market Size 2025 | USD 4.16 Billion |

| Market Forecast 2035 | USD 6.45 Billion |

| Growth Rate | CAGR of 5.0% |

| Report Pages | 220 |

| Key Companies Covered |

Kemira Oyj, Air Products and Chemicals, Inc., Ashland Inc., Bluestar Silicones International, Dow Inc., Evonik Industries AG, Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., BASF SE, Elementis PLC, Clariant AG, KCC Basildon, Eastman Chemical Company, Synalloy Chemicals, Tiny Chempro, Trans-Chemco Inc. |

| Segments Covered | By Product, By End Use, and By Region. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Defoamers Market Segmented?

The Defoamers market is segmented by product, end use, and region.

In the product segmentation of the defoamers market, silicone-based defoamers emerge as the most dominant subsegment due to their exceptional performance, versatility, and superior stability, which enable effective foam control in a wide array of industrial applications including paints, coatings, textiles, and wastewater treatment, driving the market by offering long-lasting results at low usage rates and excelling in challenging conditions such as high temperatures and diverse pH environments, thereby enhancing process efficiency and product quality; the second most dominant subsegment is water-based defoamers, which gain prominence for their eco-friendly and non-toxic properties, making them ideal for sensitive applications in food processing, pharmaceuticals, and water treatment, contributing to market growth by providing sustainable alternatives that reduce environmental impact, comply with stringent regulations, and appeal to industries prioritizing green chemistry without compromising on defoaming efficacy.

Within the end-use segmentation of the defoamers market, paints, coatings, and inks represent the most dominant subsegment owing to their critical role in controlling foam during manufacturing and application processes to ensure smooth finishes, consistency, and high-quality outputs, propelling market growth through the rising demand for high-performance and eco-friendly formulations in construction, automotive, and printing industries that adhere to regulatory standards and enhance operational efficiency; the second most dominant subsegment is water treatment, which drives the market by addressing foam-related issues in purification and wastewater management amid growing global concerns over water quality, stricter environmental regulations, and technological advancements that improve treatment processes, enabling better compliance, reduced operational disruptions, and support for sustainable water resource management in urbanizing regions.

What are the Recent Developments in the Defoamers Market?

- In November 2024, Evonik Coating Additives introduced two innovative defoamers, TEGO Foamex 16 for low to medium PVC coatings and TEGO Foamex 11 for high PVC coatings, aimed at boosting sustainability and performance in waterborne architectural coatings by providing efficient foam control with reduced environmental impact.

- In November 2023, BASF enhanced its defoamer production capabilities at the Dilovasi facility in Türkiye by adding a new production line, targeting increased supply of Foamaster and Foamstar products to meet escalating demand in South-East Europe, the Middle East, and Africa regions.

- In October 2023, Evonik unveiled TEGO Foamex 8880, a bio-based defoamer tailored for waterborne inks, leveraging hybrid technology combining bio-based polymers and polyether siloxanes to deliver superior foam prevention, seamless integration, and alignment with sustainability objectives.

How Does Regional Analysis Impact the Defoamers Market?

Asia Pacific to dominate the market

The Asia Pacific region dominates the defoamers market with a substantial revenue share, fueled by robust agricultural activities requiring agrochemicals like pesticides and fertilizers where defoamers ensure efficient production, alongside rapid industrialization and urbanization that amplify the need for wastewater treatment and sustainable practices; China stands as the dominating country, driven by stringent environmental policies on waste management and industrial emissions, coupled with expansion in the food and beverage sector including dairy, brewing, and soft drinks, which heighten demand for eco-friendly defoamers, while India’s growth is supported by a shift toward non-silicone options and applications in oil and gas for drilling and production, collectively positioning the region as a key growth hub through innovation and regulatory compliance.

Europe exhibits strong growth potential in the defoamers market, characterized by an established industrial base and rigorous environmental regulations that promote advanced wastewater treatment and waste management, emphasizing sustainability through the adoption of water-based and biodegradable defoamers in chemicals, food processing, and pharmaceuticals; Germany emerges as the dominating country, with its preference for eco-friendly solutions and innovations in specialty chemicals, bolstered by a robust industrial sector in pharmaceuticals and wastewater management, while the UK’s demand stems from end-use industries like food processing and chemicals, where defoamers aid in drug manufacturing and fermentation, driving regional expansion via technological advancements and compliance with green standards.

