Smart Building Market Size and Forecast 2026 to 2035

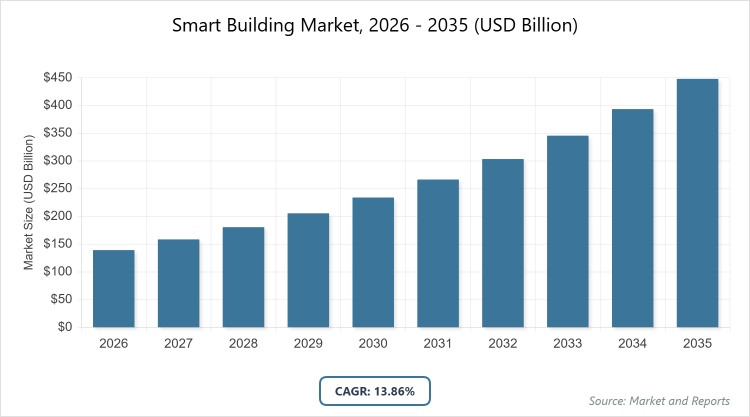

According to MarketnReports, the global Smart Building market size was estimated at USD 139.30 billion in 2025 and is expected to reach USD 510.13 billion by 2035, growing at a CAGR of 13.86% from 2026 to 2035. Smart Building Market is driven by the increasing adoption of IoT, AI, and energy-efficient technologies to enhance building automation, safety, and operational efficiency.

What are the Key Insights?

- Market Value and CAGR: The global smart building market was valued at USD 139.30 billion in 2025 and is projected to reach USD 510.13 billion by 2035, registering a CAGR of 13.86% from 2026 to 2035.

- Dominated Subsegment by Component: The solution segment dominated with over 77% revenue share in 2025.

- Dominated Subsegment by Solution: The safety & security management segment held the largest market share in 2025.

- Dominated Subsegment by Service: The implementation segment accounted for the largest market share in 2025.

- Dominated Subsegment by Building Type: The commercial segment led with over 53% market share in 2025.

- Dominated Region: North America held the largest revenue share of over 35% in 2025.

What is the Industry Overview?

Smart buildings represent an advanced ecosystem where various building systems, including heating, ventilation, air conditioning, lighting, security, and facility management, are interconnected through a centralized platform powered by technologies like the Internet of Things, artificial intelligence, and data analytics. This integration allows for real-time monitoring, predictive maintenance, and automated decision-making to optimize energy use, enhance occupant comfort, and improve overall operational efficiency. The market encompasses solutions and services that transform traditional structures into intelligent environments, catering to commercial, residential, and industrial applications. It thrives on the convergence of digitalization and sustainability, enabling buildings to adapt dynamically to user needs while reducing environmental impact through efficient resource management and seamless system interoperability.

What are the Market Dynamics?

Growth Drivers

The smart building market is propelled by the surging adoption of IoT-enabled building management systems that facilitate seamless integration and real-time data insights, coupled with a rising demand for energy-efficient solutions amid global sustainability goals. Technological advancements in automation, AI-driven analytics, and data management further accelerate growth by enabling predictive maintenance and optimized resource allocation. Urbanization and government initiatives promoting green building certifications encourage investments from both public and private sectors, while the integration of renewable energy systems and smart grids enhances environmental compliance. Additionally, the shift toward hybrid work models and the popularity of home automation drive demand for intelligent space utilization and remote management, fostering innovation through partnerships between tech providers and real estate developers.

Restraints

The smart building market faces hurdles from high initial implementation costs and the complexity of integrating diverse legacy systems, which can deter adoption in smaller or budget-constrained projects. Concerns over data privacy and cybersecurity vulnerabilities arise as interconnected systems increase exposure to potential breaches, requiring robust safeguards that add to expenses. Limited interoperability between different vendors’ technologies often leads to fragmented solutions, complicating deployment and maintenance. Moreover, a shortage of skilled professionals in emerging markets hinders effective system management and upgrades, while regulatory inconsistencies across regions can slow down standardization efforts and market expansion.

