Home Elevator Market Size, Share and Trends 2026 to 2035

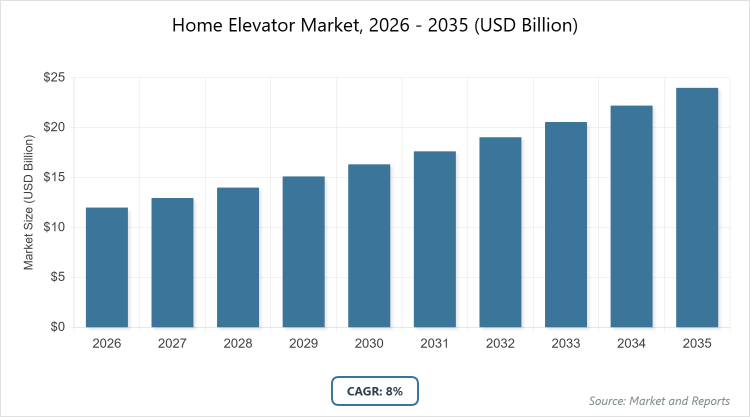

According to MarketnReports, the global home elevator market size was estimated at USD 12 billion in 2025 and is expected to reach USD 25.7 billion by 2035, growing at a CAGR of 8% from 2026 to 2035. Home Elevator Market is driven by the increasing demand for accessibility solutions among aging populations wishing to age in place, alongside rising disposable incomes and a growing preference for luxury and convenience in multi-story residences.3

What are the Key Insights into the Home Elevator Market?

- Global home elevator market valued at approximately USD 12 billion in 2025, projected to reach USD 25.7 billion by 2035.

- Expected CAGR of around 8% from 2026 to 2035, driven by aging demographics and urbanization.

- Dominant subsegment by type: Hydraulic elevators, accounting for the largest share due to reliability in low-rise homes.

- Dominant subsegment by application: Passenger elevators, holding over 70% market share for primary human transport.

- Dominant subsegment by end-user: Residential new installations, leading due to booming construction.

- Dominant region: Asia-Pacific, contributing over 40% of global revenue with China as the leading country.

What is the Home Elevator Industry Overview?

Industry Overview

Home elevators, also known as residential elevators, are vertical transportation systems designed specifically for private residences to facilitate easy movement between floors, enhancing accessibility, convenience, and property value. These devices operate on principles similar to commercial elevators but are scaled down for home use, incorporating mechanisms like hydraulic pistons, traction cables, or pneumatic vacuum systems to lift a cab within a shaft or shaftless structure. They cater primarily to multi-story homes, villas, and apartments, addressing needs arising from aging populations, mobility impairments, or lifestyle preferences for seamless indoor navigation.

Unlike traditional staircases or stairlifts, home elevators provide a fully enclosed, automated solution that integrates aesthetics with functionality, often customizable in design, size, and finishes to blend with home interiors. This market encompasses manufacturing, installation, maintenance, and modernization services, driven by evolving architectural trends toward universal design and smart homes, where elevators serve not just as utilities but as integral elements of modern living spaces that promote independence and safety for all occupants.

What are the Market Dynamics in the Home Elevator Sector?

Growth Drivers

The home elevator market is propelled by the global aging population and rising prevalence of mobility issues, as more seniors opt to age in place rather than relocate to assisted living facilities, necessitating reliable vertical mobility solutions in multi-level homes. Urbanization and the construction of high-end residential properties, including luxury villas and townhouses, further fuel demand, with homeowners seeking to enhance property aesthetics and functionality through integrated elevator systems.

Technological advancements, such as energy-efficient designs and smart controls compatible with home automation, attract tech-savvy consumers, while government incentives for accessibility modifications in homes support market expansion. Increasing awareness of universal design principles, which emphasize inclusivity for people with disabilities, combined with rising disposable incomes in emerging economies, creates a conducive environment for widespread adoption of home elevators as essential home features.

