Artificial Intelligence (AI) Powered Storage Market Size, Share and Trends 2026 to 2035

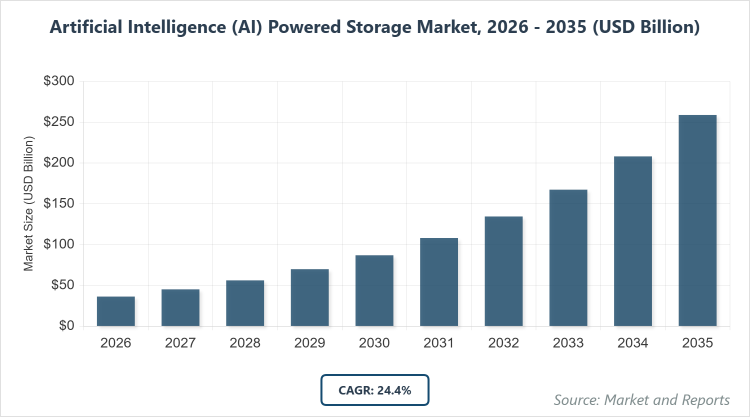

According to MarketnReports, the global Artificial Intelligence (AI) Powered Storage Market size was estimated at USD 36.28 billion in 2025 and is expected to reach USD 321.93 billion by 2035, growing at a CAGR of 24.4% from 2026 to 2035. Artificial Intelligence (AI) Powered Storage Market is driven by the rapid growth of unstructured data and AI/ML workloads requiring high-performance, low-latency storage solutions.What are the Key Insights into Artificial Intelligence (AI) Powered Storage Market?

- The Artificial Intelligence (AI) Powered Storage Market was valued at USD 36.28 billion in 2025 and is projected to reach USD 321.93 billion by 2035.

- The market is anticipated to grow at a CAGR of 24.4% from 2026 to 2035.

- The market is driven by the expansion of hybrid and multi-cloud environments necessitating automated, intelligent data management at scale.

- In the offering segment, software dominates with approximately 55% share due to its role in enabling AI-driven automation, predictive maintenance, and optimization features that enhance storage efficiency.

- In the storage system segment, NAS dominates with around 45% share because it provides scalable, high-throughput file access ideal for unstructured data in AI/ML workloads.

- In the storage architecture segment, file-and-object-based storage dominates with about 60% share owing to its suitability for handling large-scale unstructured data and enabling unified data lakes for AI workflows.

- In the storage medium segment, SSD dominates with roughly 65% share as it offers low-latency and high-IOPS performance critical for AI training and inference.

- In the end user segment, cloud service providers and hyperscalers dominate with approximately 40% share driven by their massive investments in AI compute and petabyte-scale storage infrastructures.

- North America dominates the regional market with around 40% share attributed to its advanced IT infrastructure, presence of major tech giants, and high enterprise adoption of AI technologies.

What is the Industry Overview of Artificial Intelligence (AI) Powered Storage Market?

The Artificial Intelligence (AI) Powered Storage Market refers to the ecosystem of storage solutions enhanced by AI technologies to automate data management, optimize performance, and enable efficient handling of vast data volumes for AI and machine learning applications. This market includes hardware and software components designed for high-throughput, low-latency environments, supporting tasks like predictive analytics, automated tiering, and anomaly detection in storage systems. It caters to the growing need for intelligent storage in data-intensive industries, where traditional systems fall short in scalability and efficiency for modern workloads such as generative AI and edge computing. The market definition encompasses integrated solutions that leverage AI for data placement, security, and lifecycle management, driving innovation in hybrid cloud setups and edge deployments to reduce operational costs and enhance data accessibility.

What are the Market Dynamics of Artificial Intelligence (AI) Powered Storage Market?