Opportunities

The smart building market presents significant potential through the integration of emerging technologies like edge computing and digital twins, which can enhance operational excellence and create new revenue streams for predictive and adaptive building platforms. The rise of hybrid work environments opens avenues for advanced occupancy sensors and workspace management tools to optimize space and energy use. Government policies aimed at decarbonization and clean energy adoption, including incentives for large-scale retrofits and low-carbon technologies, provide opportunities for market players to expand in sustainable infrastructure. Additionally, increasing investments in smart city initiatives and the growing demand for resilient buildings in disaster-prone areas offer pathways for innovation in renewable integration and real-time monitoring systems.

Challenges

The smart building market encounters obstacles in achieving seamless interoperability among diverse systems and vendors, which can lead to inefficiencies and higher costs during integration. Cybersecurity threats pose a persistent risk as buildings become more connected, necessitating continuous advancements in protective measures to safeguard sensitive data. Rapid technological evolution demands ongoing training and upskilling of the workforce, while economic fluctuations and supply chain disruptions can impact the availability of components like sensors and microchips. Furthermore, varying regional regulations on energy efficiency and data privacy create compliance complexities, potentially delaying project timelines and increasing operational overheads for global players.

Table Code (Report Scope)

Smart Building Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Smart Building Market |

| Market Size 2025 | USD 139.30 Billion |

| Market Forecast 2035 | USD 510.13 Billion |

| Growth Rate | CAGR of 13.86% |

| Report Pages | 210 |

| Key Companies Covered |

ABB Ltd., Johnson Controls, Cisco Systems Inc., Emerson Electric Co., Siemens AG, Honeywell International Inc., and Schneider Electric Corporation |

| Segments Covered | By Component, By Solution, By Service, By Building Type, and By Region. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

Smart Building Market: Segmentation Analysis

The Smart Building market is segmented by component, solution, service, building type, end use, and region.

By Component

The solution segment emerged as the most dominant in the smart building market, capturing over 77% of the revenue share in 2025, primarily due to its comprehensive offerings that include advanced technologies like AI-enhanced access control, biometric systems, video surveillance, and energy optimization tools, which directly address core needs for security and efficiency in modern buildings; this dominance drives the market by enabling centralized control and data-driven insights that reduce operational costs and enhance sustainability, making it indispensable for large-scale commercial and industrial applications. The service segment stands as the second most dominant, poised for the fastest growth at a CAGR of 20.7% from 2026 to 2033, encompassing predictive maintenance, commissioning, and remote monitoring that support long-term system performance; its role in ensuring ongoing efficiency and upgrades helps propel market expansion by providing value-added support that extends the lifecycle of solutions and fosters customer loyalty.

By Solution

The safety & security management segment dominated the market in 2025, driven by heightened global concerns over building safety and the integration of AI-powered features like video surveillance, access control, and emergency communication systems that provide robust protection against threats; this leadership accelerates market growth by meeting regulatory requirements and enhancing occupant trust, particularly in high-traffic commercial spaces where real-time monitoring minimizes risks and operational disruptions. The energy management segment ranks as the second most dominant, expected to achieve the fastest CAGR from 2026 to 2033, featuring technologies such as HVAC controls, lighting management, and smart metering that optimize energy consumption; its influence on the market stems from aligning with sustainability mandates and cost-saving imperatives, enabling buildings to achieve net-zero goals and attract eco-conscious investors through reduced utility bills and environmental impact.

By Service

The implementation segment held the largest market share in 2025, attributed to its critical role in the initial deployment of smart technologies including sensors, actuators, and integrated systems that form the foundation of building automation; this dominance fuels market progression by ensuring seamless setup and immediate functionality, which is essential for realizing quick returns on investment in energy savings and operational improvements across diverse building types. The support & maintenance segment is the second most dominant, anticipated to register the fastest CAGR from 2026 to 2033, offering ongoing services like system upgrades, energy audits, and remote diagnostics to maintain peak performance; it contributes to market momentum by addressing post-deployment needs, preventing downtime, and enabling adaptive enhancements that align with evolving technological and regulatory landscapes.