North America contributes significantly to the defoamers market through technological advancements and strict environmental regulations that spur demand in paints, coatings, water treatment, and food processing for efficient and sustainable foam control solutions; the United States is the dominating country, with trends toward renewable resources and green chemistry fostering bio-based defoamers in food and beverages, pharmaceuticals, and agriculture to meet high-performance needs, while Canada’s growth is propelled by expansions in the food and beverage sector for maintaining product quality and addressing pollution concerns in wastewater management, overall enhancing the region’s market position with a focus on innovation and regulatory alignment.

Latin America shows emerging potential in the defoamers market, supported by growing industrial activities in agriculture and water treatment, where defoamers aid in agrochemical formulations and wastewater processes amid increasing urbanization and environmental awareness; Brazil dominates the region, driven by its expansive agricultural sector requiring foam control in pesticides and fertilizers, alongside developments in food processing and oil extraction that necessitate sustainable defoaming solutions to comply with regional regulations and improve operational efficiency.

The Middle East & Africa region experiences steady growth in the defoamers market, primarily through oil and gas applications for drilling and wastewater treatment, combined with rising demands in food and beverage processing driven by population growth and industrialization; no single country overwhelmingly dominates, but key contributors include those with strong oil sectors like Saudi Arabia, where defoamers optimize production processes, and South Africa, which benefits from advancements in water purification and agrochemicals to address environmental challenges and support sustainable industrial practices.

Who are the Key Market Players in the Defoamers Industry and Their Strategies?

- Kemira Oyj focuses on developing sustainable chemical solutions for water-intensive industries, emphasizing innovation in eco-friendly defoamers to enhance water treatment and agrochemical applications while expanding global production capacities to meet regulatory demands.

- Air Products and Chemicals, Inc. employs strategies centered on advanced material technologies, investing in R&D for high-performance defoamers that cater to paints, coatings, and industrial cleaning, with a strong emphasis on sustainability and customer-specific formulations to drive market penetration.

- Ashland Inc. prioritizes specialty additives, leveraging acquisitions and product innovations to offer versatile defoamers for personal care, pharmaceuticals, and adhesives, aiming to align with green chemistry trends and expand in emerging markets through strategic partnerships.

- Bluestar Silicones International specializes in silicone-based technologies, focusing on R&D for efficient, long-lasting defoamers in textiles and coatings, with strategies including capacity expansions and sustainability initiatives to comply with environmental standards and capture high-growth sectors.

- Dow Inc. pursues innovation in material science, developing bio-based and water-based defoamers for diverse applications like food processing and water treatment, while employing mergers and global supply chain optimizations to strengthen market leadership and address sustainability goals.

- Evonik Industries AG drives growth through product launches like bio-based defoamers for inks and coatings, investing in hybrid technologies and sustainability to meet consumer preferences, with strategies including targeted expansions in architectural and industrial applications.

- Wacker Chemie AG emphasizes silicone expertise, focusing on eco-friendly formulations for agriculture and personal care, with strategies involving R&D investments and regional production enhancements to ensure compliance and efficiency in foam control solutions.

- Shin-Etsu Chemical Co., Ltd. leverages advanced polymer technologies, developing high-stability defoamers for extreme conditions in oil and gas, with strategies centered on innovation, quality assurance, and global market expansions to support industrial efficiency.

- BASF SE adopts capacity expansions, such as new production lines for defoamers, to meet regional demands in Europe and Africa, while innovating sustainable products for agriculture and construction to improve everyday applications and align with environmental regulations.

- Elementis PLC focuses on specialty chemicals, offering rheology and defoaming solutions for paints and personal care, with strategies including product diversification and sustainability commitments to enhance performance and reduce environmental impact.

- Clariant AG prioritizes sustainable innovations, developing biodegradable defoamers for household cleaning and water treatment, employing global collaborations and R&D to address regulatory challenges and expand in high-growth end-use sectors.

- KCC Basildon specializes in silicone defoamers, focusing on custom solutions for cosmetics and food industries, with strategies involving quality enhancements and market expansions to cater to eco-conscious consumers.

- Eastman Chemical Company invests in bio-based technologies, creating defoamers for adhesives and coatings, with strategies emphasizing sustainability and supply chain resilience to drive growth in industrial applications.

- Synalloy Chemicals targets niche markets with specialized defoamers for institutional cleaning, employing cost-effective production and innovation to meet specific industry needs and regulatory standards.

- Tiny Chempro focuses on affordable, effective defoamers for agriculture and water treatment, with strategies including local manufacturing expansions and eco-friendly product developments to penetrate developing markets.

