Hydrophobic Coatings Market Size, Share and Trends 2026 to 2035

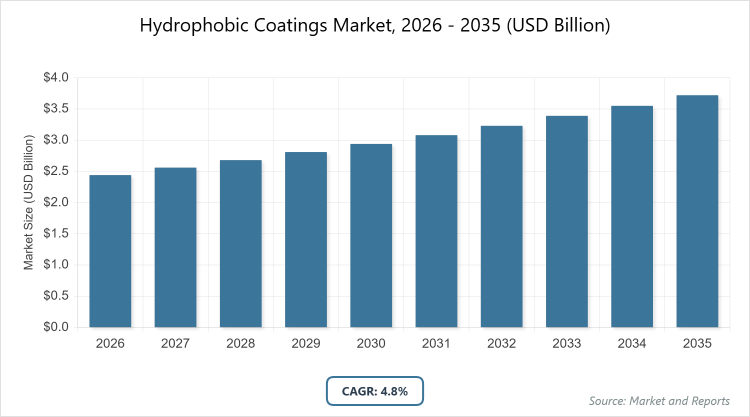

The global Hydrophobic Coatings Market size was estimated at USD 2.44 Billion in 2025 and is expected to reach USD 3.74 Billion by 2035, growing at a CAGR of 4.8% from 2026 to 2035. The global hydrophobic coatings market is primarily driven by the surging demand for water-resistant and self-cleaning surfaces across the automotive, construction, and consumer electronics industries to enhance product durability and performance.

What are the Key Insights into the Hydrophobic Coatings Market?

- Market Value in 2026: USD 2.44 billion

- Projected Market Value in 2035: USD 3.74 billion

- CAGR (2026-2035): 4.8%

- Dominated Subsegment in Property: Anti-Corrosion

- Dominated Subsegment in Substrate: Metal

- Dominated Subsegment in End-Use: Automotive

- Dominated Region: North America

What is the Hydrophobic Coatings Industry Overview?

Hydrophobic coatings are specialized surface treatments designed to repel water and other liquids, creating a high contact angle that causes droplets to bead up and roll off rather than spread or adhere. These coatings enhance material properties by providing self-cleaning, anti-corrosion, anti-fouling, anti-microbial, and anti-icing capabilities, making them essential for protecting substrates from moisture damage, contamination, and environmental degradation. They are applied across diverse industries to improve durability, reduce maintenance needs, and extend the lifespan of products, functioning through chemical compositions like fluoropolymers or silicones that alter surface energy without compromising the underlying material’s integrity.

What are the Market Dynamics in the Hydrophobic Coatings Sector?

The hydrophobic coatings market is propelled by increasing demand across key industries such as automotive, aerospace, construction, and electronics, where these coatings offer superior protection against water damage, corrosion, and fouling, thereby enhancing product longevity and performance. Rising automobile production and sales, coupled with advancements in material science like nanoparticle integrations, further fuel growth by enabling innovative applications in self-cleaning surfaces and wearable devices. Additionally, the expansion of infrastructure projects in emerging economies and a shift toward sustainable, eco-friendly coating solutions align with regulatory pressures, driving adoption and market expansion.

Restraints

Environmental concerns pose a significant restraint to the hydrophobic coatings market, as certain formulations, particularly those containing fluoropolymers, exhibit aquatic toxicity and persistence in ecosystems, leading to regulatory scrutiny and restrictions on their use. High production costs associated with advanced nanotechnology and raw materials also limit accessibility for small-scale manufacturers, while challenges in achieving long-term durability under extreme conditions can deter widespread adoption in price-sensitive sectors.

Opportunities

Opportunities in the hydrophobic coatings market abound with the growing healthcare sector’s need for anti-microbial and water-resistant coatings on medical devices and surgical tools, which can reduce infection risks and improve hygiene standards. Innovations in nanotechnology offer potential for developing multifunctional coatings that combine water repellency with additional properties like anti-icing or self-healing, opening new avenues in aerospace and marine applications. Furthermore, the rising demand for sustainable, fluorine-free alternatives presents a chance for market players to capitalize on eco-conscious consumer preferences and regulatory incentives.

Challenges

The hydrophobic coatings market faces challenges from fluctuating raw material prices and supply chain disruptions, which can impact production costs and availability, particularly for specialized components like fluoroalkylsilanes. Achieving uniform application and adhesion on complex surfaces remains technically demanding, often requiring advanced equipment and skilled labor, while competition from alternative protective technologies, such as hydrophilic coatings, adds pressure to innovate continuously.

