Autonomous Cars Market Size, Share and Forecast 2026 to 2035

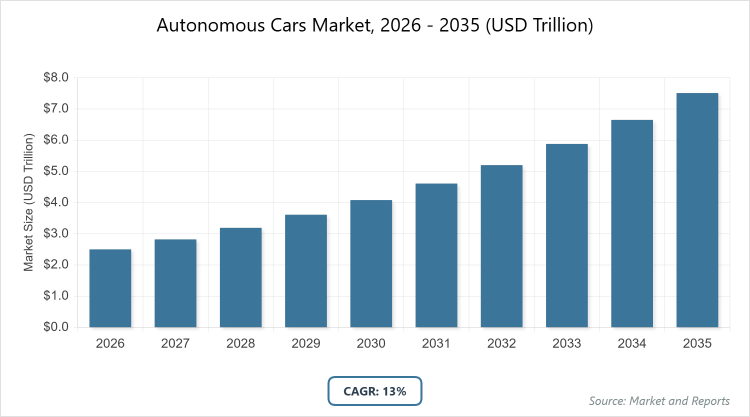

According to our latest research, the global autonomous cars market is projected to grow from approximately USD 2.5 trillion in 2026 to USD 8.2 trillion by 2035, growing at a CAGR of 13% from 2026 to 2035. The Autonomous Cars Market is primarily driven by rapid advancements in AI and sensor technologies aimed at reducing human-error-related accidents while meeting growing consumer and commercial demand for safe, efficient, and hands-free mobility.

What are the Key Insights into the Autonomous Cars Market?

- The global autonomous cars market is valued at approximately USD 2.5 trillion in 2026 and is projected to reach USD 8.2 trillion by 2035.

- The market is expected to grow at a compound annual growth rate (CAGR) of 13% from 2026 to 2035.

- Among levels of autonomy, the Level 2 segment dominates due to its widespread integration in current vehicles.

- In vehicle types, passenger cars is the leading subsegment, driven by consumer demand for advanced features.

- By component, hardware holds the largest share, supported by essential sensors and processors.

- Asia Pacific is the dominated region, fueled by rapid technological adoption and investments.

What is the Autonomous Cars Market?

Industry Overview

The autonomous cars market encompasses the development, production, and deployment of vehicles equipped with advanced driver-assistance systems (ADAS) and self-driving technologies that enable partial or full automation of driving tasks, reducing or eliminating the need for human intervention through the integration of sensors, software algorithms, artificial intelligence, and connectivity features to perceive the environment, make decisions, and control vehicle movements. It includes various levels of autonomy, from basic assistance like adaptive cruise control to fully driverless operations in defined scenarios, catering to passenger transportation, commercial logistics, and shared mobility services while addressing safety, efficiency, and accessibility in urban and highway settings. This market intersects with broader automotive, technology, and regulatory ecosystems, fostering innovations in electric and connected vehicles to mitigate traffic congestion, enhance road safety, and promote sustainable mobility solutions amid evolving consumer expectations for convenience and reduced ownership costs.

What Drives the Autonomous Cars Market?

Growth Drivers

The autonomous cars market is driven by rapid advancements in artificial intelligence, machine learning, and sensor technologies such as LiDAR, radar, and cameras, which enable precise environmental mapping and real-time decision-making, supported by increasing investments from tech giants and automakers to accelerate commercialization and scale production. Growing urbanization and traffic congestion worldwide heighten the demand for efficient mobility solutions, while government incentives for electric and autonomous vehicles, coupled with consumer preferences for safer and more convenient travel, further propel adoption by reducing accident rates and optimizing fuel efficiency through automated driving behaviors.

Restraints

Key restraints in the autonomous cars market include high development and manufacturing costs associated with sophisticated hardware and software components, which limit accessibility for mass-market adoption, alongside technical challenges in handling complex real-world scenarios like adverse weather or unpredictable pedestrian behavior that raise reliability concerns. Cybersecurity vulnerabilities in connected systems and the lack of standardized global infrastructure for vehicle-to-everything (V2X) communication also hinder progress, as they expose vehicles to hacking risks and complicate seamless integration across diverse road networks.

Opportunities

Opportunities in the autonomous cars market arise from the expansion of robotaxi services and autonomous delivery fleets, leveraging partnerships between automakers and ride-hailing companies to tap into shared mobility models that reduce ownership needs and generate new revenue streams through subscription-based access. The integration of autonomous technologies with electric vehicles offers potential for sustainable transport ecosystems, while emerging markets in developing regions present avenues for affordable entry-level autonomy solutions supported by government initiatives for smart city infrastructure.

Challenges

Major challenges in the autonomous cars market involve navigating stringent regulatory frameworks that vary by region, requiring extensive testing and certification to ensure safety compliance, which delays widespread deployment and increases operational complexities for manufacturers. Ethical dilemmas in AI decision-making during emergencies, combined with public skepticism toward fully autonomous systems due to high-profile incidents, demand robust risk management strategies to build trust and address liability issues in mixed-traffic environments.

