Renewable Energy Certificate Market Size, Share and Trends 2026 to 2035

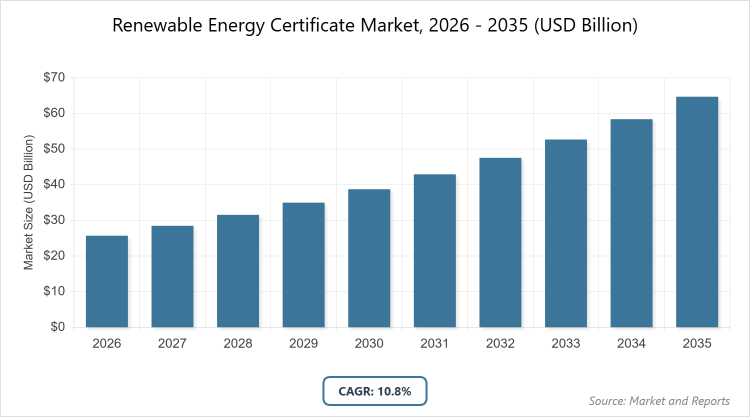

The global Renewable Energy Certificate Market size was estimated at USD 25.7 Billion in 2025 and is expected to reach USD 64.6 Billion by 2035, growing at a CAGR of 10.8% from 2026 to 2035. The Renewable Energy Certificate (REC) market is primarily driven by stringent government regulatory mandates (such as Renewable Portfolio Standards) and the escalating voluntary demand from corporations striving to fulfill net-zero and ESG sustainability commitments.

What are the Key Insights?

- The global Renewable Energy Certificate market is projected to grow from approximately USD 25.7 billion in 2026 to USD 64.6 billion by 2035.

- The market is anticipated to register a CAGR of 10.8% during the forecast period from 2026 to 2035.

- Within the energy type segment, the solar power subsegment dominates due to its widespread adoption and cost reductions.

- In the end-use segment, the compliance subsegment holds the largest share, driven by regulatory mandates.

- North America remains the dominated region, contributing significantly to the overall market value.

What is the Industry Overview?

The Renewable Energy Certificate (REC) market is a specialized segment within the broader renewable energy ecosystem that facilitates the trading of certificates representing the environmental and sustainability attributes of electricity generated from renewable sources, separate from the physical power itself. These certificates, typically issued for each megawatt-hour (MWh) of renewable electricity produced, allow organizations, utilities, and individuals to claim the benefits of green energy without directly consuming it, supporting compliance with regulatory mandates or voluntary sustainability goals. This market enables the monetization of renewable attributes, incentivizing investments in clean energy projects like solar, wind, and hydro installations, while promoting transparency through tracking systems that prevent double-counting and ensure credibility. It plays a crucial role in the global transition to low-carbon economies by bridging the gap between renewable generation and end-user demands for verifiable green credentials, fostering a dynamic trading environment influenced by policy frameworks, corporate commitments, and technological advancements in verification.

What are the Market Dynamics?

Growth Drivers

The growth of the Renewable Energy Certificate market is propelled by escalating corporate and governmental commitments to reduce carbon emissions and achieve net-zero targets, with initiatives like RE100 encouraging businesses to procure renewable attributes to offset their energy usage. Favorable regulatory frameworks, such as Renewable Portfolio Standards (RPS) in various countries, mandate utilities to source a portion of their energy from renewables, thereby increasing demand for RECs as a cost-effective compliance tool. Additionally, rising awareness of climate change, coupled with consumer and investor pressure for sustainable practices, has led to expanded voluntary participation, while advancements in digital platforms and blockchain enhance market efficiency and accessibility, further stimulating investments in renewable infrastructure across solar, wind, and other sources.

Restraints

The Renewable Energy Certificate market faces restraints primarily from price volatility, which arises from fluctuations in supply and demand influenced by inconsistent renewable energy generation, regulatory changes, and regional policy differences, making it challenging for buyers to forecast costs and plan long-term procurement strategies. High transaction costs, including administrative fees and verification expenses, also hinder smaller organizations and emerging markets from participating, while concerns over market transparency, such as risks of fraud or duplicate claims, erode trust and slow adoption in less mature regions.

Opportunities

Opportunities in the Renewable Energy Certificate market are abundant with the expansion of emerging markets in Asia-Pacific and Latin America, where new trading platforms and international standards like I-RECs are enabling cross-border transactions and attracting investments in underserved areas. The integration of advanced technologies, such as AI for demand forecasting and blockchain for enhanced traceability, presents avenues to reduce costs and improve credibility, while growing voluntary sectors among corporates and municipalities offer potential for innovative bundling with green tariffs and ESG reporting, driving broader participation and market diversification.