Hydrophobic Coatings : Report Scope

| Report Attributes | Report Details |

| Report Name | Hydrophobic Coatings |

| Market Size 2025 | USD 2.44 Billion |

| Market Forecast 2035 | USD 3.74 Billion |

| Growth Rate | CAGR of 4.8% |

| Report Pages | 215 |

| Key Companies Covered |

3M Company, PPG Industries, Inc., BASF SE, The Sherwin-Williams Company, NeverWet, LLC, Aculon, Inc., NEI Corporation, Abrisa Technologies, Surfactis Technologies, and DryWired, LLC. |

| Segments Covered | By Property, By Substrate, By End-Use, By Region. |

| Regions Covered | Asia Pacific, North America, Europe, Latin America, The Middle East and Africa. |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Hydrophobic Coatings Market Segmented?

By Property, The anti-corrosion segment emerges as the most dominant in the property category, holding a significant revenue share due to its critical role in forming protective barriers that shield substrates from moisture and corrosive elements, thereby extending material lifespan in harsh environments like marine and aerospace applications; this dominance stems from widespread industrial needs for cost-effective maintenance reduction and enhanced durability, driving overall market growth by enabling reliable performance in high-stakes sectors. The anti-microbial segment ranks as the second most dominant, gaining traction for its ability to inhibit microbial growth on surfaces while repelling water, particularly in healthcare and electronics, where it supports infection control and device protection; its prominence is fueled by rising hygiene awareness and technological advancements, contributing to market expansion through specialized applications that address evolving consumer and regulatory demands for safer, longer-lasting products.

By Substrate, In the substrate segmentation, metal stands out as the most dominant due to its extensive use in automotive, aerospace, and construction industries where hydrophobic coatings prevent rust and degradation, ensuring structural integrity and reducing repair costs; this leadership position is attributed to the high volume of metal-based components in global manufacturing, propelling market growth by facilitating broader adoption in durability-focused applications. Glass follows as the second most dominant substrate, valued for its application in optical and architectural settings where coatings enhance water repellency for clearer visibility and easier cleaning; its significance arises from increasing demands in building facades and vehicle windshields, aiding market momentum by supporting innovations in energy-efficient and low-maintenance designs.

By End-Use, Automotive represents the most dominant end-use segment, capturing a substantial market share through applications on exteriors, windshields, and interiors to improve water shedding, visibility, and corrosion resistance amid expanding vehicle production in emerging markets; this dominance is driven by the sector’s emphasis on safety, aesthetics, and longevity, significantly boosting the overall market by integrating coatings into mass-produced vehicles. Construction ranks as the second most dominant, benefiting from coatings that protect buildings and infrastructure from moisture damage and staining during rapid urbanization; its role is amplified by sustainability trends and infrastructure investments, contributing to market growth via durable, eco-friendly solutions for long-term structural preservation.

What are the Recent Developments in the Hydrophobic Coatings Market?

In June 2024, NEI Corporation unveiled NANOMYTE AM-100EC, an advanced antimicrobial coating that delivers robust protection against microorganisms while maintaining easy-to-clean properties, making it ideal for healthcare and food processing environments where it withstands frequent cleaning without losing efficacy. Nippon Paint Holdings Co., Ltd. introduced FASTAR, a groundbreaking hydrolysis antifouling paint utilizing nanotechnology with a hydrophilic and hydrophobic nanodomain structure, marking a first in the industry for enhanced marine applications. Coat-X SA developed a novel superhydrophobic nanolayer aimed at improving the performance of community and commercial masks, offering an environmentally friendly silicon-based conformal coating that enables extreme hydrophobicity on complex 3D surfaces.

How Does Regional Analysis Shape the Hydrophobic Coatings Market?

North America leads the hydrophobic coatings market, driven by strong demand from automotive, aerospace, and textile sectors, with the United States as the dominating country due to its robust industrial base, high vehicle production, and emphasis on innovative, eco-friendly coatings that enhance durability and safety in commercial applications; this region’s prominence is supported by early technology adoption and regulatory focus on sustainability, fostering market growth through widespread integration in electronics and medical devices.

Asia Pacific emerges as the fastest-growing region, propelled by industrialization and infrastructure expansion, with China as the dominating country owing to its massive manufacturing output, rising electric vehicle adoption, and construction boom that increases the need for protective coatings; India’s contributions in pharmaceuticals and healthcare further bolster the area, capitalizing on cost-effective production and emerging markets for water-resistant textiles and electronics. Europe holds a significant position with steady growth in marine, automotive, and construction industries, where Germany dominates through its engineering prowess and focus on anti-corrosive solutions for vehicles and infrastructure; the United Kingdom supports this with advancements in nanotechnology and self-cleaning applications, aligning with environmental regulations to drive innovation in sustainable coatings.