- Trans-Chemco, Inc. emphasizes custom formulations for industrial processes, investing in R&D for versatile defoamers in paints and pharmaceuticals, with strategies aimed at sustainability and customer partnerships for market growth.

What are the Current Trends in the Defoamers Market?

- Increasing preference for eco-friendly, biodegradable, and bio-based defoamers driven by global environmental awareness and sustainability objectives.

- Shift toward water-based and non-silicone defoamers as greener alternatives to traditional oil-based products, reducing environmental impact.

- Innovations in defoaming technologies to improve efficiency, performance under extreme conditions, and compliance with stringent regulations.

- Rising adoption in waterborne coatings, inks, and architectural applications to enhance product quality and process smoothness.

- Growing demand from expanding sectors such as food and beverages, oil and gas, and agriculture for specialized foam control solutions.

What Market Segments are Covered in the Defoamers Report?

By Product

-

- Water-Based

-

- Oil-Based

-

- Silicone-Based

-

- Others

By End Use

-

- Paints, Coatings, & Inks

-

- Adhesives & Sealants

-

- Personal Care & Cosmetics

-

- Agriculture

-

- Food & Beverages

-

- Household & Industrial/Institutional Cleaning

-

- Water Treatment

-

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

1.1 Report Description and Scope1.2 Research Scope1.3 Research Methodology1.3.1 Market Research Type1.3.2 Market Research MethodologyChapter 2. Executive Summary

2.1 Global Defoamers Market, (2026 - 2035) (USD Billion)2.2 Global Defoamers Market: SnapshotChapter 3. Global Defoamers Market - Industry Analysis

3.1 Defoamers Market: Market Dynamics3.2 Market Drivers3.2.1 The global defoamers market is expanding rapidly due to rising demand for agrochemicals, wastewater treatment, and high-performance industrial coatings, supported by stricter environmental regulations and advancements in eco-friendly formulations.3.3 Market Restraints3.3.1 Market growth is hindered by strict environmental regulations, volatile raw material prices for silicone and oils, and the high R&D costs associated with transitioning to bio-based alternatives.3.4 Market Opportunities3.4.1 The defoamers market is seeing growth through the rise of bio-based formulations for the food and beverage sectors, expanding oil and gas infrastructure, and the adoption of "smart" dosing systems in emerging economies.3.5 Market Challenges3.5.1 The defoamers market is challenged by the need to balance eco-compliance with performance in extreme industrial conditions, while navigating high R&D costs and complex regional regulations.3.6 Porter’s Five Forces Analysis3.7 Market Attractiveness Analysis3.7.1 Market Attractiveness Analysis By Product3.7.2 Market Attractiveness Analysis By End UseChapter 4. Global Defoamers Market- Competitive Landscape

4.1 Company Market Share Analysis4.1.1 Global Defoamers Market: Company Market Share, 20254.2 Strategic Development4.2.1 Acquisitions & mergers4.2.2 New Product launches4.2.3 Agreements, partnerships, collaborations, and joint ventures4.2.4 Research and development and regional expansion4.3 Price Trend AnalysisChapter 5. Global Defoamers Market - Product Analysis

5.1 Global Defoamers Market Overview: Product5.1.1 Global Defoamers Market share, By Product, 2025 and 20355.2 Water-Based5.2.1 Global Defoamers Market by Water-Based, 2026 - 2035 (USD Billion)5.3 Oil-Based5.3.1 Global Defoamers Market by Oil-Based, 2026 - 2035 (USD Billion)5.4 Silicone-Based5.4.1 Global Defoamers Market by Silicone-Based, 2026 - 2035 (USD Billion)5.5 Others5.5.1 Global Defoamers Market by Others, 2026 - 2035 (USD Billion)Chapter 6. Global Defoamers Market - End Use Analysis

