LiDAR Market Size and Forecast 2026 to 2035

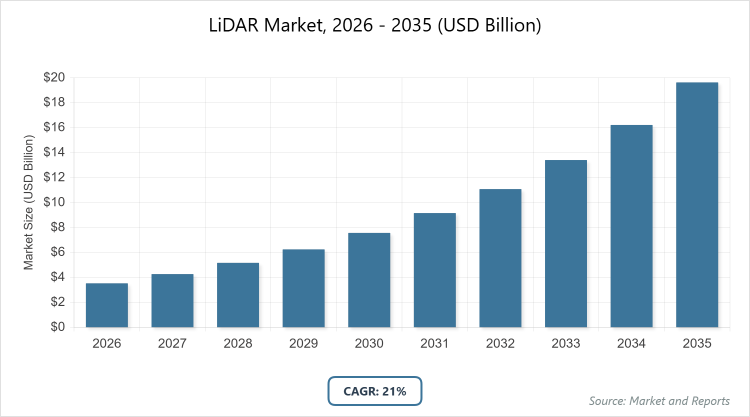

According to MarketnReports, the global LiDAR market size was estimated at USD 3.53 billion in 2025 and is expected to reach USD 20.5 billion by 2035, growing at a CAGR of 21% from 2026 to 2035. LiDAR Market is driven by the accelerating adoption of autonomous vehicle technologies and Advanced Driver Assistance Systems (ADAS).

What are the Key Insights into the LiDAR Market?

- Global LiDAR market value projected at approximately USD 3.53 billion in 2025.

- Market expected to reach around USD 20.5 billion by 2035.

- CAGR anticipated at about 21% from 2026 to 2035.

- Dominant subsegment in installation/type: Airborne, due to its efficiency in large-scale mapping and environmental applications.

- Dominant subsegment in component: Laser scanners, for their high-resolution data capture in surveying and automotive uses.

- Dominant subsegment in range: Short-range, adopted widely in robotics, security, and ADAS.

- Dominant subsegment in service: Aerial surveying, utilized for infrastructure monitoring and government projects.

- Dominant subsegment in application: Corridor mapping, essential for linear infrastructure like roads and railways.

- Dominant subsegment in end-use: ADAS & driverless cars, driven by automotive safety integrations.

- Dominant region: North America, holding the largest market share due to R&D and autonomous vehicle advancements.

- Fastest-growing region: Asia Pacific, fueled by infrastructure development and mining activities.

What is the LiDAR Industry Overview?

Industry Definition and Description

The LiDAR market revolves around Light Detection and Ranging technology, a remote sensing method that employs laser pulses to measure distances and generate precise three-dimensional representations of environments, objects, or surfaces. This technology operates on the principle of emitting light waves and calculating the time taken for them to reflect back, enabling the creation of detailed point clouds that capture geometric shapes and characteristics invisible to traditional mapping techniques.

It integrates with various platforms, such as airborne systems, ground-based units, or unmanned aerial vehicles, to support applications ranging from environmental monitoring and urban planning to autonomous navigation and infrastructure management. The market encompasses the development, manufacturing, and deployment of LiDAR sensors, systems, software, and related services, fostering innovation in sectors that demand high-accuracy spatial data for decision-making and operational efficiency.

What are the Market Dynamics in the LiDAR Market?

Growth Drivers

The LiDAR market is propelled by the surging adoption of autonomous vehicles and advanced driver assistance systems, where the technology provides real-time 3D mapping and object detection to enhance safety and navigation capabilities. Additionally, the increasing demand for precise geospatial data in smart city initiatives, infrastructure development, and environmental monitoring drives growth, as LiDAR enables accurate terrain modeling, deforestation tracking, and urban planning. Technological advancements, such as the development of compact solid-state sensors and integration with drones for cost-effective aerial surveys, further accelerate market expansion by making the technology more accessible across industries like agriculture, mining, and defense. Government regulations promoting road safety and investments in digital twins and 4D LiDAR for immersive applications also contribute significantly to this upward trajectory.