Autonomous Cars Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Autonomous Cars Market |

| Market Size 2025 | USD 2.5 Trillion |

| Market Forecast 2035 | USD 8.2 Trillion |

| Growth Rate | CAGR of 13% |

| Report Pages | 220 |

| Key Companies Covered | Tesla, Inc., Waymo (Alphabet Inc.), Cruise (General Motors), Baidu Apollo, Mobileye (Intel), Nvidia Corporation, Aurora Innovation, Ford Motor Company, Mercedes-Benz Group, and Volkswagen AG |

| Segments Covered | By Level of Autonomy, By Vehicle Type, By Component, By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Autonomous Cars Market Segmented?

The autonomous cars market is segmented by level of autonomy, vehicle type, component, and region.

By Level of Autonomy, The level of autonomy segmentation in the autonomous cars market is dominated by Level 2, which leads owing to its partial automation features like adaptive cruise control and lane-keeping assistance that are already integrated into many production vehicles, driving market growth by offering affordable enhancements to safety and convenience that appeal to a broad consumer base and encourage incremental adoption toward higher autonomy. Level 3 ranks as the second most dominant, enabling conditional automation where drivers can disengage in specific scenarios, but it trails Level 2 because the latter’s lower complexity and regulatory ease facilitate quicker market penetration, thereby accelerating overall expansion through widespread commercialization.

By Vehicle Type, In vehicle type segmentation, passenger cars emerge as the most dominant in the autonomous cars market, attributed to high consumer interest in personal mobility solutions with advanced driver aids that enhance daily commuting, propelling growth by leveraging economies of scale in manufacturing and software updates to make autonomy more accessible. Commercial vehicles follow as the second most dominant, benefiting from fleet operations in logistics and delivery that prioritize efficiency, though they lag passenger cars due to the latter’s larger volume sales and faster tech integration, contributing to market advancement via consumer-driven innovations.

By Component, Among components, hardware dominates the autonomous cars market, as it includes critical sensors, cameras, and processors that form the foundation for perception and control systems, driving growth by enabling reliable data collection essential for all autonomy levels and attracting investments in durable, high-performance tech. Software is the second most dominant, providing algorithms for decision-making and updates, but it trails hardware because the latter’s physical necessities underpin system functionality, fostering market expansion through hardware-software synergies.

What are the Recent Developments in the Autonomous Cars Market?

- In November 2025, StartUs Insights reported on the future of autonomous vehicles from 2026-2035, highlighting real-world deployments like delivery robots growing to USD 163.45 billion by 2033, with companies like Waymo expanding fleets to over 1,500 vehicles in cities such as Phoenix.

- In October 2025, Forbes predicted flying taxis and self-driving trucks arriving in 2026, noting expansions in autonomous driving globally and AI agents in public transport, with companies like Baidu Apollo advancing in China.

- In April 2025, Autofleet’s 2025 AV report extended into 2026 trends, emphasizing robotaxi growth and driverless futures, with Tesla’s Full Self-Driving updates and partnerships shaping mobility transformations.

- In September 2024, but impacting 2025-2026, AIMultiple’s stats forecasted Level 3 highway pilots operational in Europe and North America by 2025-2027, with 60% of new vehicles autonomous by 2035-2040.

- In November 2025, LTIMindtree’s automotive trends report for 2025-2026 detailed autonomous developments, including efficiency gains and shifts to electric AVs, with key trends in downtime reduction.

- In October 2025, MarketsandMarkets noted the autonomous vehicle market doubling by 2035, with 76 million self-driving cars reshaping transportation through tech convergence.

How Does the Autonomous Cars Market Vary by Region?

- Asia Pacific to dominate the market

Asia Pacific dominates the autonomous cars market with the largest share, propelled by massive investments in AI and infrastructure, along with supportive policies for electric and autonomous integration; China leads as the dominating country, contributing the majority through companies like Baidu and extensive testing zones, driving growth by addressing urban congestion in densely populated areas.

North America holds a significant position in the autonomous cars market, backed by advanced R&D ecosystems and regulatory frameworks like those from NHTSA; the United States dominates, with Silicon Valley hubs and firms like Waymo leading deployments, though challenges in federal consistency persist, fostering expansion through innovation in robotaxis.

Europe exhibits steady growth in the autonomous cars market, driven by stringent safety standards and EU-wide initiatives for connected mobility; Germany and the United Kingdom are dominating countries, with Germany excelling in engineering from Volkswagen and Bosch, and the UK advancing via testing corridors, together enhancing market through emphasis on sustainable AVs.

Latin America is emerging in the autonomous cars market with pilot programs in urban logistics, supported by partnerships for tech transfer; Brazil dominates, leveraging its automotive base for ADAS adoption in commercial fleets, navigating economic hurdles to promote safer transport.