By Building Type

The commercial segment led with over 53% market share in 2025, encompassing applications in offices, retail, hospitality, and healthcare where smart solutions like integrated HVAC and security systems enhance efficiency and user experience; its preeminence drives the market by catering to high-volume sectors with substantial energy demands, facilitating cost reductions and compliance with green standards that appeal to corporate sustainability agendas. The residential segment is the second most dominant, projected for significant CAGR growth from 2026 to 2033, incorporating features such as smart door locks, lighting, and meters for home automation; this segment advances the market by tapping into consumer preferences for convenience and energy conservation, especially in urbanizing areas where remote management and integration with IoT devices promote widespread adoption and innovation.

What are the Recent Developments?

- In December 2025, Cisco Systems Inc. announced its Advisor Select partnership with Environments to enhance network integration and automation in smart buildings, targeting sectors like offices, education, healthcare, retail, industrial facilities, and data centers through IoT ecosystems involving cameras, sensors, thermostats, lighting controls, speakers, security devices, and shades, thereby advancing interoperability and operational efficiency.

- In November 2025, ABB Ltd. launched the ABB Ability BuildingPro platform, a cybersecure integration solution designed to connect, manage, and optimize building operations across commercial real estate, education, healthcare, hospitality, and government sectors, unifying data from various systems to improve performance, reduce energy consumption, and enhance occupant experience with an open architecture for future AI-driven tools.

- In July 2025, Siemens AG collaborated with Microsoft to enable interoperability between Siemens’ Building X digital platform and Microsoft Azure IoT Operations, aiming to transform IoT data utilization in buildings, particularly in commercial, data center, and higher education facilities, to support real-time insights and enhanced management capabilities.

What is the Regional Analysis?

North America to dominate the market

North America dominated the global smart building market with over 35% revenue share in 2025, fueled by substantial public and private investments in digitalization across commercial, industrial, and residential sectors, alongside rapid adoption of IoT technologies and advancements in infrastructure that boost automation, energy efficiency, and security; the region’s leadership is supported by innovative policies promoting sustainability and smart city developments, with the United States as the dominating country holding over 74% share, driven by government focus on digitizing buildings for transparency, citizen experiences, and operational excellence in converting traditional offices into energy-efficient smart structures.

Europe is projected to grow at a CAGR of over 17% from 2026 to 2033, propelled by the integration of Industry 4.0 technologies like big data analytics, IoT, AI, and machine learning in building operations to enhance occupant safety, efficiency, predictive maintenance, and sustainability; government priorities on digitalization and decarbonization further accelerate adoption, with Germany as the dominating country, emphasizing energy cost reductions through advanced management systems for heating, ventilation, air conditioning, lighting, and electrical operations amid rising energy prices.

Asia Pacific is expected to register the fastest CAGR of 21.6% from 2026 to 2033, driven by rapid urbanization, increasing internet penetration, and a preference for IoT-powered remote building management, with governments investing heavily in smart infrastructure to upgrade commercial and residential properties; this growth is bolstered by consumer shifts toward smart-enabled facilities and 5G rollout, with China as the dominating country, advancing through digitalization of systems, widespread 5G-IoT networks, and tech giants like Huawei and ZTE developing cloud-integrated platforms for energy optimization, maintenance, and comfort.

Latin America shows promising growth in the smart building market, supported by emerging urbanization and investments in sustainable infrastructure, though adoption lags due to economic constraints; focus areas include commercial and residential sectors integrating basic IoT for energy management, with Brazil as the dominating country, leveraging government initiatives for green buildings and digital transformation to enhance efficiency in urban centers.

Middle East & Africa is experiencing gradual expansion in smart buildings, driven by oil-rich economies investing in diversification through smart city projects and energy-efficient technologies; challenges like infrastructure gaps persist, but opportunities in commercial developments abound, with the United Arab Emirates as the dominating country, prioritizing advanced automation in iconic structures to align with sustainability visions and attract global investments.