6.1 Global Defoamers Market Overview: End Use6.1.1 Global Defoamers Market Share, By End Use, 2025 and 20356.2 Paints6.2.1 Global Defoamers Market by Paints, 2026 - 2035 (USD Billion)6.3 Coatings6.3.1 Global Defoamers Market by Coatings, 2026 - 2035 (USD Billion)6.4 & Inks6.4.1 Global Defoamers Market by & Inks, 2026 - 2035 (USD Billion)6.5 Adhesives & Sealants6.5.1 Global Defoamers Market by Adhesives & Sealants, 2026 - 2035 (USD Billion)6.6 Personal Care & Cosmetics6.6.1 Global Defoamers Market by Personal Care & Cosmetics, 2026 - 2035 (USD Billion)6.7 Agriculture6.7.1 Global Defoamers Market by Agriculture, 2026 - 2035 (USD Billion)6.8 Food & Beverages6.8.1 Global Defoamers Market by Food & Beverages, 2026 - 2035 (USD Billion)6.9 Household & Industrial/Institutional Cleaning6.9.1 Global Defoamers Market by Household & Industrial/Institutional Cleaning, 2026 - 2035 (USD Billion)6.10 Water Treatment6.10.1 Global Defoamers Market by Water Treatment, 2026 - 2035 (USD Billion)6.11 Others6.11.1 Global Defoamers Market by Others, 2026 - 2035 (USD Billion)Chapter 7. Defoamers Market - Regional Analysis

7.1 Global Defoamers Market Regional Overview7.2 Global Defoamers Market Share, by Region, 2025 & 2035 (USD Billion)7.3 North America7.3.1 North America Defoamers Market, 2026 - 2035 (USD Billion)7.3.1.1 North America Defoamers Market, by Country, 2026 - 2035 (USD Billion)7.3.2 North America Defoamers Market, by Product, 2026 - 20357.3.2.1 North America Defoamers Market, by Product, 2026 - 2035 (USD Billion)7.3.3 North America Defoamers Market, by End Use, 2026 - 20357.3.3.1 North America Defoamers Market, by End Use, 2026 - 2035 (USD Billion)7.4 Europe7.4.1 Europe Defoamers Market, 2026 - 2035 (USD Billion)7.4.1.1 Europe Defoamers Market, by Country, 2026 - 2035 (USD Billion)7.4.2 Europe Defoamers Market, by Product, 2026 - 20357.4.2.1 Europe Defoamers Market, by Product, 2026 - 2035 (USD Billion)7.4.3 Europe Defoamers Market, by End Use, 2026 - 20357.4.3.1 Europe Defoamers Market, by End Use, 2026 - 2035 (USD Billion)7.5 Asia Pacific7.5.1 Asia Pacific Defoamers Market, 2026 - 2035 (USD Billion)7.5.1.1 Asia Pacific Defoamers Market, by Country, 2026 - 2035 (USD Billion)7.5.2 Asia Pacific Defoamers Market, by Product, 2026 - 20357.5.2.1 Asia Pacific Defoamers Market, by Product, 2026 - 2035 (USD Billion)7.5.3 Asia Pacific Defoamers Market, by End Use, 2026 - 20357.5.3.1 Asia Pacific Defoamers Market, by End Use, 2026 - 2035 (USD Billion)7.6 Latin America7.6.1 Latin America Defoamers Market, 2026 - 2035 (USD Billion)7.6.1.1 Latin America Defoamers Market, by Country, 2026 - 2035 (USD Billion)7.6.2 Latin America Defoamers Market, by Product, 2026 - 20357.6.2.1 Latin America Defoamers Market, by Product, 2026 - 2035 (USD Billion)7.6.3 Latin America Defoamers Market, by End Use, 2026 - 20357.6.3.1 Latin America Defoamers Market, by End Use, 2026 - 2035 (USD Billion)7.7 The Middle-East and Africa7.7.1 The Middle-East and Africa Defoamers Market, 2026 - 2035 (USD Billion)7.7.1.1 The Middle-East and Africa Defoamers Market, by Country, 2026 - 2035 (USD Billion)7.7.2 The Middle-East and Africa Defoamers Market, by Product, 2026 - 20357.7.2.1 The Middle-East and Africa Defoamers Market, by Product, 2026 - 2035 (USD Billion)7.7.3 The Middle-East and Africa Defoamers Market, by End Use, 2026 - 20357.7.3.1 The Middle-East and Africa Defoamers Market, by End Use, 2026 - 2035 (USD Billion)Chapter 8. Company Profiles