The Middle East & Africa region shows potential in the autonomous cars market through smart city projects and oil-funded innovations; the United Arab Emirates leads, with Dubai’s autonomous transport goals via RTA, propelling growth despite desert challenges by focusing on luxury and tourism AVs.

Who are the Key Market Players in the Autonomous Cars Market and What Are Their Strategies?

- Tesla, Inc.: Tesla focuses on over-the-air software updates for Full Self-Driving, vertical integration of hardware like Dojo chips, and robotaxi network expansions to lead in consumer AV adoption.

- Waymo (Alphabet Inc.): Waymo pursues fleet scaling in ride-hailing, AI enhancements via Google Cloud, and partnerships for mapping to dominate urban autonomous mobility.

- Cruise (General Motors): Cruise employs urban testing expansions, safety-focused software iterations, and investments in sensor tech to advance robotaxi services.

- Baidu Apollo: Baidu leverages open-source platforms, China-specific deployments, and AI integrations for Level 4 operations in public transport.

- Mobileye (Intel): Mobileye focuses on ADAS chipsets, scalable mapping solutions, and OEM partnerships to supply vision-based autonomy systems.

- Nvidia Corporation: Nvidia pursues GPU-driven AI platforms, DRIVE ecosystem expansions, and collaborations with automakers for high-performance computing in AVs.

- Aurora Innovation: Aurora emphasizes trucking autonomy, sensor fusion tech, and acquisitions for software to target commercial long-haul applications.

- Ford Motor Company: Ford integrates Argo AI tech, focuses on Level 4 zones, and hybrid strategies for passenger and delivery vehicles.

- Mercedes-Benz Group: Mercedes advances Drive Pilot for Level 3, luxury integrations, and regulatory compliance to lead in premium AV segments.

- Volkswagen AG: Volkswagen employs ID.Buzz for electric AVs, software from CARIAD, and global testing for mass-market autonomy.

What are the Current Market Trends in the Autonomous Cars Market?

- Expansion of autonomous delivery robots and drones, with last-mile market growing to USD 163.45 billion by 2033.

- Global rollout of self-driving trucks and flying taxis, enhancing logistics efficiency in 2026.

- Integration of agentic AI as in-car copilots for personalized driving experiences.

- Shift to software-defined vehicles with over-the-air updates for continuous improvements.

- Rise in unsupervised Full Self-Driving capabilities, focusing on robotaxi scalability.

- Emphasis on cybersecurity and data privacy in connected AV ecosystems.

- Convergence of AVs with electric vehicles for sustainable mobility solutions.

- Regulatory adaptations enabling Level 3 pilots in highways by 2026-2027.

- Growth in public transit AI agents for optimized routing and safety.

- Focus on ethical AI decision-making amid public trust-building efforts.

What Market Segments are Covered in the Report?

By Level of Autonomy

- Level 1

- Level 2

- Level 3

- Level 4

- Level 5

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

By Component

- Hardware

- Software

- Services

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Autonomous Cars Market - Industry Analysis

Chapter 4. Global Autonomous Cars Market- Competitive Landscape

Chapter 5. Global Autonomous Cars Market - Level of Autonomy Analysis

Chapter 6. Global Autonomous Cars Market - Vehicle Type Analysis

Chapter 7. Global Autonomous Cars Market - Component Analysis

Chapter 15. Autonomous Cars Market - Regional Analysis

Chapter 16. Company Profiles

Frequently Asked Questions

Autonomous cars are vehicles equipped with technologies like sensors, AI, and software that allow them to operate with minimal or no human input, performing tasks such as navigation, acceleration, and braking for safer and more efficient travel.

Key factors include AI and sensor advancements, urbanization demands for efficient transport, government incentives for AVs, and integrations with EVs, while challenges like regulations and cybersecurity may impact the pace.

The autonomous cars market is projected to grow from approximately USD 2.5 trillion in 2026 to USD 8.2 trillion by 2035, driven by technological scaling.

The compound annual growth rate (CAGR) for the autonomous cars market is expected to be 13% from 2026 to 2035.

Asia Pacific will contribute notably, holding the largest share due to investments and adoption, with China as the key driver.

Major players include Tesla, Inc., Waymo (Alphabet Inc.), Cruise (General Motors), Baidu Apollo, Mobileye (Intel), Nvidia Corporation, Aurora Innovation, Ford Motor Company, Mercedes-Benz Group, and Volkswagen AG, driving growth through innovations and deployments.

The global autonomous cars market report offers in-depth insights on size, forecasts, segmentation, drivers, restraints, opportunities, regional trends, key players, developments, and strategies to aid stakeholders.

The value chain includes R&D for tech development, component manufacturing (sensors, software), vehicle assembly, testing and certification, deployment in fleets, and aftermarket services like updates.

Trends are shifting toward AI copilots, software-defined vehicles, and robotaxis, while preferences favor safety, convenience, and sustainability over traditional driving.

Regulatory factors include safety certifications and varying global standards delaying deployments, while environmental factors involve reduced emissions from efficient AVs but concerns over manufacturing impacts.