Who are the Key Market Players and Their Strategies?

- ABB Ltd.: Focuses on operating across motion, robotics & discrete automation, electrification, and process automation segments, offering products to 24 industries including smart cities and data centers, while investing in technology ventures like AFC Energy and Numocity through ABB Technology Ventures, and maintaining a global service network in over 100 countries to ensure scalability and innovation.

- Johnson Controls: Emphasizes designing control and automation systems with a diverse portfolio covering HVAC, security, fire detection, and digital solutions, serving sectors like data centers, healthcare, and government, by prioritizing building automation and distributed energy storage to drive operational efficiency and sustainability.

- Cisco Systems Inc.: Specializes in hardware and software solutions for industries such as smart buildings, education, and healthcare, offering cloud, IoT, security, and analytics tools, while forming partnerships like the Advisor Select with Environments to enhance network integration and IoT ecosystems for automation.

- Emerson Electric Co.: Develops automation and residential solutions including fluid controls, measurement instruments, and HVAC systems, with strategies centered on providing comprehensive product lines and service kits to optimize performance in commercial and industrial applications.

- Siemens AG: Pursues collaborations such as with Microsoft for interoperability between Building X and Azure IoT Operations, focusing on digital platforms for IoT data utilization in commercial and educational facilities to advance real-time management and energy optimization.

- Honeywell International Inc.: Concentrates on integrated building management systems combining security, energy, and automation, leveraging AI and IoT to offer scalable solutions that enhance occupant comfort and reduce costs across global markets.

- Schneider Electric Corporation: Employs strategies around eco-friendly automation and energy management, developing platforms for seamless system integration and sustainability, with emphasis on partnerships to expand in smart infrastructure.

What are the Market Trends?

- Technological advancements in AI-powered analytics, edge computing, and digital twins are redefining building management by enabling predictive platforms that reduce costs and improve efficiency.

- Building management systems are evolving into adaptive tools integrated with renewable energy and smart grids to support global carbon reduction and sustainability commitments.

- The rise of hybrid work models is driving demand for occupancy sensors and intelligent workspace management to optimize space utilization and energy consumption.

- Governments are intensifying policies for clean energy, large-scale retrofits, and low-carbon technologies to combat climate change and create green jobs.

- Competitive dynamics feature innovative startups and established firms emphasizing interoperability, cybersecurity, and scalable solutions through strategic partnerships.

- Investment in infrastructure modernization is accelerating, with a focus on IoT, cloud computing, and data analytics for enhanced operational excellence.

- Growing popularity of home automation and remote work preferences are boosting residential adoption of smart technologies for convenience and efficiency.

What Market Segments are Covered in the Report?

By Component

-

- Solution

-

- Service

By Solution

-

- Safety & Security Management

-

-

- Access Control System

-

-

-

- Video Surveillance System

-

-

-

- Fire and Life Safety System

-

-

- Energy Management

-

-

- HVAC Control System

-

-

-

- Lighting Management System

-

-

-

- Others

-

-

- Building Infrastructure Management

-

-

- Parking Management System

-

-

-

- Water Management System

-

-

-

- Others

-

-

- Network Management

-

-

- Wired Technology

-

-

-

- Wireless Technology

-

-

- Integrated Workplace Management System (IWMS)

-

-

- Real Estate Management

-

-

-

- Capital Project Management

-

-

-

- Facility Management

-

-

-

- Operations and Services Management

-

-

-

- Environment and Energy Management

-

By Service

-

- Consulting

-

- Implementation

-

- Support & Maintenance

By End Use

-

- Residential

-

- Commercial

-

-

- Healthcare

-

-

-

- Retail

-

-

-

- Academic

-

-

-

- Others

-

-

- Industrial

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

1.1 Report Description and Scope1.2 Research Scope1.3 Research Methodology1.3.1 Market Research Type1.3.2 Market Research MethodologyChapter 2. Executive Summary

2.1 Global Smart Building Market, (2026 - 2035) (USD Billion)2.2 Global Smart Building Market: SnapshotChapter 3. Global Smart Building Market - Industry Analysis