Restraints

High initial costs associated with LiDAR systems, including production, engineering, calibration, and post-processing software, pose a significant barrier to widespread adoption, particularly in cost-sensitive sectors like agriculture and small-scale urban planning. The availability of cheaper alternatives, such as photogrammetry or radar-based solutions, combined with safety concerns related to unmanned aerial vehicles and autonomous systems, further restrains market penetration. Additionally, limitations in data accuracy under adverse weather conditions and privacy restrictions on geospatial information in certain regions hinder the technology’s scalability and integration into diverse applications.

Opportunities

Emerging opportunities in the LiDAR market stem from the rising integration of the technology into industrial automation, robotics, and quantum dot detectors, enabling enhanced precision in manufacturing, warehouse management, and real-time environmental adaptation. The growing popularity of compact flash LiDAR and partnerships with automotive giants for advanced geospatial solutions open avenues for expansion in electric vehicles and smart mobility projects. Furthermore, increasing reliance on drones for analytic data in hard-to-reach areas, coupled with investments in sustainable land use and climate monitoring, presents lucrative prospects for innovation and market diversification.

Challenges

The LiDAR market faces challenges from the high cost of post-processing software and the need for continuous improvements in sensor accuracy, range, and data resolution to handle large-scale projects effectively. Uncertain accuracy and privacy restrictions on geospatial data in many countries, along with competition from low-cost lightweight alternatives, complicate adoption. Balancing technological advancements with affordability while addressing regulatory dependencies and environmental factors remains a key hurdle for sustained growth.

LiDAR Market: Report Scope

| Report Attributes | Report Details |

| Report Name | LiDAR Market |

| Market Size 2025 | USD 3.53 Billion |

| Market Forecast 2035 | USD 20.5 Billion |

| Growth Rate | CAGR of 21% |

| Report Pages | 225 |

| Key Companies Covered |

Hesai Group, Ouster Inc., Leica Geosystems AG, Trimble Inc., Velodyne Lidar, Inc., RIEGL Laser Measurement Systems GmbH, SICK AG, Innoviz Technologies Ltd., FARO Technologies Inc., and Teledyne Optech |

| Segments Covered | By Installation/Type, By Component, By Range, By Service, By Application, By End-Use, and By Region. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Global LiDAR Market Segmented?

The LiDAR market is segmented by installation/type, component, range, service, application, end-use, and region.

By Installation/Type The airborne segment emerges as the most dominant in the LiDAR market, primarily due to its capability for large-scale topographic and bathymetric mapping, enabling precise data collection over vast areas for applications like environmental monitoring, flood risk assessment, and government infrastructure projects; its superiority in providing high-resolution elevation models and wide coverage drives market growth by supporting sustainable land use and disaster management initiatives. The ground-based segment ranks as the second most dominant, offering cost-effective solutions with simpler regulatory approvals for detailed surveying in meteorology, corridor mapping, and autonomous vehicles; its accessibility and integration in urban planning and engineering applications help propel the overall market by facilitating accurate, on-ground data acquisition that complements airborne efforts in creating comprehensive 3D models.

By Component Laser scanners dominate the component segment, as they provide essential high-resolution 3D data capture for mapping, construction, and forestry, with ongoing advancements in accuracy and range making them indispensable for real-time object detection in autonomous systems; this dominance drives the market by enabling efficient data processing and integration across diverse industries, enhancing overall system performance. Navigation systems, particularly inertial measurement units, are the second most dominant, growing rapidly due to their role in real-time positioning and georeferencing in vehicles and UAVs; they contribute to market expansion by improving accuracy in dynamic environments, supporting applications in ADAS and industrial automation.

