Forging Market Size, Share, Growth and Forecast 2026 to 2035

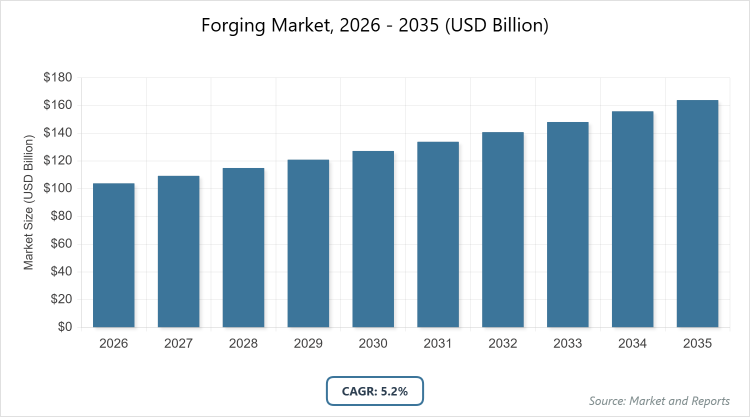

According to our latest research, the global forging market is projected to grow from USD 103.88 billion in 2026 to USD 163.04 billion by 2035, growing at a CAGR is estimated at 5.2% during 2026-2035. The Forging Market is primarily driven by the surging demand for high-strength, lightweight components in the automotive and aerospace sectors, fueled by the global transition toward electric vehicles (EVs) and the recovery of commercial aircraft production.

What are the Key Insights into the Forging Market?

- Global market value projected to reach USD 163.04 billion by 2035 from USD 103.88 billion in 2026.

- Compound Annual Growth Rate (CAGR) estimated at 5.2% during 2026-2035.

- Closed die forgings dominate the type segment.

- Automotive dominates the application segment.

- Asia Pacific dominates the regional market.

What is the Forging Market?

Industry Overview

The forging market encompasses the manufacturing process of shaping metal using localized compressive forces, typically with hammers or dies, to produce high-strength components for industries such as automotive, aerospace, construction, and energy. This technique includes open-die, closed-die, and rolled-ring methods, utilizing materials like steel, aluminum, and titanium to create durable parts like crankshafts, gears, and turbine rotors that offer superior mechanical properties compared to casting or machining. The market involves raw material suppliers, forging companies, and end-users, driven by the need for lightweight, high-performance components in modern applications, while emphasizing innovation in automation and sustainable practices to reduce waste and energy consumption.

It operates within a global supply chain focused on precision, quality control, and compliance with industry standards, addressing demands for cost-effective production in a competitive landscape influenced by technological advancements and environmental regulations.

What are the Market Dynamics in the Forging Market?

Growth Drivers

The forging market is propelled by surging demand from the automotive and aerospace sectors for high-strength, lightweight components like crankshafts and turbine rotors, fueled by the rise of electric vehicles and advanced aircraft that require durable parts to enhance performance and fuel efficiency, alongside global infrastructure development, boosting needs in construction and energy industries. Technological advancements in automation, AI, and IoT streamline production processes, improving precision and reducing costs, while government incentives for manufacturing and renewable energy projects encourage investments in forging capabilities. Additionally, the shift toward sustainable materials and green forging techniques aligns with corporate ESG goals, driving adoption of energy-efficient methods that minimize emissions and waste.

Restraints

Restraints in the forging market include high capital and operational costs for modern equipment and tooling, which limit entry for small manufacturers and strain profitability amid fluctuating raw material prices like steel and aluminum influenced by supply chain disruptions. Skilled labor shortages and the need for specialized training hinder production efficiency, while competition from alternative processes like casting or additive manufacturing offers cheaper options for certain applications. Environmental regulations on emissions and energy use add compliance burdens, particularly in regions with stringent standards, potentially slowing expansion in cost-sensitive markets.

Opportunities

Opportunities lie in the adoption of advanced materials such as titanium and aluminum alloys for lightweight applications in EVs and aerospace, where innovations in precision forging and 3D printing hybrids can capture high-margin segments, alongside emerging economies’ industrialization creating demand for infrastructure-related forgings. Partnerships for sustainable practices and automation can attract investments, while the integration of Industry 4.0 technologies opens avenues for smart manufacturing solutions. Expansion into renewable energy components, like wind turbine parts, offers growth amid global green transitions, fostering collaborations with OEMs for customized, eco-friendly products.

Challenges

Challenges encompass erratic raw material costs and supply chain vulnerabilities that disrupt operations and pricing stability, compounded by a skilled labor shortage requiring ongoing training to handle advanced automation. Environmental regulations demand investments in green technologies, while competition from substitutes like additive manufacturing pressures innovation. Geopolitical tensions affect global trade, necessitating resilient supply chains to mitigate risks and ensure continuity in high-demand sectors like automotive and aerospace.

Forging Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Forging Market |

| Market Size 2025 | USD 103.88 Billion |

| Market Forecast 2035 | USD 163.04 Billion |

| Growth Rate | CAGR of 5.2% |

| Report Pages | 220 |

| Key Companies Covered | Nippon Steel & Sumitomo Metal, Thyssenkrupp, Bharat Forge, KOBELCO, Arconic, Aichi Steel, and American Axle & Manufacturing (AAM) |

| Segments Covered | By Type, By Application, By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation Analysis for the Forging Market?

The forging market is segmented by type, application, and region.