8.1 Kemira Oyj8.1.1 Overview8.1.2 Financials8.1.3 Product Portfolio8.1.4 Business Strategy8.1.5 Recent Developments8.2 Air Products and Chemicals Inc.8.2.1 Overview8.2.2 Financials8.2.3 Product Portfolio8.2.4 Business Strategy8.2.5 Recent Developments8.3 Ashland Inc.8.3.1 Overview8.3.2 Financials8.3.3 Product Portfolio8.3.4 Business Strategy8.3.5 Recent Developments8.4 Bluestar Silicones International8.4.1 Overview8.4.2 Financials8.4.3 Product Portfolio8.4.4 Business Strategy8.4.5 Recent Developments8.5 Dow Inc.8.5.1 Overview8.5.2 Financials8.5.3 Product Portfolio8.5.4 Business Strategy8.5.5 Recent Developments8.6 Evonik Industries AG8.6.1 Overview8.6.2 Financials8.6.3 Product Portfolio8.6.4 Business Strategy8.6.5 Recent Developments8.7 Wacker Chemie AG8.7.1 Overview8.7.2 Financials8.7.3 Product Portfolio8.7.4 Business Strategy8.7.5 Recent Developments8.8 Shin-Etsu Chemical Co.Ltd.8.8.1 Overview8.8.2 Financials8.8.3 Product Portfolio8.8.4 Business Strategy8.8.5 Recent Developments8.9 BASF SE8.9.1 Overview8.9.2 Financials8.9.3 Product Portfolio8.9.4 Business Strategy8.9.5 Recent Developments8.10 Elementis PLC8.10.1 Overview8.10.2 Financials8.10.3 Product Portfolio8.10.4 Business Strategy8.10.5 Recent Developments8.11 Clariant AG8.11.1 Overview8.11.2 Financials8.11.3 Product Portfolio8.11.4 Business Strategy8.11.5 Recent Developments8.12 KCC Basildon8.12.1 Overview8.12.2 Financials8.12.3 Product Portfolio8.12.4 Business Strategy8.12.5 Recent Developments8.13 Eastman Chemical Company8.13.1 Overview8.13.2 Financials8.13.3 Product Portfolio8.13.4 Business Strategy8.13.5 Recent Developments8.14 Synalloy Chemicals8.14.1 Overview8.14.2 Financials8.14.3 Product Portfolio8.14.4 Business Strategy8.14.5 Recent Developments8.15 Tiny Chempro8.15.1 Overview8.15.2 Financials8.15.3 Product Portfolio8.15.4 Business Strategy8.15.5 Recent Developments8.16 Trans-Chemco Inc.8.16.1 Overview8.16.2 Financials8.16.3 Product Portfolio8.16.4 Business Strategy8.16.5 Recent Developments

- North America

Frequently Asked Questions

Defoamers are chemical additives designed to reduce or eliminate foam formation in industrial processes by destabilizing foam bubbles, improving efficiency in applications such as manufacturing, wastewater treatment, and agrochemical production.

Key factors influencing growth include rising demand for agrochemicals and wastewater treatment due to population growth and urbanization, advancements in sustainable defoaming technologies, stricter environmental regulations, and expansion in end-use sectors like paints, coatings, food processing, and oil and gas.

The defoamers market is projected to grow from approximately USD 4.16 billion in 2025 to USD 6.45 billion by 2035, reflecting steady expansion driven by industrial demands and sustainability trends.

The CAGR for the defoamers market from 2026 to 2035 is expected to be 5.0%, continuing the established growth trajectory based on current market dynamics and projections.

Asia Pacific will contribute notably to the defoamers market value, holding the largest revenue share due to robust agricultural and industrial activities in countries like China and India.

Major players include Kemira Oyj, Air Products and Chemicals, Inc., Ashland Inc., Bluestar Silicones International, Dow Inc., Evonik Industries AG, Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., BASF SE, Elementis PLC, Clariant AG, KCC Basildon, Eastman Chemical Company, Synalloy Chemicals, Tiny Chempro, Trans-Chemco Inc., which drive growth through innovations in sustainable products, capacity expansions, and strategic focus on eco-friendly solutions.

The global defoamers market report provides comprehensive insights including market size forecasts, segmentation analysis, regional overviews, key player strategies, trends, dynamics, and recent developments to guide stakeholders in decision-making.

The value chain includes raw material sourcing (such as silicones and oils), manufacturing and formulation of defoamers, distribution through suppliers, integration into end-use applications like coatings and water treatment, and end-user consumption with recycling or disposal considerations.

Market trends are evolving toward eco-friendly and bio-based defoamers, with consumer preferences shifting to sustainable, non-toxic options that align with environmental regulations and green chemistry principles in industrial applications.

Regulatory factors include stringent environmental standards on emissions and waste, promoting biodegradable defoamers, while environmental concerns over water quality and sustainability drive demand for green alternatives, influencing innovation and market expansion.