Restraints

High initial installation costs, including structural modifications to existing homes, pose a significant barrier to entry for many potential buyers, particularly in middle-income households where elevators are viewed as luxury rather than necessity. Regulatory hurdles and building codes varying by region can complicate approvals and increase compliance expenses, deterring homeowners from proceeding with installations.

Limited space in older or smaller residences often requires custom solutions, escalating prices and timelines, while economic uncertainties, such as inflation or recessions, can delay non-essential home improvements. Competition from cheaper alternatives like stairlifts or ramps further restrains market penetration, as these options suffice for basic mobility needs without the extensive renovations associated with elevators.

Opportunities

Emerging markets in developing regions present substantial growth potential, as rapid urbanization and improving living standards lead to increased construction of multi-story residences equipped with modern amenities like home elevators. Innovations in compact, shaftless, and eco-friendly designs open avenues for retrofitting in space-constrained homes, appealing to a broader customer base including urban apartments.

Partnerships with real estate developers to include elevators in new builds as standard features can boost market share, while the integration of IoT and AI for predictive maintenance and voice-activated controls aligns with the smart home trend, creating opportunities for premium product differentiation. Government policies promoting accessibility and aging-in-place initiatives, coupled with financing options to reduce upfront costs, could unlock demand among underserved demographics.

Challenges

Navigating diverse international standards and safety regulations remains a key challenge, as manufacturers must adapt products to meet varying certification requirements, increasing R&D and production costs. Supply chain disruptions for critical components like motors and control systems can lead to delays and price volatility, impacting project timelines. Intense competition from both established players and new entrants pressures margins, while educating consumers on the long-term benefits of home elevators over alternatives requires robust marketing efforts. Environmental concerns, such as energy consumption and material sustainability, challenge the industry to innovate greener solutions without compromising performance or affordability.

Home Elevator Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Home Elevator Market |

| Market Size 2025 | USD 12 Billion |

| Market Forecast 2035 | USD 25.7 Billion |

| Growth Rate | CAGR of 8% |

| Report Pages | 220 |

| Key Companies Covered | TK Elevator GmbH, Schindler Group, KONE Corporation, Savaria Corporation, Mitsubishi Electric Corporation, Hitachi Ltd and Other |

| Segments Covered | By Type, Application, End User, and Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Home Elevator Market Segmented?

The home elevator market is segmented by type, application, end-user, and region

By Type, The hydraulic segment dominates the home elevator market, primarily because of its proven reliability, lower initial costs compared to traction systems, and suitability for low-rise residential buildings where space for machine rooms is available, enabling smooth operation without the need for extensive overhead structures. This dominance drives the market by catering to the majority of homeowners seeking cost-effective, durable solutions that enhance accessibility in two- to three-story homes, thereby broadening adoption among middle-class families and boosting overall sales volumes through high-volume manufacturing efficiencies. The traction segment ranks second, gaining traction due to its energy efficiency, quieter operation, and eco-friendly attributes that appeal to environmentally conscious consumers in urban settings, helping to propel market growth by integrating with smart home technologies and reducing long-term operational costs, thus attracting premium buyers and supporting sustainability trends.

By Application, Passenger elevators lead the application segment, as they are specifically designed for human transport, offering safety features like emergency brakes and spacious cabs that align with the core purpose of home elevators in facilitating daily mobility for families, elderly, or disabled individuals. This subsegment drives the market by addressing the rising demand for aging-in-place solutions, increasing home values, and complying with accessibility standards, which in turn stimulates investments in residential construction and retrofits. Freight elevators follow as the second dominant, utilized for moving heavy items like groceries or furniture between floors, providing added utility in larger homes; it contributes to market expansion by diversifying product offerings and appealing to homeowners with storage or workshop needs, enhancing overall home functionality and encouraging bundled installations with passenger systems.