Growth Drivers

The primary growth drivers for the Artificial Intelligence (AI) Powered Storage Market include the exponential increase in unstructured data from sources like IoT, social media, and video analytics, which demands AI-enhanced storage for efficient processing and retrieval. Advancements in NVMe, all-flash arrays, and software-defined storage are accelerating adoption by providing scalable architectures that support GPU-intensive AI workloads, reducing bottlenecks and improving throughput. Additionally, the proliferation of hybrid and multi-cloud strategies is pushing organizations to implement intelligent storage solutions for automated data tiering, migration, and governance, ultimately lowering costs and enhancing performance in data centers and edge environments.

Restraints

Key restraints in the Artificial Intelligence (AI) Powered Storage Market revolve around the high initial costs associated with deploying AI-optimized systems, such as all-flash arrays and NVMe fabrics, which can deter small and medium-sized enterprises from adoption. Data privacy regulations and compliance requirements, including GDPR and CCPA, add complexity and potential delays in implementation, as organizations must ensure AI-driven storage maintains secure data handling. Furthermore, the lack of skilled professionals to manage and integrate these advanced systems poses a barrier, limiting widespread deployment in regions with talent shortages.

Opportunities

Opportunities in the Artificial Intelligence (AI) Powered Storage Market are abundant with the rise of edge AI and inference workloads, creating demand for distributed, low-latency storage solutions that can process data closer to the source for real-time applications like autonomous vehicles and smart cities. The growth of 5G networks and IoT ecosystems opens avenues for AI-powered storage to enable seamless data analytics and management across connected devices. Moreover, emerging multimodal AI models and generative AI applications present chances for vendors to innovate in high-performance storage, fostering partnerships with semiconductor and cloud providers to capture new market segments.

Challenges

Challenges facing the Artificial Intelligence (AI) Powered Storage Market include managing the sheer volume of exponential data growth while avoiding performance bottlenecks between storage and compute resources, necessitating ongoing innovations in parallel file systems and caching mechanisms. Ensuring interoperability across diverse hybrid environments remains difficult, as legacy systems often conflict with AI-optimized setups, leading to integration issues. Additionally, cybersecurity threats amplified by AI's predictive capabilities require robust defenses, while supply chain disruptions for components like SSDs can impact deployment timelines and costs.

Artificial Intelligence (AI) Powered Storage Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Artificial Intelligence (AI) Powered Storage Market |

| Market Size 2025 | USD 36.28 Billion |

| Market Forecast 2035 | USD 321.93 Billion |

| Growth Rate | CAGR of 24.4% |

| Report Pages | 220 |

| Key Companies Covered |

Dell Technologies, NetApp, Hewlett Packard Enterprise (HPE), IBM, Huawei Technologies, Pure Storage, VAST Data, Samsung Electronics, Cohesity, Inc., Cloudian, Inc., and Others. |

| Segments Covered | By Offering , By Storage System ,By Storage Architecture , By Storage Medium , By End User and By Region. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 - 2024 |

| Forecast Year | 2026 - 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Artificial Intelligence (AI) Powered Storage Market?

The Artificial Intelligence (AI) Powered Storage Market is segmented by offering, storage system, storage architecture, storage medium, end user, and region.

By Offering Segment, software emerges as the most dominant subsegment, followed by hardware as the second most dominant. Software dominates due to its critical role in embedding AI algorithms for automation, analytics, and optimization, which drives market growth by enabling predictive insights and efficient data management that hardware alone cannot achieve, thus enhancing overall system intelligence and reducing manual interventions.

By Storage System Segment, NAS stands out as the most dominant subsegment, with SAN as the second most dominant. NAS leads because of its scalability and ability to handle unstructured data with high-throughput access, essential for AI/ML workloads; this dominance propels the market by supporting parallel processing in GPU clusters, accelerating model training and inference while SAN contributes through reliable block-level storage for enterprise applications.

By Storage Architecture Segment, file-and-object-based storage is the most dominant subsegment, followed by block storage as the second most dominant. File-and-object-based storage prevails owing to its flexibility in managing vast unstructured datasets and creating unified data lakes, which fuels market expansion by facilitating seamless AI data pipelines and scalability in cloud environments, whereas block storage aids in high-performance transactional operations.