Latin America shows moderate potential, led by Brazil’s infrastructure and automotive sectors that utilize coatings for corrosion protection in tropical climates, though growth is tempered by economic variability; the region’s emphasis on building durability amid urbanization presents opportunities for expanded adoption.

The Middle East and Africa exhibit emerging interest, with South Africa as a key player in construction and mining applications where coatings combat harsh environmental conditions; Israel’s technological innovations in medical and aerospace further contribute, though challenges like regulatory hurdles limit broader penetration.

Who are the Key Market Players and What are Their Strategies in Hydrophobic Coatings?

3M Company employs a strategy of continuous innovation in material science, focusing on developing multifunctional coatings that integrate anti-corrosion and self-cleaning properties to cater to automotive and electronics sectors, while expanding through strategic partnerships to enhance global distribution.

PPG Industries, Inc. prioritizes sustainability by investing in fluorine-free formulations and nanotechnology, aiming to meet regulatory demands and capture market share in aerospace and construction via acquisitions and R&D collaborations.

BASF SE leverages its chemical expertise to create eco-friendly, high-performance coatings, emphasizing product diversification and supply chain optimization to dominate in anti-microbial applications for healthcare and textiles.

The Sherwin-Williams Company focuses on application-specific solutions, such as anti-icing for marine uses, through targeted marketing and customer-centric development to strengthen its position in North American and European markets.

NeverWet, LLC specializes in superhydrophobic technologies, pursuing aggressive patenting and licensing agreements to expand into consumer products like textiles and electronics, driving growth via niche innovation.

Aculon, Inc. adopts a strategy of customization for industrial clients, emphasizing nanoscale treatments for metals and glass to improve adhesion and durability, supported by rapid prototyping and technical support services.

NEI Corporation concentrates on antimicrobial and self-cleaning advancements, utilizing government grants and university partnerships to accelerate product launches and penetrate healthcare and food processing segments.

Abrisa Technologies targets optical and glass substrates, implementing vertical integration to control quality and reduce costs, while exploring emerging markets in Asia Pacific for expansion.

Surfactis Technologies focuses on bio-based alternatives, investing in R&D for non-toxic coatings to align with environmental trends and secure contracts in medical and aerospace industries.

DryWired, LLC pursues global outreach through e-commerce and distributor networks, specializing in easy-to-apply solutions for consumer electronics to capitalize on wearable device trends.

What are the Current Market Trends in Hydrophobic Coatings?

- Increasing adoption of nanotechnology for multifunctional coatings that combine water repellency with anti-icing and self-healing properties.

- Shift toward eco-friendly, fluorine-free formulations to comply with environmental regulations and meet consumer demands for sustainable products.

- Growing integration in wearable and underwater electronics for enhanced moisture protection and durability.

- Rising demand for self-cleaning textiles and anti-microbial surfaces in healthcare and construction sectors.

- Advancements in smart coating technologies, including those responsive to environmental changes for improved performance.

What Market Segments are Covered in the Hydrophobic Coatings Report?

By Property:

- Anti-Corrosion,

- Anti-Microbial,

- Anti-Icing/Wetting,

- Anti-Fouling,

- Self-Cleaning,

- Others

By Substrate:

- Metal

- Glass

- Polymer

- Concrete

- Ceramics

- Others

By End-Use:

- Automotive

- Aerospace

- Textile

- Construction

- Medical

- Electronics

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Hydrophobic coatings are surface treatments that repel water and liquids, creating beading effects to prevent adhesion, and offer properties like self-cleaning, anti-corrosion, and anti-microbial protection for various substrates.

Key factors include rising demand in automotive and construction, advancements in nanotechnology, regulatory push for sustainable formulations, and expanding applications in healthcare and electronics.

The market is projected to grow from USD 2.44 billion in 2026 to USD 3.74 billion by 2035.

The CAGR is anticipated to be 4.8% during 2026-2035.

North America will contribute notably, driven by strong industrial adoption in the United States.

Major players include 3M Company, PPG Industries, Inc., BASF SE, The Sherwin-Williams Company, and NeverWet, LLC.

The report provides comprehensive insights into market size, forecasts, segmentation, regional analysis, key players, drivers, restraints, opportunities, trends, and recent developments.

The value chain includes raw material sourcing (e.g., fluoropolymers, silicones), manufacturing and formulation, distribution and application, end-use integration, and after-sales support like maintenance.

Trends are shifting toward eco-friendly and multifunctional coatings, with consumers preferring sustainable, durable solutions for self-cleaning and protective applications in everyday products.

Regulations on aquatic toxicity and fluorinated compounds are pushing for fluorine-free alternatives, while environmental awareness drives demand for low-impact, sustainable coatings.