Challenges

The Renewable Energy Certificate market encounters challenges related to standardization gaps across regions, leading to inefficiencies in cross-border trading and complications in verifying certificate authenticity without unified global frameworks. Regional disparities in policy enforcement and market maturity exacerbate access issues for smaller players, while the risk of oversupply in mature markets or undersupply in developing ones creates imbalances that could undermine investor confidence and slow the pace of renewable energy adoption.

Renewable Energy Certificate Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Renewable Energy Certificate Market |

| Market Size 2025 | USD 25.7 Billion |

| Market Forecast 2035 | USD 64.6 Billion |

| Growth Rate | CAGR of 10.8% |

| Report Pages | 215 |

| Key Companies Covered |

3Degrees, Inc., Statkraft, ENGIE, Shell Energy, Ørsted, South Pole, and Tata Power |

| Segments Covered | By Energy Type, By End-Use, By Capacity, By Region |

| Regions Covered | Asia Pacific, North America, Europe, Latin America, The Middle East and Africa |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation?

The Renewable Energy Certificate market encounters challenges related to standardization gaps across regions, leading to inefficiencies in cross-border trading and complications in verifying certificate authenticity without unified global frameworks. Regional disparities in policy enforcement and market maturity exacerbate access issues for smaller players, while the risk of oversupply in mature markets or undersupply in developing ones creates imbalances that could undermine investor confidence and slow the pace of renewable energy adoption.

By energy type, includes solar power, wind power, hydropower, biomass, and others. The most dominant segment is solar power, which commands the largest market share owing to rapid technological advancements, declining installation costs, and supportive government incentives that have led to a surge in solar photovoltaic projects worldwide, enabling higher REC issuance volumes and appealing to both compliance and voluntary buyers seeking scalable green attributes; this dominance drives the market by accelerating investments in solar infrastructure, enhancing supply chain efficiencies, and aligning with global decarbonization goals to boost overall renewable penetration. The second most dominant segment is wind power, which benefits from established onshore and offshore developments in regions with favorable wind resources, offering reliable generation and long-term contracts that stabilize REC supply; it contributes to market growth by diversifying renewable sources, reducing dependency on variable solar output, and supporting energy security through large-scale projects that attract corporate purchasers committed to sustainability.

By end-use, encompasses compliance and voluntary categories. The compliance segment is the most dominant, holding a substantial market share because of stringent government regulations like Renewable Portfolio Standards that require utilities and energy providers to meet renewable quotas, making RECs an essential tool for fulfilling obligations without direct infrastructure ownership; this drives the market by enforcing widespread adoption, stimulating renewable project funding, and ensuring steady demand that underpins market stability and growth. The voluntary segment is the second most dominant, fueled by corporate sustainability initiatives and consumer-driven green branding, allowing businesses and individuals to offset emissions beyond mandates; it propels market expansion by attracting innovative financing, enhancing corporate reputations, and fostering voluntary platforms that complement compliance mechanisms to broaden overall participation.

By capacity, covers up to 1000 KWH, 1001-5000 KWH, and above 5000 KWH. The above 5000 KWH segment dominates, as it encompasses large-scale renewable projects that benefit from economies of scale, lower per-unit costs, and higher efficiency in REC generation, particularly in utility-owned solar and wind farms; this leadership drives the market by enabling bulk trading, attracting institutional investors, and supporting grid integration efforts that accelerate the transition to renewables on a massive scale. The 1001-5000 KWH segment is the second most dominant, catering to mid-sized installations like community solar or commercial wind setups that offer flexibility for regional needs and distributed energy solutions; it aids market growth by bridging small and large projects, promoting local energy independence, and expanding access for diverse buyers through adaptable REC volumes.

What are the Recent Developments?

- In February 2024, Statkraft signed a Virtual Power Purchase Agreement (VPPA) with Air Liquide to supply RECs from wind farms in Poland, aiming to reduce CO2 emissions by 38,000 tonnes annually and supporting corporate sustainability goals through long-term renewable attribute procurement.

- In December 2024, NSCH entered a two-year agreement with ENGIE Resources to match 100% of its energy consumption with RECs, highlighting the growing trend of institutional commitments to green energy verification and carbon neutrality.

- In May 2024, Shell Energy Europe and 3Degrees Group Inc. registered an agreement for the auction of guarantees of origin in Croatia, facilitating market liquidity and enabling broader access to European renewable attributes.

- In September 2025, Indonesia’s PT Mitra Stania Prima purchased RECs from PLN to enhance its sustainability profile, demonstrating the expansion of REC adoption in emerging Asian markets for industrial applications.

- In March 2025, Astana International Exchange (AIX) began trading I-RECs in Kazakhstan, marking a key development in Central Asia’s renewable certification landscape and promoting cross-border green energy claims.

What is the Regional Analysis?