By Range Short-range LiDAR leads as the most dominant segment, widely adopted in automobiles, security, and robotics for its effectiveness in close-proximity detection and cost efficiency; it drives market growth by facilitating safe navigation in compact environments, such as urban traffic and indoor automation, thereby accelerating adoption in consumer and industrial applications. Medium-range LiDAR is the second most dominant, experiencing high growth in engineering and construction due to its balance of coverage and precision; it aids market development by enabling detailed mapping for infrastructure projects, bridging the gap between short and long-range needs in expanding sectors like smart cities.

By Service Aerial surveying stands out as the most dominant service segment, employed for monitoring critical infrastructure like roads and bridges with high accuracy via drones or aircraft; its broad adoption by government entities drives the market by providing scalable solutions for large-area inspections, enhancing efficiency in planning and maintenance. Ground-based surveying is the second most dominant, utilized in high-volume traffic studies and environmental assessments; it supports market growth by offering detailed, localized data that complements aerial methods, fostering integrated geospatial solutions.

By Application Corridor mapping is the most dominant application segment, crucial for infrastructure planning and maintenance of linear assets such as highways, railways, and pipelines; its prominence drives the market by delivering cost-effective, high-precision data for development projects, reducing operational risks and supporting global urbanization efforts. ADAS and driverless cars rank as the second most dominant, with rapid integration of solid-state LiDAR for object detection and safety; this segment propels market expansion by aligning with automotive innovations, enabling Level 3-4 autonomy and meeting regulatory demands for safer transportation.

By End-Use Civil engineering dominates the end-use segment, relying on LiDAR for topographic mapping and site planning in construction and infrastructure; its leadership drives the market by providing essential data for progress monitoring and resource optimization, fueling growth in urban development worldwide. Forestry and agriculture are the second most dominant, using LiDAR for crop health analysis, forest inventory, and precision farming; this segment contributes to market advancement by promoting sustainable practices and efficiency gains in resource management.

What are the Recent Developments in the LiDAR Market?

- In March 2025, Ouster introduced 3D Zone Monitoring for its REV7 digital LiDAR sensor lineup, including OS0, OS1, and OSDome models, which enhances collision avoidance in warehouse automation and robotics through advanced firmware updates, improving operational safety and efficiency in industrial settings.

- In February 2025, Leica Geosystems launched the Leica CoastalMapper, an airborne bathymetric LiDAR system with a wider field of view, boosting efficiency in coastal and river surveys by up to 250%, thereby supporting more accurate environmental and infrastructure mapping projects.

- In September 2024, Teledyne Geospatial unveiled the Galaxy Edge airborne LiDAR system and Network Surveyor at INTERGEO 2024, designed for real-time mapping applications, which advances capabilities in geospatial data collection for urban and environmental planning.

- In August 2024, YellowScan partnered with Nokia to integrate the Surveyor Ultra LiDAR into drone networks for 5G-based industrial scanning, targeting telecom and utilities sectors to enable high-precision, remote inspections and data gathering.

- In June 2024, Innoviz Technologies Ltd. collaborated with an automotive OEM to incorporate its short-range InnovizTwo LiDAR into Level 4 autonomous vehicles for light commercial models, enhancing safety features and accelerating adoption in the mobility sector.

What is the Regional Analysis of the LiDAR Market?

North America to dominate the market

North America holds the largest share in the LiDAR market, driven by robust investments in autonomous vehicle development, smart cities, defense applications, and environmental monitoring, with the United States dominating due to its strong R&D ecosystem, government funding for road safety regulations, and widespread adoption in aerial mapping and agriculture; this region’s leadership fosters innovation through collaborations between tech giants and startups, enabling precise geospatial solutions that support infrastructure upgrades and disaster management, while Canada contributes with spatial data initiatives and Mexico with archeological surveying.