By Storage Medium Segment, SSD is the most dominant subsegment, with HDD as the second most dominant. SSD's dominance stems from its superior speed, low latency, and high IOPS, vital for AI-driven tasks; it drives the market by enabling faster data access for training large models, while HDD supports cost-effective bulk storage for archival needs.

By End User Segment, cloud service providers and hyperscalers are the most dominant subsegment, followed by enterprises as the second most dominant. Cloud service providers dominate due to their scale in handling petabyte-level data for AI services, boosting the market through investments in optimized infrastructures that enhance GPU utilization and reduce latency, with enterprises contributing via sector-specific adoptions in areas like BFSI and healthcare.

What are the Recent Developments in Artificial Intelligence (AI) Powered Storage Market?

- In January 2025, Dell Technologies unveiled its PowerScale and PowerFlex platforms with enhanced NVMe support, automated tiering, and GPU-aware data paths tailored for generative AI workloads, improving throughput and efficiency for enterprise users.

- In November 2024, NetApp expanded its ONTAP AI ecosystem by introducing unified file-object architectures integrated with NVIDIA DGX systems, enabling higher throughput for large language model training and hybrid data management.

- In October 2024, VAST Data launched an update to its Universal Storage platform featuring AI-driven management tools and parallel data pipelines, designed to maximize GPU saturation in AI clusters and support multimodal workloads.

- In August 2024, WEKA upgraded its NeuralMesh platform with metadata acceleration capabilities, targeting generative AI and distributed training environments to deliver low-latency performance and improved scalability.

- In June 2024, Lightbits Labs released new NVMe/TCP storage software aimed at providing elastic, low-latency block storage for AI clusters, enhancing training stability and resource utilization in cloud settings.

What is the Regional Analysis of Artificial Intelligence (AI) Powered Storage Market?

North America to dominate the global market.

North America's dominance in the Artificial Intelligence (AI) Powered Storage Market is underpinned by its robust technological ecosystem, including leading hyperscalers like AWS and Google, and significant R&D investments in AI infrastructure, with the United States as the dominating country due to Silicon Valley's innovation hub and high enterprise adoption rates in sectors like tech and finance.

Asia Pacific exhibits the fastest growth, fueled by expanding hyperscale data centers and government initiatives in AI, where China leads as the dominating country through massive investments in semiconductor manufacturing and cloud computing, alongside rapid industrialization in India and Japan supporting automotive and telecom applications.

Europe maintains steady expansion driven by stringent data regulations and green tech focus, with Germany as the dominating country owing to its strong manufacturing base and adoption in automotive AI, complemented by the UK's advancements in BFSI and France's emphasis on healthcare innovations.

Latin America shows emerging potential through increasing cloud adoption and digital transformation, led by Brazil as the dominating country with its growing tech startups and telecom infrastructure investments enhancing AI storage needs.

The Middle East and Africa are gaining traction via oil-funded AI initiatives and edge computing, with the UAE dominating through Dubai's smart city projects and investments in hyperscale data centers for diversified economies.

What are the Key Market Players and Strategies in Artificial Intelligence (AI) Powered Storage Market?

Dell Technologies focuses on a broad portfolio of all-flash arrays and software-defined storage, leveraging partnerships for NVMe integration and hybrid cloud solutions to accelerate AI infrastructure and reduce operational costs through automated tiering and GPU optimization.

NetApp emphasizes unified file-object architectures within its ONTAP ecosystem, collaborating with hyperscalers and GPU vendors to build hybrid data fabrics that enhance throughput for AI workloads and support seamless multi-cloud data management.

Hewlett Packard Enterprise (HPE) pursues innovation in AI-optimized platforms like GreenLake, integrating edge-to-cloud strategies with AI-driven analytics to provide scalable storage for enterprises, aiming at cost efficiency and sustainability in data centers.

IBM integrates AI storage with its Watson ecosystem, focusing on hybrid cloud deployments and security features to cater to regulated industries like BFSI, using acquisitions and R&D to advance predictive maintenance and data governance.