By type segment, closed die forgings emerge as the most dominant subsegment, followed by open die forgings as the second most dominant. Closed die forgings lead due to their precision in creating complex, high-strength parts with minimal waste, ideal for automotive and aerospace applications like gears and connecting rods where uniformity and durability are critical; this dominance drives the market by enabling mass production efficiency, attracting investments in advanced dies and automation that reduce costs and improve quality, thereby expanding adoption in high-volume industries and boosting overall revenue through premium pricing for intricate components. Open die forgings, as the second dominant, offer flexibility for large, custom parts like shafts in power generation, contributing to market growth by catering to heavy industries with cost-effective methods for bulk items.

By application segment, Automotive is the most dominant subsegment in the application segment, followed by aerospace as the second most dominant. Automotive dominates owing to high demand for lightweight, high-strength components like crankshafts and chassis parts in EVs and traditional vehicles, driven by global production growth and fuel efficiency needs; this leadership propels the market by generating volume sales, fostering material innovations like aluminum alloys, and enabling supply chain integrations that lower costs and support expansion into emerging auto hubs, thus increasing market scale and investment. Aerospace, with needs for turbine rotors and landing gear, contributes through high-value, precision forgings that align with safety standards, supporting growth via defense and commercial aviation demands.

What are the Recent Developments in the Forging Market?

- In September 2025, Scot Forge expanded its open-die forging capabilities with a new hydraulic press at its Illinois facility, handling larger components in titanium and nickel alloys for aerospace and defense, reducing lead times and supporting customized solutions.

- In November 2025, advancements in closed die forging technology were highlighted, with automation integrations improving precision for automotive applications amid industry growth.

What is the Regional Analysis of the Forging Market?

- Asia-Pacific to dominate the market

Asia Pacific holds the largest share in the forging market, driven by rapid industrialization, automotive production hubs, and infrastructure investments; China dominates this region with approximately 30% global share, through its massive manufacturing base, low-cost labor, and policies like Made in China 2025 that promote high-tech forging for EVs and machinery, enabling exports and addressing domestic demand in construction and energy sectors amid urbanization.

Europe represents a mature market with focus on automotive and aerospace, where Germany leads through its engineering prowess, companies like Thyssenkrupp, and EU sustainability directives promoting green forging for wind turbines and vehicles, supported by France and Italy in precision components.

North America shows steady growth with high-tech applications in defense and oil/gas, led by the United States through reshoring initiatives, advanced alloys for aerospace, and investments in automation to enhance competitiveness.

Who are the Key Market Players and Their Strategies in the Forging Market?

- Nippon Steel & Sumitomo Metal focuses on technology improvements and automation to enhance automotive forgings, expanding capacities for lightweight alloys.

- Thyssenkrupp emphasizes global manufacturing and strong industry relationships, investing in precision for aerospace and sustainability practices.

- Bharat Forge targets automotive and emerging markets, pursuing expansions and innovations in energy-efficient forging for commercial vehicles.

- KOBELCO leverages Asia-Pacific advantages in cost and logistics, focusing on eco-friendly operations and product diversification.

- Arconic concentrates on high-performance aerospace forgings, employing mergers and R&D for advanced materials.

- Aichi Steel adopts eco-friendly strategies and capacity increases to meet automotive demands.

- American Axle & Manufacturing (AAM) customizes solutions for automotive, integrating supply chains for efficiency.

What are the Market Trends in the Forging Market?

- Integration of AI-IoT for automation, precision, and quality control in processes.

- Shift to lightweight materials like aluminum and titanium alloys for fuel efficiency.

- Emphasis on sustainability and green forging to reduce emissions.

- Advancements in production for high-strength components in EVs and aerospace.

- Adoption of Industry 4.0 technologies like robotics and simulation software.

What Market Segments are Covered in the Forging Market Report?

By Type

- Closed Die Forgings

- Open Die Forgings

- Rolled Rings Forgings

By Application

- Automotive

- Aerospace

- Agricultural

- General Industrial

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Forging Market - Industry Analysis

Chapter 4. Global Forging Market- Competitive Landscape

Chapter 5. Global Forging Market - Type Analysis

Chapter 6. Global Forging Market - Application Analysis

Chapter 7. Forging Market - Regional Analysis

Chapter 8. Company Profiles

Frequently Asked Questions

Forging is a metalworking process that shapes metal using compressive forces, often with dies or hammers, to produce strong, durable components for industries like automotive and aerospace.

Key factors include demand from automotive and aerospace for high-strength parts, technological advancements in automation, raw material volatility, sustainability trends, and infrastructure growth in emerging economies.

The market is projected to grow from USD 103.88 billion in 2026 to USD 163.04 billion by 2035.

The CAGR is estimated at 5.2% during 2026-2035.

Asia Pacific will contribute notably, holding the largest share due to manufacturing hubs and industrialization.

Major players include Nippon Steel & Sumitomo Metal, Thyssenkrupp, Bharat Forge, KOBELCO, Arconic, Aichi Steel, and American Axle & Manufacturing (AAM).

The report provides insights into market size, forecasts, segmentation, regional analysis, key players, trends, dynamics, and developments.

The value chain includes raw material sourcing (metals like steel, aluminum), forging processes (compression forming), automation and technology integration (AI-IoT, 3D printing), and distribution of finished components to industries like automotive and aerospace.

Trends are evolving toward AI-IoT automation and lightweight materials, with preferences shifting to sustainable, high-performance components for EVs and aerospace.

Regulatory factors include emission standards and trade policies, while environmental factors involve sustainability demands pushing for green forging and reduced waste.