Europe exhibits significant growth in the LiDAR market, fueled by advancements in automotive R&D, smart mobility projects, and environmental sustainability efforts aimed at reducing emissions and improving infrastructure monitoring, with Germany leading as the dominant country through its focus on autonomous driving and ADAS integrations in the automotive sector; the region benefits from innovative corridor mapping in France, terrain analysis for flood risks in the UK, and modernization initiatives in Poland and Nordic countries, collectively driving adoption in urban planning, coastline management, and industrial automation.

Asia Pacific is the fastest-growing region in the LiDAR market, propelled by rapid infrastructural development, smart city expansions, forest management, and mining activities, with China dominating through its advancements in drone technology and large-scale surveying operations; the region sees contributions from Japan in autonomous vehicles, South Korea in factory optimization, India in highway mandates and infrastructure projects, and Australia in climate monitoring, collectively enhancing market penetration via government investments in urban expansion and disaster management across Southeast Asian nations like Indonesia, Malaysia, Thailand, and Vietnam.

The Rest of the World region, encompassing South America, the Middle East, and Africa, shows promising growth in the LiDAR market through topographic mapping, environmental monitoring, and smart infrastructure projects, with Brazil leading in South America via mining operations and urbanization efforts; the Middle East, dominated by the UAE and Saudi Arabia, focuses on sustainability and smart nation initiatives, while South Africa drives adoption in Africa for resource assessment and biodiversity studies, overall supporting regional development in disaster-prone and resource-rich areas.

Who are the Key Market Players in the LiDAR Market and Their Strategies?

- Hesai Group focuses on product innovation through partnerships, such as integrating ATX LiDAR into vehicle headlamps with Marelli to reduce costs and volume, while expanding its portfolio for automotive and industrial applications to increase market share.

- Ouster, Inc. emphasizes new product launches like the REV7 digital LiDAR sensors with 3D Zone Monitoring firmware, targeting warehouse automation and robotics to enhance collision avoidance and global presence.

- Leica Geosystems AG pursues technological advancements and collaborations, including the launch of CoastalMapper for efficient surveys and partnerships with LocLab for digital realities in transportation and urban planning.

- Trimble Inc. adopts strategies of product introductions and acquisitions, such as the Trimble R580 GNSS receiver for positioning and partnerships for terrain mapping in engineering and highway projects.

- Velodyne Lidar, Inc. concentrates on series expansions like Puck and Velarray for high-resolution scanning, collaborating with startups and OEMs to advance solid-state sensors for autonomous vehicles.

- RIEGL Laser Measurement Systems GmbH invests in R&D for models like VUX-18024 and VZ-600i, focusing on high-precision applications in aerial and terrestrial surveying to strengthen its position in geospatial markets.

- SICK AG drives growth through launches like multiScan136 and MRS1000 series, emphasizing time-of-flight technology for 3D perception in robotics and outdoor environments.

- Innoviz Technologies Ltd. forms strategic collaborations with automotive OEMs for InnovizTwo integration in Level 4 vehicles, aiming to expand in commercial mobility solutions.

- FARO Technologies, Inc. specializes in portable 3D scanners and software, using mergers and acquisitions to broaden its customer base in manufacturing and forensics.

- Teledyne Optech focuses on bathymetric solutions like CZMIL SuperNova and Galaxy Edge, partnering for real-time mapping in climate and infrastructure applications.

- YellowScan engages in partnerships, such as with Nokia for 5G-integrated drone scanning, to target utilities and telecom for industrial applications.

What are the Current Market Trends in the LiDAR Market?

- Increasing adoption of solid-state LiDAR for its compact design, cost-effectiveness, and resistance to shock, disrupting traditional mechanical systems in autonomous vehicles and ADAS.

- Integration of LiDAR with AI and machine learning for enhanced data processing, enabling real-time object detection and environmental adaptation in robotics and smart cities.

- Growth in UAV and drone-based LiDAR for versatile, real-time data collection in agriculture, mining, and hard-to-access areas, reducing operational costs.

- Shift toward 4D LiDAR technology incorporating time dimensions for dynamic mapping in autonomous navigation and infrastructure monitoring.