3.1 Smart Building Market: Market Dynamics3.2 Market Drivers3.2.1 The smart building market is growing rapidly as IoT, AI, and sustainability goals drive demand for energy-efficient automation, predictive maintenance, and intelligent space management.3.3 Market Restraints3.3.1 Growth in the smart building market is hindered by high costs, legacy system complexity, cybersecurity risks, and a lack of interoperability and skilled labor.3.4 Market Opportunities3.4.1 The smart building market is poised for growth through the adoption of digital twins, edge computing, and hybrid-work tools, supported by government decarbonization policies and smart city investments.3.5 Market Challenges3.5.1 Smart building progress is frequently stalled by system interoperability issues, escalating cybersecurity risks, workforce skill gaps, and supply chain-driven component shortages.3.6 Porter’s Five Forces Analysis3.7 Market Attractiveness Analysis3.7.1 Market Attractiveness Analysis By Component3.7.2 Market Attractiveness Analysis By Solution3.7.3 Market Attractiveness Analysis By Service3.7.4 Market Attractiveness Analysis By End UseChapter 4. Global Smart Building Market- Competitive Landscape

4.1 Company Market Share Analysis4.1.1 Global Smart Building Market: Company Market Share, 20254.2 Strategic Development4.2.1 Acquisitions & mergers4.2.2 New Product launches4.2.3 Agreements, partnerships, collaborations, and joint ventures4.2.4 Research and development and regional expansion4.3 Price Trend AnalysisChapter 5. Global Smart Building Market - Component Analysis

5.1 Global Smart Building Market Overview: Component5.1.1 Global Smart Building Market share, By Component, 2025 and 20355.2 Solution5.2.1 Global Smart Building Market by Solution, 2026 - 2035 (USD Billion)5.3 Service5.3.1 Global Smart Building Market by Service, 2026 - 2035 (USD Billion)Chapter 6. Global Smart Building Market - Solution Analysis

6.1 Global Smart Building Market Overview: Solution6.1.1 Global Smart Building Market Share, By Solution, 2025 and 20356.2 Safety & Security Management6.2.1 Global Smart Building Market by Safety & Security Management, 2026 - 2035 (USD Billion)6.3 Energy Management6.3.1 Global Smart Building Market by Energy Management, 2026 - 2035 (USD Billion)6.4 Building Infrastructure Management6.4.1 Global Smart Building Market by Building Infrastructure Management, 2026 - 2035 (USD Billion)6.5 Network Management6.5.1 Global Smart Building Market by Network Management, 2026 - 2035 (USD Billion)6.6 Integrated Workplace Management System (IWMS)6.6.1 Global Smart Building Market by Integrated Workplace Management System (IWMS), 2026 - 2035 (USD Billion)Chapter 7. Global Smart Building Market - Service Analysis

7.1 Global Smart Building Market Overview: Service7.1.1 Global Smart Building Market Share, By Service, 2025 and 20357.2 Consulting7.2.1 Global Smart Building Market by Consulting, 2026 - 2035 (USD Billion)7.3 Implementation7.3.1 Global Smart Building Market by Implementation, 2026 - 2035 (USD Billion)7.4 Support & Maintenance7.4.1 Global Smart Building Market by Support & Maintenance, 2026 - 2035 (USD Billion)Chapter 8. Global Smart Building Market - End Use Analysis

8.1 Global Smart Building Market Overview: End Use8.1.1 Global Smart Building Market Share, By End Use, 2025 and 20358.2 Residential8.2.1 Global Smart Building Market by Residential, 2026 - 2035 (USD Billion)8.3 Commercial8.3.1 Global Smart Building Market by Commercial, 2026 - 2035 (USD Billion)8.4 Industrial8.4.1 Global Smart Building Market by Industrial, 2026 - 2035 (USD Billion)Chapter 9. Smart Building Market - Regional Analysis