North America holds a prominent position in the Renewable Energy Certificate market, driven by robust regulatory frameworks such as Renewable Portfolio Standards in the United States and voluntary corporate initiatives in Canada, with the region benefiting from well-established trading platforms and high corporate demand for sustainability reporting; the dominating country is the United States, where state-level mandates and federal incentives have led to significant REC issuance from solar and wind projects, fostering market maturity, attracting investments, and enabling utilities to meet compliance targets efficiently while supporting net-zero ambitions across industries like technology and manufacturing.

Europe leads in market share within the Renewable Energy Certificate sector, propelled by the EU Renewable Energy Directive and Guarantees of Origin systems that enforce stringent emission reductions and promote cross-border trading, with corporate sustainability pledges further amplifying demand; Germany emerges as the dominating country, renowned for its Energiewende policy that has spurred massive investments in wind and solar, resulting in high REC volumes, enhanced grid stability, and leadership in voluntary markets that influence global standards and drive innovation in green energy procurement.

Asia-Pacific is the fastest-growing region in the Renewable Energy Certificate market, fueled by rapid renewable infrastructure expansion and policies like feed-in tariffs in countries pursuing aggressive clean energy targets, alongside increasing corporate participation in voluntary schemes; China stands out as the dominating country, with its mandates on green electricity certificates and vast solar and wind deployments generating substantial REC supply, which supports domestic compliance, exports green attributes internationally, and accelerates the region’s shift toward sustainable development amid rising urbanization and industrial demands.

Latin America is emerging as a key player in the Renewable Energy Certificate market, supported by frameworks like I-RECs and national renewable goals that encourage hydro and solar projects, with growing voluntary adoption among multinationals operating in the region; Brazil is the dominating country, leading in I-REC issuance through its abundant hydropower resources and policy incentives that facilitate large-scale REC trading, enhancing energy diversification, attracting foreign investments, and aiding corporate efforts to achieve sustainability in agriculture and mining sectors.

The Middle East & Africa region is witnessing gradual growth in the Renewable Energy Certificate market, driven by renewable initiatives in oil-dependent economies transitioning to green energy and international standards enabling certificate trading; Saudi Arabia dominates, with its Vision 2030 program promoting solar projects and I-REC issuance to diversify energy sources, reduce reliance on fossils, and position the country as a regional hub for sustainable investments while meeting global climate commitments.

Who are the Key Market Players and Their Strategies?

3Degrees, Inc.: This player focuses on comprehensive REC portfolios and digital solutions, employing strategies like collaborations with organizations for P-REC transactions and auctions to enhance market accessibility and support humanitarian solar projects in emerging regions.

Statkraft: As a leading European entity, Statkraft emphasizes Virtual Power Purchase Agreements (VPPAs) for REC supply from wind and hydro assets, with strategies centered on long-term contracts to reduce emissions and expand into new markets like Poland.

ENGIE: ENGIE adopts multi-year agreements for REC matching with corporate energy consumption, leveraging strategies that include partnerships for compliance and voluntary markets to promote transparency and sustainability across utilities and industries.

Shell Energy: Shell Energy pursues agreements for origin guarantees and auctions, with strategies involving diversification into European and global trading to manage volatility and support corporate transitions to renewable attributes.

Ørsted: Ørsted concentrates on wind-based RECs through Power Purchase Agreements (PPAs), implementing strategies like bundling with large-scale projects to meet RE100 commitments and drive offshore renewable growth.

South Pole: South Pole specializes in climate impact solutions, using strategies such as advisory services and REC bundling for voluntary buyers to facilitate carbon offsetting and ESG compliance in diverse sectors.

Tata Power: Tata Power focuses on solar and wind RECs in Asia, with strategies including multipliers for emerging technologies and Virtual PPAs to enhance self-consumption and corporate procurement in India.

What are the Market Trends?

- Increasing integration of AI and blockchain for real-time verification, forecasting, and transparent trading to reduce fraud and enhance market efficiency.

- Shift toward voluntary markets with corporate net-zero pledges, representing a growing share of green energy procurement through long-term agreements.

- Expansion of small-scale projects under 5 MW, particularly in solar, to promote distributed energy and local sustainability initiatives.

- Rise in cross-border REC trading via standards like I-RECs, enabling emerging markets to participate in global sustainability efforts.

- Evolving regulations aligning with Paris Agreement goals, including carbon pricing and multipliers for innovative renewable technologies.

- Growing adoption of bundled certificates linked to new projects, fostering direct investments in renewable infrastructure.

What Market Segments are Covered in the Report?

- By Energy Type

- Solar Power

- Wind Power

- Hydropower

- Biomass

- Others

- By End-Use

- Compliance

- Voluntary

- By Capacity

- Up to 1000 KWH

- 1001-5000 KWH

- Above 5000 KWH

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America