By End-User, New installations dominate the end-user segment, fueled by the surge in multi-story home constructions worldwide, particularly in emerging markets, where elevators are incorporated during building phases to meet modern living standards and regulatory requirements for accessibility. This leadership accelerates market growth by syncing with global urbanization trends, enabling economies of scale in production, and fostering partnerships with builders to standardize elevator inclusion, thereby expanding market reach. Retrofit or modernization ranks second, driven by the need to upgrade existing homes for aging residents or to increase resale value, helping to drive the market through aftermarket services that extend product lifecycles, incorporate advanced tech like IoT, and tap into the vast stock of older residences, thus sustaining revenue streams beyond initial sales.

What are the Recent Developments in the Home Elevator Market?

- In 2023, Savaria Corporation expanded its product line with the introduction of energy-efficient shaftless elevators, targeting the growing demand for compact, easy-to-install solutions in urban homes, which enhanced their market position through improved accessibility features and reduced installation times. TK Elevator launched advanced machine-room-less (MRL) models

- in 2024, incorporating IoT for predictive maintenance, addressing sustainability concerns and appealing to eco-conscious consumers, thereby boosting adoption in retrofit projects across North America and Europe.

- In 2025, Otis Elevator Company partnered with real estate developers in Asia to integrate smart elevators in new residential builds, featuring voice-activated controls and integration with home automation systems, which accelerated market penetration in high-growth regions like China and India. Schindler Group announced the acquisition of a smaller home elevator specialist in early 2026, aiming to strengthen its portfolio with customizable designs for luxury segments, fostering innovation in aesthetic and functional enhancements to meet diverse consumer preferences.

What is the Regional Analysis of the Home Elevator Market?

- Asia-Pacific to dominate the market

Asia-Pacific dominates the global home elevator market, driven by rapid urbanization, a burgeoning middle class, and extensive residential construction in countries like China, which leads the region due to its massive population, government-backed infrastructure projects, and increasing adoption of Western-style multi-story homes. The region’s growth is fueled by rising disposable incomes enabling luxury home features, coupled with policies promoting elderly care, resulting in high demand for affordable hydraulic and traction systems; China, as the dominating country, contributes significantly through its manufacturing hubs that export components globally, while India and Japan follow with strong retrofit markets, enhancing overall regional revenue through economies of scale and technological localization.

North America holds a substantial share in the home elevator market, characterized by an aging population and emphasis on aging-in-place initiatives, with the United States as the dominating country owing to its large housing stock, high per capita income, and supportive regulations like the Americans with Disabilities Act that encourage installations. The region benefits from advanced retrofit services and integration with smart home ecosystems, driving demand for premium shaftless and pneumatic elevators; Canada complements this with growing urban developments, but the U.S. leads through innovative companies offering customizable solutions, boosting market expansion via consumer awareness campaigns and financing options that make elevators accessible to a wider demographic.

Europe exhibits steady growth in the home elevator market, focused on sustainability and architectural integration, with Germany as the dominating country due to its engineering prowess, strict building codes favoring energy-efficient designs, and a mature market for modernization in historic homes. The region is propelled by EU directives on accessibility and environmental standards, promoting traction and MRL elevators; France and Italy contribute through luxury segments in villas, but Germany’s leadership stems from its export-oriented manufacturers and R&D in green technologies, fostering market development by addressing demographic shifts toward older populations and enhancing property values across the continent.

The Rest of the World, including Latin America, Middle East, and Africa, shows emerging potential in the home elevator market, with Brazil dominating in Latin America through urban expansion and luxury real estate, while the UAE leads in the Middle East with high-end residential towers incorporating elevators as standard features. Growth is driven by increasing foreign investments and tourism-related developments, though adoption lags due to economic disparities; Saudi Arabia and South Africa follow with infrastructure pushes, but the region’s overall progress relies on affordable import solutions and local partnerships to overcome installation challenges, gradually increasing market share through targeted segments like affluent households.

Who are the Key Market Players and Their Strategies in the Home Elevator Industry?

Otis Elevator Company: Focuses on innovation through smart technology integration, such as IoT-enabled predictive maintenance and customizable designs for residential applications, aiming to expand market share via partnerships with developers and emphasis on energy efficiency to appeal to eco-conscious consumers.