9.1 Global Smart Building Market Regional Overview9.2 Global Smart Building Market Share, by Region, 2025 & 2035 (USD Billion)9.3 North America9.3.1 North America Smart Building Market, 2026 - 2035 (USD Billion)9.3.1.1 North America Smart Building Market, by Country, 2026 - 2035 (USD Billion)9.3.2 North America Smart Building Market, by Component, 2026 - 20359.3.2.1 North America Smart Building Market, by Component, 2026 - 2035 (USD Billion)9.3.3 North America Smart Building Market, by Solution, 2026 - 20359.3.3.1 North America Smart Building Market, by Solution, 2026 - 2035 (USD Billion)9.3.4 North America Smart Building Market, by Service, 2026 - 20359.3.4.1 North America Smart Building Market, by Service, 2026 - 2035 (USD Billion)9.3.5 North America Smart Building Market, by End Use, 2026 - 20359.3.5.1 North America Smart Building Market, by End Use, 2026 - 2035 (USD Billion)9.4 Europe9.4.1 Europe Smart Building Market, 2026 - 2035 (USD Billion)9.4.1.1 Europe Smart Building Market, by Country, 2026 - 2035 (USD Billion)9.4.2 Europe Smart Building Market, by Component, 2026 - 20359.4.2.1 Europe Smart Building Market, by Component, 2026 - 2035 (USD Billion)9.4.3 Europe Smart Building Market, by Solution, 2026 - 20359.4.3.1 Europe Smart Building Market, by Solution, 2026 - 2035 (USD Billion)9.4.4 Europe Smart Building Market, by Service, 2026 - 20359.4.4.1 Europe Smart Building Market, by Service, 2026 - 2035 (USD Billion)9.4.5 Europe Smart Building Market, by End Use, 2026 - 20359.4.5.1 Europe Smart Building Market, by End Use, 2026 - 2035 (USD Billion)9.5 Asia Pacific9.5.1 Asia Pacific Smart Building Market, 2026 - 2035 (USD Billion)9.5.1.1 Asia Pacific Smart Building Market, by Country, 2026 - 2035 (USD Billion)9.5.2 Asia Pacific Smart Building Market, by Component, 2026 - 20359.5.2.1 Asia Pacific Smart Building Market, by Component, 2026 - 2035 (USD Billion)9.5.3 Asia Pacific Smart Building Market, by Solution, 2026 - 20359.5.3.1 Asia Pacific Smart Building Market, by Solution, 2026 - 2035 (USD Billion)9.5.4 Asia Pacific Smart Building Market, by Service, 2026 - 20359.5.4.1 Asia Pacific Smart Building Market, by Service, 2026 - 2035 (USD Billion)9.5.5 Asia Pacific Smart Building Market, by End Use, 2026 - 20359.5.5.1 Asia Pacific Smart Building Market, by End Use, 2026 - 2035 (USD Billion)9.6 Latin America9.6.1 Latin America Smart Building Market, 2026 - 2035 (USD Billion)9.6.1.1 Latin America Smart Building Market, by Country, 2026 - 2035 (USD Billion)9.6.2 Latin America Smart Building Market, by Component, 2026 - 20359.6.2.1 Latin America Smart Building Market, by Component, 2026 - 2035 (USD Billion)9.6.3 Latin America Smart Building Market, by Solution, 2026 - 20359.6.3.1 Latin America Smart Building Market, by Solution, 2026 - 2035 (USD Billion)9.6.4 Latin America Smart Building Market, by Service, 2026 - 20359.6.4.1 Latin America Smart Building Market, by Service, 2026 - 2035 (USD Billion)9.6.5 Latin America Smart Building Market, by End Use, 2026 - 20359.6.5.1 Latin America Smart Building Market, by End Use, 2026 - 2035 (USD Billion)9.7 The Middle-East and Africa9.7.1 The Middle-East and Africa Smart Building Market, 2026 - 2035 (USD Billion)9.7.1.1 The Middle-East and Africa Smart Building Market, by Country, 2026 - 2035 (USD Billion)9.7.2 The Middle-East and Africa Smart Building Market, by Component, 2026 - 20359.7.2.1 The Middle-East and Africa Smart Building Market, by Component, 2026 - 2035 (USD Billion)9.7.3 The Middle-East and Africa Smart Building Market, by Solution, 2026 - 20359.7.3.1 The Middle-East and Africa Smart Building Market, by Solution, 2026 - 2035 (USD Billion)9.7.4 The Middle-East and Africa Smart Building Market, by Service, 2026 - 20359.7.4.1 The Middle-East and Africa Smart Building Market, by Service, 2026 - 2035 (USD Billion)9.7.5 The Middle-East and Africa Smart Building Market, by End Use, 2026 - 20359.7.5.1 The Middle-East and Africa Smart Building Market, by End Use, 2026 - 2035 (USD Billion)Chapter 10. Company Profiles