- Emphasis on environmental applications, including climate change monitoring, deforestation tracking, and sustainable land use through high-precision geospatial solutions.

- Advancements in frequency-modulated continuous-wave and photon-counting LiDAR for improved range and accuracy in defense and surveillance.

- Rising partnerships between LiDAR providers and automotive OEMs for headlamp-integrated sensors, making technology more affordable for electric vehicles.

- Focus on compact flash LiDAR and quantum dot detectors to expand applications in industrial automation and compact devices.

- Incorporation of LiDAR in smart manufacturing and Industry 4.0 for obstacle avoidance and material handling in warehouses.

- Evolving consumer preferences toward eco-friendly, data-driven solutions in precision agriculture and urban planning.

What Market Segments are Covered in the LiDAR Market Report?

By Installation/Type

- Airborne

- Ground-based

- Terrestrial

- Mobile

- UAV

By Component

- Laser Scanners

- Navigation (IMU)

- GPS/GNSS

- Inertial Navigation Systems

- Cameras

- Micro Electro Mechanical Systems

By Range

- Short (0-200 m)

- Medium (200-500 m)

- Long (above 500 m)

By Service

- Aerial Surveying

- Asset Management

- GIS Services

- Ground-based Surveying

- Other Services

By Application

- Corridor Mapping

- Engineering

- Environment

- ADAS & Driverless Cars

- Exploration

- Urban Planning

- Cartography

- Meteorology

- Seismology

- Others

By End-Use

- Civil Engineering

- Forestry & Agriculture

- Mining

- Transportation

- Defense & Aerospace

- Archaeology

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

LiDAR, or Light Detection and Ranging, is a remote sensing technology that uses laser pulses to measure distances and create detailed three-dimensional maps of environments, objects, or surfaces by calculating the time for light to reflect back, generating precise point clouds for applications in mapping, autonomous navigation, and monitoring.

Key factors include advancements in autonomous vehicles and ADAS, increasing demand for 3D mapping in smart cities and infrastructure, technological innovations in solid-state sensors reducing costs, government regulations for safety and environmental monitoring, and expanding applications in agriculture, mining, and industrial automation.

The LiDAR market is projected to grow from approximately USD 3.53 billion in 2025 to around USD 20.5 billion by 2035, reflecting steady expansion across various segments and regions.

The CAGR for the LiDAR market is anticipated to be approximately 21% from 2026 to 2035, driven by technological advancements and increasing adoption in key industries.

Asia Pacific will contribute notably to the LiDAR market value, as the fastest-growing region fueled by infrastructural development, smart city projects, and mining activities in countries like China and India.

Major players include Hesai Group, Ouster, Inc., Leica Geosystems AG, Trimble Inc., Velodyne Lidar, Inc., RIEGL Laser Measurement Systems GmbH, SICK AG, Innoviz Technologies Ltd., FARO Technologies, Inc., and Teledyne Optech, who drive growth through innovations, partnerships, and product expansions.

The global LiDAR market report provides comprehensive insights into market size, forecasts, dynamics, segmentation, regional analysis, key players, recent developments, trends, and value chain, offering detailed data for strategic decision-making and industry benchmarking.

The value chain stages include research and development for sensor innovation, raw material supply and component manufacturing (e.g., lasers and IMUs), system integration and assembly, supply and distribution through providers, data processing and software development, and end-use applications in sectors like automotive and geospatial services.

Market trends are evolving toward solid-state and AI-integrated LiDAR for compact, affordable solutions, while consumer preferences shift to eco-friendly, data-driven applications in autonomous vehicles, precision agriculture, and smart cities, emphasizing real-time accuracy and sustainability.

Regulatory factors include government mandates for ADAS and drone usage in safety and infrastructure, such as RoHS and GDPR for data protection, while environmental factors involve climate monitoring regulations promoting LiDAR for deforestation tracking and sustainable development, influencing growth through compliance and funding support.