TK Elevator GmbH: Employs strategies centered on sustainability and compactness, developing machine-room-less and shaftless models while pursuing acquisitions to broaden product portfolios and strengthen presence in emerging markets through localized manufacturing.

Schindler Group: Prioritizes digital transformation with AI-driven controls and voice activation, combined with strategic mergers to enhance customization options, targeting retrofit segments to capitalize on aging housing stocks globally.

KONE Corporation: Leverages R&D in eco-friendly traction systems and modular installations, focusing on customer-centric services like extended warranties and financing to drive adoption in urban residential projects.

Savaria Corporation: Concentrates on accessibility solutions for the elderly, expanding through product diversification into affordable hydraulic and pneumatic elevators, with a strategy of geographic expansion via dealership networks.

Mitsubishi Electric Corporation: Emphasizes high-reliability engineering and integration with home automation, pursuing joint ventures in Asia to dominate regional markets while investing in green materials for sustainable growth.

Hitachi Ltd.: Adopts a technology-forward approach with compact designs for space-limited homes, focusing on export strategies and collaborations to penetrate North American and European markets effectively.

What are the Current Market Trends in the Home Elevator Sector?

- Increasing integration of smart features like app controls, voice activation, and IoT for remote monitoring, enhancing user convenience and safety.

- Shift toward energy-efficient and eco-friendly designs using sustainable materials and low-power consumption systems to align with global green building standards.

- Growing popularity of shaftless and pneumatic vacuum elevators for easy retrofitting in existing homes without major structural changes.

- Emphasis on aesthetic customization, with elevators featuring glass panels, wood finishes, and LED lighting to blend seamlessly with home decor.

- Rise in demand driven by aging-in-place trends, with features like wheelchair accessibility and emergency communication systems becoming standard.

- Expansion in luxury segments, incorporating high-end tech like biometric access and integration with smart home ecosystems.

What Market Segments are Covered in the Report?

By Type

-

- Hydraulic

- Traction

- Pneumatic/Vacuum

- Shaftless

- Others

By Application

-

- Passenger

- Freight

By End-User

-

- New Installation

- Retrofit/Modernization

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Home elevator Market - Industry Analysis

Chapter 4. Global Home elevator Market- Competitive Landscape

Chapter 5. Global Home elevator Market - Type Analysis

Chapter 6. Global Home elevator Market - Application Analysis

Chapter 7. Global Home elevator Market - End-User Analysis

Chapter 8. Home elevator Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Home elevators are compact vertical transportation systems installed in residential properties to enable easy movement between floors, designed for safety, convenience, and integration with home aesthetics, typically using hydraulic, traction, or pneumatic mechanisms.

Key factors include the aging global population driving demand for accessibility solutions, rapid urbanization leading to more multi-story homes, technological advancements in smart and energy-efficient designs, and supportive government policies on elderly care and building inclusivity.

The home elevator market is projected to grow from approximately USD 12 billion in 2026 to USD 25.7 billion by 2035, reflecting steady expansion across segments and regions.

The CAGR for the home elevator market during 2026-2035 is expected to be around 8%, supported by demographic shifts and innovation.

Asia-Pacific will contribute notably, accounting for over 40% of the market value, led by high construction activity in China and India.

Major players include Otis Elevator Company, TK Elevator GmbH, Schindler Group, KONE Corporation, Savaria Corporation, Mitsubishi Electric Corporation, and Hitachi Ltd., through innovation and strategic expansions.

The global home elevator market report provides comprehensive insights into market size, segmentation, dynamics, regional analysis, key players, trends, and forecasts, aiding stakeholders in decision-making.

The value chain includes raw material procurement (metals, electronics), manufacturing and assembly, distribution and installation by dealers, after-sales maintenance services, and end-user modernization or upgrades.

Market trends are shifting toward smart, sustainable, and customizable elevators, with consumers preferring energy-efficient models integrated with home automation, prioritizing accessibility and aesthetics over basic functionality.

Regulatory factors include building codes for safety and accessibility, while environmental factors involve mandates for energy efficiency and sustainable materials, influencing product design and increasing compliance costs but promoting green innovations.