Huawei Technologies invests in high-performance NVMe and all-flash solutions, targeting telecom and government sectors in emerging markets with cost-effective, scalable architectures to support 5G-enabled AI applications.

Pure Storage specializes in all-flash arrays with AI automation for predictive insights, partnering with NVIDIA for GPU integrations to optimize flash-based storage for high-IOPS AI training and inference workloads.

VAST Data develops universal storage platforms with parallel pipelines, emphasizing AI-driven management to achieve high GPU utilization and unified access for global file systems in hyperscale environments.

Samsung Electronics leverages its semiconductor expertise in SSDs and memory solutions, focusing on high-speed storage mediums to drive low-latency performance for edge AI and consumer electronics applications.

Cohesity, Inc. offers data management platforms with AI-powered backup and recovery, targeting enterprise resilience through secondary storage optimization and ransomware protection strategies.

Cloudian, Inc. provides object storage solutions with AI enhancements for scalability, aiming at hybrid cloud users with S3-compatible systems to facilitate data lakes for AI analytics and archival needs.

What are the Market Trends in Artificial Intelligence (AI) Powered Storage Market?

- Shift towards AI-optimized platforms like unified data fabrics to address GPU bottlenecks and improve model training efficiency.

- Increasing strategic partnerships between storage vendors, semiconductor firms, and AI providers for accelerated innovation in data pipelines.

- Adoption of NVMe-over-Fabrics and parallel file systems to enable low-latency access in distributed AI environments.

- Rise of software-defined storage and edge solutions for real-time analytics in IoT and 5G ecosystems.

- Focus on data security and cost reduction through AI-driven automation, predictive maintenance, and anomaly detection.

- Emergence of hybrid deployment models balancing on-premises control with cloud scalability for diverse workloads.

What Market Segments and their Subsegments are Covered in the Artificial Intelligence (AI) Powered Storage Market Report?

By Offering

- Hardware

- Software

- Others

By Storage System

- Direct Attached Storage (DAS)

- Network Attached Storage (NAS)

- Storage Area Network (SAN)

- Others

By Storage Architecture

- File-and-Object-Based Storage

- Block Storage

- Others

By Storage Medium

- Hard Disk Drive (HDD)

- Solid State Drive (SSD)

- Others

By End User

- Enterprises

- Cloud Service Providers/Hyperscalers

- Government Bodies

- Telecom Companies

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

The Artificial Intelligence (AI) Powered Storage Market involves storage solutions integrated with AI to optimize data management, performance, and security for AI/ML workloads, encompassing hardware, software, and systems like NAS and SSDs.

Key factors include rising unstructured data volumes, advancements in NVMe and flash technologies, hybrid cloud adoption, edge AI expansion, and the need for low-latency storage in AI training and inference.

The market is projected to grow from over USD 36.28 billion in 2025 to USD 321.93 billion by 2035.

The CAGR is expected to be 24.4% from 2026 to 2035.

North America will contribute notably, holding around 40% share due to advanced infrastructure and major tech investments.

Major players include Dell Technologies, NetApp, Hewlett Packard Enterprise (HPE), IBM, Huawei Technologies, Pure Storage, VAST Data, Samsung Electronics, Cohesity, Inc., and Cloudian, Inc.

The report offers comprehensive analysis including market size, forecasts, segmentation, trends, drivers, restraints, opportunities, challenges, regional insights, key players, and competitive strategies.

Stages include component manufacturing (hardware like SSDs), software development for AI integration, system assembly, distribution through vendors, deployment in end-user environments, and ongoing services like maintenance and upgrades.

Trends are shifting towards edge AI, hybrid deployments, and sustainable storage, with preferences favoring low-latency SSDs, automated management, and scalable solutions for cost efficiency and performance in AI applications.

Factors include data privacy regulations like GDPR impacting compliance, environmental concerns driving energy-efficient designs, and sustainability mandates promoting green data centers and reduced e-waste from storage upgrades.