10.1 ABB Ltd.10.1.1 Overview10.1.2 Financials10.1.3 Product Portfolio10.1.4 Business Strategy10.1.5 Recent Developments10.2 Johnson Controls10.2.1 Overview10.2.2 Financials10.2.3 Product Portfolio10.2.4 Business Strategy10.2.5 Recent Developments10.3 Cisco Systems Inc.10.3.1 Overview10.3.2 Financials10.3.3 Product Portfolio10.3.4 Business Strategy10.3.5 Recent Developments10.4 Emerson Electric Co.10.4.1 Overview10.4.2 Financials10.4.3 Product Portfolio10.4.4 Business Strategy10.4.5 Recent Developments10.5 Siemens AG10.5.1 Overview10.5.2 Financials10.5.3 Product Portfolio10.5.4 Business Strategy10.5.5 Recent Developments10.6 Honeywell International Inc.10.6.1 Overview10.6.2 Financials10.6.3 Product Portfolio10.6.4 Business Strategy10.6.5 Recent Developments10.7 Schneider Electric Corporation10.7.1 Overview10.7.2 Financials10.7.3 Product Portfolio10.7.4 Business Strategy10.7.5 Recent Developments

- North America

Frequently Asked Questions

Smart buildings are structures that integrate advanced technologies such as IoT, AI, and automation to connect systems like HVAC, lighting, security, and facility management into a centralized platform, enabling real-time monitoring, data-driven optimization, energy efficiency, and enhanced occupant comfort.

Key factors include the adoption of IoT-enabled systems, technological advancements in AI and data analytics, urbanization, government sustainability initiatives, integration of renewable energy, and the rise of hybrid work models, though the report forecasts up to 2033 with similar drivers expected to persist.

The market is projected to grow from USD 139.30 billion in 2025 to USD 510.13 billion by 2035, with extrapolated growth beyond based on the 18.9% CAGR, potentially reaching higher values by 2035 assuming sustained trends.

The CAGR is estimated at 13.86% from 2026 to 2035, with similar growth rates likely continuing to 2035 driven by ongoing technological and sustainability advancements.

North America will contribute notably, holding over 35% revenue share in 2025 and maintaining dominance through investments in digital infrastructure and IoT adoption.

Major players include ABB Ltd., Johnson Controls, Cisco Systems Inc., Emerson Electric Co., Siemens AG, Honeywell International Inc., and Schneider Electric Corporation, driving growth through innovations in automation, partnerships, and sustainable solutions.

The report provides comprehensive insights into market size, CAGR, segmentation, dynamics, regional analysis, key players, trends, recent developments, and segments covered, offering data-driven forecasts and strategic recommendations for stakeholders.

The value chain includes research and development of technologies, manufacturing of components like sensors and software, system integration and implementation, service provision such as maintenance and consulting, and end-user deployment in buildings, with distribution through vendors and partnerships.

Market trends are shifting toward AI-driven predictive platforms, renewable integration, and cybersecurity, while consumer preferences favor energy-efficient, convenient solutions like home automation and remote management for sustainability and comfort.

Regulatory factors include government mandates for green building certifications and decarbonization policies, while environmental factors encompass net-zero commitments, energy conservation initiatives, and climate change mitigation efforts promoting low-carbon technologies and efficient systems.